Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Need Capital for Your Funding or Lending Company? 3Jane Does it On Blockchain

July 27, 2026“I’m a big believer in agentic capital markets. I think we’re going to see a Cambrian explosion of novel primitives, driven largely by two pieces. Today, it’s just very easy to construct arbitrary financial building blocks using smart contracts,” said Jacob Chudnovsky, Founder of 3Jane, to deBanked.

3Jane provides credit facilities and forward flow arrangements across a range of products, including consumer loans, small business loans, and even merchant cash advances. The company previously provided a $10 million senior warehouse facility to consumer lender LendSwift, for example, and followed that with an inaugural $8.5 million purchase of small business loans from Slope, an embedded credit infrastructure provider that powers business lending programs for major players across the US, including Amazon. According to Chudnovsky, 3Jane would like to do even more deals in the small business lending and MCA space.

But with a twist.

3Jane has built an entire protocol on the blockchain. It offers a credit-backed “yieldcoin” that earns its yield “from warehouse facilities, forward-flow programs, and credit-lines.” Investors can mint the coin on Ethereum, and it earns a yield backed by the performance of 3Jane’s credit assets. Minting is not open to US investors, but the company’s capital markets offerings are focused exclusively on North America. So, if you’re a small business funder seeking a credit facility or forward flow arrangement, 3Jane wants to speak with you.

3Jane has built an entire protocol on the blockchain. It offers a credit-backed “yieldcoin” that earns its yield “from warehouse facilities, forward-flow programs, and credit-lines.” Investors can mint the coin on Ethereum, and it earns a yield backed by the performance of 3Jane’s credit assets. Minting is not open to US investors, but the company’s capital markets offerings are focused exclusively on North America. So, if you’re a small business funder seeking a credit facility or forward flow arrangement, 3Jane wants to speak with you.

Chudnovsky is a software engineer by trade and entered the DeFi space in 2020.

“…around 2024, I basically came to the realization that credit is still an extremely underdeveloped vertical in crypto and particularly both the capital aggregation and the capital distribution side of it,” he said. “My initial focus was ‘can we get the best of crypto to distribute capital in a better way?’ and so I founded 3Jane, and we started off by doing unsecured lines of credit for crypto users in the United States who had a bunch of these different assets and could not really borrow against it in a streamlined way.”

That effort eventually led to 3Jane’s current business model. If the name 3Jane sounds familiar, it’s because Chudnovsky drew it from the 1984 novel Neuromancer, the famous William Gibson book that coined the phrases “cyberspace” and “the matrix.” By pure coincidence, Apple TV is releasing a 10-episode series based on the book in January 2027.

That effort eventually led to 3Jane’s current business model. If the name 3Jane sounds familiar, it’s because Chudnovsky drew it from the 1984 novel Neuromancer, the famous William Gibson book that coined the phrases “cyberspace” and “the matrix.” By pure coincidence, Apple TV is releasing a 10-episode series based on the book in January 2027.

“I just think we’re going to enter this complete renaissance of new different financial primitives and I think it’s going to drive a lot of adoption, new ways of thinking about our financial system and that sort of really resonated with me with the book,” Chudnovsky said.

And that new way of thinking is starting to take root. The capital markets utilizing blockchain to create efficiencies is already cropping up around the industry. Since 3Jane last spoke with deBanked, its purchase of embedded finance products from Slope has increased to a total of $60 million.

3Jane’s customers do not need to be crypto experts. The company handles that side of the transaction while underwriting the risk and executing what is otherwise a conventional capital markets deal, but one in which the infrastructure is robust enough that this can be a lender’s first and last facility. On 3Jane’s part, doing this requires a strong understanding of the various financial products it evaluates, including MCA.

“…there are a number of MCA operators in the United States that are doing things right, they’re growing significantly and they need leverage to scale their business,” Chudnovsky said. “and so warehouse facilities and to a lesser extent forward-flows for MCAs sort of equally make sense for them as long as you are cognizant of the risks.”

It’s Live, You Can Now Invest in a Credibly Warehouse Line Through Figure

July 21, 2026 IT’S LIVE. Less than two months after Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails,” investors big and small are now able to share in the earnings of a Credibly business loan warehouse line.

IT’S LIVE. Less than two months after Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails,” investors big and small are now able to share in the earnings of a Credibly business loan warehouse line.

Specifically, Credibly boarded a business loan portfolio on July 21 and can already borrow against it using Figure’s Democratized Prime. Investors can now effectively participate in the earnings of that line by lending their own money into the pool. The amount of capital contributed to the pool and the utilization rate of it play a big role in the yield generated from that. Investors can pull out of the pool at any time assuming there is liquidity available to do so.

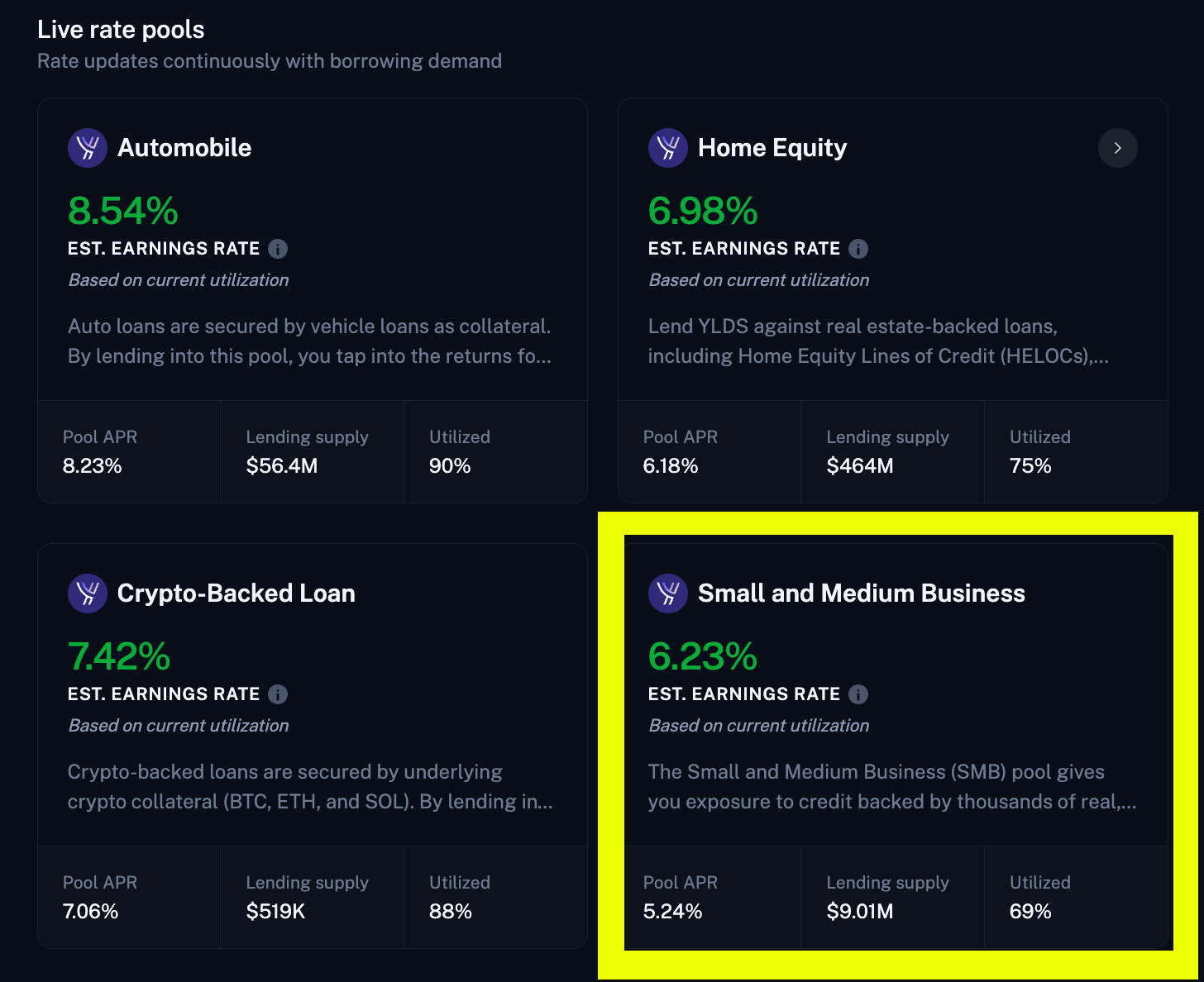

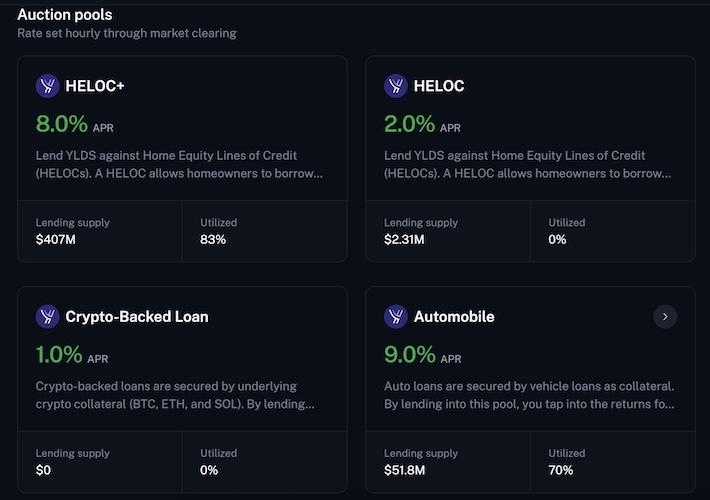

Unlike most investing platforms, investors can only participate in this one using blockchain rails (as was explained in deBanked’s May 23 story). Investors fund their accounts using dollars, crypto, or stablecoins, convert them into Figure YLDS tokens, and then lend those tokens into any number of available pools. As of the time of this writing investors can participate in HELOCs, auto loans, crypto loans, and now “small and medium business loans” which at present is sourced from Credibly. This all takes place on the Provenance blockchain and can all be easily conducted through the Figure Markets mobile app. deBanked was able to execute this process with no issues while using the investor side of the platform.

The investing opportunities on Figure’s Democratized Prime are warehouse lines for institutional-grade portfolios so investors are likely to see returns that resemble warehouse line rates (versus what one might expect if they do direct syndication with mom & pop lenders/funders). Credibly stands to benefit in the long run by the likelihood of lower borrowing rates and costs versus other capital market options and then being able to pass those savings onto their customers.

Investors will see some stats for the inaugural small and medium business loan pool which looked like this at the time of this writing:

The page also offers this information:

The Small and Medium Business (SMB) pool gives you exposure to credit backed by thousands of real, vetted American small businesses. The receivables represent payments owed by operating U.S. businesses. By lending into the pool, you earn from the cash flows those businesses generate as they repay their financing obligations. Backed by institutional-grade small-business credit, the SMB pool provides yield generated by a tangible, collateralized asset class, and a new way to diversify your portfolio.

Risk parameters

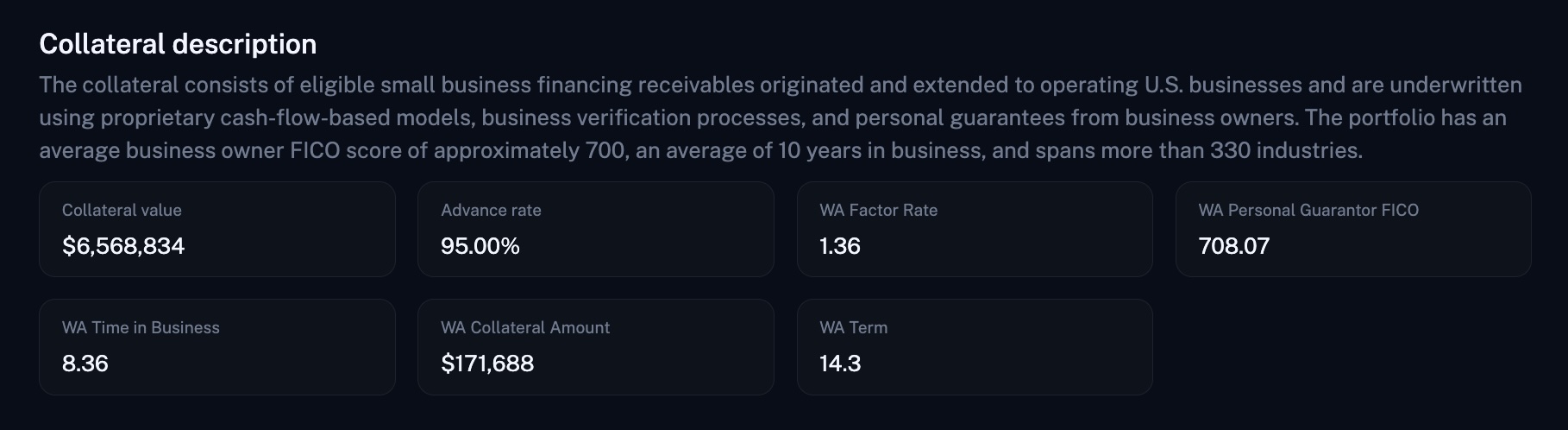

Democratized Prime manages risk through a structured financing facility backed by a diversified pool of prime small business financing receivables. The facility benefits from multiple layers of credit enhancement ensuring the pool can absorb a variety of adverse conditions before depositor yield is affected. This is enabled by a variety of mechanisms, including a 95% advance rate cap, reserve account funding, overcollateralization, originator repurchase obligations, and full recourse provisions. All receivables included in Democratized Prime must satisfy established eligibility requirements and be performing at the time of inclusion.Collateral description

The collateral consists of eligible small business financing receivables originated and extended to operating U.S. businesses and are underwritten using proprietary cash-flow-based models, business verification processes, and personal guarantees from business owners. The portfolio has an average business owner FICO score of approximately 700, an average of 10 years in business, and spans more than 330 industries.

The author contributed $5,000 in YLDS tokens into the Small and Medium Business loan pool on his own volition prior to the publication of this article for test purposes.

American Brokers Help Fuel Canada’s Small Business Finance Boom

July 10, 2026 Canada’s small business finance industry is growing, and behind the scenes, American brokers are helping fuel that momentum.

Canada’s small business finance industry is growing, and behind the scenes, American brokers are helping fuel that momentum.

“They’re kind of killing it here right now, from what we see from the partners that we work with,” said Vlad Sherbatov, President & Co-founder of Smarter Loans, an online lending marketplace in Canada. “…for the American players that have come in, they’re already really good at the broker channel.”

Some Canadian small business funders, particularly those offering an MCA product, told deBanked that a significant amount of deal volume is coming from south of the border. And with that, the environment and culture of the business itself is beginning to shift. In their view, it is becoming more Americanized.

“…a lot of the Americanization of the industry, if you will, is coming from US brokers and funders,” said Avrohom Bernstein, CEO at 2M7 Financial Solutions.

Part of that shift is a new level of competition among firms as brokers try to maximize the options available to their clients. Bernstein, for example, said it often starts with an American broker inquiring about submitting a few Canadian deals. Lately, however, it’s been escalating into situations where eight different brokers might submit the same clients.

“Every deal now you’ve got to hustle, you’ve got to fight, you have to really work it,” Bernstein said.

That competition once meant fighting to become the one and only exclusive partner for a merchant. Now, it has become more common to find that a submitted applicant already has multiple active advances.

“…that used to be unheard of in Canada, like that used to be excessively unusual to see more than three positions, now ten is not insane anymore,” said Bernstein. “It really escalated in a way that we haven’t seen, and that’s probably over the last 12, maybe 24 months, that it started really picking up,” Bernstein said.

Jodi Levy, Head of Sales and Business Development for BizFund in Canada, said she has made a similar observation. When she first started in the industry there, something like a third position was unheard of. Now, she said, they see it much more often.

“I feel like that’s definitely more an American influence,” Levy said.

BizFund has a large American operation as well, so the company is no stranger to how things work on the other side of the border. But like others, its Canadian funding arm also works with the American broker community.

“…partners are great, American, Canadian, we don’t care where you’re from, as long as you’ve got good business,” Levy said, adding that what matters is whether those partners have a direct relationship with their merchants. She also said that working with the broker community requires operating with a sense of urgency, something she has instilled in her team as a culture of NOW.

The diversity of products brokers can offer may not be as wide as what is available in the US. Sherbatov said that once a business steps outside of traditional banking sources, it is essentially entering MCA territory. As a result, much of the new competition entering the space is focused there.

“Among the new players that have come in, MCA is definitely the product that they’ve been leading with,” Sherbatov said.

“We have like five or six banks, and then like a couple credit unions, and then there’s not really anyone between, and there’s A-paper guys, and then B, C, D type of guys,” said Bernstein of 2M7.

According to Statistics Canada, banks provided 68.5% of all capital to SMEs in 2023, while credit unions and government institutions provided 20.6% and 9.4%, respectively. Only 2.2% was funded by “online alternative lenders.” The total market size at the time was estimated at $94 billion.

“I think the big gap is—there’s tons of businesses that want capital,” said Rafael Rositsan, CEO and co-founder of Smarter Loans. “There are some funders that offer it, but they’re pretty tight, and I feel like if somebody can come in and take on a bit more risk and open up their books a bit, then there’s plenty opportunity to fund a lot of Canadian businesses.”

As for why there has been such a push from Americans into Canada, no one pointed to a single definitive reason, but the runway for growth in the alternative lending segment, as illustrated by the report, may provide a clue as to the interest. Bernstein of 2M7 said there has long been a pattern of Americans entering and exiting the Canadian market, but he had also long believed that sustained success required boots on the ground. Now, he is reconsidering that view, at least on the broker side, as the current wave of broker entrants appears to be holding more firm. For funders, however, he said it still does not really work as a remote business.

As for why there has been such a push from Americans into Canada, no one pointed to a single definitive reason, but the runway for growth in the alternative lending segment, as illustrated by the report, may provide a clue as to the interest. Bernstein of 2M7 said there has long been a pattern of Americans entering and exiting the Canadian market, but he had also long believed that sustained success required boots on the ground. Now, he is reconsidering that view, at least on the broker side, as the current wave of broker entrants appears to be holding more firm. For funders, however, he said it still does not really work as a remote business.

“Every funder that’s actually doing decent volume is here, except for one,” Bernstein said.

In 2019, deBanked held a conference in Toronto for what was then a burgeoning small business finance industry, but held off on further events there after Covid disrupted plans for 2020 and 2021. It did not go unnoticed, however, that deBanked’s more recent American-based events have had more email addresses ending in .ca on the attendee lists. At the most recent Broker Fair conference in New York City, for example, some firms were exclusively advertising Canadian funding products to American brokers.

Canada’s population is relatively small, at roughly 41 million residents. That is about the size of California and only 25% larger than Texas. Homegrown Canadian brokerages do exist, of course, and a lot of business in Canada stays within Canada. Not all of the deals are originating through brokers either. Some merchants prefer to work directly with a funding source, while others prefer the comfort of applying through a Canadian lending marketplace like Smarter Loans, for example. If a merchant is ultimately eligible for some kind of funding, Sherbatov said, they are going to know it through their platform.

“We love the fact that we can help the small business economy thrive in the country, it’s responsible for a lot of positive things,” Sherbatov said. And whether the funding sources originate from Canada or the US, he said those companies ultimately find their way to them.

“We’re just becoming a more critical part of that journey for the merchant, and I think that explains why a lot of the new companies, when they come in, they gravitate toward us,” said Sherbatov. “…because in the business financing space we’ve carved out a nice niche for ourselves after Covid, and usually the new players gravitate to us because they know that merchants come to us as well.”

Levy of BizFund said part of the Canadian business experience is kindness. “That stuff goes far, we love that stuff up here in Canada,” she said. On the company website, photos of the company’s team, including Levy, show them smiling and ready to fund businesses.

For stalwarts like 2M7, which launched in Canada in 2008, the market’s evolution has been dramatic. Bernstein said the industry has gone from being a bit quiet and under the radar to seeing a lot of energy recently, whether from American brokers or from Canadian brokers that have decided this is the niche they are going to focus on entirely.

“In the US, I know a lot of brokers who also do equipment and also term loans and also SBA and also all this other type of stuff, it doesn’t exist so much in Canada,” Bernstein said. “It’s like if you’re selling to small businesses and you’re offering them financing, there’s not that many products you could line up, so it’s like if you’re doing brokerage, you got to be all in, like if you’re doing MCA, you got to do MCA.”

“I think that it was evident to a lot of players outside of the market that there is a big market opportunity that’s untapped,” Sherbatov said, “just because so little financing is being released by alternative lenders, that they started to come into the space, and we’ve seen, I mean, not even for the past two years, but I’d say in the past 18 months, our own roster of business lenders on Smarter Loans has doubled, like we went from 10 to where now we have 20, and the majority of that expansion actually happened from US players coming into the country.”

And the growth is just getting started.

“There’s a lot more room for it,” said Rositsan of Smarter Loans.

Serial Litigants May Target Websites and “Trackers” As Alternative to TCPA

June 12, 2026![]() The small business loan brokerage had played it safe. Rather than robodial and take their chances in the minefield of TCPA compliance, they ran ads on Facebook and Instagram and had the merchants call them. Inbound leads were gold, they cheered, until one of those inquiries came through a little differently. It was a demand for damages for having been tracked on the internet.

The small business loan brokerage had played it safe. Rather than robodial and take their chances in the minefield of TCPA compliance, they ran ads on Facebook and Instagram and had the merchants call them. Inbound leads were gold, they cheered, until one of those inquiries came through a little differently. It was a demand for damages for having been tracked on the internet.

The merchant alleged that they had only been served ads on social media by that company because they had been tracked from a prior website visit. They hadn’t wanted to be tracked and there was no option to opt out of tracking. As a result, they demanded to be compensated, heftily.

By now, most internet users have at least heard the term GDPR, the General Data Protection Regulation that became a never-ending source of controversy throughout Europe, but not all are aware that states and litigants in the US have tried to create a similar framework for privacy. For some in the small business finance industry, the vast complexity of compliance was not fully understood until the lawyers came calling.

“Pretty much every MCA company is potentially a victim because they’re all doing advertising,” said Richart Ruddie, CEO of Captain Compliance, a firm that specializes in safeguarding companies against these sorts of threats. “What we do is we protect against the rise and surge in privacy lawsuits and privacy litigation. So, anybody running TikTok ads, Facebook ads, Instagram ads, any sort of technology that does session-replay where it watches you move the cursor on the screen, if they’re running Google Analytics, all of these are cases that have been tried and are being litigated over.”

Ruddie said that companies within the small business finance industry, including a few within the segment of MCA, have been hit with claims, and they’re now actively working with them to make sure it doesn’t happen again.

“What our software does is provides the ability for users to have consent to opt-in or opt-out of any sort of ad targeting, tracking, session-replay technology,” Ruddie said. “And then we also provide software that constantly keeps businesses’s privacy notices and privacy policies up to date with their tracking and what they’re doing as well as their data handling practices.”

“What our software does is provides the ability for users to have consent to opt-in or opt-out of any sort of ad targeting, tracking, session-replay technology,” Ruddie said. “And then we also provide software that constantly keeps businesses’s privacy notices and privacy policies up to date with their tracking and what they’re doing as well as their data handling practices.”

The larger issue is that for companies that might already be aware of the risks, the solutions they’re using may not actually be compliant with the laws.

“What’s happening now is there’s a handful of these cookie banner softwares but they don’t work and they’re creating bigger issues because they’re like ‘Hey, you told me I could opt out, and then I turned off the selling and sharing of my personal information and you still track me,'” Ruddie explained.

This is made all the more complex by the fact that there are nearly two dozen states with their own twists on compliance. And a growing cottage industry of serial litigants that know this complexity could make website operators easy targets to profit off of. For instance, some of them are going around and running automated website scans just to see who to target. Ruddie said that he’s seen claims reach into the tens of thousands or hundreds of thousands of dollars for alleged privacy violations.

Preventative measures are within reach, however. Ruddie says that for a brand new customer they can get a company compliant in one to three business days. It’s hard for companies to hide in the shadows if they’re online because it doesn’t take much to see what’s there and what isn’t.

“You can right-click and look at the code and then you can see all the different tech and what’s running on the website,” Ruddie said.

Soon, You’ll Be Able to Lend Against Credibly Small Business Loan Pools

May 23, 2026For most people in the small business lending and revenue-based financing industry, news of a billion-dollar securitization barely resonates. It’s too big, too abstract, especially if you’re used to the ground game of syndicating a couple million bucks in deals you handpicked with funders you personally know. Wall Street-level capital markets has always felt like a mysterious private club, where a hundred million here and a billion there changes hands through an old-fashioned system outsiders hardly ever get to see, aside from the press release that later announces a deal happened.

But something recently changed. Capital markets, at least a corner of it, is being democratized. That became obvious when someone told me I could lend a hundred bucks toward a warehouse line of credit for Credibly just to see it for myself.

Me? Somehow involved in a warehouse line for Credibly???

On May 5, Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails.” It sounds like a buzzwordy headline from the 2010s. Not AI, blockchain. In 2026. Though there are certainly AI technologies involved.

Figure is a familiar name, not only because it is publicly traded, but also because I had the honor of sharing a stage with Figure CEO Michael Tannenbaum last fall at the B2B Finance Expo in Las Vegas for a fireside chat. While I mainly asked him about how small business owners could leverage their home equity to obtain capital, Tannenbaum pivoted at moments to explain how the company was reshaping capital markets by using blockchain. At the time, some of it went over my head.

“Everybody else is trying to use an origination system, and then on the back end figure out where to sell the loan,” said Tannenbaum on Peter Renton’s recently released Fintech One-on-One podcast, “and that figuring out process creates all this back and forth between the lender, the borrower, and the ultimate buyer, and we eliminated that, and we eliminated the people-based approach and standardized it.”

In a nutshell, Figure being in the mortgage game meant it was inevitably tied up in the capital markets game. And they found the capital markets game very old-fashioned. So they made their own capital markets marketplace, with one segment called Democratized Prime, and built it on blockchain rails.

Democratized Prime is essentially like a universal warehouse line, one that is “much easier to borrow and lend against than the arduous process of getting a warehouse line with lots of third-party diligence and legal fees,” Tannenbaum told Renton. It has rapidly become popular for mortgages. If you signed up for the platform today, you would see HELOC pools and their corresponding credit profiles that you could lend against.

Mortgages were just the start. You can also lend against an auto loan pool brought on by Agora. That deal was announced this past February as a landmark moment that kicked off the democratization of new asset classes. Credibly will bring SMBs into the mix next, where the company’s small business loans and revenue-based financing deals will be pooled up and available to lend against with as little as $10 at a time. That means this opportunity is open to just about anybody.

The yield can be determined in one of two ways. One is a Dutch auction, where participants compete to lend into the pool by offering lower rates, which is good for Credibly as the number goes down. If you bid too high or the pool is full, you may have to wait until the next hourly auction to try again. The process resets each hour, with the lowest acceptable bids getting priority, meaning lenders are not just deciding whether they want exposure to the pool, they are also competing on price for the right to put their money to work. The other is a live-rate system where rates change automatically based on utilization. You can exit an auction pool if your funds are not in use or if someone else’s funds are ready to replace yours. For live rates, you can request an exit up to the available liquidity at the time. Credibly is not on the Democratized Prime system just yet. That is supposed to happen this quarter. But HELOC and auto loan pools are already there.

I first tried the platform myself with just a couple hundred bucks. I entered digits into an auction-pool form indicating that I’d be willing to lend at 7.9% APR all-in to a HELOC pool. The pool wasn’t taking any offers for higher than 8% so that’s how I came up with my figure. My funds were accepted, and they’re now earning a return. Not in some magic back room, but visibly on the blockchain.

While you can obviously fund your account with dollars, I dusted off an old stockpile of ETH and sent funds using MetaMask to Figure Markets. Therein lies the only caveat. To lend against the pools, you have to use Figure’s stablecoin, YLDS.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS exists on the Provenance blockchain. You’re assigned a wallet address, and you can trace where your funds went using Provenance’s main block explorer, ZoneScan. That also lets you see a bit of what other users are doing, as well as what Figure is doing. By being on blockchain rails, everything is kind of out there for audit and inspection. I saw my ETH get swapped for YLDS on the block explorer and then saw my funds interact with a corresponding HELOC pool smart contract.

If you think this blockchain stuff is still niche, consider that in 2025, stablecoins processed $28 trillion in real economic volume, according to Chainalysis. By 2035, that number could reach $1.5 quadrillion, surpassing today’s entire cross-border payments market. Those are eye-popping numbers, but even if one discounts the forecast, the broader point is hard to ignore: stablecoins are no longer a fringe experiment.

Of course, this is not risk-free just because it is transparent. Pool performance still matters. Borrower credit quality still matters. Liquidity may depend on whether other participants are ready to replace your funds. And because YLDS is itself a security, participants need to understand what they are holding, how it works, and what risks come with using it. The blockchain may make the mechanics easier to inspect, but it does not make credit risk disappear.

While Democratized Prime can make it easier for lenders to tap into capital, this also is not a solution for everyone. Credibly, for example, has provided access to over $3 billion in working capital to more than 61,000 small businesses, with four completed KBRA-rated securitizations, its most recent one completed in the first quarter of 2026 for $124 million, expandable up to $225 million. That is sort of the baseline quality: true institutional-level assets from an institutional-tier lender. A small funder looking to graduate away from syndication is not going to be an immediate candidate for something like this. One of the HELOC loan pools, for example, has taken in $340M from parties looking to lend their YLDS.

One benefit for Credibly in challenging traditional finance ABS markets and adopting this technology is that greater efficiency and reduced friction should ultimately enable the company to pass savings on to its small business customers.

Would you lend a million dollars against a Credibly business loan and revenue-based financing pool? Before now, you probably wouldn’t ever have had that opportunity. Now Figure is making that possible.

Barney Frank Once Answered My Question About Business Loans

May 20, 2026 Former Congressman Barney Frank has died. He was 86 years-old. While he left Congress in January 2013, his legacy has lived on through the Dodd-Frank Act of 2010. Readers may recall that’s the law that gave birth to the Consumer Financial Protection Bureau and with that a debate that has spanned more than 15 years over how to implement its small business loan data collection mandate.

Former Congressman Barney Frank has died. He was 86 years-old. While he left Congress in January 2013, his legacy has lived on through the Dodd-Frank Act of 2010. Readers may recall that’s the law that gave birth to the Consumer Financial Protection Bureau and with that a debate that has spanned more than 15 years over how to implement its small business loan data collection mandate.

In any case, I once personally crossed paths with Congressman Frank in a hallway at the Exponential Finance Conference presented by Singularity University and CNBC. It was in 2014 and I had official press credentials. I had limited time so I fired away the first question I could think of and that was “would you be in favor of a federal maximum cap on business loan interest rates?” He said that he would not be.

Talking further about this subject, Frank went on to say that he supported transparency in business loan transactions, such that the borrower should be easily able to identify the terms, but that the premise behind consumer loan protections was that consumers were less sophisticated.

In a second question, I brought up overdraft fees and their tendency to be characterized by critics as short-term loans. Should a loan term of just a single day be required to disclose an annual percentage rate? He believed that they should.

This exchange and a summary of topics discussed at the conference appeared in the July/August 2014 issue of DailyFunder’s periodic trade journal. RIP Congressman Frank.

Got Hit By The IEEPA Tariff? There’s a Company That Will Help Get Your Cash Back From It

May 5, 2026 On February 20, 2026, the Supreme Court of the United States ruled that the Trump Administration could not impose tariffs on imported goods under the International Emergency Economic Powers Act (IEEPA). While the President immediately pivoted to enforce tariffs under a different legal basis, many people began to wonder what would happen with the billions of dollars already collected from importers.

On February 20, 2026, the Supreme Court of the United States ruled that the Trump Administration could not impose tariffs on imported goods under the International Emergency Economic Powers Act (IEEPA). While the President immediately pivoted to enforce tariffs under a different legal basis, many people began to wonder what would happen with the billions of dollars already collected from importers.

Aharon Margolin, the CEO & Founder of Tariff Recovery Group, told deBanked that the court ruling was brought to the Court of International Trade (CIT) to determine next steps, and on March 4 it was decided that all importers would be refunded the IEEPA tariffs. It’s a lot of dough, approximately $166B. $55B of that is attributed to more than 236,000 small businesses that are now due a refund, and by all accounts it seems like the system is working with haste to handle this.

“They’ve actually outlined the process to start facilitating these refunds,” said Margolin, “and they even opened up a portal on the Customs Border Patrol (CPB) Website for importers to start to file their refunds.”

But a portal means paperwork, and a refund comes with the unknown of when it will be received. The CPB, for example, has announced that the first refund will be issued on May 11, which is less than a week from now, but is advising that they’ll generally take 60–90 days from the time a claim is filed. Small businesses have heard such speedy promises before, with the Employee Retention Credit (ERC), for example, and ended up waiting far longer than they ever could have anticipated.

But even if all parties move quickly, the Trump Administration has the option to appeal the CIT refund order and potentially cause a stay of the refund process altogether. This kind of delay or any prolonged delay could result in claims eventually getting denied entirely because of normal deadlines to protest tariffs. If businesses don’t file or protest the tariff in a timely manner, for example, the window to get refunded could simply close. Would they let that happen? No one knows for sure.

Similar to previous government programs, not everybody is aware of what is happening, what they’re even supposed to do, or if they’re supposed to do anything at all.

“…a lot of these merchants, I’m sure don’t even know they’re entitled to a refund,” said Margolin. “A lot of them are, and I think specifically the subset of the merchants that are turning to the the alternative funding industry are because they need that help.”

Margolin echoed what the rest of the small business finance industry was saying before the SCOTUS ruling: that applicants were often citing tariffs as being disruptive to their supply chains, generating demand for working capital solutions from a variety of sources, including products like MCAs. Margolin said the easiest cash flow solution would be for businesses to first get the tariff refund money that is actually owed to them. But that’s subject to the 60–90 day wait in a best-case scenario and an unknowable amount of time in a worst-case scenario.

What then if the need is urgent? That’s where Tariff Recovery Group comes in. They assess how much a business is owed in tariff refunds and can then work out a deal to pay the business cash upfront.

“It all depends on the nature of the claim,” Margolin said. “We’re able to liquidate that claim for money upfront right here, which could provide significant cash flow relief and working capital to the business.”

In his experience, many business owners aren’t even aware of exactly how much they paid in IEEPA tariffs. Because of that, they first assess all of their history and, if eligible, give them all the materials, deadlines, and instructions to file a claim. The business could simply stop there and use that as a standalone service or proceed to the next step, which is to sell the refund claim to Tariff Recovery Group.

Given all the moving pieces, certain unknowns, and the benefits of acting swiftly, Margolin’s company is hoping to educate as many people in the small business finance industry as possible, especially those who would normally just pitch loans or other solutions to their clients. They can also offer a tariff refund filing service or turn those refunds into cash upfront by referring those businesses to him.

“There’s a real service that you could be offering them, they could be getting real money back,” Margolin said. “There’s real commission to be made by brokers.”

Brokers can make commissions by referring businesses to go through the assessment with Tariff Recovery Group and file a claim, and then earn another commission if the business owner sells their claim. It’s, at the very least, a tool in the arsenal to provide a helpful service.

“The worst thing to hear is that a small business paid these types of tariffs and is not recovering them, that would just be money left on the table,” Margolin said.

What the Velocity Capital Group Announcement Revealed

April 21, 2026 Velocity Capital Group has deployed over $1 billion to small businesses, newly unveiled financial stats show, shedding light on the firm’s performance as it enters a new phase of institutional-scale expansion. Across more than 10,000 transactions, VCG reports a 37.1% renewal rate and a sub-10% default rate.

Velocity Capital Group has deployed over $1 billion to small businesses, newly unveiled financial stats show, shedding light on the firm’s performance as it enters a new phase of institutional-scale expansion. Across more than 10,000 transactions, VCG reports a 37.1% renewal rate and a sub-10% default rate.

The firm says it operates in all 50 states and is actively preparing to extend its model globally, with origination volumes projected to continue accelerating through 2030. As part of that, VCG has hired Michelle Melo as Director of Financial Operations & Capital Markets.

deBanked has been covering VCG’s expansion since 2018, starting with a profile that captured CEO Jay Avigdor’s rise from solopreneur to a large office on Long Island. At the time, Avigdor told deBanked: “We crawl before we walk before we run.” The company now appears to be in a full sprint as it looks globally.

This past February, Velocity Capital Group’s booth at deBanked CONNECT MIAMI included a surprise guest appearance from NBA All Star Bam Adebayo. Now with its recent big hire of Melo, Avigdor says, “VCG’s tech- and data-powered platform is scaling faster and more efficiently than nearly any peer in our category, and Michelle is here to institutionalize that advantage. She will drive pre-securitization discipline, standardized reporting, and the investor relationships we need to remove scaling friction and enable the next generation of growth. With Michelle on board, VCG is significantly closer to achieving our target of $1 billion in annual originations.”