Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Google’s Payday Loan Ad Ban Smells Like Government Intimidation

May 12, 2016 CFPB Director Richard Cordray

CFPB Director Richard CordrayGoogle loved payday lending and products like it, until something happened.

Google Ventures is one of the most notable investors in LendUp, a personal lender that charges up to 333% APR over the period of 14 days. The famous creator of Gmail, Paul Buchheit, is also listed as one of LendUp’s investors. Four months ago, Google Ventures even went so far as to double down on their love for the concept by participating in LendUp’s $150 Million Series B round.

This week, Google Inc. has apparently found Jesus after “reviewing their policies” and determined that personal loans over 36% APR or under 60 days will be forever BANNED from advertising on their systems. “This change is designed to protect our users from deceptive or harmful financial products,” they wrote in a public message. Ironically of course, Google is tacitly admitting that it must protect users from its own products that it has invested tens of millions of dollars in because they are deceptive or harmful.

LendUp is not the only company that Google Ventures has invested in that charges more than 36% APR. A business lender they previously invested in charged up to 99% APR. That investment was for $17 million as part of a Series D round. At the time, they called the management team’s vision “game changing.”

The only thing game-changing now is their about-face after their supposed policy and research review. It’s hard to imagine that in 2016, Google is just finally reading research about payday lending, especially considering that payday loan spam has for so long been a part of their organic search results. It cannot be understated that they’ve even created entire algorithms over the years dedicated to payday search queries and results. And “loans” as a general category is their 2nd most profitable. Yes, surely they know about payday.

Predatory middleman

Google has good reason lately to be afraid of sending a user to a website to get a payday loan however, even if they’re just an innocent middleman in all of this.

Last month, the Consumer Financial Protection Bureau filed a lawsuit against Davit (David) Gasparyan for violating the Consumer Financial Protection Act of 2010 through his previous payday loan lead company T3Leads. In the complaint, the CFPB acknowledges that T3Leads was the middleman but argues that its failure to properly vet the final lender customer experience is unfair and abusive. At its core, T3Leads is being held responsible for the supposed damage caused to individuals because they may not have ended up getting the best possible loan terms.

One has to wonder if Google could be subject to the same fate. Could they too be accused of not auditing every single lender they send prospective borrowers off to?

Four months before being sued by the CFPB personally, the CFPB sued T3Leads as a company.

Gasparyan however, is already running a new company with a similar concept, Zero Parallel. That company is indeed advertising on Google’s system.

Chokepoint

For the CFPB, coming fresh off of having made the allegations that even a middleman sending a prospective borrower off to an unaudited lender is culpable for damages, the most bold way to achieve their goals of total payday lending destruction going forward would be to threaten the Internet itself, or in more certain terms, Google.

It’s quite possible that Google has been strong-armed into this new policy of banning short term expensive loans by a federal agency like the CFPB. Not giving in to such a threat would likely put them at risk of dangerous lawsuits, especially now that there are some chilling precedents. By forcing Google to carry out its agenda under intimidation, the CFPB wouldn’t have to do any of its day-to-day work of penalizing lenders individually that break the rules. Google essentially becomes a “chokepoint” and that’s quite literally something right out of the federal regulator playbook.

In 2013, the Department of Justice and the FDIC hatched a scheme to kill payday lenders by intimidating banks to stop working with them even though there was nothing illegal about the businesses or their relationships. That plan, which caused a massive public outcry, had been secretly codenamed “Operation Chokepoint” by the DOJ. A Wall Street Journal article uncovered this and a Congressional investigation finally put an end to the scheme after two years, but not before some companies went out of business from the pressure.

Given this history, it’s highly plausible that Google has been pressured in such a way that it’s too afraid to reveal it.

Google has long known all about payday lending. Their recent decision smells like government and they just might very well be the chokepoint.

Loan Originations Slow Industrywide

May 10, 2016

It’s not just one marketplace lender experiencing a slowdown in originations. Some of the largest players across the spectrum cooled their jets in Q1 of this year compared to Q4 of last year.

| Company | Origination Growth |

| Lending Club | +7% |

| Square Capital | +4% |

| OnDeck | +2% |

| Prosper | -12% |

| Avant | -27% |

While Lending Club weathered the storm relatively well, the resignation of their CEO amid a loan manipulation scandal does not bode well for its immediate future prospects.

Avant CEO Al Goldstein, whose company’s loan volume among the bunch dropped off the most, told Crain’s Chicago last month, “If we can’t find capital, we’re not going to grow fast. If we can, we will.”

In a later comment to the WSJ, an Avant spokesperson explained that Q4 loan volumes are typically elevated because of the holidays and Q1’s volume down because many borrowers are receiving their tax refunds.

Did Peer-to-Peer Lending Sell its Soul to Wall Street?

May 8, 2016

“We have so many fans but we also have some people here that are looking to take advantage of us, that are here for a short term trade and they won’t be part of this industry.” – Ron Suber, President of Prosper Marketplace

Ron Suber may have been talking about specific players in the capital markets when he said those words at LendIt just a few weeks ago but that characterization could just as easily apply to all of Wall Street in general. During his presentation, he offered two real world examples about how their message got hijacked by the same facilitators they originally believed were there to help them. The first was a case of bad buyers.

“When a marketplace lender sells a bunch of loans and the buyer isn’t aligned with the marketplace, if the buyer of those loans is going to buy those loans and leverage them, rate them, and securitize them every single quarter without alignment with the industry and just sell those bonds into the marketplace, […] that won’t be good for you, for the industry,” he said. “And we learned that lesson. When we don’t have alignment with our investors, when groups sell our loans into the market no matter what if the market’s not ready, it’s not good and we learned that at Prosper this year.”

Keynote Presentation by Ron Suber of Prosper at the LendIt USA 2016 conference in San Francisco, California, USA on April 11, 2016. (photo by Gabe Palacio)

What he was saying is that the buyer matters because if they’re repackaging up the product for mass consumption, it is ultimately the original seller (i.e. companies like Prosper) that is being judged for the success or failures of the product’s reception down the line.

A second example stemmed from mismatched projections. You might think it’d be a good thing if a rating agency’s own analysis of your loan portfolio projected even lower loss rates than you projected on your own. Not so, and this actually happened; Moody’s projected loss rates for the loans packaged inside of Citigroup-issued Prosper bonds were lower than what Prosper projected itself for the same vintage. So when default rates were on pace to exceed Moody’s aggressive projections (and fall in line with Prosper’s), news of an impending bond downgrade due to allegedly poor performance roiled the market. The media interpreted Moody’s adjustment to mean that something was wrong with Prosper, not that something was wrong with Moody’s initial assessment.

Suber summed these experiences up by telling the audience, “we must control our story.” That’s a challenge because Wall Street loves to commoditize things, especially loans. The value goes up, the value goes down, and Wall Street will sell it if there is a buyer for it without any regard for the story. What to do then?

CommonBond CEO David Klein said on a panel in late March that marketplace lenders will look to tap back into individual investors, that there will be a return to the industry’s peer-to-peer roots.

Fundera CEO Jared Hecht, a co-panelist, said that “retail investors are more loyal to a specific platform” and that this can create a “network effect.”

The problem of course with retail investors, aside from the steep regulatory hurdles to sell to them, is the comparably slow speed at which they allow a platform to scale. The downside for any company that takes this organic approach is that they could grow so slowly that they get eclipsed by everyone else.

But perhaps the underlying issue is that some companies that originally set out to be peer-to-peer lenders have succumbed to this identity of being “online lenders.” That’s a problem because traditional financial institutions can use technology to lend online too and the Internet will eventually become the standard medium for all lending. That means that soon being an online lender will just mean being a lender period. And if you are just a lender, well then Wall Street will indeed take advantage, control the story and charge their standard fare just for playing the game.

The price? One soul.

And once you sell yours, it’s hard to get it back.

Jim Cramer Unimpressed With Square Capital’s 4% Bad Debt

May 6, 2016

Jim Cramer told TheStreet that he wasn’t impressed by Square Capital’s 4% bad debt because as he put it, the average default rate on credit cards is about 2.67% right now. That comparison belies the fact that Square’s customers make payments daily, the cost of capital is more expensive than a credit card, and that Square did little or no underwriting to achieve these results.

In fact, a study conducted jointly by deBanked and Bryant Park Capital last year determined the average industry (SMB Lending & MCA) default rate to be 6.4%. Square if anything, is outperforming some of their successful peers and given some recent structural changes, they probably stand to improve even further.

OnDeck’s default rate is reportedly about 7% and that’s with an underwriting model often touted as revolutionary.

The comparison between credit cards and Square Capital’s daily payment product is interesting but misleading. Nonetheless, Cramer appears to be unimpressed with alternative lending in general. “Is Square going to be like an On Deck and Lending Club? We don’t want that,” he said, referring to their recently depressed stock prices.

Three days ago, Cramer made his views known through a tweet.

I do not like these new kinds of “banks” https://t.co/DO33G0cBCz

— Jim Cramer (@jimcramer) May 3, 2016

You can watch his comments about Square Capital, OnDeck and Lending Club below:

So far his analysis is quite the opposite of what it was imagined to be 18 months ago.

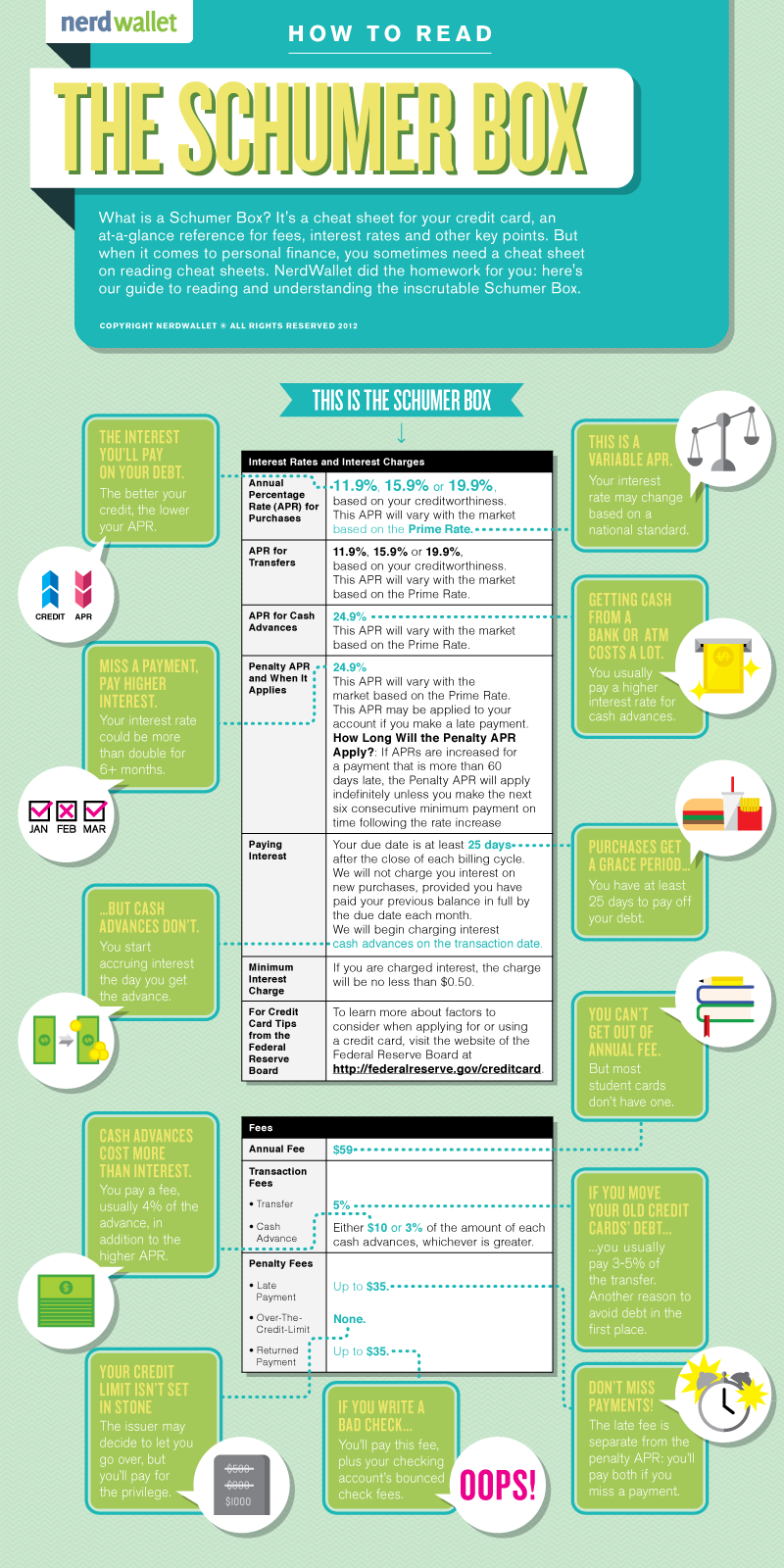

Online Lending APR ‘SMART Box’ To Apply To Loans, Not Merchant Cash Advances

May 5, 2016

OnDeck, Kabbage and CAN Capital have launched an initiative to make online loan shopping easier. Dubbed the SMART (Straightforward Metrics Around Rate and Total Cost) Box, these lenders plan to present small businesses “with a chart of standardized pricing comparison tools and explanations, including various total dollar cost and annual percentage rate metrics that enable a comprehensive pricing comparison of loans of equivalent duration.”

The Box, clearly meant to increase transparency, was explained in an ironically confusing way, particularly where it said it would include annual percentage rate metrics. An Annual Percentage Rate (APR) is indeed a representation of several metrics and thus it wasn’t clear if the Box would just include some of these individual metrics and conveniently leave out the APR itself.

OnDeck CEO Noah Breslow for example told Forbes only six months ago that annual terms don’t make sense. “The APR overstates the actual cost of the loan to the borrower,” he said. He was not alone in thinking that way. Several studies have concluded too that merchants don’t always even know what APR represents. Lendio for example, found that two-thirds of small businesses selected the total dollar cost of a loan as the easiest to understand. Only 17.4% said the APR was the easiest.

And there’s another thing, the fact that CAN doesn’t just do loans, they also do a significant amount of merchant cash advances. What role could an APR have there? While the Box’s final system won’t be decided until after the conclusion of a 90-day national engagement period that begins next month, one can only imagine that it might have a Schumer Boxer feel to it.

A Schumer Box explained:

Via: NerdWallet

The syntactic ambiguity in the announcement however was unintentional. A spokesperson for the group (Known as the Innovative Lending Platform Association) said that the SMART Box will indeed include Annual Percentage Rates.

But that’s where loans are concerned…

When deBanked asked about merchant cash advances, Daniel Gorfine, vice president and associate general counsel of OnDeck; Parris Sanz, Chief Legal Officer of CAN Capital and Azba Habib, assistant general counsel of Kabbage, submitted the following joint response:

“As part of the SMART Box initiative, we are interested in engaging with providers of MCA products. Based on consistent assumptions about a small business’s future sales volumes and its ability to deliver the contracted amount of receivables within the period of time estimated during underwriting, the SMART Box could apply to MCA products.”

So long as SMART Box disclosure is voluntary, an MCA company could perhaps employ their own version of it. It just might come sans APR given the product’s history with state regulations. The Association is emphatic however that this concept could be used by MCA companies and others in the small business financing space. After all, the initiative is rooted in transparency for the small business owner, they say.

In September, the Association “will encourage those interested in promoting the responsible development of the small business lending industry to voluntarily adopt or support the model disclosure.”

Given the level of influence these companies have on the industry, the voluntary nature of the SMART Box has the potential to spark an industry-wide box revolution. MCA companies however would need to structure transparent disclosure around their contractual frameworks. But even that could be a good thing. One commercial financing broker for example, posted a redacted service fee agreement to the DailyFunder forum earlier this week that purported to show another broker trying to charge a merchant a 26% premium (26% of the funding amount) for their work. Despite this unusually high cost, the charge itself was hard to find, hidden among fine print on an otherwise benign looking page. Naturally, others in the industry did not respond kindly to it. Even other brokers referred to it as “outrageous,” “nonsense,” or “bs.”

Their reactions make clear that there is a desire for transparency even among the group most often blamed for the lack thereof. Some of the industry’s forward thinkers have told deBanked that a system like a SMART Box is the future of the industry whether one agrees with it or not. And if not for the sake of small businesses and regulators, then for the sake of being able to compete fairly against companies that may be relying on truly hidden fees.

SMART Box. All aboard the transparency train?

Square Capital’s Default Rate is 4%

May 5, 2016

Square revealed today that its Square Capital division had extended $153 million through more than 23,000 advances and loans in the first quarter. The company is still transitioning from merchant cash advances to loans to appease institutional investors. This was not only said at LendIt by Jackie Reses but also reiterated in their Q1 earnings report. “We believe that the transition to a loan product further increases our ability to attract new Square Capital investors,” it said.

Their default rate continued to hover at 4%.

That number is shockingly low considering that under a pure merchant cash advance model they did not conduct credit checks, nor did even they review bank statements or tax returns. Rather the company relied almost entirely on a merchant’s sales history with Square.

This process may have made funding easy but was potentially a hard sell to regulators. As part of their transition to a lending model, all applicants are now subject to a credit approval and have to supply identifying documents. Square also bought an analytics startup less than two months ago to help them make more informed underwriting decisions. This can only mean that if their default rate was 4% with no underwriting, their prowess as a lender will likely increase considerably.

Jim Cramer Tweeted About OnDeck and Online Lenders

May 4, 2016Eighteen months ago and prior to OnDeck’s IPO, I joked about how an online business lender might be evaluated by the mainstream financial media, particularly through Jim Cramer memes.

You can view all of the rest of those on the bottom of this page here.

In the meantime, the real Jim Cramer is not as entertained by these types of businesses. Here’s what he had to say about OnDeck and companies like them:

I do not like these new kinds of “banks” https://t.co/DO33G0cBCz

— Jim Cramer (@jimcramer) May 3, 2016

Meanwhile, below is a video of Jim Cramer talking to Lending Club CEO Renaud Laplanche just 1 year ago when he was more open to the idea:

Video not working? click here

Is The Marketplace Lending Apocalypse Upon Us?

May 3, 2016

Days after rumors leaked that Prosper Marketplace had planned to lay off staff, the WSJ is now reporting that the company is indeed eliminating 171 jobs, closing their Utah office and letting go of their chief risk officer. CEO Aaron Vermut’s salary has also been cut to zero.

The timing for the industry they’re a part of couldn’t be worse. OnDeck’s stock closed down 34% today after Q1 losses and revised projections took analysts by surprise. The source of the pain? OnDeck’s “Marketplace.” The institutional investors typically willing to pay a high premium for loans disappeared, according to OnDeck executives on the earnings call.

Unsurprisingly, Prosper’s “Marketplace” has historically relied on institutional buyers for their loans too, as much as 92% of all loans on the platform in fact. Prosper’s roots as a peer-to-peer lender don’t make it an ideal candidate to just shift loans to their balance sheet like OnDeck, which could make the changing capital markets landscape even more painful for them.

Two months ago, Prosper raised the interest rates they charge, citing a “turbulent market environment.” And just weeks ago, Citigroup announced that they would no longer buy loans from Prosper to package into bonds. Now, signs of stress are finally starting to show.

And then there’s Lending Club, a “marketplace” rival to both Prosper and OnDeck, who experienced a 10% decline in its stock price today. The company’s model is under fire through a class action lawsuit that alleges among other things that they along with WebBank are Racketeer Influenced Corrupt Organizations. Lending Club plans to release their Q1 earnings on May 9th.

And it’s not just the capital markets and lawsuits shaking up the landscape. Half a dozen trade associations have been formed over the last few months to quell some of the negative rhetoric surrounding online lending in Washington and to educate policymakers on the positive aspects of these services.

In the Illinois State Senate for example, a pending bill has the potential to outlaw all nonbank business lending altogether.

Some of those that broker business loans have already fallen on hard times due to things like the cost of leads skyrocketing.

“Anybody can fund deals – the talent lies in collecting the money back at a profitable level,” said Capify CEO David Goldin in deBanked’s most recent magazine. “There’s going to be a shakeout. I can feel it.”

The early signs of that prediction may finally be starting to unfold.

After the Lendit Conference last month, I speculated that marketplace lending euphoria ended because the relationship between investors and platforms was in some ways based on lust, not love. The breakup is now starting to manifest itself in the form of missed earnings and layoffs.

Is the apocalypse upon us? Probably not yet, but these foreshocks are a good sign that we’ll soon be separating the wheat from the chaff.

Make sure to wear your hazmat gear as you enter the marketplace.