Industry News

Recent Merchant Cash Advance News

April 14, 2013 In case you missed some of the big headlines in this last week, below is a summary:

In case you missed some of the big headlines in this last week, below is a summary:

Forbes changed its tune on MCA after five years

It took only a handful of journalists to set the Merchant Cash Advance industry’s momentum back YEARS. One of those journalists was Maureen Farrell, a previous writer for Forbes. Her story on January 31, 2008, titled Look Who’s Making Coin Off The Credit Crisis mercilessly labeled Merchant Cash Advance providers as blood sucking vampires borne out of the Great Recession. Sensational headlines attract attention and Farrell did her job well. But for someone whose background is Art History, English, and Journalism, she may not have been in the best position to make a qualified assessment of such a unique method of alternative finance. It’s unfortunate then that Forbes ran the story since it no doubt impacted public opinion in a negative manner for years.

That’s why it was so refreshing to see ‘Money, Money’ — How Alternative Lending Could Increase Your Company’s Revenue in 2013. Published by Cheryl Conner, she wastes no time in pointing out Farrell’s prior coverage as one of personal opinion and skepticism. Merchant Cash and Capital’s CEO, Stephen Sheinbaum was instrumental in Conner’s fresh assessment of the industry.

Read the new article on Forbes…

Deals being stretched out over 15 to 24 months may not be a step in the right direction

At least that’s the take of RapidAdvance’s CEO Jeremy Brown. In his latest post on DailyFunder Brown argued permanent capital solutions do not fit working capital needs.

Read his post…

Major executive shake-up occurs at Capital Access Network

Capital Access Network, the parent company of AdvanceMe, CapTap, and NewLogic recently let go of several top executives. Before official announcements were made, word had already leaked out and was being discussed on DailyFunder.

Read the discussion…

Merchant Cash Group announced the winner of their NCAA March Madness contest

NCAA basketball took us for a wild ride this year, but Merchant Cash Group is still awarding all their participants with bobble heads. The first place winner got cold hard cash.

His name is….

On Deck Capital embraces startup culture

Video games and ping pong tables adorn On Deck’s new office. Is the culture changing in alternative lending?

Read the story…

The ETA Expo is fast approaching. Are you going? Plan meetups

ETA expo thread on DailyFunder…

Kabbage Closed on a $75 million credit line

Read the story…

Merchant Cash Group NCAA Contest Winners Announced

April 10, 2013 If you weren’t in this year’s NCAA bracket competition hosted by Merchant Cash Group, you missed out on a lot of fun!! But that’s okay, because well there’s always next year 🙂

If you weren’t in this year’s NCAA bracket competition hosted by Merchant Cash Group, you missed out on a lot of fun!! But that’s okay, because well there’s always next year 🙂

From Heather at Merchant Cash Group:

“Merchant Cash Group had the privilege of hosting a NCAA March Madness Bracket Challenge offering a top cash prize of $500.00. We invited people from all over the financial industry to join our friendly competition where even the losers walk away with a cool prize. The Brackets were shaken up severely with the Cinderella story of Florida Gulf College and the early elimination of some of the top schools, uh hum Kansas St, New Mexico and UNLV to name a few. By April 8th we were down to only one person (Billy Crowe) who had Louisville winning it all and with that made a come behind win with a 15 point spread.

Now, while Billy is walking away with the Grand Prize all the other participants will be receiving a basketball bobble head trophy announcing to everyone that they in fact our bracket challenged. I would like to thank everyone who participated in the competition and I look forward to hosting more networking opportunities for our space. Below is the final standings and in the interest of saving ego’s please do not rag the losers to hard after all they are stuck with a bobble head.”

- Billy Crowe – PricewaterhouseCoopers Final Score: 111

- Heather Francis – Merchant Cash Group Final Score: 96

- Badger Morning – Merchant Cash Group Final Score: 80

- Sean Murray – Raharney Capital Final Score: 74

- Kara B – Merchant Cash Group Final Score: 73

- Jason Fullen – NVMS Final Score: 69

- Michael Bernier – SBS Capital Final Score: 59

- J. Mark Anderson – Business Funding USA Final Score: 50

- Scott Williams – Financial Advantage Group Final Score: 48

————————————

My chances at bracket gold were dashed when New Mexico lost in the first round to Harvard. Harvard…

Thank you Heather for the fun and also I want to let everyone know that I will be spending some time at Merchant Cash Group’s booth during the ETA expo (#751) on behalf of MPR and DailyFunder. Merchant Cash Group is a great MCA company and I am honored to participate in their exhibit.

MCA Industry Continues Expansion

April 3, 2013 It’s said that one way to measure success or growth of an industry is to count how much capital is being raised. In that case, Kabbage and On Deck Capital have been on fire lately.

It’s said that one way to measure success or growth of an industry is to count how much capital is being raised. In that case, Kabbage and On Deck Capital have been on fire lately.

Early this morning, Kabbage announced they had secured a new $75 million line, after having just raised $30 million 6 months ago. The Forbes article announcement states that Kabbage has funded 60,000 deals to date and predicts to fund 100,000 deals in 2013 alone, a figure hard to comprehend considering that’s equivalent to the amount of transactions Capital Access Network has managed to do over the course of 15 years. I understand that Kabbage may do smaller, shorter term deals, but Capital Access Network has dominated MCA for a long time. Could Kabbage really do 100,000 deals this year? I’m unsure about this one.

Are traditional MCA funders missing out by letting Kabbage rule Ebay, Amazon, and Etsy unchecked? Is the Internet really that different than the brick and mortar market? Late last year, Amazon entered the financing market but for the purpose of strengthening their selling partners, so there are several reasons funders are tapping that market.

Paypal has been sitting on the sidelines and is perhaps considering jumping in the ring themselves. They are beta testing now with Ebay sellers.

Merchant Cash Advance is exploding in all directions. Did you hear that Yellowstone Capital funded $700,000 to a restaurant with the help of Strategic Funding Source? That’s a lot of money for a restaurant!

The Inefficient Merchant Lending Market Theory

March 5, 2013There are 4 major factors used to determine approvals in the merchant lending market:

• FICO Score / Credit Report history of owners

• Monthly Gross Revenue

• Time in Business

• Average Daily Bank Balance

Only 1 of these factors considers the applicant’s reputation, and that’s credit reports. Credit reports reveal past payment history with other creditors. They show lawsuits, unpaid taxes, and bankruptcies. Knowing whether an applicant pays on time or not is valuable to lenders but it fails to reveal an even more important metric, the business’s ability to generate future profits. If you’re shaking your head and saying “credit reports aren’t for that purpose,” I would respond by asking which of the 4 factors then is?

The amount of money deposited in someone’s bank account in the past reveals how much they took in, but it doesn’t indicate what will happen in the future. Similarly, a substantial daily ending bank balance may show responsibility to maintain a cash cushion, but it says nothing about how likely customers are to buy from that business in the future.

Could time in business then tell us? Is it safe to assume that a business that has been operational for a year, two years, or five years will be there for many more years to come? The local auto mechanic that’s been around for 5 years may only have lasted because no one else has gotten around to opening up a rival auto shop. Would it be safe to give the most hated mechanic in town a three year loan when their success is simply the result of being the only auto mechanic in the community? There may be somewhat of a correlation between time in business and customer satisfaction but it is by no means strong enough to predict future success.

In effect, the major metrics used to judge small businesses for financing today take no consideration of the number one thing that matters to a business for survival, customers. Without customers, the amount deposited historically means nothing. Without customers, a 700 FICO score cannot produce sales, profits, or money to repay a loan. Without customers, a 50 year old restaurant can’t continue to stay open just because it’s been there for 50 years. And without customers you better hope that $1 million in sales last year made you really rich, since without customers, you’re going to need to start a new business… preferably one WITH customers.

This doesn’t mean that these 4 factors are irrelevant, they’re not. But I believe these factors combined are but a tiny sliver of data to predict how well a business will do in the future and at the same time repay a loan. Relying on weak indicators forces lenders to charge higher rates since they must compensate for the risk of unknowns. It also decreases the length of time that lenders can trust their borrowers to hold their money for.

It is no surprise then that loan terms in the merchant lending industry only range from 3 to 12 months. None of the lenders are able to predict how their borrowers are going to do far into the future, so they bank on the odds that sales and deposits in the next few months will mimic sales and deposits in the last few months. That’s also the reason why there are a lot of test/starter/trial funding rounds that are short to witness how a merchant “does” before funding additional capital on a longer term. Underwriters are flying blind. They have to see how you do because they have no data to suggest what will happen.

The big firms do have SOME data by now, but they’re broad statistics that say a certain industry in a certain region is likely to perform X with a Y margin of error. Or FICO scores below 600 are likely to have a Z rate of default. Yet this data also ignores a business’s reputation and relationship with its customers. It applies a blanket assumption of performance over the period of 3 to 12 months. These statistics are highly important to a lender because they can use them to predict defaults and delinquencies as a whole and enable them to set rates that will cover all of it and then some.

The big firms do have SOME data by now, but they’re broad statistics that say a certain industry in a certain region is likely to perform X with a Y margin of error. Or FICO scores below 600 are likely to have a Z rate of default. Yet this data also ignores a business’s reputation and relationship with its customers. It applies a blanket assumption of performance over the period of 3 to 12 months. These statistics are highly important to a lender because they can use them to predict defaults and delinquencies as a whole and enable them to set rates that will cover all of it and then some.

The owner of an ISO once asked me, “Wouldn’t it be great if we got to the point where we were funding every business in America?” My answer was “No.” If 10, 20, or 30% of those businesses failed to repay or eventually went out of business (and they would if you funded everyone) and the lender STILL made money, then the ones in good standing had to of gotten charged way too much. It would also mean that there had to be a portion of performing loans that were actually distressing the borrower, causing the capital they obtained to work against them, rather than for them. The goal shouldn’t be to fund EVERYONE, but rather to fund the few that could truly benefit.

A great example of doing it wrong is Wonga, a UK based lender that accepted a 41% rate of bad debt in 2011 while still managing to reap £62.4 million in profit. If Wonga had a few hundred bucks, a few thousand bucks, or heck only a million, they’d probably be very careful about who they approved and why they approved them. But venture capital changes the game and not always in a positive way. Putting a few hundred million dollars in the hands of Wonga has caused them to become incredibly inefficient.

Why should they only fund 5,000 people through a highly comprehensive underwriting process when they can fund 30,000 people with a one-size fits all rate, ask no questions, and accept that they will burn a lot of their customers along the way? This is the question they must have asked themselves years ago. (You can read the founder’s interview HERE)

At some point when they were developing their business model they had to admit that they really didn’t care what the outcome would be for their borrowers, so long as the business made money. And so they created an algorithm that would statistically predict the rate of default based on weak indicators like demographics, how they answered a few questions, and credit score and the resulting delinquencies were just necessary casualties to make the system work. In essence, Wonga knows they will devastate a portion of their customers and accepts this. They’re like a restaurant that only sells sugar frosted donut cheese ice cream to obese people and accepts that 41% of their revenues will be lost due to their customers dying. Can a lender truly be helping a community or economy where it intentionally hurts a percentage of borrowers because it’s still profitable at the end of the day? Do their contests, soccer sponsorships, and positive messaging on social media make up for their disruption to the economy?

Wonga’s mission is to grab market share, a strategy to make holy their blanket performance statistics and the rate that has to be charged to make money. Every single individual in the country becomes a candidate for their loans even though the lender will never know anything about the individual borrowers, their long term prospects, or what they can afford. The math says it doesn’t matter because an acceptable amount of the loans will perform and applicants can either accept the high rate or get nothing.

How I portray Wonga is not what I think of the merchant lending market in the US but rather I believe they’re a good example of the trap that merchant lenders COULD fall into if they come into too much money. When I first began to hear lenders fresh off a capital raise saying they wanted to fund the sh*t out of small business and would do anything in their power to fund as many deals as possible, I fear they could end up disrupting communities more than they could help them.

You know that thing called the Internet?

You know that thing called the Internet?

So I’ve talked a lot about what lenders don’t know but nothing about what they can learn. There is an unbelievable amount of free data available on the web that can collectively be used as a strong indicator of future business performance. You know those all important customers I spoke about earlier? The ones that make a business a business? Well lucky for us, they seem to go online and offer feedback about their experiences. Yelp, Zagat, and Facebook come to mind.

How is a business REALLY doing? Reviews will tell you a lot so long as there are enough of them, and not just the star meter, but the actual written reviews. I assure you that it will help a lender if they see that the last 10 reviews say that the owner is a no good lying crook that stopped paying his employees and punched a customer just the other night. A business’s whole reputation can’t be assessed from paperwork and credit scores, but it can be by hearing from people in the local community. That community is online.

That brings me to another point here. If a small business isn’t online, then no faith should be put in that small business in 2013. I don’t know why there are still so many small businesses out there that don’t use e-mail, don’t have a website, and don’t participate on social networks. Unless their shtick is that they are an Amish style operation striving for authenticity, then not being online should be an indicator that they do not care much about their long-term success. I would go so far as to say that any business that does not have at least a website, business fan page on Facebook, twitter account, or a reasonable substitute should be automatically declined for financing. Yeah, I said it!

In 2013, ignoring the Internet is like opening a store with no sign, boarding up the windows, and surrounding the front door with barbed wire. Sure, the locals might know you’re there and be smart enough to come in the back door, and maybe they’re enough to keep your business stable but no one else will find you and the ones that do, will see that you have no interest in being something more. You don’t have to be on every social network but if you’re not on any, you’re doing something wrong. Ideally, you should be somewhat active with your customers online too. This doesn’t mean sending each person that dined at a restaurant a Thank-You e-mail, but it does mean addressing complaints if there are any, posting announcements so customers can see them, and taking steps to improve your reputation.

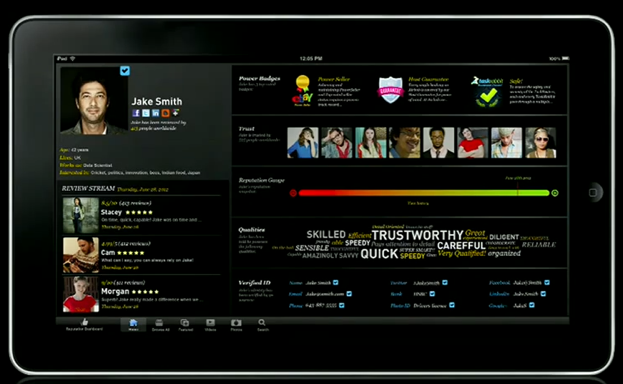

There are many, many trust and reputation signals online. At the most recent TED Conference, Rachel Botsman talked about collaborative consumption, trust, and reputation. She believes that trust is the most vital currency in our economy, not the money in your bank account, but trust. I highly recommend you watch it below. You should definitely take notice of what may eventually become a reality, an individual’s reputation scorecard, a report that aggregates reviews from everyone you’ve ever had an exchange with, and one that has the ability to evaluate the transactions which have the most meaning. My stellar e-bay seller record going back to 1999 might be on there (72 rave reviews baby!) but they won’t be as important if you’re looking to determine how credible I am as a business lending analyst. Still, in the grand scheme of reputation, they could have their place if someone wanted to gauge how trustworthy I am to deliver on something I agreed to.

Release the darn data

You want to know who is holding out on making the merchant lending industry and American economy a better place? The North American Merchant Advance Association (NAMAA) is. NAMAA possesses a database of every merchant that has defaulted or gone delinquent with a funding member in the last 4 years. There’s thousands of names in it. Not a member of NAMAA? You won’t get to know if a merchant has tried some funny stuff with another funder or gone out of business while having an advance.

But you want to know who this private bank of data hurts most? It hurts every business and wholesaler these merchants work with in the future. A month after a retail store fraudulently skips out on a $100,000 advance, that same retailer could apply for 60 day terms with a supplier and sign a 5 year lease for a new business location. Don’t that supplier and landlord deserve to know that their “awesome” new client has a reputation for committing theft and fraud as recent as 30 days ago? I think it’s our duty to let them know. NAMAA is withholding information that could prevent a lot of unreputable people from doing further harm in local economies. Make this data public and we’ll allow suppliers, landlords, and other lenders to make more informed decisions.

But you want to know who this private bank of data hurts most? It hurts every business and wholesaler these merchants work with in the future. A month after a retail store fraudulently skips out on a $100,000 advance, that same retailer could apply for 60 day terms with a supplier and sign a 5 year lease for a new business location. Don’t that supplier and landlord deserve to know that their “awesome” new client has a reputation for committing theft and fraud as recent as 30 days ago? I think it’s our duty to let them know. NAMAA is withholding information that could prevent a lot of unreputable people from doing further harm in local economies. Make this data public and we’ll allow suppliers, landlords, and other lenders to make more informed decisions.

I’ve heard the argument that privacy can be a big selling point to borrowers. They don’t necessarily want outsiders to know that they borrowed money or to suffer the shame if they don’t pay it back. I can understand the benefits of privacy from a competitive standpoint for a borrower but it defies all logic and reason for a lender to keep a default under tight wraps. Public record of a default discourages borrowers from defaulting in the first place and is helpful to everyone that may interact with that borrower in some way in the future. How many merchants would reconsider signing on the dotted line for $50,000 if they knew a default meant the lender would personally message all of their fans on Facebook to tell them about it? Is this wrong? Is this any of the customers business? What if their customers were paying for services 12 weeks in advance? Would their customers have the same confidence that their service would be rendered knowing this new information? It is likely that some customers would view a default as a sign that the business cannot deliver on their promises and reconsider using them. By not letting them know, you are putting them all at risk of paying for services they might not get.

Even though everyone hates me, I project 300% growth!

Show an underwriter a chart of sales projections for the next two years and they’ll have no idea if it’s just wishful thinking. All the demographic research in the world won’t convince the bank that people will trust your product. Show an underwriter that 50, 100, or a thousand people are saying positive things about their experience with you online, and they might believe you’re on to something. Time in business, cash flow, profitability, and positive credit history show what someone did and what they have, but reputation and trust reveal what someone’s success in the future will be like.

It’s not just what they say about you

Your reputation goes beyond just what people are saying about you. At some point, you’ll talk back and what you say can clue lenders into who you are and what you are doing. I’ve caught a few business announcements on Facebook that went something like “To our loyal customers, we are making a last ditch effort to get a merchant cash advance to pay off our landlord by Friday and keep the business open. If it does not happen, then we want to thank you all for your support over the years as we will close for good.” Yeah, it’s interesting to see things like this after you just had a 15 minute conversation with that same person that claimed the funds would be used for a marketing campaign.

With hundreds of millions of dollars burning a hole in their pocket, a lender may be tempted to take the Wonga approach. I guarantee Wonga would say I wasted my time by examining a business owner’s social interactions. They’d say there were statistics and data that show they should fund that business anyway because the FICO score and sales volume are within their parameters, that defaults were acceptable and built into the numbers, and that funding as many businesses as fast as you can above a certain interest rate, is better than funding fewer businesses with more appropriate terms.

This is the premise of my inefficient merchant lending hypothesis for lenders that get real sloppy when they have too much money. Would you rather be a lender that charges more, funds more, and knows less about your borrowers or would you rather charge less, fund more intelligently, and know more about who you’re funding? The first road accepts that you will outright devastate a percentage of your customers, disrupt local economies, and leave a bad taste in the mouth of a handful of people. It might be profitable, but could you really claim to be a helper of small business?

When you fund EVERYONE, businesses with bad reputations can knock out competitors with good reputations, the cost of debt can harm more than it helps, or lenders can get skinned alive by defaults they never saw coming. We need to be aware that there are consequences to backing a business with a bad reputation because it can allow them to squeeze out the guys that would’ve actually had the most positive impact on a community. The counter argument may be the theory by the philosopher Adam Smith, a gentleman famous for promoting economic principles such that the pursuit of self-interest promotes the good of society. By this standard, if it’s good for the lender, then ultimately it must be good for the economy. However, allowing yourself to devastate a percentage of your customers isn’t good for the lender’s reputation even if it’s profitable. In a sense, pursuing immediate profit doesn’t mean pursuing ones self-interest. It may be months or years before enough unsatisfied borrowers begin to affect your reputation as a whole. Eventually, public opinion will sway. It’s happening to Wonga right now. If a lender’s business practices today could force them out of business in 5 years, then they are not pursuing their self-interest.

When you fund EVERYONE, businesses with bad reputations can knock out competitors with good reputations, the cost of debt can harm more than it helps, or lenders can get skinned alive by defaults they never saw coming. We need to be aware that there are consequences to backing a business with a bad reputation because it can allow them to squeeze out the guys that would’ve actually had the most positive impact on a community. The counter argument may be the theory by the philosopher Adam Smith, a gentleman famous for promoting economic principles such that the pursuit of self-interest promotes the good of society. By this standard, if it’s good for the lender, then ultimately it must be good for the economy. However, allowing yourself to devastate a percentage of your customers isn’t good for the lender’s reputation even if it’s profitable. In a sense, pursuing immediate profit doesn’t mean pursuing ones self-interest. It may be months or years before enough unsatisfied borrowers begin to affect your reputation as a whole. Eventually, public opinion will sway. It’s happening to Wonga right now. If a lender’s business practices today could force them out of business in 5 years, then they are not pursuing their self-interest.

Real predictions, not just hoping tomorrow’s financial standing will be the same as it was yesterday

I look forward to the day when a merchant lender announces a 3, 5, or 7 year program. Their underwriting analysis would have to be incredibly well thought out, but that’s not a bad thing. Borrowers shouldn’t be forced to choose between an 8 month loan and a 9 month loan because so few lenders are willing to make real long-term projections. A business might make good use of short term financing to pay for an aggressive marketing campaign, but the likelihood that they could “open a 2nd store” and pay back all of the money with interest in 4 months isn’t very good.

My advice to the merchant lenders that are flexing their hundred million dollar muscles right now? Don’t carpet bomb the entire country with loans and hope that a one-size fits all rate and term will have a positive impact on the economy. It won’t. Writing off a portion of your customers today as collateral damage will hurt your reputation in the long run. Some businesses shouldn’t be getting funded even if they have money in the bank and a history of revenue. Others can’t sustain such short term repayments. These things should matter not just in the context of how much it will impact profits, but how much it will impact communities.

Incorporating factors like trust and reputation don’t have to slow the application process down. There are technologies to help aggregate, sort, and make sense of these signals online. Automation and speed are good but the day that lenders stop caring about who they’re funding and why they’re funding them is the day that lending becomes inefficient. When it becomes purely a numbers game, we’ll be in bubble territory. Can you think of any other industries where lenders stopped considering whether or not the loans were good for their borrowers and played the numbers? I’m sure you can 😉

Incorporating factors like trust and reputation don’t have to slow the application process down. There are technologies to help aggregate, sort, and make sense of these signals online. Automation and speed are good but the day that lenders stop caring about who they’re funding and why they’re funding them is the day that lending becomes inefficient. When it becomes purely a numbers game, we’ll be in bubble territory. Can you think of any other industries where lenders stopped considering whether or not the loans were good for their borrowers and played the numbers? I’m sure you can 😉

Lend efficiently, be a good citizen, and don’t be afraid to place a value on what customers are saying about your applicants.

– Merchant Processing Resource

https://debanked.com

MPR.mobi on iPhone, iPad, and Android

MCA Industry More Fractured

February 1, 2013 Everyone agrees that the Merchant Cash Advance (MCA) industry has grown substantially over the last few years. Our best calculations estimated that $600 million in MCA deals took place in 2010. Some believed that figure was too low, especially when Capital Access Network (CAN) projected they would fund $700 million all by themselves in 2012. Could CAN really be funding more alone than what the entire industry including them funded in 2010?

Everyone agrees that the Merchant Cash Advance (MCA) industry has grown substantially over the last few years. Our best calculations estimated that $600 million in MCA deals took place in 2010. Some believed that figure was too low, especially when Capital Access Network (CAN) projected they would fund $700 million all by themselves in 2012. Could CAN really be funding more alone than what the entire industry including them funded in 2010?

The debate starts there because they have put a large focus on their NewLogic subsidiary, a company that specializes in short term loans, not MCAs. And like NewLogic, much of the growth the industry experienced in the last few years has not been centered around split-funding purchases of credit card sales, but on the alternatives. We’ve made it a point in previous articles to point out the lack of consensus on what the product is being called now, especially since everyone is offering their own version of short term financing. We even went so far as to say that by 2015, the term MCA won’t even exist anymore. We may have exaggerated a bit, but after playing around with Google’s Trends tool, we realized that prediction was much more than a hunch.

If MCA has grown so much in the last few years, why is it that 38% more people searched for MCA on Google in December 2007 than they did in December 2012? Why is it that searches for MCA information peaked in February 2009 and never recovered? According to Google’s search data, nearly 50% fewer searches are being made for MCA today than there were three years ago.

Notice that MCA as a term did not really exist on the Internet prior to June 2007. We presented our estimate of when that term was coined in Before it was Mainstream. It first appeared in print in May 2005, but didn’t pick up traction until March, 2006 in private Internet forums. The first Merchant Cash Advance Internet blog began in July 2007, weeks before people began to first start searching for information about the term. It is very likely they were also trying find the blog itself.

So is Google’s data just plain wrong? Is something fishy? The only thing wrong is the belief that the MCA industry is just about MCAs. The creation of alternatives and the recent practice of private labeling have contributed to the decline of MCA.

three new terms: merchant loans, ach loan, merchant financing

Business Cash Advance takes a dive. Seriously, who calls it that anymore? Merchant Funding is on the way back up.

There were 500% more searches for small business loans in April 2004 than there were in December 2012.

So what does this all mean? We leave you to draw your own conclusions. 2007-2009 was a period of sudden mass awareness of MCA but there has never been as much money in the industry as there is now. There are experts that say business owners feel that the recession never ended, causing them to continue hunkering down instead of seeking financing to expand. There are insiders who will attribute this to the negative stigma the product had and the need to call it something else. We believe the most likely suspect though, is the fracturing of the MCA industry. It’s possible that people aren’t typing “small business loans” or “merchant cash advance” into Google because so many companies are promoting alternative financing options that people are looking for those specific products instead.

Whatever the answer is, it appears that alternative business financing has grown tremendously but the MCA term has not. Share your thoughts about this with us. We want to hear theories.

– Merchant Processing Resource

https://debanked.com

MPR.mobi on iPhone, iPad, and Android

Wonga Retreats

January 30, 2013 For about a month, we’ve discussed the merger negotiations between On Deck Capital and UK based lender, Wonga. It seems now that our quest to evaluate Wonga’s potential success in the US was all for naught. BusinessWeek reported yesterday that the deal is off after a price disagreement. The only figure known to us is the amount originally publicized in November at $250 million. We hope our readers realize that we made a lot of fuss about this merger because it was said to be in an advanced stage months ago.

For about a month, we’ve discussed the merger negotiations between On Deck Capital and UK based lender, Wonga. It seems now that our quest to evaluate Wonga’s potential success in the US was all for naught. BusinessWeek reported yesterday that the deal is off after a price disagreement. The only figure known to us is the amount originally publicized in November at $250 million. We hope our readers realize that we made a lot of fuss about this merger because it was said to be in an advanced stage months ago.

With the deal dead, it has become evident that something was gained by all of this, and that is the valuable insight from Merchant Cash Advance (MCA) veterans on a range of topics. LinkedIn lit up like a light bulb when it came to debating UK lending practices and algorithmic underwriting. Below are a few snippets from the conversation:

There are significant cultural and other differences between MCA and small business lending in the UK and the US that work against a purely algorithmic MCA underwriting model in the US. In the UK, most small businesses have been established or owned for generations – or longer. Imagine underwriting a pub that has been in existence for 200 years, or a bucolic inn in the Scottish highlands that has been owned by the same family for over 100 years. The entrepreneurial culture in the US where anyone who needs a job starts a small business – and applies for a cash advance – doesn’t exist in the UK.

The rates MCA companies charge is less of an issue in the UK, there is more alternative finance that is generally accepted and rates are not objected to, which is probably why Wonga doesn’t have an issue with the rates they charge, and when borrowers don’t have a problem with the rate they are less likely to feel entitled to default. Also borrowers don’t move as much in the UK and tend to be much more stable in their communities and banking relationships which is correlative to default in the US. Lastly we saw very little fraud in the UK, which is a significant underwriting issue in the US. It will be interesting to see if this deal gets done and what Wonga might do in the US market with their business intelligence, but it may not be as easy as they think.

Our company uses a algorithm to help with our underwriting practices, but there is something to be said about the personal touch when it comes to merchant cash advance space.

After several years of researching the U.K. marketplace and preparing for significant differences—including no UCC filings–what I found were striking similarities. These included resistance to higher (than bank) fees, switching processors, mistrust of terms or the agreement (sale and purchase of future credit card receipts), difficulty recruiting referral partners or ISO s, etc. There were, however, two very important differences between the U.S. and European business models. The first, as J. Brown points out, is cultural. The European attitude toward debt assumption and repayment is more “responsible” than it is in the U.S. Many Pubs and Inns in the U.K. have been in the family for generations. Additionally, there are over 10,000 India restaurants in the U.K. most are run by hard working families. These are considered “honorable” professions and defaulting on an obligation is not “proper.” The second is product distribution and monitoring the performance of the distribution channels. In the U.K. distribution channels were “business referral partners.”

Automation and the proper utilization of technology is certainly the backbone to having a viable and more importantly scalable lending business. I do have however disagree that algorithms and data can completely eliminate the review of a file by a human brain. The ability to ascertain the credit worthiness, borrowing ability and most importantly likelihood of repayment of a business differs vastly from the consumer finance space.

Credit goes to J. Brown, F. Capozza, M. Landau, H. Francis, and everyone else for excellent input on these subjects.

Previous Wonga Articles:

Made for Each Other? 12/12/12

Funding Down to a Science 12/21/12

Not Science 1/14/13

– Merchant Processing Resource

https://debanked.com

MPR.mobi on iPhone, iPad, and Android

Not Science

January 14, 2013 We’ve published 2 articles recently about UK based lender, Wonga. In both, we expressed awe at their scientific algorithm that makes loans in 15 minutes without human interaction. Now we’re not sure that praise is deserved. A Guardian article recently revealed that their top secret super computer racked up 41% bad debt in 2011 as a percentage of annual revenue. 41%, a number that equates to 76.8 million pounds in write-offs. That’s apparently 4x higher than what it was in the previous year.

We’ve published 2 articles recently about UK based lender, Wonga. In both, we expressed awe at their scientific algorithm that makes loans in 15 minutes without human interaction. Now we’re not sure that praise is deserved. A Guardian article recently revealed that their top secret super computer racked up 41% bad debt in 2011 as a percentage of annual revenue. 41%, a number that equates to 76.8 million pounds in write-offs. That’s apparently 4x higher than what it was in the previous year.

Is this science? Charge a high enough interest rate and you’re bound to find a balance between bad debt and profit. This isn’t science. This is what the average man calls rolling the dice. The problem with this strategy in the US is that most states cap the maximum interest rate so you can’t force a profit by charging an unlimited APR. Besides, there is proof that the worse the economy gets, the more their defaults pile up. Shouldn’t their algorithm factor in an economic downturn? What will their P&L look like in 2012 and 2013?

For years, we’ve made the case that aggressive lenders who make a point to grab market share while boasting of their dominance are the first to get smoked in the market. For some reason we let our guard down on this one. Maybe it had something to do with it being a British company. Believe it or not Wonga is still profitable, but to claim there is some kind of magic behind what they do is wishful thinking. To take a blogger’s words about this:

I’m sure Wonga would much rather it could know in advance who was going to default. Then it could charge its non-defaulting customers a lot less for its service.

Wonga apparently can’t do what it claims it is best at. Congrats on earning a profit Wonga, but here’s some words of advice about lending in the US. Technology is great, but don’t lend without humans. Trust us.

—–

Previous Wonga Posts:

Funding Down to a Science

Made For Each Other?

Surprise! We Are the Market

January 13, 2013Merchant Cash Advance (MCA) is an alternative to a small business loan. Look around. MCA players have spent so much energy on gaining mainstream acceptance, that we’ve become oblivious to reality. We ARE the small business lending market. There are alternatives out there such as credit cards and SBA loans, but they are industries of their own. Small businesses in 2013 really only have one place to obtain fast unsecured short term financing, and that’s here, the MCA industry. That assumes of course that you agree with our definition of MCA, which we stopped limiting to a purchase of future credit card sales some time ago.

Over the past few months, we began to realize that the only small business lenders making headlines are people we know. Is the country that small or does MCA dominate the market that much?

A glimpse at the sponsored advertisements on Bing in the NYC region:

Where are the multi-billion dollar banks? If $15 a click isn’t in their budget, something is wrong, and it may possibly be due to the fact that business loans aren’t on their priority lists.

Lenders, brokers, and bankers on the front lines can’t stop talking about MCA. It is a recurring theme in their columns:

The alternative financing industry is growing rapidly and, I believe, will continue to grow in 2013. These lenders are extremely entrepreneurial and are leaving the banks behind with their speed and use of technology. Many are backed by premier investment banks and Silicon Valley venture capital powerhouses — investors who understand that entrepreneurs and small-business owners are throwing up their hands in frustration over how long it can take to get a loan from a bank, especially if the loan is backed by the S.B.A. More and more businesses are willing to pay the price of the alternative lenders just to be able to get their capital and move on.

-Ami Kassar

The State of Small Business Lending – NY Times 1/8/13

Ami’s Column on NY Times

Cash advance companies, accounts receivable financiers, factors, and micro lenders all have become increasingly more attractive funders for three reasons: flexibility, use of technology, and speed.

-Rohit Arora

Three Reasons for the Rise of Alternative Lending – Fox Business 11/29/12

Rohit’s column on Fox Business

Here’s a dilemma that might have contributed to the growth of MCA… Banks don’t like offering loans and business owners don’t like applying for them if it’s hard:

There’s a large small business segment that needs and wants to borrow on a commercial basis, but their needs are very small. Business owners want $10,000, $20,000 or $30,000 loan–the average is somewhere around $25,000. Traditionally, that’s been a very unprofitable business for a bank. Some banks argue that they are willing to lose money on those loans because they can make it up in deposits. But what happens when the borrower has no deposits? It’s a very tough balancing act.

– The Federal Reserve Bank of San Francisco

A newsletter report that reveals banks lose money on small business loans

Community Investments Volume 8; No 4; Fall 1996

Business owners say the documentation involved is overwhelming. They’ve also found the qualification terms almost impossible to meet.

– Catherine Clifford

Feedback reveals that a burdensome application process and extensive paperwork requirements are enough to discourage business owners even if the loans carry 0% interest.

CNN 1/26/10

Thousands of researchers publish statistics on bank lending every month. Not only do they all contradict each other but journalists that use this data to make bold claims often fail to acknowledge that an increase in bank lending has nothing to do with the applicants, the economy, or the banks themselves. It has to do with the Government. We all know that the SBA will cover the losses banks incur, but there are programs that go one step further. The Federal Government actually bribes banks to make loans. For example, the Small Business Lending Fund is a dedicated investment fund that encourages lending to small businesses by providing capital to community banks. Meaning, covering the losses on defaults doesn’t seem to be enough, so they’ll actually provide the money to make the loans as well.

Click to see full size on mobile

According to the SBA, small business bank borrowing totaled $584.1 billion in the third quarter of 2012. That number dwarfs the volume produced by the MCA industry, but its not an apples to apples comparison. A loan of $1 million dollars is within the range of a small business loan by the SBA, an amount atypical (though not impossible) in the MCA world. Banks are also prodded and coddled by the Government so much that it has reached the extent that we dare claim they are an extension of the Federal Government itself. There’s some food for thought for the Occupy Wall Street movement! They also conveniently got bailed out when they were on the verge of failure, a safety net that MCA companies don’t have.

According to the SBA, small business bank borrowing totaled $584.1 billion in the third quarter of 2012. That number dwarfs the volume produced by the MCA industry, but its not an apples to apples comparison. A loan of $1 million dollars is within the range of a small business loan by the SBA, an amount atypical (though not impossible) in the MCA world. Banks are also prodded and coddled by the Government so much that it has reached the extent that we dare claim they are an extension of the Federal Government itself. There’s some food for thought for the Occupy Wall Street movement! They also conveniently got bailed out when they were on the verge of failure, a safety net that MCA companies don’t have.

Subtract the Federal Government’s meddling and there is only one profitable form of B2B lending, Merchant Cash Advance. That is of course again if you accept our definition. There are many young B2B lending firms that claim to be an alternative to MCA, who then go on to describe their product in a manner that is textbook MCA.

Our thesis may be debatable and lacking in concrete proof, but we’re not writing dissertations here. Business owners are increasingly looking to the Internet for loan information and it’s obvious what they’re finding. One would expect a quick Internet search to bring up ads for the billion dollar powerhouses, you know the ones that are given millions to lend out and then millions again when the loans go bad. Instead we find companies owned by friends or friends of friends. The small business loan market isn’t run by anonymous Wall Street kingpins, it’s run by a small community of entrepreneurs that all started from the ground up. Only the community isn’t so small anymore. There was once a handful of MCA companies claiming to be an alternative to a small business loan. Now there are a handful of companies claiming to be an alternative to MCA. It doesn’t take a genius to figure out why that is. After years of fighting to be recognized in the market, something remarkable happened, we became the market itself…

– Merchant Processing Resource

https://debanked.com