Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

SCORCHED EARTH – Controversial Bill Could Eliminate Marketplace Lending, Merchant Cash Advance and Nonbank Business Loans in Illinois (and starve small businesses in the process)

April 9, 2016

The State of Illinois wants to make it a Class A misdemeanor for providing small businesses with quick, easy working capital.

The world’s strangest bill, dubbed the Small Business Lending Act, could send marketplace lenders, nonbanks, and merchant cash advance companies to prison for up to 1 year if applicants don’t submit at the very least, their most recent six months bank statements, the previous year’s tax return, a current P&L, a current balance sheet, and an accounts receivable aging.

Loans in which the monthly payments exceed at least 50% of the business’s monthly net income would be illegal, which implies that any business that is either breaking even or running at a loss would be banned from obtaining a loan from alternative sources.

This is not an April Fools’ prank. Not even preemption granted under the National Bank Act or Federal Deposit Insurance Act is safe.

Introduced into the State Senate under the pretense that it would squash predatory lenders, the bill’s licensing and compliance proposal would also effectively outlaw marketplace lending and securitizations by making the sale of loans illegal unless it’s to a bank or another state-licensed party. Even merchant cash advances are referenced specifically but almost as an afterthought and defined in such a way that even traditional factoring companies may be in jeopardy.

No licensee or other person shall pledge, assign, hypothecate, or sell a small business loan entered into under this Act by a borrower except to another licensee under this Act, a licensee under the Sales Finance Agency Act, a bank, savings bank, community development financial institution, savings and loan association, or credit union created under the laws of this State or the United States, or to other persons or entities authorized by the Secretary in writing. Sales of such small business loans by licensees under this Act or other persons shall be made by agreement in writing and shall authorize the Secretary to examine the loan documents so hypothecated, pledged, or sold.

At a time when most fintech lenders are advocating for smart regulation, the State of Illinois apparently wants to end all nonbank commercial finance under $250,000 completely, with the exception of one organization (which we’ll get to shortly).

At a time when most fintech lenders are advocating for smart regulation, the State of Illinois apparently wants to end all nonbank commercial finance under $250,000 completely, with the exception of one organization (which we’ll get to shortly).

There are some exemptions granted under this proposal of course. Loans over $250,000 aren’t subject to it, nor are any loans made by Illinois-based banks or credit unions, that is unless they are acting as the agent for another party like say perhaps a marketplace lender.

Hidden inside is also an exemption for nonprofit lenders, a loophole left open for Accion Chicago, the nonprofit masterminds behind the bill who seem to want the entire state’s lending market all for themselves.

Illinois State Senator Jacqueline Collins Introduced This Bill

Senator Collins introduced the legislation as an amendment to Senate Bill 2865 on April 6th. A former journalist, she’s now the chairwoman of the Illinois Senate Financial Institutions Committee. Among her self-professed accolades is that she “has played a key role in addressing predatory lending and high foreclosure rates in Chicago through legislation that protects homebuyers and homeowners with subprime mortgages.” She lists the Mortgage Rescue Fraud Act, the landmark Sudan Divestment Act and the Payday Loan Reform Act among her major legislative accomplishments.

It’s no surprise then that sections of the bill are borrowed straight out of the Payday Loan Reform Act. Collins isn’t acting on her own however…

Chicago City Treasurer Kurt Summers

In January, Senator Collins joined Chicago City Treasurer Kurt Summers in a call for “new legislation to protect small business owners from misleading and dishonest predatory lenders.” In a closed-door hearing, the committee supposedly heard from business owners, advocates and elected officials on predatory lending.

“Chicago’s small business community deserves protection from the unchecked greed of predatory lenders,” Treasurer Summers said. “While access to capital is the number one concern of small business owners across the state, bank and commercial loans continue to decline, steering them to underhanded lenders. As we continue to urge banking partners to increase their local investment, this new, common-sense legislation would ensure transparency in lending that so often puts our entrepreneurs at risk.”

Of note is his use of the phrase “banking partners” since this bill has bankers all over it, as we’ll get into shortly. Summers represents the Chicago Mayor’s office and the Mayor’s office says they’ve launched this campaign thanks to partners like Accion Chicago.

Hon. Kurt Summers, Treasurer, City of Chicago from City Club of Chicago on Vimeo.

Accion Chicago and the Mayor’s Office

Last year, Mayor Rahm Emanuel announced a joint campaign with Accion Chicago to help small businesses avoid predatory lending.

Accion Chicago, ironically makes business loans themselves, having originated 535 loans totaling $4.8 million in 2014 with a maximum loan size of $100,000.

Who is Accion Chicago really?

The Small Business Lending Act virtually ensures that small business loans under $250,000 only be facilitated by banks and nonprofits. Isn’t it convenient then that Accion Chicago is not only a nonprofit, but also funded and staffed by banks?

According to their 2014 annual report, Citibank and JPMorgan Chase were two of their three largest supporters (the third was the US Treasury!). Below are some of the figures:

$100,000+

- Citibank

- JPMorgan Chase

$50,000 – $99,999

- Bank of America

$20,000 – $49,999

- Fifth Third Bank

- PNC Bank

- U.S. Bank

$5,000 – $19,999

- American Chartered Bank

- Alliant Credit Union

- BMO Harris Bank

- First Bank of Highland Park

- First Eagle Bank

- First Midwest Bank

- Ridgestone Bank

- State Bank of India

- The PrivateBank

- Wells Fargo Bank

About a dozen more banks gave less than $5,000.

JPMorgan Chase has also been a partner of the annual Taste of Accion fundraising event, and was the lead sponsor in 2014, a spot that costs $30,000. Benefactor sponsorships which cost $20,000 each were comprised of American Chartered Bank, Capital One, Northern Trust Company, and Wintrust Bank. And the lesser sponsorships? Again, mostly banks.

JPMorgan Chase has also been a partner of the annual Taste of Accion fundraising event, and was the lead sponsor in 2014, a spot that costs $30,000. Benefactor sponsorships which cost $20,000 each were comprised of American Chartered Bank, Capital One, Northern Trust Company, and Wintrust Bank. And the lesser sponsorships? Again, mostly banks.

You know who hasn’t donated to Accion Chicago? Marketplace lenders and merchant cash advance companies.

Accion Chicago raised only $1.4 million in 2014 from public support, the bulk of which came from banks or related traditional financial institutions. So is it just a coincidence that this predatory lending bill they’re supporting grants exemptions to all the banks from compliance?

Accion Chicago’s 2014 Board of Directors includes executives from:

- American Chartered Bank (chairman)

- First Eagle Bank

- JPMorgan Chase

- Ridgestone Bank

- MB Financial Bank

- Talmer Bank & trust

- Citibank

- First Midwest Bank

The 2014 committees were made up almost entirely of bank executives from:

- First Eagle Bank

- The PrivateBank

- Ridgestone Bank

- U.S. Bank

- JPMorgan Chase

- Forest Park National Bank & Trust Co.

- MB Financial Bank

- FirstMerit Bank

- Wintrust Bank

- Standard Bank & Trust Co.

- First Midwest Bank

- Wells Fargo Bank

- Seaway Bank & Trust Co.

- Metropolitan Capital Bank

- Evergreen Bank Group

- First Financial Bank

- PNC Bank

Thanks to the impartial work of these good citizens, they have discovered that small businesses should only be working with banks or nonprofits funded and staffed by banks and have craftily devised a bill to legislate all the alternatives out of existence.

If this was really about predatory lending, then they screwed up big time

All coincidences aside, some of the bill’s rules have nothing to do with protecting borrowers, like the required $500,000 surety bond to become licensed for example. Compare that to California’s $25,000 licensed lender surety bond. And the restriction on being able to sell or securitize a loan, how does that help small businesses?

These requirements and others suggest that it’s about preventing all alternatives from existing in the marketplace, rather than predatory alternatives. The losers would undoubtedly be small businesses and the Illinois job market. Senator Collins and Treasurer Summers, both of whom have a strong track record of empowering their constituents financially, may have underestimated or overlooked the likely negative consequences of this bill.

The nonbanks

Several nonbank trade groups are reportedly in the process of formulating a response.

The Commercial Finance Coalition for example, a nonprofit coalition of financial technology companies, told deBanked that they are concerned about the impact this will have on the Illinois job market and will indeed have representatives on the ground in Illinois.

They also wanted to make known that they welcome support from marketplace lenders, nonbanks and merchant cash advance companies in these efforts and that interested parties should email Mary Donahue at mdonohue@commercialfinancecoalition.com

To contact Senator Jacqueline Collins who introduced the bill, call her at 217-782-1607.

LendingRobot is Now Your On-The-Go Marketplace Lending Robo-Advisor

April 8, 2016

Checking your marketplace lending portfolio is now as easy as checking a stock quote

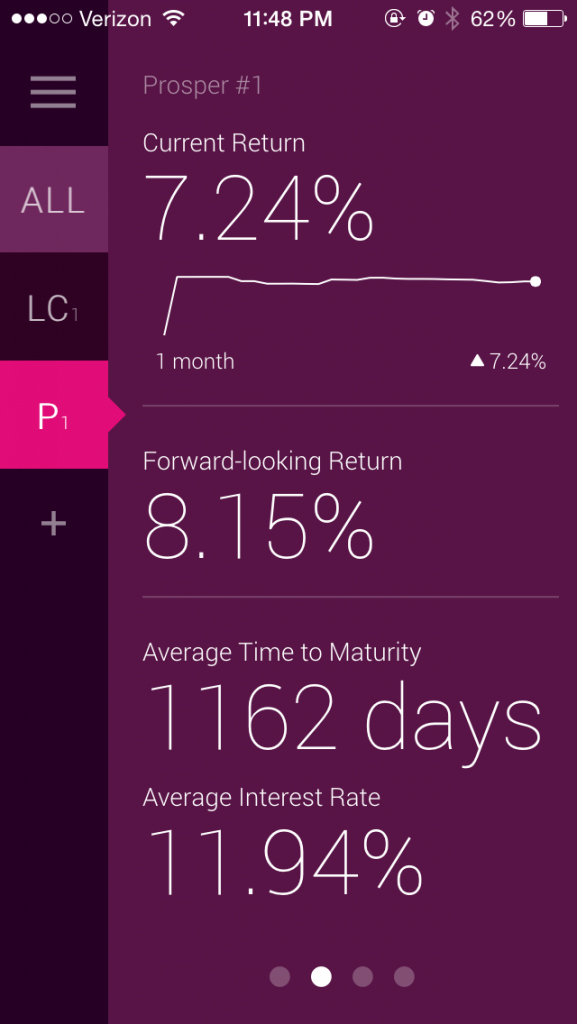

Marketplace Lending just became a little bit more friendly for investors thanks to LendingRobot’s new mobile app. The app allows investors to track the daily performance of their Lending Club, Prosper and Funding Circle portfolios all in one place. Its utility valued is bolstered by the fact that none of the three integrated platforms have published their own investor-oriented mobile apps, which came as a surprise even to LendingRobot CEO Emmanuel Marot.

The app complements the existing web service where investors can set custom filters to automatically buy notes that meet their criteria from the platforms whenever they become available. To date, more than 5,000 investors have signed up to use LendingRobot and more than $80 million of their collective investments are being measured by the service. Most of those users have only integrated their Lending Club or Prosper portfolios as of now, and not just because Funding Circle is a new addition, but also because their model is slightly different. “You have to be an accredited investor,” Marot said of using Funding Circle. There is no such requirement for the other two platforms.

The app complements the existing web service where investors can set custom filters to automatically buy notes that meet their criteria from the platforms whenever they become available. To date, more than 5,000 investors have signed up to use LendingRobot and more than $80 million of their collective investments are being measured by the service. Most of those users have only integrated their Lending Club or Prosper portfolios as of now, and not just because Funding Circle is a new addition, but also because their model is slightly different. “You have to be an accredited investor,” Marot said of using Funding Circle. There is no such requirement for the other two platforms.

The app is unique because it makes your aggregate marketplace lending portfolio data as handy as the latest stock quote. “It was kind of surprising actually for us to see that we have about 30% of our clients coming several times per week just to check it,” Marot said.

But perhaps as adoption of marketplace lending continues to catch on as part of a normal everyday diversified investment strategy, this will become more of a trend. For investors with large portfolios for example, the robo-advisor is likely acquiring notes for them multiple times per day every day, increasing the likelihood an investor will want to check in regularly to see how they’re doing.

Along with calculating the aggregate and individualized returns based on formulas that LendingRobot devised themselves, users can quickly refer to a baseline value known as their “portfolio health.” This number is not based on some proprietary advanced formula, Marot explained, but is rather the straightforward percentage of notes that are in good standing relative to all “live” notes. Charged-off notes are no longer considered live, Marot said.

Along with calculating the aggregate and individualized returns based on formulas that LendingRobot devised themselves, users can quickly refer to a baseline value known as their “portfolio health.” This number is not based on some proprietary advanced formula, Marot explained, but is rather the straightforward percentage of notes that are in good standing relative to all “live” notes. Charged-off notes are no longer considered live, Marot said.

Users can also check their portfolio composition, the average time to maturity and the average interest rate being assessed, in addition to being able to review raw figures such as how many notes became late in the last week or paid in full, for example.

Lending Club, Prosper and Funding Circle are just the beginning, Marot said, while expressing optimism about adding other platforms in the future. They saw the original three platforms they’re integrated with now as being a good fit because they are “safe.” “We are very cautious,” he said. Notably, those companies are also the three founders of the newly formed Marketplace Lending Association, of which he voiced support for.

Michael Raneri, a PwC Managing Director and Fintech Advisory Lead, wrote on Forbes that millennials will serve as early adopters for robo-advisors. “The next generation of investors has been quick to embrace new technologies and experiences, and this should apply to robo-advisors,” he wrote. “Furthermore, millennials have a general mistrust of large financial institutions, particularly in the wake of the financial crisis of 2008. Unlike their parents, who forged close relationships with advisors—even using their phones to have conversations with them, as primitive as that sounds—millennials are equally comfortable with making digital connections. They’ve been conditioned to accept that technology can match the performance of its human predecessors, while offering reduced fees and providing greater convenience.”

Marketplace Lending Association Formed to Defend Investor Marketplaces

April 6, 2016

Funding Circle, Lending Club and Prosper have joined forces to create a collaborative non-profit body, i.e. a trade association. Its mission is “to promote a more transparent, efficient, and customer-friendly financial system by supporting the responsible growth of marketplace lending, fostering innovation in financial technology, and encouraging sound public policy.”

Among the already available resources on the association’s website is a white paper dictating “operating standards.”

The standards are broken down into five broad categories:

- Investor Transparency and Fairness

- Responsible Lending

- Safety and Soundness

- Governance and Controls

- Risk Management

The group’s initial members are notable because Prosper only does consumer loans and Funding Circle only does business loans. Lending Club bridges the gap by doing a combination of both. That means that the group’s prospective membership will be fantastically broad. After all, what does a commercial lender providing capital to a $10 million/year business have in common with a personal lender helping a single mother refinance a credit card? The answer is their investor base.

All 3 companies allow investors to invest in loans on their respective marketplaces and lo and behold “investor transparency and fairness” is the first, foremost and most detailed category of their white paper.

All 3 companies allow investors to invest in loans on their respective marketplaces and lo and behold “investor transparency and fairness” is the first, foremost and most detailed category of their white paper.

Indeed, one requirement to join the association is to be matching 75% of loans, by dollar, with commitments for funding from investors before the loans are issued.

The Marketplace Lending Association therefore probably seeks above all else, permanent acceptance of the ability for investors to buy loans or securities backed by loans in online marketplaces.

And it’s no wonder, just last week SEC Chairman Mary Jo White questioned these marketplaces during a keynote speech at Stanford University. “We expect that investors will receive disclosures about the loans underlying their investments, including information about the borrowers as well as the platform’s proprietary risk and lending models, that will enable them to make informed investment decisions – both at the time of investment and on an ongoing basis,” she said.

The SEC is not alone in their interest, hence the need for and now the emergence of, a Marketplace Lending Association.

Business Loan Brokers Encounter Hard Times

April 6, 2016 Feeling a little bearish about the business lending industry lately? If you’re a business loan broker, you’re not alone.

Feeling a little bearish about the business lending industry lately? If you’re a business loan broker, you’re not alone.

Marketing costs are going up while the response rates of marketing are generally going down. It’s a trend that’s lightly covered in the March/April issue of our magazine that has just been dropped in the mail. But there’s more to it. Several recent new broker shops have failed or are failing within just their first few months of operation. Employers have become more litigious with former employees, alleging violations of non-competes and/or non-solicit agreements, and at least one sales agent apparently went too far and was arrested in early February for backdooring deals.

The number of emails deBanked has received about stolen commissions, rogue employees and general grievances has shot up in recent months, and on one industry forum, sales agents are now publicly voicing their frustrations. One thread that was aptly titled, Merchant cash advance crushed me, was posted by a discouraged broker. “I’ve been in this business for a year and I can say this is the hardest thing I’ve ever done from a business perspective,” he said. One user responded by saying, “fail rate is very high. Competition is crazy. If you can’t spend money on marketing, including a sizable outbound sales force, you are a dead duck.”

“The market has changed,” said Fundzio CEO Eddie Siegel to deBanked in the previous issue. “The cost of capital has gotten a lot lower for the customer, and since there are more brokers in the marketplace they are willing to take a lesser amount just to get the deal to the finish line.”

“A lot of brokers are carpet bombing, they’re on the phone all day,” said Blindbid President Michael O’Hare. “I talked to one guy who said he makes 400 or 500 calls a day on a manual dial.”

In an environment of more calls, lower response rates and lower commissions, it’s no surprise that outrage over backdoored deals has overshadowed stacking as the industry’s most pressing issue.

Even funders have stepped up their legal pursuit of other funders through allegations of tortious interference. Whether such cases have merit is for the courts to decide, but they are a sign of the times that money is no longer raining from the sky. Lines are being drawn. In a market where everyone was once a winner, now there must be losers.

Even funders have stepped up their legal pursuit of other funders through allegations of tortious interference. Whether such cases have merit is for the courts to decide, but they are a sign of the times that money is no longer raining from the sky. Lines are being drawn. In a market where everyone was once a winner, now there must be losers.

Even the political atmosphere is changing. In just the last few months, the Small Business Finance Association has hired an executive director and two additional new advocacy groups were formed, the Commercial Finance Coalition and the Coalition for Responsible Business Finance.

“A few years ago, individual brokers could be making $20,000 or even $40,000 a month. Now those numbers are much more difficult to reach unless brokers have a unique lead generation method or their own money to participate in the deals,” said Zachary Ramirez, a vice president at World Business Lenders.

Of course, it’s not bad for everyone. In February, deBanked featured a sales closer whose team collectively originated $47 million in deals last year. He’s not alone. Veteran players, particularly those that have been in the industry for nearly a decade acknowledge that they have first mover advantage over the newer entrants because their portfolios are so big or they have weathered the bumps and don’t get as frustrated by them.

Funders that know the pains brokers are going through are attempting to address it in their marketing, with some assuring their prospective partners that they have no inside sales force, and thus no way to steal a deal. For those with inside sales forces, they are relying on their well established reputations to do the talking.

Anonymous deal soliciting has been mostly outlawed on industry forums to curtail bad experiences, but they still happen on other mediums. One broker complained on LinkedIn this week that a lead generator based in the Philippines had allegedly pocketed his $2,500 upfront fee and then changed their phone number and disappeared. That lead generator is still advertising his wares through social media.

If that’s not a sign of the times, then I don’t know what is.

Senator Elizabeth Warren Rips Former Protégé in CFPB Debate

April 6, 2016 Massachusetts Senator Elizabeth Warren was forced to confront an unexpected witness yesterday in a Senate hearing over consumer finance regulations, former protégé Leonard Chanin. Chanin, who was there to testify about why he believed the Consumer Financial Protection Bureau (CFPB) was acting outside its intended scope, was accused by Warren of being the person responsible for not catching the entire 2008 financial crisis.

Massachusetts Senator Elizabeth Warren was forced to confront an unexpected witness yesterday in a Senate hearing over consumer finance regulations, former protégé Leonard Chanin. Chanin, who was there to testify about why he believed the Consumer Financial Protection Bureau (CFPB) was acting outside its intended scope, was accused by Warren of being the person responsible for not catching the entire 2008 financial crisis.

“Of all the people who might be called on to advise Congress about how to weigh the costs and benefits of consumer regulations, I am surprised that my Republican colleagues would choose a witness who might have one of the worst track records in history on this issue,” Warren said.

Of note however, is that after the financial crisis, she herself hired Chanin to be the CFPB’s rule-writer after he came highly recommended for his service as the deputy director of the Federal Reserve’s Division of Consumer and Community Affairs. “I’m also pleased to have Leonard Chanin playing a key role in building an effective and efficient rule writing team,” she said back in December 2010.

Chanin spent nearly 20 years at the Fed and received a Federal Reserve Board Special Achievement Award for his work on the Truth in Savings Act.

“So my question is, given your track record at the Fed, why should anyone take you seriously now?” she asked Chanin, even while acknowledging that she had hired him previously based upon that same track record.

Chanin is now an attorney at Morrison & Foerster LLP.

The CFPB is often attributed as being Warren’s brainchild and she is believed to be a contender for Vice President on the Democratic ticket.

Watch the exchange between Warren and Chanin below:

The APR Enigma Confuses Everyone – Even Lenders

April 3, 2016

A study published by Lendio last week confirmed the results found in recent government studies, that small businesses are confused by Annual Percentage Rates. But they’re not alone…

It might be time to reconsider the calls for APR standards in small business lending. In a recent survey of 1,000 small business owners, only 17.4% of respondents chose APR as the easiest method to understand the cost. The vast majority selected the total net dollar cost of the loan as being the easiest.

The data matches the results found in a study conducted by the Federal Reserve Bank of Cleveland last year, in which small business owners generally responded that there was nothing confusing about a loan when cost was presented as a total dollar value. It was interest rates that tripped them up, the Fed determined.

When attempting to answer questions about the total amount owed and interest rates, participants became notably less confident in their ability to make an informed borrowing decision, with many qualifying their answers or indicating they were “not sure.”

– Federal Reserve Conclusion from Alternative Lending through the Eyes of “Mom-and-Pop” Small-Business Owners 8/25/15

Additionally in the Fed study, small business owners guessed the interest rate of a presented hypothetical loan to be anywhere from 5% to 50%, with some saying they just didn’t know. All of them were wrong. An analyst for the Federal Reserve Bank later acknowledged that it was a trick question. “The correct answer is that ‘it depends on how long it takes to pay back,'” said Ellyn Terry, an economic policy analysis specialist. The Fed report itself had to be amended more than a month later because this question and the answers produced in the study were confusing to even the sophisticated parties trying to make sense of it. That amendment reads as follows:

*Note: In practice, for a credit product structured like Product A, the effective interest rate varies depending on how long it takes a borrower to repay which, in turn, depends on the volume and timing of credit card sales receipts. Simply put, the interest owed on Product A is 30% of the principal value, but assuming consistent monthly sales and daily payments, the effective interest rate is on the order of 60%, and higher if funds are repaid sooner than one year. (Added 9.29.2015)

Does that clear it up for you??? Even the added note intended to make the interest rate question more clear is confusing. Small business owners never stood a chance…

But it seems those on the lending side of things are confused too.

Lendio CEO Brock Blake followed up his study with a blog post on LendAcademy to try and articulate the implications of the findings. Titled, Communicating the Cost of Capital in Alternative Lending, Blake was roasted in the comments for comparing a 6-month loan to a 5-year loan by those presumably involved in lending themselves.

Apparently, math is very subjective

In an example Blake used to illustrate a point, he gave a 6-month loan an Effective APR of 83% and a 5-year loan an Effective APR of 19%. Critics eager to point out holes in his argument challenged the fundamental numbers used to construct it.

“By the way, I tried to verify the APR of that #1 loan, and I get 137.03%, not 83%. Has anyone else tried to verify this calculation?”

“I ran the numbers on #1 but came up with a different number altogether. I think the error is in total cost of capital, which should be $4,500 vs. $4,016. With 22% simple interest, interest paid would be $3,960 plus the $540 origination fee.”

One set of facts, 4 different opinions on APR. How can this be?

In sparking this debate, Blake may not have fully convinced readers that a 6-month high-APR loan can be better than a 5-year low-APR loan, but he did unintentionally demonstrate support for his study’s findings, that APR as a universal measurement is flawed since even those that believe they understand it came up with different percentages than their peers.

Consider that the Federal Reserve study referenced above implied to business owners that APR is simply an abbreviation for interest rate, which isn’t true. “When it comes to borrowing for the short term, are you more comfortable knowing the interest rate (APR) or total cost of repayment?” it asked those polled.

Bad form

Bad form

The Truth in Lending Act (TILA) makes a clear distinction between an APR and an interest rate. “Since an APR measures the total cost of credit, including costs such as transaction charges or premiums for credit guarantee insurance, it is not an ‘interest’ rate, as that term is generally used.” Well then why are they presented as the same thing in a Fed study measuring comprehension of loan costs?

Note also that only one of the Fed study’s mock products mentioned an APR and only in the context of an Effective APR, something that the Fed has long known to be confusing. In April 2006, Macro International (now ICF International) was hired by the Fed to examine the comprehensibility of these very formulas.

One of the most consistent findings was that very few participants understood the meaning of an Effective APR (At that time known as the Fee-Inclusive APR). “Participants had a wide variety of incorrect interpretation of these percentages, including that they were the interest rates that would be paid on fees, penalty rates that would be charged if late payments were made, or the percentages of total transactions that were made of each type.”

It got worse though, because “in addition to a general lack of understanding of the [Effective APR], qualitative testing also found several instances when participants confused this term with their nominal APR for a given transaction.”

But it’s gotten better right?

For all of the studies conducted and regulations implemented, one might expect that banks, which bear the brunt of disclosure requirements in the financial world, would receive the highest marks on transparency. But that’s not the case. Another study, one jointly published by seven Federal Reserve banks, found that dissatisfied business borrowers were slightly more likely to encounter transparency issues with large banks than they were with online lenders.

Bankers probably aren’t surprised by that

Last Fall, B. Doyle Mitchell Jr, who spoke on behalf of the Independent Community Bankers of America during a House subcommittee hearing, said that new loan disclosures [required by Dodd-Frank] was not making it easier for borrowers to understand, to the point that they don’t even know what they are signing anymore. “In fact it is even more cumbersome for them now,” he said.

Non-bank lending critic Ami Kassar has publicly claimed that lenders are simply afraid of disclosing APRs because they don’t want their borrowers to know the real cost.

The data indicates however that borrowers don’t know what to make of APRs. Worse, the issue seems to be a universal one, one that confounds consumers, business owners, government surveyors and those within the lending industry itself.

APRs also struggle to remain relevant as a measure for short term loans. For example, OnDeck CEO Noah Breslow has said that a six month loan with a 60% APR may actually only cost 15 cents on the dollar. “The APR overstates the actual cost of the loan to the borrower,” he previously told Forbes.

“Asked which method was easiest to understand, two-thirds of respondents chose total payback amount,” Lendio’s survey concluded.

That seems to be the trend indeed.

Marketplace Lenders Played Everyone for April Fools

April 2, 2016Friday, April 1st, transported the marketplace lending industry into another dimension, one that made us all April Fools. Here’s some of the believable and not so believable jokes that you might have missed:

A federal judge granted a temporary injunction to halt the entire marketplace lending industry

A late-night meeting on Capitol Hill between representatives of three big banks and several members of Congress quickly spiraled out of control, resulting in an emergency hearing that temporarily shuttered the marketplace lending industry.

Donald Trump funded his presidential campaign with a loan from Prosper

Donald Trump funded his presidential campaign with a loan from Prosper

Trump didn’t need the money but he borrowed $35,000 anyway because the deal was too good to pass up.

Donald Trump addressed the Money20/20 Conference community

Make payments great again, said Trump.

Survey revealed that kids aged 1 to 4 are concerned about pre-school debt

Without formal credit history, CommonBond is underwriting pre-schoolers for loans based on their favorite character on Sesame Street. “My CommonBond consultant prepared me to make the transition to pre-school,” says Sawyer Thurston Howell III, a 2-year-old and CommonBond member since March 2016.

Loans now funded via drone delivery

As an alternative to ACH, Dealstruck has begun to transfer piles of money to approved borrowers via drones. “After my deal was funded, I logged on, popped in my address and a bag of cash arrived at my business in half an hour! I didn’t even have to go to the bank,” said one customer.

A free puppy with every loan

Borrowell is proud to announce that our loans will now come with a little something extra!https://t.co/CwEczxsxVo pic.twitter.com/nHArqBP1xr

— Borrowell (@Borrowell) April 1, 2016

Much to the disappointment of applicants, this was indeed an April Fools’ joke.

Of course with all the jokes being made out there on Friday, some people thought that OnDeck’s announcement that President Obama had joined their board of directors was also an April Fools’ joke. OnDeck actually made that announcement two days prior, but unfortunately for OnDeck, it didn’t pick up steam in the press until Friday, which by that point gave it the appearance of a prank.

Due to a federal law that prohibits certain presidential conflicts of interest, Obama’s board seat will not have voting power until after his term ends in January 2017. In an interview with the Wall Street Journal on Thursday, OnDeck CEO Noah Breslow denied rumors that Obama was actually being vetted to replace him as CEO. “We will absolutely value his expertise and experience, but it’s unrealistic to think that a former president will have the time to run a publicly traded company.”

Just kidding. April Fools!

Breaking News: Judge Grants Temporary Injunction to Halt Entire Marketplace Lending Industry

April 1, 2016April Fools 2016

A late night session on Capitol Hill has led to a catastrophic outcome for the marketplace lending industry.

A late night session on Capitol Hill has led to a catastrophic outcome for the marketplace lending industry.

At approximately 11:30 PM Thursday night, lobbyists working on behalf of Bank of America, Wells Fargo and TD Bank scheduled an emergency meeting with six members of Congress to discuss, among other issues, the impact of marketplace lending on their bottom lines. “Q1 earnings won’t officially be released for a while,” said Oregon Congressman Edward Duchovny, who was present, “but loan volumes were down across all three banks by a substantial percentage.”

The drops were so alarming, that each bank had initially concluded that their financial reports had been hacked. “They thought there was a security breach,” said a congressional staff member with knowledge of the meeting who was not authorized to speak on the record. “One bank’s consumer lending unit experienced a drop in originations by 50% year over year.”

Shortly after midnight, a team of bleary-eyed auditors and staff members from the Treasury Department concluded that the numbers were correct and that something nefarious was to blame. “We knew that something like this might happen,” said US Treasury forecast analyst Andrea Mitchells. “When we conducted the RFI last year, we met with some of the banks and flat out told them that marketplace lending was irreversibly changing how people borrow money.”

The revenue loss to banks from marketplace lenders in just the first quarter of this year may total as high as $947 Billion, Mitchells said, which warranted the attention of Federal Reserve Chairman Janet Yellen. Though it was the dead of night, Yellen arrived within the hour, along with a team of economists and attorneys.

“The atmosphere changed really quick,” said the anonymous congressional staff member. “One minute we were eating pizza and Chinese food while parsing these boring financial reports and the next minute Chairman Yellen is warning us all about the systemic threat this poses to the very notion of bank lending altogether.”

Yellen, two attorneys, and three of the six Congressmen present, including Edward Duchovny, arranged for an emergency hearing with a federal judge on the grounds that banks stood to suffer irreparable harm unless drastic temporary action was undertaken.

Within minutes, an attorney argued with a straight face that Bank of America might not even survive to see the market’s close on Friday, in part because almost all of its business had been “hijacked” by marketplace lenders. Judge Thomas McAdams III was clearly rattled by what he heard. “I have no idea what the hell marketplace lending even is,” McAdams pontificated from the bench. “It sounds like you’re just describing every single type of lending that exists and then just adding the word marketplace to it,” he shouted, while waving his gavel around.

Ads run by SoFi, a marketplace lender known mainly for student loans, had apparently inflicted devastating damage with their “Don’t Bank” campaign.

“People saw those advertisements and then actually decided not to bank,” said Jane Martin, SVP of TD Bank. “We thought we had a great case for a temporary restraining order.”

McAdams, who held everyone present in contempt of court, nonetheless granted a temporary injunction on all of marketplace lending.

“I think the judge did the right thing,” said Mitchells of the US Treasury.

Duchovny’s feelings however, were mixed. “I thought we were trying to stop people from lending money at supermarkets,” he said. “I asked Yellen if this would affect my loan with Lending Club and she just gave me the dirtiest look.”

Investors across the world from the US to China are bracing themselves for what is expected to be a tumultuous Friday for stocks.

APRIL FOOLS 🙂

{kind=link}