Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Online Lenders Plummet Simultaneously to All-Time Lows

January 14, 2016 If it was involved in online lending, investors dumped it on Wednesday January 13th. LendingTree, a consumer lending platform, dropped nearly 30% for the day despite reporting positive results.

If it was involved in online lending, investors dumped it on Wednesday January 13th. LendingTree, a consumer lending platform, dropped nearly 30% for the day despite reporting positive results.

OnDeck closed at a new all-time low of $7.33, a drop of almost 14% for the day.

Lending Club also closed at a new all-time low. They finished at $8.86, after a comparably modest drop of 6.5%.

Enova International, the company that acquired The Business Backer back in August, closed at an all-time low. At $5.58, their stock dropped 3.13% for the day.

Square, a payments company with a substantial merchant cash advance operation, was down 4%, but they did not break the record for the all-time low they had just set six day earlier.

Yirendai, a Chinese peer-to-peer lender on the New York Stock Exchange, also managed to escape an all-time low despite being down 1.55%. Their all-time low record was also set just six days earlier.

For comparison’s sake, the S&P 500 was down 2.5% on the day. The continuous beating for online lenders, which can’t seem to catch a break in the market, is especially ominous because the economy is not in a recession and there are no indications that any of their business models are legitimately threatened. Nearly a decade since the beginning of the financial crisis, it’s apparently still cool to hate lenders. For LendingTree in particular, the precipitous drop on POSITIVE news was ugly enough to make the headlines in the New York Post. “LendingTree stock was sliced, diced, creamed and puréed,” the Post wrote.

Out there, the little guys who took a leap of faith to support fintech disruption seem like they’re preparing to riot in the streets:

$lc $ONDK ipo underwriters should be in prison

— TheMoneyTeamTMT (@TheMoneyTeamTMT) Jan. 13 at 03:42 PM

This is absurd $LC …this stock is either complete sh*t or we're going to have a monster rally

— Alex (@ROIRogers) Jan. 13 at 03:25 PM

$LC $ONDK new lows… starting to trade like a big recession is already here

— Mark Holder (@StoneFoxCapital) Jan. 13 at 01:42 PM

— BasicNews (@BasicNews) Jan. 13 at 11:49 PM

$SQ Here's another garbage company with bloated forward earnings, all these p o s stocks headed way lower

— QEBubble (@QEBubble) Jan. 13 at 05:18 PM

$LC F* this!

— Don Juan (@fluppy) Jan. 13 at 02:56 PM

$LC selling into oblivion. wtf

— Bork Bork (@calicat) Jan. 11 at 05:00 PM

Perhaps contributing to the damage in Lending Club’s case is that company executives have been dumping their shares over the last several months despite the stock constantly hovering near all-time lows. It certainly doesn’t show a lot of short-term confidence that something is going to change soon.

Insider selling is not the issue in OnDeck’s case which hasn’t really had any. While they were most likely just collateral damage from today’s unyielding carnage, Noah Breslow proclaimed on Squawk Box prior to the opening bell that OnDeck was regulated like a “non-bank commercial lender,” one of those rare characterization departures from their supposedly being a tech company. Aside from that was the sobering letdown that disrupting banks may have never been the goal for them or for online lenders. In a recent article by Broadmoor Consulting’s Todd Baker, he argued that “disruptor” has been the wrong word used to describe many of these companies and that their potential may only go as far as to digitally “enable” banks who are struggling with lagging technology to enable themselves in the modern era. Sound boring? Maybe there’s something bigger in play.

OnDeck and Bank Partnership Concept Debated on CNBC

January 13, 2016On CNBC’s Squawk Box, OnDeck CEO Noah Breslow responded to questions about why the fintech goal post of putting banks out of business has seemingly been readjusted. Breslow said that their mission all along has been to extend the market for credit, namely by originating small dollar loans (under $1 million) that banks can’t or have been unwilling to do. He supported that by saying that this market has always historically been underserved and is not just a consequence of the last recession.

More importantly though is the debate over whether or not banks should build, buy or partner with alternative lenders. (Hello marketplace Lending Hunger Games!) OnDeck believes their 8-year head start is an attractive reason as to why banks should “partner” with them.

On regulation, Breslow classified OnDeck as a “non-bank commercial lender,” which may be true from a regulatory perspective, but it’s a big departure from the sexy technology marketplace platform characterization that they’ve historically campaigned under.

Lastly, the OnDeck – JPMorgan Chase deal apparently does carry exclusivity and it is possible for them to engage in other partnerships.

Full video on CNBC below:

A Recession Could Turn Marketplace Lending Into The Hunger Games

January 13, 2016 When you don’t have the upper hand, one strategy is to partner up with opponents whose skills complement yours in order to compete with everyone else. But partnerships, while essential to self-preservation in an ultra competitive environment, are fleeting on the road to victory. When the field starts to narrow, it’s only a matter of time before truces are cancelled. The enemy of your enemy is your friend until they eventually become your enemy as well. Katniss Everdeen was not a lender last I checked, but her story is not so different.

When you don’t have the upper hand, one strategy is to partner up with opponents whose skills complement yours in order to compete with everyone else. But partnerships, while essential to self-preservation in an ultra competitive environment, are fleeting on the road to victory. When the field starts to narrow, it’s only a matter of time before truces are cancelled. The enemy of your enemy is your friend until they eventually become your enemy as well. Katniss Everdeen was not a lender last I checked, but her story is not so different.

Just last year, OnDeck partnered up with Chase while Fundation partnered up with Regions bank. Dozens of other “lenders” have partnered up in a different way with WebBank, Bank of Internet and Celtic Bank. Marketplace lending platforms that serve as centralized matchmakers have partnered up with hundreds of lenders and merchant cash advance companies. And Wells Fargo has had an arrangement with CAN Capital for what seems like forever.

Bank of America however, has vowed to fight on alone. According to the Wall Street Journal, BoA CEO Brian Moynihan “has no plans to partner with online or alternative lenders in part because of potential dings to its reputation.” Is that decision at their own peril?

While 2015 became the year of alternative lenders gushing about partnerships with banks (and that supposedly being the plan all along), Broadmoor Consulting Managing Principal Todd Baker relegated these alleged disruptors to a lesser status he refers to as “enablers.” Baker posits that OnDeck’s future for example, “may be brighter as a technology provider to banks than as a freestanding finance company subject to the vagaries of economic, credit, liquidity and regulatory cycles.” While perhaps not intentional, he seems to suggest that overtaking banks through technological innovation was unlikely and that alternative lenders are destined to a life of impotence, one that merely “enables” the competitors they were never going to beat.

Somewhere out there in the arena, Baker’s best friend Mike Cagney of SoFi is gearing up to win the 2016 Hunger Games. By openly admitting that banks like Wells Fargo and First Republic are the enemy, Cagney exhibits the ferocity one would expect of a tribute from District 2. SoFi has made nearly $7 billion in loans and wants their borrowers to leave their banks.

Behind the scenes, the Head Gamemaker is threatening to shower the arena with regulations and rising interest rates. While the alternative lending contestants partner up to ensure survival at least until the later rounds, there is potential trouble brewing in and around Panem, another recession. To hear most companies tell it, they would welcome a recession because they believe their models are built to withstand boom and bust cycles. Indeed, the atmosphere at Money2020 was exactly that, that it would be really convenient if the weak could hurry up and die already.

We should however consider that the consequences of a recession may go one step further and tip the scales of lending in a way that the “enablers” almost unwittingly become the new masters few now believe they’re destined to be. The Royal Bank of Scotland chief credit officer for example has already gone on record and told the public to sell bloody everything and prepare for the impending end of the world. 2016 will be a “cataclysmic year,” Andrew Roberts said. Fortune and Forbes have run less harrowing stories in recent days but warned that China, declining oil prices, and market signals indicate a recession could happen this year or the next. Reuters says we’re just facing a little thing called a “profit recession.” But whether these issues are false flags or indications of something more, an environment where credit once again becomes frozen in the traditional banking system could mean a suspension of partnerships between banks and alternative lenders. For alternative lenders that rely entirely on traditional banks for capital to begin with, the end for them will be swift and painful.

For those that don’t, let’s just say there’s a certain long-term advantage to being open for business when everyone else is closed. The merchant cash advance industry for example, which operated in an abyss between 1998 and 2008, suddenly awoke like a sleeping dragon during the Great Recession. In what is now a $7 billion/year industry or a $20 billion/year industry depending on how you define a merchant cash advance, the concept is now widely accepted as an alternative to traditional financing, even if at times criticized.

Foundation Capital’s Charles Moldow believes that “marketplace lending” will be a trillion dollar industry by 2025. “Consumers are fed up,” writes Moldow in his white paper. “Banks are no longer part of their communities. Rates are high for borrowers and not even keeping up with inflation for depositors. During the Great Recession of 2008-2009, when consumers and small businesses needed access to credit more than ever, many banks stopped offering loans and lines of credit.”

71% of Millenials would rather go to their dentist than listen to what banks are saying, according to Viacom’s Scratch. 33% believe they won’t need a bank at all in 5 years.

The presumption is often that banks will prevail in the lending tug-of-war anyway because they are more or less tasked by the federal government to be the arbiters of all lending activity. An economy where consumers and businesses regularly conducted their finances outside the purview of the banking system would be a nightmare scenario for a government that relies on the ability to monitor and control everything. Ergo alternative lenders should partner up with these banks, “enable them” and surrender to a future of impotence in which their only purpose is to serve their masters until perhaps one day the banks replace them with something else.

With alternative lenders still operating unfettered for now, today’s developing regulatory pressure would in all likelihood be traded for support in a recession, even if that support came in the form of willful ignorance.

If Millenials would already rather get a root canal than talk to their bank, then it’s probably not a good time for banks to become even less friendly, as would happen in a recession. The timing of one in the near future is almost to be expected considering how long it’s been since the last one, but the next one could be one of those transformative moments in history in which the world actually comes out looking a little bit different. Make no mistake, today’s alternative lenders are disruptive, they’ve just been playing the game rather safely. Partner up, work together, “enable” if they must, whatever it takes to ensure their survival into the later rounds. From student loans to consumer loans to business loans, 2016’s tributes are a force to be reckoned with.

There was only supposed to be one victor of the 74th hunger games, the banks. And there was always one until one year there were two. They surprisingly weren’t there to serve and enable their master either. The system that always was, was irreversibly disrupted.

The next recession could produce a similar outcome. Partnering with banks now seems like a great idea, but absent an actual merger or acquisition, they should be considered temporary alliances. You know what that means…

To the marketplace lenders and the technologies that power them, happy 2016! And may the odds be ever in your favor.

Online Lending IPOs Off to a Bad Start

January 12, 2016All the major stock indexes have tanked so far in 2016 but the new online lending stocks have really taken a beating.

OnDeck closed at $8.57 yesterday, near its all-time low. Investors, who originally appeared to have renewed interest after the JPMorgan Chase partnership announcement, have disappeared, even before details of the announcement emerged.

Lending Club and Yirendai have also plummeted. Meanwhile loanDepot cancelled their IPO altogether after concerns about the pricing environment in the public markets.

Hopefully the Elevate IPO is more elevated than the other disastrous online lending IPOs $YRD $ONDK $LC $ELVT #IPO pic.twitter.com/ffyrS9Dn54

— Renaissance Capital (@IPOtweet) January 11, 2016

Yirendai, a Chinese Peer-to-Peer lender that was spun off from CreditEase has gone nowhere but down in its first month. They had originally hoped to get a public valuation of $2 billion but instead came in at around $625 million.

Here is what some day traders are saying out there:

$ONDK Ondeck will probably double this year. While $LC is going to be highly challenged. Their market cap still too high.

— WingPuppy (@WingPuppy) Dec. 26 at 01:11 PM

$LC $ONDK These stocks have been left for dead, but fundamentals are great! Excellent sales, profit growth, and cheap. Like both for 2016

— Stanky Pigano (@StankyPigano) Dec. 23 at 01:23 PM

$ONDK Awful Business Model, lend at insanely high interest rate to "subprime" businesses, they cant pay because the rate is so high #deault

— Alex Baker (@abaker) Jan. 5 at 10:19 PM

How is $LC not a massive buy right now? It is trading at a 52 week low and at 50% of IPO.

— Kaz Nejatian (@CanadaKaz) January 7, 2016

Will online lenders change the mind of the public markets later this year?

Strategic Funding Source Acquires Tyrian Bull

January 11, 2016Tyrian Bull CEO Joshua Jones announced earlier today that their company had been acquired by Strategic Funding Source. Both based out of NYC, Tyrian posted across social media that their “clients and partners will be able to take advantage of more financing options, while still benefiting from the same standards of transparency and integrity they have come to expect with Tyrian Bull.”

Tyrian Bull’s website already displays a “POWERED BY STRATEGIC FUNDING” label in the footer.

Bernie Sanders is Probably Not the Marketplace Lending Candidate of Choice

January 6, 2016 Perhaps the fastest way for Americans to become deBanked is to elect Bernie Sanders as President. In a proposal he laid out on Tuesday, Sanders pledged to break up commercial banks, shadow banks and insurance companies that he believes are “Too-Big-to-Fail.” While not everyone would be especially sad to see something like that happen, there’s a whole bunch of other reasons Sanders might not be the marketplace lending candidate of choice.

Perhaps the fastest way for Americans to become deBanked is to elect Bernie Sanders as President. In a proposal he laid out on Tuesday, Sanders pledged to break up commercial banks, shadow banks and insurance companies that he believes are “Too-Big-to-Fail.” While not everyone would be especially sad to see something like that happen, there’s a whole bunch of other reasons Sanders might not be the marketplace lending candidate of choice.

Here’s a summary of what he said:

- The Business Model on Wall Street is Fraud.

- All consumer loans should have an interest rate cap of 15%.

- Lenders who charge more than 15% are awaited in the Seventh Circle of Hell.

- Quote: “Today, we don’t need the hellfire and the pitch forks, we don’t need the rivers of boiling blood, but we do need a national usury law.”

- Big banks need to stop acting like loan sharks and start acting like responsible lenders.

- Post offices should become government banks so that free market lenders will go out of business.

While Sanders admittedly said we don’t need the rivers of boiling blood, a large portion of lenders, marketplace lenders included, apparently have a special place in hell reserved for them. His over the top statements come on the heels of a gaffe, in which he revealed very publicly on twitter his ignorance over how loan underwriting actually works.

Will you be voting for Bernie Sanders this primary season?

Meet the Lending Platform With 0% Interest (Kiva)

January 6, 2016 Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Chany of Angela’s Boutique in Philadelphia, PA needs $5,000 to help purchase new signage and lighting to improve her storefront. She’s been turned down by banks even though she’s been in business for more than five years. 61 participants have already contributed to her loan thanks to a marketplace lending platform, which puts her very close to her goal. If it funds, all of the participants will get back their principal from her payments over the next 24 months and NO interest.

Meet Kiva Zip, the anti-Lending Club because the borrowers are far from anonymous and the yield delivered to investors is negative due to inflation.

Angela’s Boutique, which is a real prospect on the Kiva Zip platform, includes a picture of the owner, her bio, endorsements, and comments from supporters.

According to Jessica Feingold, Kiva’s East Coast Manager of Development, “Kiva is the world’s first and largest crowdfunding platform for social good with a mission to connect people through lending to alleviate poverty and expand economic opportunity.”

And just like Lending Club, contributions as small as $25 are accepted. Obviously structured as a non-profit, “Kiva and its growing global community of 1.2 million lenders has crowdfunded more than $775 million in microloans to over 1.7 million entrepreneurs in 83 countries, all the while maintaining a 98% repayment rate,” according to Feingold.

Normally thought of as an overseas endeavor, Feingold said that “in 2011, Kiva launched Kiva Zip, a pilot program in the US that provides 0% interest crowdfunded loans to small business entrepreneurs.” Their underlying purpose and target market sounds very much like those being served by for-profit alternative lenders. “Kiva doesn’t require a minimum FICO score, collateral, or a minimum operations period for the business,” Feingold said.

Since inception they’ve made loans to over 1,800 borrowers in 47 days states, Peru, and Guam.

Notably, Lending Club promises borrowers that their “identity will at all times remain confidential and not be disclosed to anyone,” according to their website. Kiva by contrast is looking to “instill empathy” in their lenders. “We want to show that whether in East New York or Uganda, underserved entrepreneurs are credit-worthy, and will pay you back,” Feingold said. “All of these features on the Kiva websites enhance our ability to do so.”

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

While there is definitely a certain allure about being able to see the borrower for yourself, the concept seems to fly in the face of Dodd-Frank’s Section 1071 which stipulated that lenders are prohibited from knowing the sex and gender of business loan applicants. While the CFPB is not currently enforcing the law until the rules can be clarified, Democratic members of Congress have been pushing them to take action.

According to the law, no loan underwriter or other officer or employee of a financial institution, or any affiliate of a financial institution, involved in making any determination concerning an application for credit shall have access to any information provided by the applicant about whether or not the business is women-owned or minority owned.

As small businesses often celebrate the heritage of their founders, and at times that can be the entire reason customers buy from them in the first place, the law has presumably put the small business lending world in an awkward position (and that’s why the law should be repealed). Non-profits like Kiva have embraced the very things that make a small business bankable outside of a credit score, like the owner, their background, and their story.

Borrowers on the Kiva Zip platform don’t raise all the money from strangers though. Their credit-worthiness is based on their ability to recruit friends and family to fund a small portion of their loan. The other lenders though of course may make their decisions based on the numbers or entirely on the perceived cultural, racial, or gender values of the borrower, all of the things that the CFPB is attempting to eradicate in the for-profit arena.

I didn’t ask Kiva any questions about Dodd Frank or Section 1071, but many people might empathize with their empathy approach as a way to fund small businesses that otherwise don’t qualify for bank loans. Its reminiscent of the subjective underwriting that a lot of alternative lenders and merchant cash advance companies employ to get deals done that banks won’t touch.

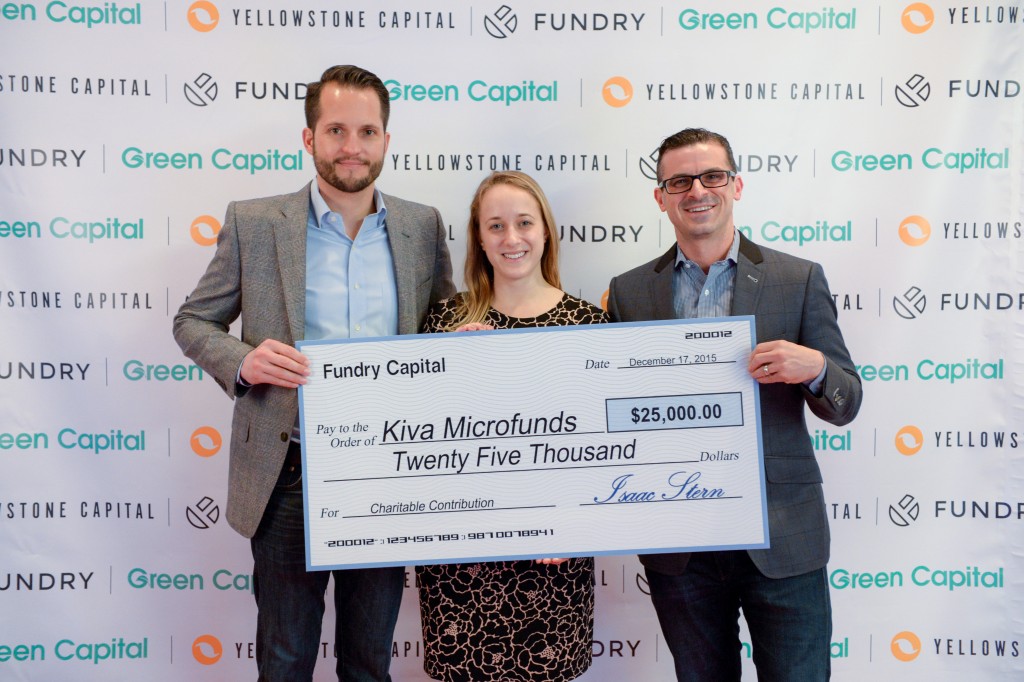

Not so coincidentally, Fundry, Yellowstone Capital’s parent company, donated $25,000 to Kiva just last month to support their cause.

Kiva’s Feingold (pictured at center above) said in regards to that, “Kiva is thrilled to receive a grant from Fundry to further our work to make credit more affordable.”

Invest in Marketplace Lending in 2016 (New Year’s Resolution)

January 4, 2016 The story of 2015, at least according to CNN, was that 70% of investors lost money. The big winners were apparently people that didn’t invest at all or those that took humongous risks. Millennials are notorious for being perpetually pessimistic about the stock market and headlines like these probably don’t raise their spirits. And while there’s nothing wrong with caution and skepticism, there’s really no reason that 2015 should’ve been a losing year, especially for such a large percentage of people.

The story of 2015, at least according to CNN, was that 70% of investors lost money. The big winners were apparently people that didn’t invest at all or those that took humongous risks. Millennials are notorious for being perpetually pessimistic about the stock market and headlines like these probably don’t raise their spirits. And while there’s nothing wrong with caution and skepticism, there’s really no reason that 2015 should’ve been a losing year, especially for such a large percentage of people.

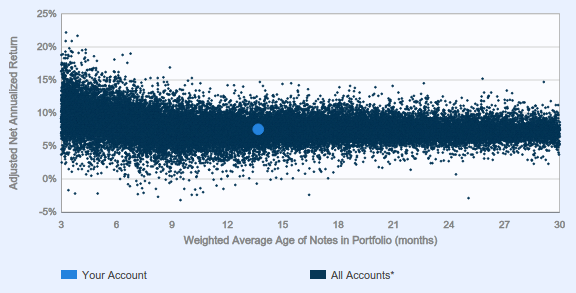

Peer-to-peer lending evangelist Peter Renton is earning more than 10% a year through his Lending Club and Prosper investments. And he’s not an anomaly. The majority of Lending Club investors are earning above 5%, including myself as shown below as the dot compared to everyone else:

After splurging on very high risk notes in 2014, I’ve since settled on a strategy of only A & B-rated notes for individuals making more than $85,000 a year. Since July of 2015, my notes have been purchased automatically by LendingRobot based upon the filters I’ve programmed in. Thus, marketplace lending has become a rather passive investment for me that runs in the background and it should for you too, especially if you work in the alternative lending industry.

In May and June of last year, we told you to break out of your bubble. If you didn’t heed those words, maybe the new year will give you the excuse you need to give marketplace lending some consideration.

Over the last two years, I’ve personally invested nearly $75,000 in consumer debt through Lending Club and Prosper, entirely in $25 increments. Suffice to say, I didn’t lose money on these in 2015. The monthly principal and interest payments from them are constantly reinvested into new loans on a daily basis, compounding my earnings. It definitely beats not investing at all, which is apparently what a lot of people did last year.

Even if marketplace lending isn’t for you, you can earn a few hundred basis points less per year with an FDIC guaranty. 5-year CDs are paying up to 2.42% right now. Back in June I wondered whether or not the risk undertaken with consumer debt was worth a few extra percent a year, especially considering how these notes are taxed (you may only be able to deduct up to $3,000 in losses per year).

I guess you could say that I decided it was worth it. My new investing strategy takes the $3,000 loss cap in stride because the number of A and B-rated notes (which are all I buy now) that default are very low. In fact, I’ve never even had an A-rated note default in the two years I’ve been investing.

The one disclaimer I will add is that I did indeed invest more money in mutual funds (stocks) in 2015 than I did in marketplace lending. While I enjoy the reprieve from daily volatility that Lending Club and Prosper notes bring, it’s important to never lose sight of the fact that those investments are ultimately in Lending Club and Prosper themselves. Originally envisioned as peer-to-peer, both companies actually just issue bonds to investors that are backed by nothing other than the performance of chosen loans. So if Lending Club and Prosper blew up tomorrow (or worse), it might not matter how all those loans were performing. If the secret to investing is to diversify, then you should treat your total investment on a marketplace lending platform as if it were a single stock. That’s precisely why I won’t open an IRA with Lending Club or Prosper, even if the tax advantages would be better.

Nevertheless, as my mutual funds were flat for the year, my marketplace lending portfolio pushed me forward. At the very least I plan to reinvest all the payments from my portfolio this year into new notes on a daily basis. If you were discouraged by the headlines that 70% of investors lost money last year, you should consider complementing your stock portfolio with marketplace lending this year.

Consumer debt might seem like an odd choice for an individual to invest in, but once you get the hang of it, you’ll eventually consider it to be an integral part of diversification.