Online Lending

How LendingTree and SnapCap Crossed Paths

September 25, 2017 LendingTree in recent days revealed the acquisition of online platform for small business lending SnapCap’s non-lending assets in a $21 million deal, including $12 million upfront and $9 million in contingency payments. The deal gives online lending marketplace LendingTree more scale in the small business market ahead of what could shape up to be recovery in 2018.

LendingTree in recent days revealed the acquisition of online platform for small business lending SnapCap’s non-lending assets in a $21 million deal, including $12 million upfront and $9 million in contingency payments. The deal gives online lending marketplace LendingTree more scale in the small business market ahead of what could shape up to be recovery in 2018.

J.D. Moriarty, LendingTree Chief Financial Officer, told deBanked that SnapCap’s 20 employees will stay in Charleston, and the brand will remain intact. “For them, their employer just got both a whole lot more stable and scalable. As with anything we acquire, we will keep the brand in place and test it to see what is most effective,” said Moriarty.

LendingTree has been connecting small businesses with lenders since 2014, and the latest deal reflects a strategy to add scale.

“It’s a bit of what you might call an acqui-hire. LendingTree is growing quickly and scaling. We hired a really good team in SnapCap that will basically be our way of scaling in small business,” said Moriarty.

LendingTree is lifting its profile in the small business segment amid an industry transformation that is thinning the pack and has seen some players shifting gears entirely.

“Small business lending might do very well in 2018. And we are investing now to grow the base of our business. On a macro level, we expect our business to do well in 2018 regardless. But if small business lending recovers and suddenly you see companies like OnDeck doing well, we will benefit from that. But we position any acquisition assuming that the market doesn’t recover and the deal still must be attractive to us, even if the market continues to struggle.”

Moriarty went on to provide a glimpse into the financial structure of the deal.

“Last year, SnapCap set up a special purpose vehicle (SPV), which was funded by outside capital with which they would actually make loans. There’s a balance sheet aspect to that business we are not acquiring. But it was a small percentage of their business,” Moriarty explained.

Inside the Marketplace

LendingTree is largely known as a marketplace for mortgage loans where they represent about 50 percent of comparison shopping for mortgages. “That is how people think of us for sure,” said Moriarty. The revenue drivers have expanded in recent years, however.

For instance, mortgages used to account for 90 percent of revenue. Today, based on the most recent quarter, less than half of business originates from mortgages while the balance is in personal loans, credit cards, home equity, small business and auto loans.

LendingTree is no stranger to acquisitions, having done five such deals since June 2016. “What we’re trying to do is to build other marketplaces where people want to comparison shop,” said Moriarty.

But growth by acquisition is not their only growth strategy. “We’re growing period,” said Moriarty, adding that organic growth has been very good but small business in particular is a tough market to scale.

One of the recent deals, the acquisition of CompareCards a year ago, led them to gain market share in the credit card space. That deal also led LendingTree to SnapCap. CompareCards founder and president Chris Mettler and his wife own more than a one-third equity stake in SnapCap.

“SnapCap was introduced to us through Chris. He’s now a LendingTree employee. The introduction was absolutely from him. But it’s very consistent with our strategy, which we have conveyed to the market. We will continue to make small, accretive acquisitions and that will help us to gain scale in certain businesses and diversify,” said Moriarty.

Hybrid Model

While LendingTree and SnapCap both facilitate loans to the small business community, they take slightly different approaches to get there. “SnapCap’s core business is not unlike ours, meaning they are essentially finding high quality leads for lenders,” said Moriarty.

SnapCap uses a concierge model in which customers have a broker experience. They talk to someone at the company who helps them to identify a lender.

“LendingTree will be bigger and more scalable through both the traditional LendingTree model and SnapCap’s concierge approach. We will simply be able to serve lenders more effectively. If I’m a lender making small business loans, this is a pretty good thing.” he said.

SnapCap, meanwhile, is looking forward to the very same scale that LendingTree is targeting.

“The mission of SnapCap has always been to serve small business owners with access to funding. LendingTree’s leading online lending marketplace combined with SnapCap’s successful concierge model will enable us to serve an even wider range of business owners,” Hunter Stunzi, co-founder of SnapCap, told deBanked.

C-level Credit Exec Leaves Lending Club for Affirm

September 21, 2017Lending Club’s Chief Credit Officer and Interim General Manager, Sandeep Bhandari, has joined fintech lender Affirm, according to Affirm CEO Max Levchin. Levchin posted the following on LinkedIn:

I am excited to announce and welcome Sandeep Bhandari to Affirm, Inc. as Chief Strategy and Risk Officer (CSRO).

Sandeep joins us from Lending Club where he was the Chief Credit Officer (CCO). Prior to Lending Club, he was at Capital One for many years, where he was Assistant Chief Credit Officer at Capital One Bank (Credit Risk Management) and Venture Partner (Capital One Ventures). Prior to that Sandeep held a variety of roles requiring expertise in strategy, credit risk management, marketing, product development, and underwriting across several lines of business including consumer and small business credit card, auto lending, and mortgage and home equity lending.

We are excited for Sandeep to join us for our next phase of rapid growth and to help us fulfill our mission of delivering honest financial products that improve lives.

The move comes on the heels of Lending Club announcing their “most advanced and predictive credit model ever.” Bhandari was responsible for credit strategy and overall credit risk management at Lending Club and presumably would’ve overseen that.

Talkative investors on the LendAcademy forum were not immediately sold on Lending Club’s new system, however. Some users bemoaned that Lending Club is ignoring common sense in favor of data. In one instance, the CEO of PeerCube referenced an interest rate anomaly alleged to be discovered in Lending Club’s pricing as “Data-driven but knowledge-unaware.”

Affirm and Lending Club differ. Whereas Lending Club targets the credit card refinancing market, Affirm helps consumers finance purchases. Last month, Affirm and Walmart were reportedly in talks to offer financing to consumers.

What Will it Take to Grow OnDeck’s Stock Price?

September 20, 2017OnDeck closed at the exact same price on September 14th as it did on July 20th, $4.58. In between, OnDeck reported one of their best quarters ever (they released their 2nd quarter earnings on August 7th) and experienced a temporary boost to $5. Even then, the stock was 75% down from the IPO price and more than 80% down from their all-time high, yet that too couldn’t be sustained.

In Q2, OnDeck only had a GAAP net loss of $1.5 million and announced that they had expanded their collaboration with JPMorgan Chase for up to four years to provide the underlying technology supporting Chase’s online lending solution to its small business customers.

In the rest of the lending world, optimism is in style. Square is up 121% year-to-date, according to the deBanked Online Lender Tracker and even Lending Club is up 14%.

More traditional finance companies like American Express and Intuit are meanwhile hovering near their 52-week highs, according to the Specialty Business Lending Tracker.

Some of OnDeck’s former employees at least appear to be doing well. Just recently, the former Chief Sales Officer was named COO of CoverWallet, the former Director of External Sales was named Chief Revenue Officer of Pearl Capital and the former Director of Portfolio Management and Credit Operations was named SVP at Breakout Capital.

New CTO at Breakout Capital is Former CTO of Capital One Labs

September 18, 2017 Firoze Lafeer, the former Capital One Head of Tech Fellows Program and CTO, Capital One Labs, is now the CTO of Breakout Capital, a Breakout representative confirmed. Lafeer was with Capital One for five years, most recently running the company’s experimental product & technology incubator and accelerator.

Firoze Lafeer, the former Capital One Head of Tech Fellows Program and CTO, Capital One Labs, is now the CTO of Breakout Capital, a Breakout representative confirmed. Lafeer was with Capital One for five years, most recently running the company’s experimental product & technology incubator and accelerator.

Breakout Capital is a fintech small business lender based in Mclean, VA where Lafeer will lead technology, including scaling their tech platform.

Last month, Breakout hired Robert Fleischmann as Senior Vice President, Strategic Partnerships and Tom McCammon as Senior Vice President, Business Operations. Fleischmann was previously Director of Strategic Partnerships at RapidAdvance. McCammon was previously the Director of Portfolio Management and Credit Operations at OnDeck.

The Google Battle for Lending and SMB Finance Keywords

September 14, 2017The online lending battle is at least in part being fought online. Below is a chart of organic page 1 rankings in Google for some of the industry’s biggest players, banks, and the SBA. (Hat tip to Fundera and NerdWallet):

| Keywords | OnDeck | Kabbage | Fundera | Lending Club | NerdWallet | National Funding | Traditional Banks | SBA.gov |

| business loan | 1 | 9 | 3 | 5 | 4,7 | 6 | ||

| merchant cash advance | 2 | 3 | 4 | 8 | ||||

| working capital | 9 | 4 | ||||||

| commercial loan | 3 | 2,7 | ||||||

| small business loans | 2 | 3 | 5 | 7 | 1 | |||

| business line of credit | 3 | 2 | 11 | 1,4 | 6,7,8,9,10 | 5 | ||

| fast business loan | 1 | 4 | 2 | 5,6 | ||||

| business loan with bad credit | 7 | 1 | 2 | 3 |

The Top 10 Google Search Results for Merchant Cash Advance in February 2012 compared to now:

| February 2012 | September 2017 |

| MerchantCashinAdvance.com | Wikipedia |

| Yellowstone Capital | OnDeck |

| Entrust Cash Advance | Fundera |

| Merchants Capital Access | NerdWallet |

| Merchant Resources International | Businessloans.com |

| American Finance Solutions | Bond Street |

| Nations Advance | Capify |

| Bankcard Funding | National Funding |

| Rapid Capital Funding | CNN |

| Paramount Merchant Funding | CAN Capital |

The top result in 2012 is a great example of how much easier it was to game Google’s system back then. After achieving rank #1 for MCA and 300 other related keywords, MerchantCashInAdvance.com, which was just a lead generation site, sold for $75,000 in December 2011. The site was later clobbered by Google Penguin for black hat SEO and banished from visibility.

A major shift has obviously taken place over the last 5 and a half years. Is the search results game rigged to advance Google’s own interests? Three years ago I put forth my theory on that.

One thing that’s different between then and now is that Google now has 4 paid links above the organic search results as opposed to 3 and the paid links blend in more with the organic results. With the organic results pushed further down the page, they’re not as visible as they were five years ago.

Read my previous analyses on the industry’s search war over the years:

December 2015 Google Serves Low Blow to Merchant Cash Advance Seekers

March 2015 Google Culls Online Lenders – Pay or Else?

October 2014 Merchant Cash Advance SEO War Still Raging

August 2014 Six Signs Alternative Lending is Rigged: Do Lending Club and OnDeck have a helping hand?

October 2013 Google Penguin 2.1 takes swing at the MCA industry

August 2013 Your merchant cash advance press release may be hurting you

December 2012 Is Google your only web strategy?

July 2012 The other 93% [of leads]

April 2012 The SEO war continues

February 2012 The SEO War for Merchant Cash Advance: The first story on this topic

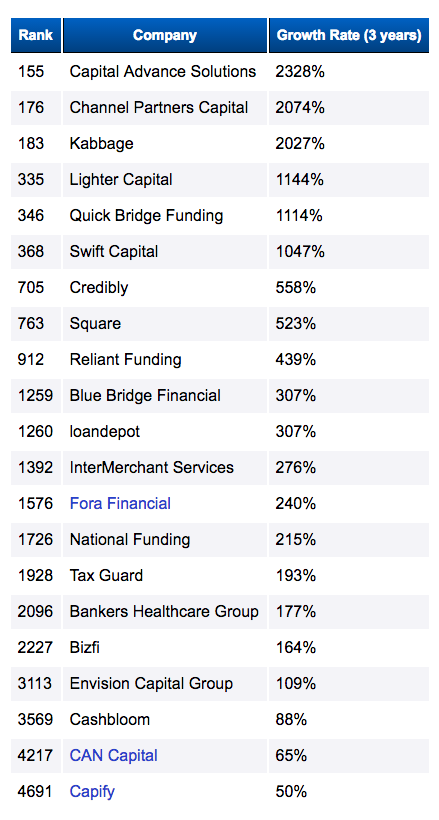

Where Alternative Finance Ranks on the Inc 5000 List

September 14, 2017Here’s where your peers rank on the Inc 5000 list for 2017:

| Ranking | Company Name | Growth | Revenue | Type |

| 15 | Forward Financing | 12,893.16% | $28.3M | MCA |

| 47 | Avant | 6,332.56% | $437.9M | Online Consumer Lender |

| 219 | OppLoans | 1,970.22% | $27.9M | Online Consumer Lender |

| 260 | US Business Funding | 1,657.42% | $5.8M | Business Lender |

| 361 | nCino | 1,217.53% | $2.4M | Software |

| 449 | Kabbage | 979.31% | $171.8M | Online Consumer Lender |

| 634 | Lighter Capital | 712.03% | $6.4M | Online Business Lender |

| 694 | Swift Capital | 652.08% | $88.6M | Business Lender |

| 789 | CloudMyBiz | 575.46% | $2.1M | IT Services |

| 1418 | loanDepot | 286.11% | $1.3B | Online Consumer Lender |

| 1439 | Nav | 281.98% | $2.7M | Online Lending Services |

| 1731 | United Capital Source | 224.85% | $8.5M | MCA |

| 1101 | ZestFinance | 165.99% | $77.4M | Online Lending Services |

| 2050 | National Funding | 184.74% | $75.7M | Online Business Lender |

| 2572 | Blue Bridge Financial | 136.73% | $6.6M | Online Business Lender |

| 2708 | Bankers Healthcare Group | 127.51% | $149.3M | Financial Services |

| 2714 | Tax Guard | 127.02% | $9.9M | Financial Services |

| 2728 | Fora Financial | 125.81% | $41.6M | Online Business Lender |

| 2890 | Reliant Funding | 121.61% | $51.9M | Online Business Lender |

| 4005 | Cashbloom | 70.47% | $5.4M | MCA |

| 4945 | Gibraltar Business Capital | 42.08% | $16M | MCA |

Compare that to last year’s list below:

Of the companies on the 2016 list, Capify and Bizfi were wound down while CAN Capital ceased operations but then later resumed them more than half a year later.

Bond Street Has Stopped Lending

September 13, 2017 NYC-based small business lender Bond Street has stopped making new loans, according to sources who worked with them. The Wall Street Journal published a similar report earlier today. In addition, the WSJ reported that Goldman Sachs is hiring 20 of Bond Street’s employees.

NYC-based small business lender Bond Street has stopped making new loans, according to sources who worked with them. The Wall Street Journal published a similar report earlier today. In addition, the WSJ reported that Goldman Sachs is hiring 20 of Bond Street’s employees.

Just seven months ago, Bond Street announced that they had closed a $300 million loan purchase agreement with Jefferies. The WSJ reported that an inability to raise additional equity is what threw a wrench in their future. The same situation happened to Bizfi just a few short months ago, who wound down after 10 years and shipped their portfolio off to rival Credibly to service.

Bond Street’s 1-3 year loans with APRs ranging from 8% – 25% were terms that many in the alternative business lending universe say is a fundamentally unprofitable model. The company now appears to be joining the ever growing purgatory of alternative small business finance companies. They join Dealstruck, Herio Capital, Bizfi, and Nulook Capital. CAN Capital was previously on that list but was recently restructured and revived.

Able Lending, another small business lender, denied that they were going out of business but admitted they were looking to be acquired.

Square is also reportedly in talks to hire Bond Street employees, the WSJ claims. When Bizfi closed, their employees were mainly picked up by rivals World Business Lenders, Strategic Funding, iPayment, 6th Avenue Capital, and others.

The State of The Industry (In Memes)

September 2, 2017The state of things in MCA, online lending, and fintech through the disloyal boyfriend meme:

SEE MANY MORE DEBANKED MEMES

The History of Alternative Finance (As Told Through Memes)

Ready to Trade ONDK and LC? Scroll to the bottom of the page

10 Clues You’re Hardcore About Merchant Cash Advance