technology

Serial Litigants May Target Websites and “Trackers” As Alternative to TCPA

June 12, 2026![]() The small business loan brokerage had played it safe. Rather than robodial and take their chances in the minefield of TCPA compliance, they ran ads on Facebook and Instagram and had the merchants call them. Inbound leads were gold, they cheered, until one of those inquiries came through a little differently. It was a demand for damages for having been tracked on the internet.

The small business loan brokerage had played it safe. Rather than robodial and take their chances in the minefield of TCPA compliance, they ran ads on Facebook and Instagram and had the merchants call them. Inbound leads were gold, they cheered, until one of those inquiries came through a little differently. It was a demand for damages for having been tracked on the internet.

The merchant alleged that they had only been served ads on social media by that company because they had been tracked from a prior website visit. They hadn’t wanted to be tracked and there was no option to opt out of tracking. As a result, they demanded to be compensated, heftily.

By now, most internet users have at least heard the term GDPR, the General Data Protection Regulation that became a never-ending source of controversy throughout Europe, but not all are aware that states and litigants in the US have tried to create a similar framework for privacy. For some in the small business finance industry, the vast complexity of compliance was not fully understood until the lawyers came calling.

“Pretty much every MCA company is potentially a victim because they’re all doing advertising,” said Richart Ruddie, CEO of Captain Compliance, a firm that specializes in safeguarding companies against these sorts of threats. “What we do is we protect against the rise and surge in privacy lawsuits and privacy litigation. So, anybody running TikTok ads, Facebook ads, Instagram ads, any sort of technology that does session-replay where it watches you move the cursor on the screen, if they’re running Google Analytics, all of these are cases that have been tried and are being litigated over.”

Ruddie said that companies within the small business finance industry, including a few within the segment of MCA, have been hit with claims, and they’re now actively working with them to make sure it doesn’t happen again.

“What our software does is provides the ability for users to have consent to opt-in or opt-out of any sort of ad targeting, tracking, session-replay technology,” Ruddie said. “And then we also provide software that constantly keeps businesses’s privacy notices and privacy policies up to date with their tracking and what they’re doing as well as their data handling practices.”

“What our software does is provides the ability for users to have consent to opt-in or opt-out of any sort of ad targeting, tracking, session-replay technology,” Ruddie said. “And then we also provide software that constantly keeps businesses’s privacy notices and privacy policies up to date with their tracking and what they’re doing as well as their data handling practices.”

The larger issue is that for companies that might already be aware of the risks, the solutions they’re using may not actually be compliant with the laws.

“What’s happening now is there’s a handful of these cookie banner softwares but they don’t work and they’re creating bigger issues because they’re like ‘Hey, you told me I could opt out, and then I turned off the selling and sharing of my personal information and you still track me,'” Ruddie explained.

This is made all the more complex by the fact that there are nearly two dozen states with their own twists on compliance. And a growing cottage industry of serial litigants that know this complexity could make website operators easy targets to profit off of. For instance, some of them are going around and running automated website scans just to see who to target. Ruddie said that he’s seen claims reach into the tens of thousands or hundreds of thousands of dollars for alleged privacy violations.

Preventative measures are within reach, however. Ruddie says that for a brand new customer they can get a company compliant in one to three business days. It’s hard for companies to hide in the shadows if they’re online because it doesn’t take much to see what’s there and what isn’t.

“You can right-click and look at the code and then you can see all the different tech and what’s running on the website,” Ruddie said.

Soon, You’ll Be Able to Lend Against Credibly Small Business Loan Pools

May 23, 2026For most people in the small business lending and revenue-based financing industry, news of a billion-dollar securitization barely resonates. It’s too big, too abstract, especially if you’re used to the ground game of syndicating a couple million bucks in deals you handpicked with funders you personally know. Wall Street-level capital markets has always felt like a mysterious private club, where a hundred million here and a billion there changes hands through an old-fashioned system outsiders hardly ever get to see, aside from the press release that later announces a deal happened.

But something recently changed. Capital markets, at least a corner of it, is being democratized. That became obvious when someone told me I could lend a hundred bucks toward a warehouse line of credit for Credibly just to see it for myself.

Me? Somehow involved in a warehouse line for Credibly???

On May 5, Credibly announced a strategic partnership with Figure to “modernize SMB capital markets via blockchain rails.” It sounds like a buzzwordy headline from the 2010s. Not AI, blockchain. In 2026. Though there are certainly AI technologies involved.

Figure is a familiar name, not only because it is publicly traded, but also because I had the honor of sharing a stage with Figure CEO Michael Tannenbaum last fall at the B2B Finance Expo in Las Vegas for a fireside chat. While I mainly asked him about how small business owners could leverage their home equity to obtain capital, Tannenbaum pivoted at moments to explain how the company was reshaping capital markets by using blockchain. At the time, some of it went over my head.

“Everybody else is trying to use an origination system, and then on the back end figure out where to sell the loan,” said Tannenbaum on Peter Renton’s recently released Fintech One-on-One podcast, “and that figuring out process creates all this back and forth between the lender, the borrower, and the ultimate buyer, and we eliminated that, and we eliminated the people-based approach and standardized it.”

In a nutshell, Figure being in the mortgage game meant it was inevitably tied up in the capital markets game. And they found the capital markets game very old-fashioned. So they made their own capital markets marketplace, with one segment called Democratized Prime, and built it on blockchain rails.

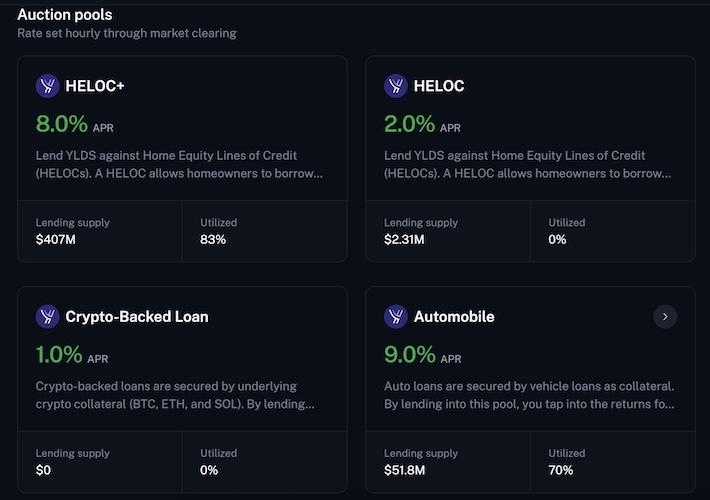

Democratized Prime is essentially like a universal warehouse line, one that is “much easier to borrow and lend against than the arduous process of getting a warehouse line with lots of third-party diligence and legal fees,” Tannenbaum told Renton. It has rapidly become popular for mortgages. If you signed up for the platform today, you would see HELOC pools and their corresponding credit profiles that you could lend against.

Mortgages were just the start. You can also lend against an auto loan pool brought on by Agora. That deal was announced this past February as a landmark moment that kicked off the democratization of new asset classes. Credibly will bring SMBs into the mix next, where the company’s small business loans and revenue-based financing deals will be pooled up and available to lend against with as little as $10 at a time. That means this opportunity is open to just about anybody.

The yield can be determined in one of two ways. One is a Dutch auction, where participants compete to lend into the pool by offering lower rates, which is good for Credibly as the number goes down. If you bid too high or the pool is full, you may have to wait until the next hourly auction to try again. The process resets each hour, with the lowest acceptable bids getting priority, meaning lenders are not just deciding whether they want exposure to the pool, they are also competing on price for the right to put their money to work. The other is a live-rate system where rates change automatically based on utilization. You can exit an auction pool if your funds are not in use or if someone else’s funds are ready to replace yours. For live rates, you can request an exit up to the available liquidity at the time. Credibly is not on the Democratized Prime system just yet. That is supposed to happen this quarter. But HELOC and auto loan pools are already there.

I first tried the platform myself with just a couple hundred bucks. I entered digits into an auction-pool form indicating that I’d be willing to lend at 7.9% APR all-in to a HELOC pool. The pool wasn’t taking any offers for higher than 8% so that’s how I came up with my figure. My funds were accepted, and they’re now earning a return. Not in some magic back room, but visibly on the blockchain.

While you can obviously fund your account with dollars, I dusted off an old stockpile of ETH and sent funds using MetaMask to Figure Markets. Therein lies the only caveat. To lend against the pools, you have to use Figure’s stablecoin, YLDS.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS is an SEC-registered security. It is pegged 1:1 with the U.S. dollar and also earns a return on its own just for holding it, a little over 3% at the time of this writing. Users use their YLDS to lend against the pools and are paid their interest in YLDS (hourly!). This can be swapped back into dollars, Bitcoin, or whatever else one is comfortable with.

YLDS exists on the Provenance blockchain. You’re assigned a wallet address, and you can trace where your funds went using Provenance’s main block explorer, ZoneScan. That also lets you see a bit of what other users are doing, as well as what Figure is doing. By being on blockchain rails, everything is kind of out there for audit and inspection. I saw my ETH get swapped for YLDS on the block explorer and then saw my funds interact with a corresponding HELOC pool smart contract.

If you think this blockchain stuff is still niche, consider that in 2025, stablecoins processed $28 trillion in real economic volume, according to Chainalysis. By 2035, that number could reach $1.5 quadrillion, surpassing today’s entire cross-border payments market. Those are eye-popping numbers, but even if one discounts the forecast, the broader point is hard to ignore: stablecoins are no longer a fringe experiment.

Of course, this is not risk-free just because it is transparent. Pool performance still matters. Borrower credit quality still matters. Liquidity may depend on whether other participants are ready to replace your funds. And because YLDS is itself a security, participants need to understand what they are holding, how it works, and what risks come with using it. The blockchain may make the mechanics easier to inspect, but it does not make credit risk disappear.

While Democratized Prime can make it easier for lenders to tap into capital, this also is not a solution for everyone. Credibly, for example, has provided access to over $3 billion in working capital to more than 61,000 small businesses, with four completed KBRA-rated securitizations, its most recent one completed in the first quarter of 2026 for $124 million, expandable up to $225 million. That is sort of the baseline quality: true institutional-level assets from an institutional-tier lender. A small funder looking to graduate away from syndication is not going to be an immediate candidate for something like this. One of the HELOC loan pools, for example, has taken in $340M from parties looking to lend their YLDS.

One benefit for Credibly in challenging traditional finance ABS markets and adopting this technology is that greater efficiency and reduced friction should ultimately enable the company to pass savings on to its small business customers.

Would you lend a million dollars against a Credibly business loan and revenue-based financing pool? Before now, you probably wouldn’t ever have had that opportunity. Now Figure is making that possible.

QuickBooks Capital: ~$1.7B Funded Last Quarter, Repeats that AI is Not a Threat, But Rather an Advantage

May 21, 2026 Intuit’s QuickBooks’s capital originated about $1.7B in small business loans in Q3 FY 2026. That brings the total for the trailing nine month period ending April 30 to $4.3B. During the earnings call, Intuit CEO Sasan Goodarzi said “We are growing our line of credit offerings with buy now, pay later, directly embedded within QuickBooks, and the launch of Intuit business credit card.”

Intuit’s QuickBooks’s capital originated about $1.7B in small business loans in Q3 FY 2026. That brings the total for the trailing nine month period ending April 30 to $4.3B. During the earnings call, Intuit CEO Sasan Goodarzi said “We are growing our line of credit offerings with buy now, pay later, directly embedded within QuickBooks, and the launch of Intuit business credit card.”

Like other software companies, analysts have been questioning the sustainability of their product offerings as AI looms large as a threat. Like the previous quarter, Goodarzi offered a rebuttal on this subject, expressing that they are effectively the AI solution customers would seek.

“It is important to recognize that businesses, while they use Google, they use LLMs to do searches, do queries, you cannot run your business with an LLM because you are managing your books, you are managing your money, you are managing your payroll, and accuracy and compliance of doing that matters,” Goodarzi said. “And running a business is mission critical. And so psyche of businesses is such that and accountants is that they need us to be their AI platform to provide expertise so they can run and grow their business.” Goodarzi cited Anthropic and OpenAI as partners they are already working with, for example.

Goodarzi also said that winning customers is not necessarily about the best software anyway, but rather about the confidence the assistance with the work instills in the customer. And given the integrations they have, the reputation they have, the AI power that they use, and ability to assist customers, this is where they are actually structurally advantaged.

Deep Search, Merchant Lawsuits, and More

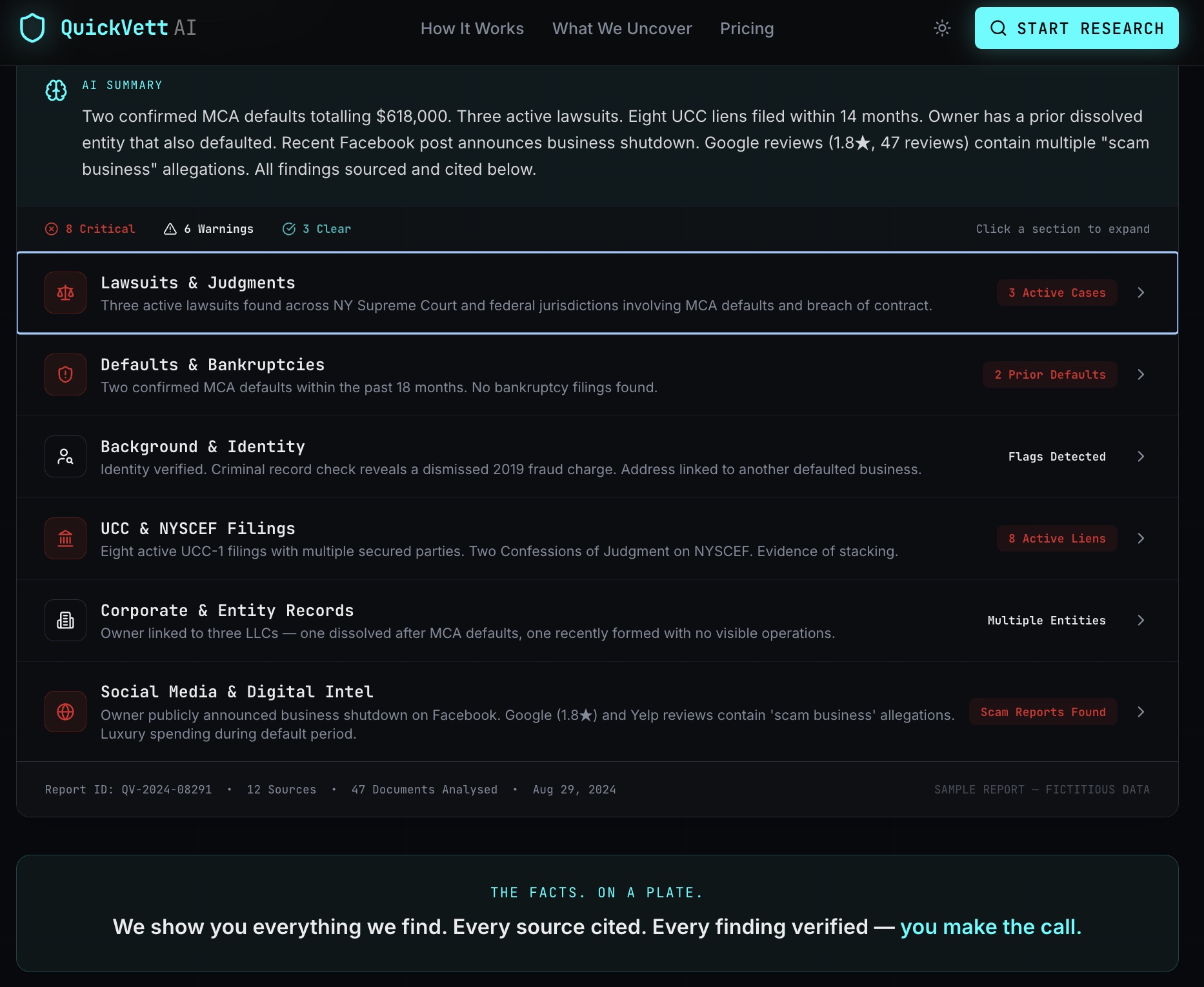

May 19, 2026 The deal came into underwriting and within minutes alerts popped up. The merchant had been sued by an MCA company in 2018. An auto-decline? Perhaps. Or maybe a closer look into the court records would shed light on whatever happened there to see if the situation is manageable, that is if the records are even easily accessible to begin with and the underwriter doesn’t mind parsing through a docket full of filings.

The deal came into underwriting and within minutes alerts popped up. The merchant had been sued by an MCA company in 2018. An auto-decline? Perhaps. Or maybe a closer look into the court records would shed light on whatever happened there to see if the situation is manageable, that is if the records are even easily accessible to begin with and the underwriter doesn’t mind parsing through a docket full of filings.

QuickVett will spare you the trouble and cut right to the chase. That lawsuit? A dispute over $3k that happened at the tail-end of a large $100k deal. The outcome? A satisfied settlement. It’ll all be right there in its report. No manual lookup on the case required. QuickVett, which describes itself as a merchant intelligence platform, scans state and federal court records across the US. If there’s a hit involving an MCA it will use an MCA-specific AI analysis to present relevant details to an MCA underwriter. An immediate default is distinguishable from one that happened after a long lengthy relationship, for example. Maybe a conflict arising after the 7th renewal provides clarity that otherwise wouldn’t be readily obvious. Most underwriters are already familiar with NYSCEF but if the deal is not in the New York State court system, it’s not going to be found. QuickVett says they’ll find it wherever it is.

QuickVett also does creative searches on its own, such that it will discover if the merchant’s DoorDash account or e-commerce site has gone offline, for example, or if employees of the business recently updated their LinkedIn accounts to say that they no longer work there. QuickVett also pays special attention to the corporate structure and job title of the officers. For example, in an impromptu trial afforded to deBanked for test purposes, QuickVett’s deep search system discovered a sworn affidavit filed by a business owner in an old court case and compared what he said to public records and his LinkedIn profile about his role in the business. The result was that everything matched. But if it hadn’t, an underwriter might have to contend with why a business owner swore he had partners in an obscure court case but listed himself as the 100% owner on a funding application and proceed accordingly.

Overall, “QuickVett scans court records, background databases, corporate filings, social media, and the web — delivering a complete merchant intelligence dossier in under 5 minutes,” the company states. Its AI systems custom tailor the findings to an MCA-style underwriting process.

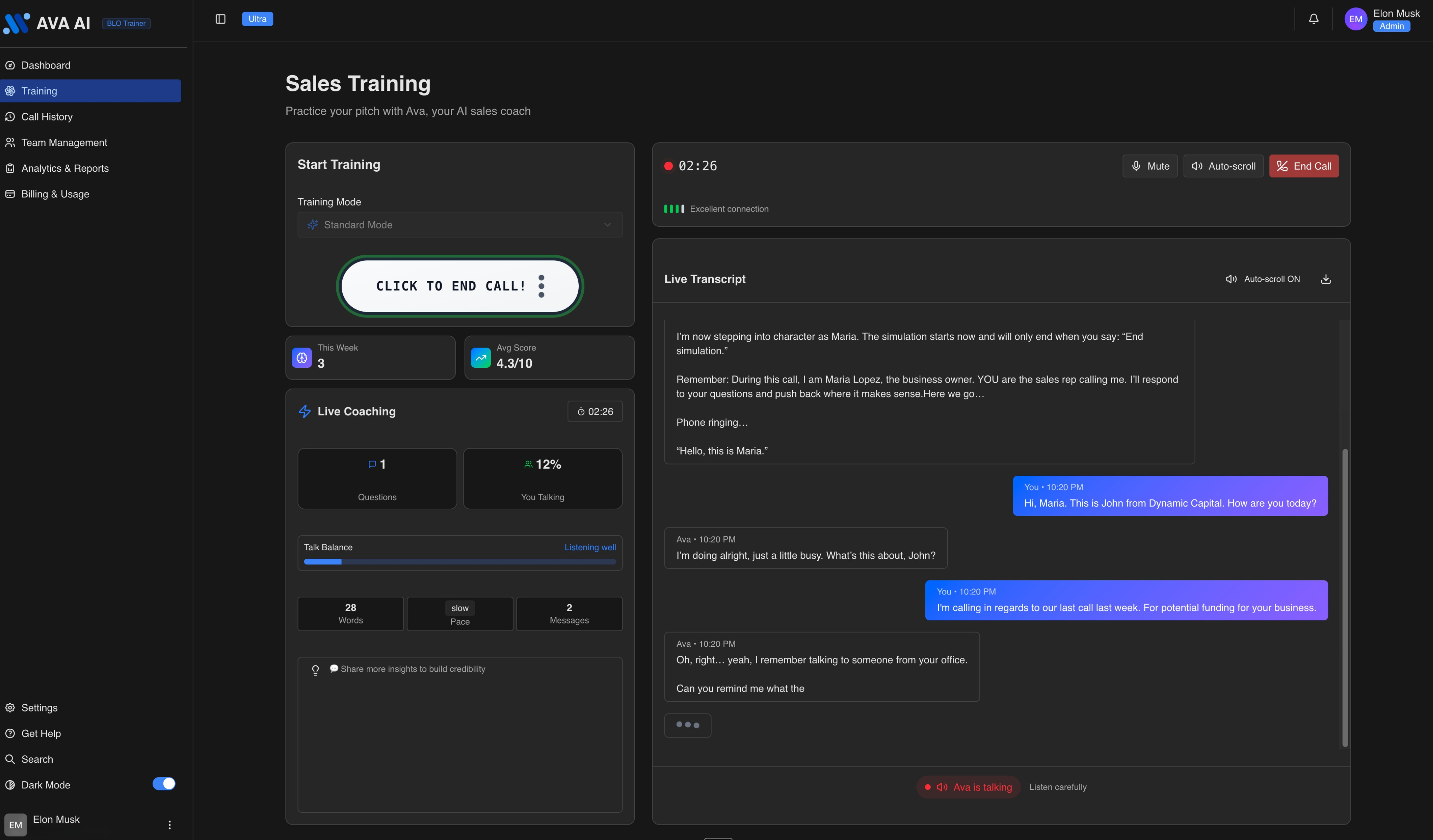

Getting Your Reps to Perform at the Ultimate Level? This ISO is Using AI to Train Them

February 2, 2026“I‘m unable to get 80, 90 guys to work in the area that I am in so I have to actually max out the team that I have,” says Steven Edisis, CEO of Dynamic Capital. “So my whole thing is onboarding guys and getting them to perform at the ultimate level.”

Edisis says that training small business finance sales reps takes extreme discipline, hours and hours of manual training. Training in the morning. Training in the afternoon. Training at night. Training and then some more training. Some of that training involves roleplaying. Other times it’s live calls. In either case, he’s found there are weaknesses in those systems. For instance, in a roleplay, the trainer has to contend with maintaining rapport with the individual they’re training. Persistent unfavorable feedback, even if warranted, could actually be demoralizing and create tension in the relationship.

“When you’re roleplaying with your buddy, your buddy’s a human,” Edisis says. “After two or three or four times of them getting it wrong, do you just stop correcting it? And you let it go.”

The end result is that they’re not actually in top shape and ready for calls, but they could be deceived into thinking that they are. Meanwhile, live-call training presents another dilemma. If you give the trainee good leads and they mess up, are the good leads wasted? And if you give them really cheap leads and they don’t get anywhere with them, how are they supposed to be judged or learn from it?

For Dynamic Capital, the solution to all of the above has been AI. About a year ago, Edisis began using an AI agent called Ava, a product by Reech AI that’s led by CEO Liran Weissenberg. Ava does for Dynamic Capital what Edisis did for a long time, trains, but on steroids. Trainees, experienced reps, and even veteran pros at the game can roleplay with Ava, a voice AI, in any setup of circumstances they choose. It can be a straight-up cold call, a warm lead, or a follow-up, for example. It can be tuned to easy mode, regular mode, hard mode, or even impossible mode. The best part is that Ava knows how to play the role of a merchant, speaks in real time, and speaks with human-believable tones and emotions. Voice AI technology, once considered clunky or plagued by latency in years past, has finally become virtually indiscernible from a real person.

In a live demo performed for deBanked to show it in action, the AI answered the phone and Edisis went right into the normal flow of business.

“This is Steven with Dynamic Capital. Last week you went online, requested some information for some working capital for your business, how are you today?”

“I’m ok, just a little busy right now,” Ava responded somewhat suspiciously. “yeah, I remember poking around online. I put in my info but I never really got a clear idea what you guys actually do.”

From there, Edisis played it out to a conclusion. When it was over, Ava rated him on his performance, gave him a score, and shared what he did well, as well as things he could have done better. It seemed to understand the relevance of open balances a merchant might have with loans or MCAs, which is key to making it impactful. Ava’s an AI, so a trainee would not be able to attribute the constructive criticism it offered to being singled out or picked on. For instance, if the AI said the trainee needed to work on tone and pacing of speech, there’s no way for the trainee to attribute that to personal bias from a trainer.

“The cool thing is that we can model the AI to behave in very specific scenarios and to have very specific analysis,” said Weissenberg of Reech AI, who created Ava.

Meanwhile, no real leads were wasted in the process. This is especially valuable since Edisis says that he teaches a specific technique—or rather, an art—called the interruption, a very delicate tactic used to keep a call on track. But it only works if delivered correctly, because it involves literally interrupting the prospect while they’re speaking. Learning how to interrupt in the circumstances that call for it is a massive gamble that could not only lead to lost sales revenue but also negative customer feedback if executed poorly. This is a perfect example of where AI training comes into play.

“It’s really nice to [practice it] on Ava versus blowing up and getting negative reviews from a live person,” Edisis said. “So that’s a really cool way that I can train people.”

Weissenberg said that when Ava is being used across a whole sales floor, a sales manager can view transcripts of all the calls, along with feedback and analytics. One could literally have a full-on simulated call center where all the prospects are AI agents being used to train reps.

“The coolest thing about the app is the analytics,” Weissenberg said. “It’s only going to get better too because AI is getting smarter and it’s getting more human.”

“On top of [new trainees], my other guys over the years—some have been here up to ten years—every once in a while they get a little rusty, revert back to bad habits, etc.,” Edisis said. “This allows me to keep them honest. And when some new person comes to me and tells me my leads are bad, I say, “let’s go to Ava… you tell me your pitch, I’ll do the same pitch.”

If Edisis significantly outscores them, it becomes evident that lead quality isn’t the issue, but rather all the other factors that go into having a successful call.

“It keeps some honesty between the program and reality,” he said.

RadioShack is Launching a Crypto Swap

December 19, 2021 If you had RadioShack on your 2021 DeFi bingo card, congratulations, you’ve won. The company announced that its “mission is to be the first protocol to bridge the gap in mainstream usage of DeFi” and it plans to do this, apparently, by launching a swap.

If you had RadioShack on your 2021 DeFi bingo card, congratulations, you’ve won. The company announced that its “mission is to be the first protocol to bridge the gap in mainstream usage of DeFi” and it plans to do this, apparently, by launching a swap.

RadioShack wants to compete with the likes of Uniswap, a smart-contract-based crypto exchange where users can “swap” tokens without having to register on a formal exchange like Coinbase.

The business is a gold mine, according to RadioShack.

“The concept of a swap stands out first and foremost as the place of low-hanging fruit – fruit that is spinning off incredible levels of net profit,” the company said. “Profit not just from speculation like Bitcoin or other cryptocurrencies, but ones born out of trading fees. Some existing swaps like Uniswap or Sushiswap reportedly are doing $1-$7 million net profit per day! They are the current profitable forces of nature in the DeFi world.”

Use of a “swap” is how tokens issued by the ConstitutionDAO crowdfunding saga leaked out into the publicly tradeable marketplace, for example. What was supposed to be a “governance token” to vote on where a copy of the United States Constitution would be held, instead turned into a tradeable novelty asset (like pogs or baseball cards) with a soaring value, all because of decentralized swapping. More than $100 million worth of the novelty governance tokens stemming from the failed bid to buy the Constitution were traded just in the last 24 hours alone, according to Coinmarketcap.com.

“RadioShack DeFi is focused on the early majority,” the company said. “It will become the first to market with a 100 year old brand name that’s recognized in virtually all 190+ countries in the world.”

Study Finds Fintech Puts Customer Rentention on the Clock with Biometrics

October 21, 2021 Onfido and Okta, a verification authenticity company and an independent identity provider, respectively, found that consumer-based businesses —regardless of industry—need to earn their customer’s trust in no longer than ten minutes or risk losing their business altogether.

Onfido and Okta, a verification authenticity company and an independent identity provider, respectively, found that consumer-based businesses —regardless of industry—need to earn their customer’s trust in no longer than ten minutes or risk losing their business altogether.

According to the report, 65% of customers who want to open a bank account want the process to be less than ten minutes, 69% when booking a car rental, 72% when opening a telemedicine account, and 77% when registering a gaming account, among other industries.

“From the moment a consumer visits a service provider’s website or downloads an app, they’re evaluating whether the business can deliver a trusted digital service, providing security and keeping their data private,” says Mike Tuchen, CEO of Onfido. “Businesses have just minutes to establish the confidence that consumers expect in the digital world. Those that can offer low or zero friction during verification and authentication will positively differentiate themselves in a market where digital services have become the norm and consumer trust breeds brand loyalty.”

After surveying 5,000 consumers from across the United States and Europe, the companies found that the moment the onboarding process begins in a virtual space, customers aren’t looking to spend much time putting information into a database to complete their transaction. The study found that customers felt that brands should know and trust them, while also having a strong desire for a seamless verification process rather than a fraud-preventing rigorous one.

Half of consumers expect that it should take less than three minutes to approve a banking transaction (49%) or place a bet (48%), and approximately 1 in 3 (35%) consumers believe it should take the same time to fill prescriptions.

Those consumers that were evaluated also desired to have companies recognize them on multiple devices, which just a third of responses claimed businesses currently do. 70% of customers claimed they “suffered” from a lack of an efficient digital process in a business transaction. Biometrics, according to the study, will be a way to solve these inefficiencies in the authentication and transactional software space.

In a blog post that accompanied the release, Onfido broke down the confidence that consumers have in Biometrics in the marketplace. According to them, 80% of customers have confidence in both the convenience and security of Biometrics.

“Let’s say you’ve verified an identity document. You need Onfido’s biometric technology to verify that the document truly belongs to the person making the transaction. So biometrics adds a layer of protection against stolen IDs and impersonation attacks,” the blog reads.

“Ensuring that digital account onboarding and access meets users’ expectations for speed, experience and security will require many businesses to reassess their identity platform requirements,” says Ben King, Regional Chief Security Officer, Okta. With biometric recognition putting identity at the heart of the authentication process to offer a robust yet seamless experience across any and every device, it is little surprise that consumers worldwide are increasingly opting for it in place of traditional passwords or in-branch verification checks.”

Google to Purchase Manhattan Building in Mega Deal

September 21, 2021 In the footsteps of other giant companies like Facebook and Amazon, it seems that Google has joined in on buying a tremendous piece of New York City office space, as Google’s parent company Alphabet has announced a tentative $2.1 billion deal Tuesday to purchase the building they already lease.

In the footsteps of other giant companies like Facebook and Amazon, it seems that Google has joined in on buying a tremendous piece of New York City office space, as Google’s parent company Alphabet has announced a tentative $2.1 billion deal Tuesday to purchase the building they already lease.

Under extensive renovations, Google plans on making a 1.7 million square foot community of office space by adding the former freight terminal to their New York offices— competing with some of the biggest names and workspaces in the city.

Google will remain in complete control of two other office spaces in Soho and Greenwich Village in conjunction with the new acquisition on the Hudson. The combination of these three offices will create a campus-esque environment for the tech giant. All the offices are within about a mile radius of one another.

First reported by the Wall Street Journal, the purchase is New York’s largest single office building sale since pre-pandemic days, while also being one of the biggest purchases in New York City commercial real estate history.

As smaller fintech companies are seemingly leaving the city in droves, it is the big players in the industry who are looking to stick around and ride out Manhattan’s post-pandemic and remote work woes.

It seems that Google, along with the other tech giants, are expecting a large in-person working environment to return to New York. According to CEO Sundar Pichai in an announcement on Google’s blog from August 31, the company plans on keeping remote work an option for all employees until January 10. After that, they are leaving it up to local officials to dictate if employees can be asked to return in person.

“To make sure everyone has ample time to plan, [employees will] have a 30-day heads-up before [they’re] expected back in the office,” Pichai wrote.

With Facebook’s acquisition of office space at Penn Station and Amazon’s purchase of Lord and Taylor’s former 5th Avenue landmark building, Google is late to the Manhattan real estate grab. These giants are paying top dollar for these spaces, as eight-figure real estate deals are status quo for a city that is littered with empty storefronts and a questionable future for many of its longtime tenants.

Google has a track record of building a presence in New York. An east coast presence is nothing new for the company. “Our investment in New York is a huge part of our commitment to grow and invest in U.S. facilities, offices and jobs,” wrote SVP and CFO Ruth Porat on a Google Blog back in 2018 when the lease agreement for the building was made.

Earlier this year, the company committed to a $150 million investment in New York workspaces.

Google’s new offices will serve as the main hub of their New York City offices. As the new year arrives, Google expects to see 1/5 its workforce still remote. With their new offices already functioning, the new office should complete the Google campus in 2023.

It seems that Silicon Valley’s presence may be creeping East as the finance industry continues to head South. With the price of commercial real estate sky high, the reputation for the city at a low, and a political climate that is creeping its way into business, it seems as if New York may be evolving into the East Coast Silicon Valley hub.