Bitty Advance Opens Office in NYC

June 6, 2019

Bitty Advance has expanded to midtown Manhattan. The company’s first location, in Fort Lauderdale, FL, will remain intact as the corporate office.

“We wanted to have a New York presence to hire sales talent, underwriters and, of course, raise more capital because obviously this is the mecca for finance,” said CEO of Bitty Advance Edward Siegel.

Siegel said he is currently hiring salespeople and experienced underwriters for the New York office. There were about 10 well-dressed salespeople at the spacious Bitty Advance office in New York this morning, and Siegel said he plans to grow the office to about 20. He said there are 30 employees in Florida, none of whom moved to the New York office. The New York office does sales and underwriting, while the corporate office in Florida also handles sales and underwriting and houses the customer service and executive teams.

“We also wanted to have a presence in New York for our partners,” Siegel said.

Siegel’s partners include ISOs and other funders that don’t fund the smaller deals that Bitty Advance specializes in. Bitty Advance provides “micro advances” (from $2,000 to $10,000) to merchants doing less than $100,000 in revenue.

Siegel has another Florida-based funding company called Fundzio, and Bitty Advance launched in 2017 when Siegel recognized that almost 50% of online applications to Fundzio were coming from merchants doing less than $100,000 in revenue.

“I realized that the only proper way to do this was to create another company, carve out a niche, and build a team that was just focused on micro advances,” Siegel said.

ForwardLine, One of the Original Funding Companies, is Back

June 5, 2019 Steve Carlson, CEO, ForwardLine

Steve Carlson, CEO, ForwardLineForwardLine Financial originated well over $65 million in loans in 2018, according to CEO Steve Carlson. ForwardLine would not share its origination numbers, but Carlson said the company is comfortably on the deBanked list of top originators. ($65 million is the lowest origination number on the list).

Last week, the company announced that it secured a $100 million credit facility from Credit Suisse AG and Neuberger Berman private equity funds. This is the company’s largest credit facility to date. Its previous credit facility was with East West Bank and that relationship is still in place.

ForwardLine is a direct marketer that provides working capital loans of up to $200,000 to small businesses.

Carlson told deBanked that ForwardLine, which was founded in 2003, has been scaling its business dramatically over the past year and a half. This is no coincidence. Instead, Carlson said this is the result of years worth of planning following a majority investment in ForwardLine in 2015 by a private equity firm called Vistria Group.

“We spent 2016 and 2017 very thoughtfully building out a technology platform, a data infrastructure, and a management team to scale the business,” Carlson said. “We’re now actioning on that plan. So this is all part of a multi-year strategy.”

A company statement said that the company’s loan performance in 2018 was record-breaking. ForwardLine increased year-over-year total originations by over 300% in the first quarter of 2019.

Carlson said that the new facility will be used primarily to grow the business. ForwardLine is located in Woodland Hills, CA, and it employs 110 people, more than half of whom work in the sales department. Other employees include underwriters and data and analytics people.

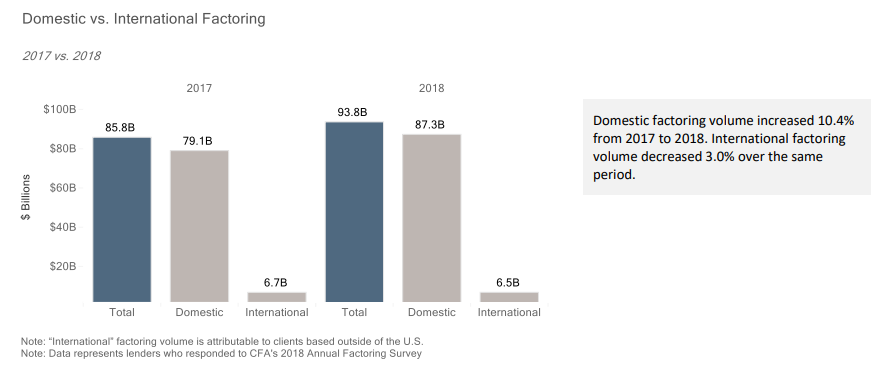

CFA Report Shows Increase in US Factoring Volume

May 30, 2019The Commercial Finance Association (CFA) recently published a report on asset-based lending and factoring which showed a 10.4 % increase in domestic factoring volume in 2018 compared to 2017. While the increase isn’t enormous, it is consistent with a gradual growth in factoring, according to Jeff Goldrich, CEO at Princeton, NJ-based North Mill Capital, which provides invoice factoring.

“It’s not a hockey stick, it’s gradual growth,” Goldrich said.

Goldrich attributed the growth, albeit moderate, to two factors. One is that, while not everywhere, he said there’s been some tightening of credit with banks, which leads companies to consider factoring.

The other is that he said large sized companies are increasingly using factoring as a financing option. While factoring is generally more expensive than taking out a bank loan, companies don’t have to worry about having stellar financial history because factors are less concerned with the financial health of the borrower and more concerned with the strength of the receivable.

Another finding in the CFA report is that Recourse factoring increased by roughly 11% in 2018 compared to 2017. Recourse factoring is when a factor has recourse if a company fails and is unable to pay a receivable to a factor’s client, according to Harvey Gross, Executive Director of the New York Institute of Credit. This is unlike the more common Non-Recourse factoring, where the factor can do nothing if the company that the owes the receivable goes out of business. Gross says that Recourse factoring is becoming more common as factors don’t want to take on as much risk.

Gross said that the older, traditional factors (which often cater to the apparel and toy industries, for example) are still Non-Recourse factors. They shoulder the loss if a company can’t pay its invoices. But at the same time, Gross said that these factors want clients with a large volume of invoices and invoices from solid companies.

BlueVine is one of the few companies that offers factoring online, where a company can get funded online without first interacting with a company representative.

“I see a continuation of factoring marrying fintech,” Goldrich said. “That’s where the big backers have interest.”

Liquid FSI Partners With Stackfolio

May 28, 2019

Liquid FSI announced today that it has entered into a joint venture with Stackfolio, an online loan marketplace, which allows small banks, hedge funds and credit unions to buy and sell loans. Liquid FSI funds mostly doctor’s offices, as a factor, and it also builds financial technology products to make it easier to fund healthcare providers.

Through this new partnership with Stackfolio, all of Liquid FSI’s applicants will now automatically be posted to Stackfolio’s marketplace. Since Liquid FSI is a funder, why send deals to the competition?

“Just like there’s a college for everyone, there’s a loan [or type of funding] for everyone,” said CEO of Liquid FSI Frank Capozza.

And for deals that come from Liquid FSI but are funded elsewhere on the Stackfolio marketplace, Liquid FSI will get an origination fee and a transaction fee.

Capozza said that their proprietary technology gives banks a far clearer picture of the finances of medical offices, which can be risky to fund because insurance companies often pay a fraction of what doctors bill.

“Now they don’t have to turn business away,” Capozza said of banks that have declined medical offices because of imprecise data which he says Liquid FSI provides.

From Stackfolio’s CEO, Pavleen Thukral, “We are excited for this new partnership with Liquid FSI. It not only aligns our view of the loan trading and origination markets moving online, but more critically for our clients, it helps fill a loan growth gap with commercial and industrial customer opportunities in the healthcare industry.”

In conjunction with this new partnership, Capozza said that he is in final talks with a 55-person, California-based brokerage that will help increase medical office applications to Stackfolio, via Liquid FSI.

“We’re the acquisition engine,” Capozza said.

He said that this brokerage, to be announced at the end of the week, will have its people on the phone and on the ground (i.e., pitching doctors in their offices). Brokers will get a percentage of the origination and residuals on monthly factoring transactions.

Does The Borrower Even Exist? Image Algorithms, Site Inspectors Spot The Fakers

May 24, 2019 Their product research lab was the real deal. That’s what a business seeking capital hoped to convince a lender of when they snapped a photo of a $450,000 microscope and sent it over to underwriting along with two dozen other photos of their warehouse.

Their product research lab was the real deal. That’s what a business seeking capital hoped to convince a lender of when they snapped a photo of a $450,000 microscope and sent it over to underwriting along with two dozen other photos of their warehouse.

Most of the pictures were genuine, but the microscope was not. Truepic, a virtual site inspection and photo verification company that the lender had relied on, algorithmically determined that the microscope was actually a photo of a photo, one that had been grabbed off the web.

If they had just emailed these photos directly to the lender, the loan would’ve been issued, but this image analyzing technology changed everything.

Truepic founder and COO Craig Stack said that they were able to identify the false ones because of software they have that can detect when a photo is being taken of a two-dimensional image. Truepic didn’t just obtain the photos, they were taken in real time using their mobile photo-taking app. In addition to detecting only two dimensions, Truepic also found the real photos online through a reverse-image search to show where the photos came from.

Photo verification isn’t brand new. Nationwide Management Services has been providing these very same services to their customers since 2015, according to its CEO John Marsh. Marsh started his company in 2005 and originally provided traditional on-site inspections with certified field agents taking pictures.

“You can’t tell the difference,” Marsh said of photos taken by a field agent, compared to those taken virtually by the owner of the store or office. In the virtual one, the merchant receives a text and clicks on a link that essentially turns the merchant’s phone into a live video feed for the lender.

Commonly, the lender wants to see, among other things, the company’s signage, credit card machine and merchant’s driver’s license. Using GPS technology, Nationwide Management Services can tell exactly where the merchant is, so they can’t be taking photos – in real time – of a different store.

Marsh still offers on-site inspection for clients, but mostly as discreet, unannounced visits to check up on a merchant that is having a hard time making payments. Sometimes a field agent will find that a direct competitor moved in across the street or the neighborhood is declining and there are a number of vacant stores, Marsh said.

Marsh still offers on-site inspection for clients, but mostly as discreet, unannounced visits to check up on a merchant that is having a hard time making payments. Sometimes a field agent will find that a direct competitor moved in across the street or the neighborhood is declining and there are a number of vacant stores, Marsh said.

Marsh’s virtual video verification product is instantaneous, allowing the lender to see the merchant’s space – and face – in real time, virtually eliminating misrepresentation of the merchant’s store. Stack said that Truepic also has a video verification product that they will be releasing in less than three weeks.

Marsh said that would-be merchant fraudsters get scared as soon as they hear about a real time virtual inspection.

“When we reach out to them for the virtual inspection, they go dark,” Marsh said.

Most of the deception Marsh has encountered is of merchants giving a P.O. Box address as the address of their “physical store.”

Gayle Juhl, President and CEO of Metro Inspections, said that one of her field agents found a merchant with a far more unusual distortion of its company address. The field agent went to the address of the merchant only to find a 1970s bright blue Volvo station wagon with a sign on it, parked in front of the address listed, which belonged to a completely different store.

The man seeking funding, who came out of the car-turned-store, was apparently confrontational, according to the field agent’s report.

Juhl said that she will coordinate a virtual inspection upon request, but that her company primarily does onsite inspections.

“You can’t replace a handshake and an eye-to-eye to see what’s really going on,” Juhl said.

This may be true, but Marsh said that it can take 24 to 48 hours to collect photos for his onsite inspections whereas it can take as little as four minutes with his virtual video or virtual photo services. (This depends on how many images the lender is looking to capture.) Granted, Juhl said that Metro Inspections’ on-site inspections can be collected and delivered on the same day it was requested, given that the request comes early enough in the day.

Stack, who has only been servicing the online lending industry for about five months, says that he has gotten financial services clients who are very excited about the speed of virtual inspections and the fact that they are far less invasive for the merchant. Rather than have a stranger come in to take pictures – raising questions among employees and customers – the business owner can discreetly photograph their space at their convenience. Stack’s company has never offered onsite inspections and says he never will.

“Our camera doesn’t lie,” he said.

BFS Capital Joins ILPA

May 23, 2019

The Innovation Lending Platform Association (ILPA), a group of online small business financing and service companies, announced today the addition of BFS Capital. ILPA is known for creating the Straightforward Metrics Around Rate and Total Cost (SMART) Box.

“We believe that transparency matters,” Ruddock told deBanked.

“BFS Capital is committed to being both a responsible and an innovative lender,” Ruddock said. “Our membership in the ILPA allows us to work with industry leaders who are dedicated to advancing standards and best practices in the critical small business lending marketplace… [and] we believe that clarity and transparency is critical in helping [small businesses] make educated and informed financial decisions.”

As a new member of ILPA, BFS will join current members including OnDeck, Kabbage, BlueVine and 6th Avenue Capital.

“We applaud Mulligan Funding and BFS Capital for committing to adopt fair and transparent disclosure best practices to ensure small businesses are well informed when seeking funding,” said ILPA CEO Scott Stewart. (ILPA announced that Mulligan Funding has joined the association as well).

BFS is also a member of the Small Business Finance Association (SBFA) and Ruddock told deBanked that BFS will remain a member of that trade association as well.

Separately, BFS announced today that it has named Fred Kauber as the company’s new Chief Technology Officer and Chief Product Officer. Kauber was previously with fintech marketplace platform CAIS Group and he served in senior roles at First Data, Dun & Bradstreet and IBM.

“I’m confident that Fred is the right person to advance both our vision and our capabilities [at BFS,]” Ruddock said.

The Road Back to Residual Commissions

May 17, 2019

“We’re still getting resids from a company 14 years later.” That’s what Phil Dushey said about a factoring client he has at Global Financial Services, a New York-based financial brokerage firm he founded.

He was speaking at deBanked’s “Broker Fair” to a room filled mostly with MCA brokers. Years ago, in the early stages of the merchant cash advance industry, brokers would earn residual payments from credit card processing companies when the merchants were converted from one merchant account to another to make the advance possible. Brokers also got residuals from MCA funders that would pay them over time as the merchant paid back.

Now that MCA companies rarely ever rely on credit processors and since they started to offer brokers their entire commission upfront, the concept of residual payments for MCA brokers became history. But for MCA brokers interested in broadening their product offering, residuals can resurface as a revenue stream if they embrace factoring.

Dushey later conceded that residuals from a factoring client lasting 14 years is highly unusual. What is common, though, is to get residuals that last four to five years, he said.

Ed DeAngelis, founder of Amerifi, a brokerage of 12 in Pennsylvania, said that brokers’ residual payments can be anywhere from 8% to 15% of what the factor collects from the merchant. He presented what he said was a realistic example of a merchant factoring a $100,000 invoice. The factor might typically take a 2% factoring fee, or $2,000. And the broker might take 10% of that amount, or $200, for every month that the invoice is outstanding.

“It’s a steady drip that makes a puddle,” DeAngelis said.

Of course, for a larger invoice, like for $500,000, the broker would get $1,000 a month, as long as the client keeps factoring. But DeAngelis said that most factoring companies have a one year agreement and that most clients stay with their factoring company for two to three years. And some, like Dushey’s client, stay for as many as 15 years. Since DeAngelis opened his brokerage two years ago, he said that all of his factoring clients are still in their agreements.

Eyal Lifshitz, CEO of BlueVine, one of the larger factoring companies, said that MCA brokering definitely pays more upfront, whereas factoring is more about building a book of business.

“There are factoring brokers that make quite a lot, but I would say they probably focus on larger deals,” Lifshitz said.

Lifshitz wouldn’t disclose the average size of a BlueVine factoring deal, but his estimation was that the industry average was $250,000 to $500,000.

“What we’re trying to build is a 20 to 30 year sustainable business,” DeAngelis said. “…So we’re trying to build those small residuals because five years from now, who knows? With regulations [in] cash advance, it may not be around. We’re already diversifying our portfolio with all these other traditional products so we’re not cash advance dependent.”

Not all brokers of factoring deals make residuals, according to Frank Capozza, founder of LiquidFSI, which provides factoring services to doctors offices. He said that he works with select brokers and they generally don’t get residual payments from his company. Instead, he pays them an origination fee.

Still, it seems more common for brokers of factoring deals to receive residuals. But it might not be for everyone.

For MCA brokers interested in also offering factoring, Lifshitz said: “They need to understand the product and what merchant could fit the criteria. It is more complex to understand than MCAs in my opinion.”

How To Scale Your Broker Shop

May 15, 2019

When it comes to hiring, it’s quality over quantity. That’s what the co-founders of Everlasting Capital Josh Feinberg and Will Murphy told a packed room at deBanked’s Broker Fair last week. They presented a panel called “How to Scale Your Broker Shop,” where they shared tips on how to do just that.

“We wanted to scale so badly and throw bodies in seats,” Murphy said.

And that’s what they did until they realized that they were doing just as much volume when they had fewer people.

CEO of National Funding Dave Gilbert, who spoke on a different panel at Broker Fair, said that he’s a fan of small brokers. He later explained to deBanked that when brokers get too big, they can get stuck with legacy staff. Instead, he said that when they stay lean and spend money on high quality salespeople, they can be much more effective with five or fewer people than with 10.

“It’s not the amount of bodies in the office, it’s the processes you have in place,” Murphy said.

Processes like hiring, training employees and organizing data, which they said should be as simple as possible. Bigger isn’t better and perfect isn’t realistic, they conveyed.

“Don’t worry about trying to create the perfect website or business card,” Feinberg said.

Instead, he said to think about five elements when trying to scale a brokerage shop:

- Focus on cash flow.

- Know that you will fail.

- Don’t quit before the miracle happens.

- Be different than your competition.

- Think bigger.

Meanwhile, Murphy presented concrete actions to take to grow a broker shop:

- Get customers.

- Build relationships.

- Be transparent.

- Find a mentor.

- Ask questions.

- Specialize in two programs (products)

- Brand yourself / your company

Everlasting Capital, which now has 19 people on staff and is based in New Hampshire, facilitates MCA funding and equipment financing.

On Diversification: Acknowledging that MCAs have an uncertain future, Feinberg said it’s important to diversify. He said that three years ago they were doing exclusively MCA deals and now they do 50% MCA and 50% equipment financing.

On social media marketing: “Be consistent. It’s not about the likes. It’s about [good] content and consistency,” Murphy said.

On broker performance: Brokers are given a six month training program at Everlasting Capital. After the six month period, they’re expected to fund four deals a month.

They also said it’s important to make friends with people in the industry.