1st Global Capital Sues Capital Stack and Others Over Momentum Auto Group

December 18, 2018 The notorious $40 million merchant cash advance deal has a new twist, even more cash advances. On Friday, the now-bankrupt 1st Global Capital filed a lawsuit against Momentum Auto Group, related entities, and 4 merchant cash advance companies including Capital Stack.

The notorious $40 million merchant cash advance deal has a new twist, even more cash advances. On Friday, the now-bankrupt 1st Global Capital filed a lawsuit against Momentum Auto Group, related entities, and 4 merchant cash advance companies including Capital Stack.

According to documents filed in the case, Momentum Auto was behind on taxes and loans to floor plan lenders to the tune of $15.5 million in February this year. That’s in addition to their inability at the time to pay 1st Global Capital and other MCA funders millions of dollars in advanced funds.

To fix the problem, 1st Global Capital established themselves as the senior creditor in which they required rival funders to enter into Subordination And Standstill agreements. In return for 1st Global Capital keeping Momentum Auto solvent with additional funds, the subordinate funders were only permitted to collect a fraction of their originally-stipulated daily payments (and only if Momentum Auto had adequate liquidity and cash flow, otherwise they were not allowed to collect anything at all until 1st Global had been paid in full). In the case of Capital Stack, it was agreed they could only debit 20% of what they were normally entitled to. For others it was 10%.

1st Global Capital says both restrictions were violated, that the funders collected above their agreed percentage and that they also collected from Momentum Auto despite the business not having adequate liquidity and cash flow. As relief, 1st Global Capital is seeking that each MCA funder return all funds they collected from Momentum Auto Group to 1st Global Capital.

Momentum Auto Group is a conglomerate of car dealerships in California that shut their doors in November. Soon after, lawsuits flew, and in one case the judge has ordered the dealerships be placed into receivership.

1st Global Capital is itself in receivership, having filed bankruptcy in July this year. The company and its founder were also charged with fraud by the SEC after they allegedly relied on the sale of unregistered securities to more than 3,400 investors nationwide.

Business That Left Merchant Cash Advance Companies Hanging is Under FBI Investigation

December 16, 2018 In 2017, several judgments were issued in the New York Supreme Court against one Michael Willhoit, a resident and business owner in Springfield, Missouri. No lawsuits were filed, Willhoit had merely confessed judgment to nearly a half million dollars collectively.

In 2017, several judgments were issued in the New York Supreme Court against one Michael Willhoit, a resident and business owner in Springfield, Missouri. No lawsuits were filed, Willhoit had merely confessed judgment to nearly a half million dollars collectively.

By the following summer, a visitor would come knocking on the door of Willhoit’s fully-customized multimillion dollar safari-themed home, dubbed “The African Queen.” It was the FBI. He was under investigation for bank fraud.

According to the Springfield News-Leader, Willhoit’s wife told an investigator that her husband’s exotic car business was gone. But if so, several banks want to know where $4.25 million in unpaid loans went and what happened to the 33 vehicles that Willhoit had given them paperwork for. The banks, who sparked the FBI investigation, sued, and by November Willhoit’s wife filed for bankruptcy. Among her listed possessions were

- Two roaring lion masks

- Two 7-foot tall hand-carved wooden tusks

- An eight-legged genuine impala horn zebra-hide chair

- A 15-foot African warrior statue

- A 3,000-pound (approximately) bronze rhino

- Four gazelle taxidermy mounts

- A baboon, full-body mount

A youtube video tour of the home shows even more exotic paraphernalia. Realtor.com described the residence, which went on the market in July for $8.9 million, as a trophy showcase of African art. Willhoit told a News-Leader reporter in 2016 that he spent $3 million renovating the property including $400,000 for a 900-square-foot wood floor and $300,000 for landscaping.

More recently, News-Leader reported that Willhoit is the target of a federal grand jury investigation. In one of the bank lawsuits filed against him, Willhoit’s defense is reportedly that it’s the bank’s fault.

The Funder: From Office of One to Eighteen in Under a Year

December 13, 2018 Not even a full year in business, Velocity Capital Group announced that it has secured $15 million in financing; $5 million in a series A, plus a $10 million line of credit. The entire investment comes from a family hedge fund in California, according to Jay Avigdor, Velocity’s President and CEO. Twenty-six year old Avigdor started the company out of his home in February and now employs 18 people in an office in Cedarhurst, Long Island.

Not even a full year in business, Velocity Capital Group announced that it has secured $15 million in financing; $5 million in a series A, plus a $10 million line of credit. The entire investment comes from a family hedge fund in California, according to Jay Avigdor, Velocity’s President and CEO. Twenty-six year old Avigdor started the company out of his home in February and now employs 18 people in an office in Cedarhurst, Long Island.

Avigdor told deBanked that he started Velocity earlier this year with $50,000 of his savings, having spent nearly five years working for Pearl Capital. Already, he said that Velocity, which finances MCA deals, has funded over $20 million. Avigdor said he started at Pearl shortly after finishing college when he was about 19. (He said he graduated early thanks to credits he used from studying abroad and because he started college at 16). At Pearl, Avigdor said he wanted to get on the phones immediately. But with only two days of training, they wouldn’t let him.

“I thought ‘screw it,’” he recalled. “I only had $16.25 to my name and I wanted [the opportunity] to make money.”

So he said he found an old yellow pages phone book, brought it to the office with his phone charger and just started making calls from his own phone. Shortly thereafter, from his own cold calling, he said he closed a $250,000 MCA deal with an auto dealer in California.

“When I went back to the office the following day, they had two computers set up for me,” Avigdor said.

While Velocity funds a variety of businesses, Avigdor said they most commonly fund medical, technology and construction companies.

Avigdor said that while Velocity uses technology for efficiency, they also have a personal touch. For instance, he said they use an automated onboarding process for brokers, yet the actual underwriting and funding calls with merchants are done on the phone. At least that’s the way it works now.

“We crawl before we walk before we run,” Avigdor said.

He said that they give 10% of the net of proceeds on each file to a charity, which changes each month. Currently, it’s The Wounded Warriors.

Avigdor said tries to follow the advice of a rich, wise man he knows, who told him: “You won’t be remembered for how much gold you had, but for how many gold bars you’ve given away.”

Defunct MCA Company Tried to Escape Signed Confession of Judgment

December 13, 2018 When a Florida-based merchant cash advance company, World Global Financing (WGF), declared bankruptcy this past May, it entered into a binding settlement agreement with its largest creditor, a hedge fund known as Eaglewood.

When a Florida-based merchant cash advance company, World Global Financing (WGF), declared bankruptcy this past May, it entered into a binding settlement agreement with its largest creditor, a hedge fund known as Eaglewood.

There was a caveat.

Eaglewood required that WGF sign a Confession of Judgment (COJ) as part of the agreement that would afford Eaglewood the right to file and obtain a judgment without further litigation if WGF breached the settlement. On August 3, that’s exactly what happened. After WGF failed to make the stipulated payments to Eaglewood, the COJ was filed in the New York Supreme Court so as to obtain a nearly $6 million judgment against WGF and company founder Cyril Eskenazi.

While it can be virtually impossible to invalidate a COJ, the courthouse Clerk nonetheless refused to enter it because of alleged technical defects, one of which involved WGF’s use of an out-of-state notary to witness a New York State affidavit.

“The alleged Affidavit of Confession of Judgment upon which Eaglewood’s request for a Judgment by Confession stands like a house of cards is no affidavit at all under New York law, and cannot be used in a New York litigation,” WGF’s attorney argued.

The absurdity of the argument was not lost on Eaglewood because the notary WGF challenged on technical grounds was the notary that WGF and its counsel had themselves chosen and approved. Eaglewood called the charade of contesting the validity of one’s own affidavit signed in the presence of counsel, utterly frivolous and a fraud upon the Court.

Defects or not, the judge concurred with Eaglewood because WGF had irrevocably and unconditionally agreed to the entry of judgment if they breached the settlement agreement in the first place, which they did, rendering the alleged technical errors with the COJ itself a moot point.

The COJ was therefore deemed valid and the judge ordered the Clerk to enter the judgment.

On Nov 29, a judgment for $5,866,477 was entered against WGF and Eskenazi. The index # is 651489/2018 in the New York Supreme Court.

Senate Bill Introduced to Ban Confession of Judgments Nationwide

December 6, 2018 Senators Sherrod Brown and Marco Rubio have called for a nationwide ban on Confessions of Judgment in response to the Bloomberg Businessweek series published last month. The bill, which would amend the Truth in Lending Act, may be named the Small Business Lending Fairness Act.

Senators Sherrod Brown and Marco Rubio have called for a nationwide ban on Confessions of Judgment in response to the Bloomberg Businessweek series published last month. The bill, which would amend the Truth in Lending Act, may be named the Small Business Lending Fairness Act.

You can download the bill here

Though Businessweek has been successful in pressuring regulators to conduct inquiries into several merchant cash advance companies and the New York City marshals, authors Zachary Mider and Zeke Faux have remained notably silent on the gaping holes in their narrative. Questions posed to each reporter have yet to receive any responses.

deBanked researched the accuracy of Businessweek’s findings only to determine that two of the purported victim’s stories were not credible. In one case, a business owner that was said to have been “wiped out,” was bragging about his new luxury race car on facebook while public records revealed he was still paying himself six figures a year from the allegedly defunct company that had more than $700,000 running through its bank accounts. In another case, a victim that claimed to be selling off household furniture to buy food after a run-in with a predatory lender, turned out to be a multimillionaire TV station owner.

OnDeck Expands Canadian Business with Merger

December 5, 2018 OnDeck announced today that it has entered into an agreement to merge its Toronto-based Canadian business with Evolocity Financial Group (Evolocity), an online small business funder headquartered in Montreal. OnDeck will have majority ownership of Evolocity and the combined entity will be rebranded as OnDeck Canada.

OnDeck announced today that it has entered into an agreement to merge its Toronto-based Canadian business with Evolocity Financial Group (Evolocity), an online small business funder headquartered in Montreal. OnDeck will have majority ownership of Evolocity and the combined entity will be rebranded as OnDeck Canada.

“The combination of OnDeck’s Canadian operations with Evolocity will create a leading online platform for small business financing throughout Canada and represents a significant investment in the Canadian market,” said Noah Breslow, Chairman and CEO of OnDeck. “There is an enormous need among underserved Canadian small businesses to access capital quickly and easily online.“

According to the announcement, “the transaction will combine the direct sales, operations, and local underwriting expertise of the Evolocity team with the marketing and business development capabilities of the OnDeck team.”

As part of the merger, Neil Wechsler, who is the CEO of Evolocity, will become the CEO of OnDeck Canada. And the management team will include Evolocity co-founders David Souaid as Chief Revenue Officer and Harley Greenspoon as Chief Operating Officer. OnDeck Canada will be governed by a Board of Directors chaired by Breslow and composed of existing OnDeck and Evolocity management.

Currently, OnDeck offers a variety of loans up to $500,000 and lines of credit up to $100,000. Evolocity offers small business loans and an MCA product, from $10,000 to $300,000. deBanked inquired with OnDeck to see if OnDeck Canada will retain the MCA product from Evolocity, but has yet to hear back. Since OnDeck entered the Canadian market in 2014, it has originated over CAD $200 million in online small business loans there. Evolocity has provided over CAD $240 million of financing to Canadian small businesses since 2010.

Currently, OnDeck offers a variety of loans up to $500,000 and lines of credit up to $100,000. Evolocity offers small business loans and an MCA product, from $10,000 to $300,000. deBanked inquired with OnDeck to see if OnDeck Canada will retain the MCA product from Evolocity, but has yet to hear back. Since OnDeck entered the Canadian market in 2014, it has originated over CAD $200 million in online small business loans there. Evolocity has provided over CAD $240 million of financing to Canadian small businesses since 2010.

Investment in online small business lending in Canada is growing. IOU Financial, a Montreal-based small business funder that primarily funds American small businesses, told deBanked last month that they made a concerted marketing effort in the third quarter to reach Canadian small business owners. Meanwhile, Thinking Capital, a Canadian online small business funder, announced in July the launch of BillMarket, a service that provides Canadian small businesses with a credit grade (A through E), making it easier for them to get funded.

“BillMarket represents a cash flow revolution for the Canadian small business market,” said Jeff Mitelman, CEO of Thinking Capital, which has roughly 200 employees between its Toronto and Montreal offices.

According to a recent Canadian government report cited by OnDeck in its announcement today, there are 1.14 million small businesses in Canada that represent 97.9 percent of all businesses in the country. Also, small businesses employed over 8.2 million people in Canada, or 70.5 percent of the total private workforce.

According to a recent Canadian government report cited by OnDeck in its announcement today, there are 1.14 million small businesses in Canada that represent 97.9 percent of all businesses in the country. Also, small businesses employed over 8.2 million people in Canada, or 70.5 percent of the total private workforce.

Evan Marmott, founder of Canadian small business funder, Canacap, told deBanked earlier this year that unlike the saturated small business market in the U.S., the Canadian small business market is still ripe for growth. Not only this, he said that while the market is smaller in Canada, the default rates are generally lower and he found that Canadian merchants do less shopping around. He also said he has seen less fraud in Canada than in the U.S.

“For brokers, while commissions are lower, you could actually speak to business owners who are not being bombarded with calls [as they are in the U.S.] and have a much higher closing rate,” Marmott said.

Evolocity has 70 full-time employees and offices in Montreal, Vancouver and Marham, in the Toronto area. OnDeck has funded over $10 billion to small businesses and became a public company (NYSE: ONDK) in 2014. OnDeck is headquartered in New York.

“We are excited to join forces with OnDeck…to enhance our best in class digital financing solutions to small businesses across Canada,” said Wechsler, Evolocity CEO. “Additionally, this transaction will augment our data science and analytics capabilities to help deliver an unparalleled merchant experience.”

Popular Business-Lending Marketplace Dealstruck Restructures

December 3, 2018VALLEY STREAM, N.Y., Dec. 3, 2018 — Innovative online business-lending marketplace Dealstruck.com (which has been featured in CNBC, The New York Times, Forbes and many other publications) has reorganized. A private investment group of fintech experts acquired the company. “This acquisition represents a significant strategic opportunity for our client base,” said Dealstruck CEO Anthony Porrata.

Dealstruck is a leader in the alternative lending space. The company provides small and medium-sized business owners with seamless access to capital. Advances in technology make the process quick and efficient with minimal paperwork.

During the restructuring process, the company paused providing loans. “Recently, many people have asked, ‘What happened to Dealstruck?’ There were rumors that Dealstruck shut down but that was not true,” noted Porrata. “We’re happy to announce the Dealstruck news that a group of private investors has created a new ownership coalition that is leading a bold evolution for the company.” The new investment group combines a portfolio of existing small business capital providers with the highest technological advances in the field of online business loans.

Company leaders expect the change will help small businesses immensely. “Clients will see quicker approval turnarounds and a more streamlined process,” said Porrata. “This will also help clients who would not otherwise have equal access to growth opportunities.”

Vice President Chris Jones expects small business owners will be excited about the Dealstruck news. “This restructuring will allow us to approve more clients than ever before,” he smiled. “I’m looking forward to joining many new business ribbon-cutting ceremonies. Nothing gives us more pride than a grand opening.”

The reorganization allows Dealstruck to expand its mission while maintaining the personalized service that makes it so well known. The new management team has access to more capital and creative financing terms for Dealstruck clients.

About Dealstruck: As a leading online capital facilitator, Dealstruck connects small and medium-sized businesses with access to a variety of working capital options. These options help business owners find custom-tailored loans, so they can better manage their time and achieve their goals. For more information, visit dealstruck.com.

Contact:

Anthony Porrata – CEO

855-610-5626

info@dealstruck.com

What We Learned About Credibly From Credibly’s Securitization

November 29, 2018Today, Credibly CEO Ryan Rosett told deBanked that the company’s October securitization will be used, in part, to roll out its new Market Expansion Product (MXP), which will allow Credibly to service merchants with FICO scores as low as 500 and those that have been in business for less time.

“We believe the MXP will open up the funnel by allowing us to serve business owners that we previously couldn’t,” Rosett said.

Kroll Bond Rating Agency assigned preliminary ratings to three classes of notes as part of Credibly’s first securitization. Rosett said this securitization follows a large warehouse line of credit from SunTrust Bank which is also the primary underwriter, of the securitization.

In addition to the new MXP product, Rosett said that Credibly intends to launch a line of credit product in 2019. Currently, Credibly provides merchant cash advances up to $150,000, business expansion loans up to $250,000, with terms up to 24 months, and working capital loans up to $250,000 with terms up to 17 months. Rosett said that the company’s working capital loan is its most popular product.

In an interview yesterday with Benzinga, Rosett said that he has seen a strong increase in demand for Credibly’s products and that they are currently evaluating over 10,000 applications per month.

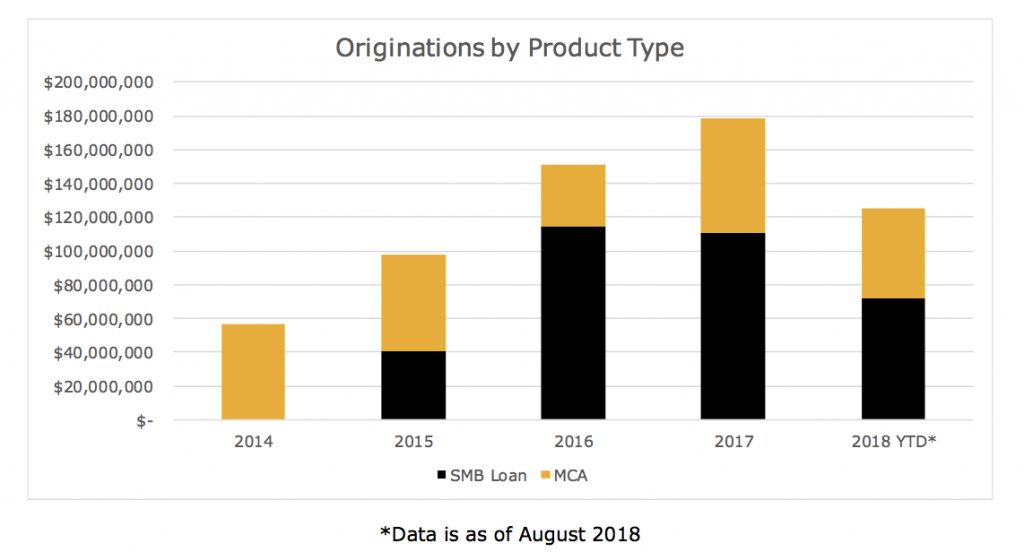

2017 net revenue before provisions: $33 million

2017 earnings: $1.4 million

Total shareholder equity: $18.7 million

Lifetime funding volume: $700+ million

Raw # of fundings: 17,000+

Majority owned by: Flexpoint Ford

# of employees: 140

Notable deal: Acquired the rights to service BizFi’s $250 million MCA portfolio in August 2017

Provides: Small business loans (in 37 states and D.C.) and merchant cash advances

Founded: 2010 by co-CEOs Edan King and Ryan Rosett

Generates deals via: Brokers and inside sales