The Inefficient Merchant Lending Market Theory

There are 4 major factors used to determine approvals in the merchant lending market:

• FICO Score / Credit Report history of owners

• Monthly Gross Revenue

• Time in Business

• Average Daily Bank Balance

Only 1 of these factors considers the applicant’s reputation, and that’s credit reports. Credit reports reveal past payment history with other creditors. They show lawsuits, unpaid taxes, and bankruptcies. Knowing whether an applicant pays on time or not is valuable to lenders but it fails to reveal an even more important metric, the business’s ability to generate future profits. If you’re shaking your head and saying “credit reports aren’t for that purpose,” I would respond by asking which of the 4 factors then is?

The amount of money deposited in someone’s bank account in the past reveals how much they took in, but it doesn’t indicate what will happen in the future. Similarly, a substantial daily ending bank balance may show responsibility to maintain a cash cushion, but it says nothing about how likely customers are to buy from that business in the future.

Could time in business then tell us? Is it safe to assume that a business that has been operational for a year, two years, or five years will be there for many more years to come? The local auto mechanic that’s been around for 5 years may only have lasted because no one else has gotten around to opening up a rival auto shop. Would it be safe to give the most hated mechanic in town a three year loan when their success is simply the result of being the only auto mechanic in the community? There may be somewhat of a correlation between time in business and customer satisfaction but it is by no means strong enough to predict future success.

In effect, the major metrics used to judge small businesses for financing today take no consideration of the number one thing that matters to a business for survival, customers. Without customers, the amount deposited historically means nothing. Without customers, a 700 FICO score cannot produce sales, profits, or money to repay a loan. Without customers, a 50 year old restaurant can’t continue to stay open just because it’s been there for 50 years. And without customers you better hope that $1 million in sales last year made you really rich, since without customers, you’re going to need to start a new business… preferably one WITH customers.

This doesn’t mean that these 4 factors are irrelevant, they’re not. But I believe these factors combined are but a tiny sliver of data to predict how well a business will do in the future and at the same time repay a loan. Relying on weak indicators forces lenders to charge higher rates since they must compensate for the risk of unknowns. It also decreases the length of time that lenders can trust their borrowers to hold their money for.

It is no surprise then that loan terms in the merchant lending industry only range from 3 to 12 months. None of the lenders are able to predict how their borrowers are going to do far into the future, so they bank on the odds that sales and deposits in the next few months will mimic sales and deposits in the last few months. That’s also the reason why there are a lot of test/starter/trial funding rounds that are short to witness how a merchant “does” before funding additional capital on a longer term. Underwriters are flying blind. They have to see how you do because they have no data to suggest what will happen.

The big firms do have SOME data by now, but they’re broad statistics that say a certain industry in a certain region is likely to perform X with a Y margin of error. Or FICO scores below 600 are likely to have a Z rate of default. Yet this data also ignores a business’s reputation and relationship with its customers. It applies a blanket assumption of performance over the period of 3 to 12 months. These statistics are highly important to a lender because they can use them to predict defaults and delinquencies as a whole and enable them to set rates that will cover all of it and then some.

The big firms do have SOME data by now, but they’re broad statistics that say a certain industry in a certain region is likely to perform X with a Y margin of error. Or FICO scores below 600 are likely to have a Z rate of default. Yet this data also ignores a business’s reputation and relationship with its customers. It applies a blanket assumption of performance over the period of 3 to 12 months. These statistics are highly important to a lender because they can use them to predict defaults and delinquencies as a whole and enable them to set rates that will cover all of it and then some.

The owner of an ISO once asked me, “Wouldn’t it be great if we got to the point where we were funding every business in America?” My answer was “No.” If 10, 20, or 30% of those businesses failed to repay or eventually went out of business (and they would if you funded everyone) and the lender STILL made money, then the ones in good standing had to of gotten charged way too much. It would also mean that there had to be a portion of performing loans that were actually distressing the borrower, causing the capital they obtained to work against them, rather than for them. The goal shouldn’t be to fund EVERYONE, but rather to fund the few that could truly benefit.

A great example of doing it wrong is Wonga, a UK based lender that accepted a 41% rate of bad debt in 2011 while still managing to reap £62.4 million in profit. If Wonga had a few hundred bucks, a few thousand bucks, or heck only a million, they’d probably be very careful about who they approved and why they approved them. But venture capital changes the game and not always in a positive way. Putting a few hundred million dollars in the hands of Wonga has caused them to become incredibly inefficient.

Why should they only fund 5,000 people through a highly comprehensive underwriting process when they can fund 30,000 people with a one-size fits all rate, ask no questions, and accept that they will burn a lot of their customers along the way? This is the question they must have asked themselves years ago. (You can read the founder’s interview HERE)

At some point when they were developing their business model they had to admit that they really didn’t care what the outcome would be for their borrowers, so long as the business made money. And so they created an algorithm that would statistically predict the rate of default based on weak indicators like demographics, how they answered a few questions, and credit score and the resulting delinquencies were just necessary casualties to make the system work. In essence, Wonga knows they will devastate a portion of their customers and accepts this. They’re like a restaurant that only sells sugar frosted donut cheese ice cream to obese people and accepts that 41% of their revenues will be lost due to their customers dying. Can a lender truly be helping a community or economy where it intentionally hurts a percentage of borrowers because it’s still profitable at the end of the day? Do their contests, soccer sponsorships, and positive messaging on social media make up for their disruption to the economy?

Wonga’s mission is to grab market share, a strategy to make holy their blanket performance statistics and the rate that has to be charged to make money. Every single individual in the country becomes a candidate for their loans even though the lender will never know anything about the individual borrowers, their long term prospects, or what they can afford. The math says it doesn’t matter because an acceptable amount of the loans will perform and applicants can either accept the high rate or get nothing.

How I portray Wonga is not what I think of the merchant lending market in the US but rather I believe they’re a good example of the trap that merchant lenders COULD fall into if they come into too much money. When I first began to hear lenders fresh off a capital raise saying they wanted to fund the sh*t out of small business and would do anything in their power to fund as many deals as possible, I fear they could end up disrupting communities more than they could help them.

You know that thing called the Internet?

You know that thing called the Internet?

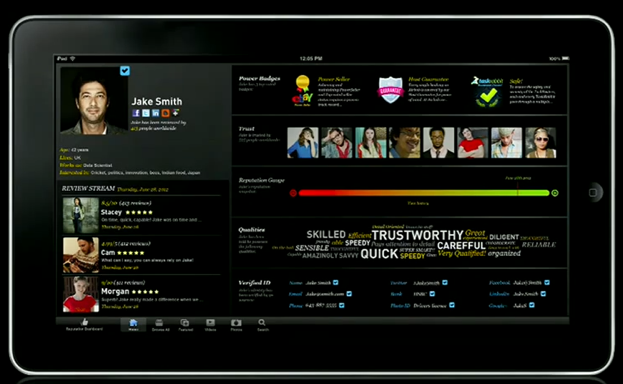

So I’ve talked a lot about what lenders don’t know but nothing about what they can learn. There is an unbelievable amount of free data available on the web that can collectively be used as a strong indicator of future business performance. You know those all important customers I spoke about earlier? The ones that make a business a business? Well lucky for us, they seem to go online and offer feedback about their experiences. Yelp, Zagat, and Facebook come to mind.

How is a business REALLY doing? Reviews will tell you a lot so long as there are enough of them, and not just the star meter, but the actual written reviews. I assure you that it will help a lender if they see that the last 10 reviews say that the owner is a no good lying crook that stopped paying his employees and punched a customer just the other night. A business’s whole reputation can’t be assessed from paperwork and credit scores, but it can be by hearing from people in the local community. That community is online.

That brings me to another point here. If a small business isn’t online, then no faith should be put in that small business in 2013. I don’t know why there are still so many small businesses out there that don’t use e-mail, don’t have a website, and don’t participate on social networks. Unless their shtick is that they are an Amish style operation striving for authenticity, then not being online should be an indicator that they do not care much about their long-term success. I would go so far as to say that any business that does not have at least a website, business fan page on Facebook, twitter account, or a reasonable substitute should be automatically declined for financing. Yeah, I said it!

In 2013, ignoring the Internet is like opening a store with no sign, boarding up the windows, and surrounding the front door with barbed wire. Sure, the locals might know you’re there and be smart enough to come in the back door, and maybe they’re enough to keep your business stable but no one else will find you and the ones that do, will see that you have no interest in being something more. You don’t have to be on every social network but if you’re not on any, you’re doing something wrong. Ideally, you should be somewhat active with your customers online too. This doesn’t mean sending each person that dined at a restaurant a Thank-You e-mail, but it does mean addressing complaints if there are any, posting announcements so customers can see them, and taking steps to improve your reputation.

There are many, many trust and reputation signals online. At the most recent TED Conference, Rachel Botsman talked about collaborative consumption, trust, and reputation. She believes that trust is the most vital currency in our economy, not the money in your bank account, but trust. I highly recommend you watch it below. You should definitely take notice of what may eventually become a reality, an individual’s reputation scorecard, a report that aggregates reviews from everyone you’ve ever had an exchange with, and one that has the ability to evaluate the transactions which have the most meaning. My stellar e-bay seller record going back to 1999 might be on there (72 rave reviews baby!) but they won’t be as important if you’re looking to determine how credible I am as a business lending analyst. Still, in the grand scheme of reputation, they could have their place if someone wanted to gauge how trustworthy I am to deliver on something I agreed to.

Release the darn data

You want to know who is holding out on making the merchant lending industry and American economy a better place? The North American Merchant Advance Association (NAMAA) is. NAMAA possesses a database of every merchant that has defaulted or gone delinquent with a funding member in the last 4 years. There’s thousands of names in it. Not a member of NAMAA? You won’t get to know if a merchant has tried some funny stuff with another funder or gone out of business while having an advance.

But you want to know who this private bank of data hurts most? It hurts every business and wholesaler these merchants work with in the future. A month after a retail store fraudulently skips out on a $100,000 advance, that same retailer could apply for 60 day terms with a supplier and sign a 5 year lease for a new business location. Don’t that supplier and landlord deserve to know that their “awesome” new client has a reputation for committing theft and fraud as recent as 30 days ago? I think it’s our duty to let them know. NAMAA is withholding information that could prevent a lot of unreputable people from doing further harm in local economies. Make this data public and we’ll allow suppliers, landlords, and other lenders to make more informed decisions.

But you want to know who this private bank of data hurts most? It hurts every business and wholesaler these merchants work with in the future. A month after a retail store fraudulently skips out on a $100,000 advance, that same retailer could apply for 60 day terms with a supplier and sign a 5 year lease for a new business location. Don’t that supplier and landlord deserve to know that their “awesome” new client has a reputation for committing theft and fraud as recent as 30 days ago? I think it’s our duty to let them know. NAMAA is withholding information that could prevent a lot of unreputable people from doing further harm in local economies. Make this data public and we’ll allow suppliers, landlords, and other lenders to make more informed decisions.

I’ve heard the argument that privacy can be a big selling point to borrowers. They don’t necessarily want outsiders to know that they borrowed money or to suffer the shame if they don’t pay it back. I can understand the benefits of privacy from a competitive standpoint for a borrower but it defies all logic and reason for a lender to keep a default under tight wraps. Public record of a default discourages borrowers from defaulting in the first place and is helpful to everyone that may interact with that borrower in some way in the future. How many merchants would reconsider signing on the dotted line for $50,000 if they knew a default meant the lender would personally message all of their fans on Facebook to tell them about it? Is this wrong? Is this any of the customers business? What if their customers were paying for services 12 weeks in advance? Would their customers have the same confidence that their service would be rendered knowing this new information? It is likely that some customers would view a default as a sign that the business cannot deliver on their promises and reconsider using them. By not letting them know, you are putting them all at risk of paying for services they might not get.

Even though everyone hates me, I project 300% growth!

Show an underwriter a chart of sales projections for the next two years and they’ll have no idea if it’s just wishful thinking. All the demographic research in the world won’t convince the bank that people will trust your product. Show an underwriter that 50, 100, or a thousand people are saying positive things about their experience with you online, and they might believe you’re on to something. Time in business, cash flow, profitability, and positive credit history show what someone did and what they have, but reputation and trust reveal what someone’s success in the future will be like.

It’s not just what they say about you

Your reputation goes beyond just what people are saying about you. At some point, you’ll talk back and what you say can clue lenders into who you are and what you are doing. I’ve caught a few business announcements on Facebook that went something like “To our loyal customers, we are making a last ditch effort to get a merchant cash advance to pay off our landlord by Friday and keep the business open. If it does not happen, then we want to thank you all for your support over the years as we will close for good.” Yeah, it’s interesting to see things like this after you just had a 15 minute conversation with that same person that claimed the funds would be used for a marketing campaign.

With hundreds of millions of dollars burning a hole in their pocket, a lender may be tempted to take the Wonga approach. I guarantee Wonga would say I wasted my time by examining a business owner’s social interactions. They’d say there were statistics and data that show they should fund that business anyway because the FICO score and sales volume are within their parameters, that defaults were acceptable and built into the numbers, and that funding as many businesses as fast as you can above a certain interest rate, is better than funding fewer businesses with more appropriate terms.

This is the premise of my inefficient merchant lending hypothesis for lenders that get real sloppy when they have too much money. Would you rather be a lender that charges more, funds more, and knows less about your borrowers or would you rather charge less, fund more intelligently, and know more about who you’re funding? The first road accepts that you will outright devastate a percentage of your customers, disrupt local economies, and leave a bad taste in the mouth of a handful of people. It might be profitable, but could you really claim to be a helper of small business?

When you fund EVERYONE, businesses with bad reputations can knock out competitors with good reputations, the cost of debt can harm more than it helps, or lenders can get skinned alive by defaults they never saw coming. We need to be aware that there are consequences to backing a business with a bad reputation because it can allow them to squeeze out the guys that would’ve actually had the most positive impact on a community. The counter argument may be the theory by the philosopher Adam Smith, a gentleman famous for promoting economic principles such that the pursuit of self-interest promotes the good of society. By this standard, if it’s good for the lender, then ultimately it must be good for the economy. However, allowing yourself to devastate a percentage of your customers isn’t good for the lender’s reputation even if it’s profitable. In a sense, pursuing immediate profit doesn’t mean pursuing ones self-interest. It may be months or years before enough unsatisfied borrowers begin to affect your reputation as a whole. Eventually, public opinion will sway. It’s happening to Wonga right now. If a lender’s business practices today could force them out of business in 5 years, then they are not pursuing their self-interest.

When you fund EVERYONE, businesses with bad reputations can knock out competitors with good reputations, the cost of debt can harm more than it helps, or lenders can get skinned alive by defaults they never saw coming. We need to be aware that there are consequences to backing a business with a bad reputation because it can allow them to squeeze out the guys that would’ve actually had the most positive impact on a community. The counter argument may be the theory by the philosopher Adam Smith, a gentleman famous for promoting economic principles such that the pursuit of self-interest promotes the good of society. By this standard, if it’s good for the lender, then ultimately it must be good for the economy. However, allowing yourself to devastate a percentage of your customers isn’t good for the lender’s reputation even if it’s profitable. In a sense, pursuing immediate profit doesn’t mean pursuing ones self-interest. It may be months or years before enough unsatisfied borrowers begin to affect your reputation as a whole. Eventually, public opinion will sway. It’s happening to Wonga right now. If a lender’s business practices today could force them out of business in 5 years, then they are not pursuing their self-interest.

Real predictions, not just hoping tomorrow’s financial standing will be the same as it was yesterday

I look forward to the day when a merchant lender announces a 3, 5, or 7 year program. Their underwriting analysis would have to be incredibly well thought out, but that’s not a bad thing. Borrowers shouldn’t be forced to choose between an 8 month loan and a 9 month loan because so few lenders are willing to make real long-term projections. A business might make good use of short term financing to pay for an aggressive marketing campaign, but the likelihood that they could “open a 2nd store” and pay back all of the money with interest in 4 months isn’t very good.

My advice to the merchant lenders that are flexing their hundred million dollar muscles right now? Don’t carpet bomb the entire country with loans and hope that a one-size fits all rate and term will have a positive impact on the economy. It won’t. Writing off a portion of your customers today as collateral damage will hurt your reputation in the long run. Some businesses shouldn’t be getting funded even if they have money in the bank and a history of revenue. Others can’t sustain such short term repayments. These things should matter not just in the context of how much it will impact profits, but how much it will impact communities.

Incorporating factors like trust and reputation don’t have to slow the application process down. There are technologies to help aggregate, sort, and make sense of these signals online. Automation and speed are good but the day that lenders stop caring about who they’re funding and why they’re funding them is the day that lending becomes inefficient. When it becomes purely a numbers game, we’ll be in bubble territory. Can you think of any other industries where lenders stopped considering whether or not the loans were good for their borrowers and played the numbers? I’m sure you can 😉

Incorporating factors like trust and reputation don’t have to slow the application process down. There are technologies to help aggregate, sort, and make sense of these signals online. Automation and speed are good but the day that lenders stop caring about who they’re funding and why they’re funding them is the day that lending becomes inefficient. When it becomes purely a numbers game, we’ll be in bubble territory. Can you think of any other industries where lenders stopped considering whether or not the loans were good for their borrowers and played the numbers? I’m sure you can 😉

Lend efficiently, be a good citizen, and don’t be afraid to place a value on what customers are saying about your applicants.

– Merchant Processing Resource

https://debanked.com

MPR.mobi on iPhone, iPad, and Android

Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.