technology

Snapchat Acquired Mobile Shopping App Founded By Former MCA Execs

July 2, 2021 A brother and sister team formerly known throughout the merchant cash advance industry have achieved major success in another market altogether, mobile shopping.

A brother and sister team formerly known throughout the merchant cash advance industry have achieved major success in another market altogether, mobile shopping.

Recently, their app was acquired by Snapchat, according to various news outlets, and the tech has since been integrated into the Snapchat app.

Molly and Meir Hurwitz, both original stalwarts of the old Pearl Capital in New York, co-founded Screenshop in 2017, an app that integrated shopping with fashion and social media. Its initial launch received added buzz thanks to Kim Kardashian’s early involvement as an advisor. Notably, Screenshop CEO Mark Fishman was previously a Risk Manager at Pearl Capital, rounding out the former MCA crew.

“We’re No. 5 on the app store category of fashion,” Meir Hurwitz told deBanked in November 2017. “We’re just getting started.”

The success continued.

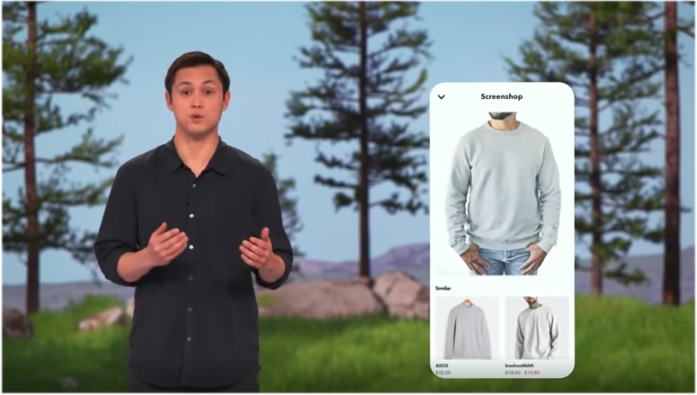

“Screenshop gives shopping recommendations from hundreds of brands when you Scan a friend’s outfit,” Snapchat wrote in a published announcement this past May.

More than 170 million Snapchatters use scan features every month, the company revealed.

“Screenshop is now a part of ‘Scan’ said Snapchat CTO Bobby Murphy during the company’s annual Partner Summit broadcast on May 20. The above screenshot is of Murphy demonstrating the Screenshop technology.

Ocrolus Named #1 Fastest Growing Fintech By Inc.

September 1, 2020 Ocrolus, a document analytics company, was recently named Inc.’s #1 fastest growing fintech company in the US and #1 fastest growing software company in NYC. The rating is based on percentage revenue growth between 2016 and 2019. Ocrolus placed as the #30 fastest-growing private company in America overall.

Ocrolus, a document analytics company, was recently named Inc.’s #1 fastest growing fintech company in the US and #1 fastest growing software company in NYC. The rating is based on percentage revenue growth between 2016 and 2019. Ocrolus placed as the #30 fastest-growing private company in America overall.

Ocrolus was founded in 2014 and has grown by 8,000% to become an industry-leading document scanning platform. Automating document applications for partners like BlueVine, Cross River, and Square, Ocrolus recently facilitated 761,455 small business applications for PPP loans.

So what sets Ocrolus apart? CEO and Co-Founder Sam Bobley credits the growth factor on just how fast and accurate the Ocrous API is.

“Lenders who were not using Ocrolus were not able to get to underwriting decisions as fast as lenders that were using Ocrolus- we saw a domino effect,” Bobley said. “Once we got a few big consumers on the platform, we were able to quickly onboard more and more funders and help them increase speed in their underwriting process.”

Bobley also said that while competitor document applications struggle with the accuracy at which they can read documents, landing somewhere in the 70-85% accuracy area, Ocrolus boasts more than 99% accuracy.

Success snowballed, and Ocrolus was helping grow businesses. The API directly addresses many financial institutions’ problems with scale- typically, more applications require more manpower to sift through paperwork.

“Typically, when a customer starts using our platform, within one year of using our platform, they double their volume, and within two years they quadruple,” Bobley said. “One of the reasons for that is they no longer have to staff up and deal with the operational complexities of handling the fluctuating volume of loans.”

With Ocrolus plugged in, customers were free from a major operating cost, and could go all out taking on new clients- which would mean more paperwork to process with Ocrolus.

Today, the company employs more than 900 team members across four offices but was founded in New York City. And like Seinfeld, Bobley loves the city, especially as a thriving hub for fintech activity.

“There’s no better place to do it than in the heart of the financial center of the US here in New York City,” Bobley said. “We’re right near where a lot of our lender customers are operating.”

On the news of recent acquisitions and reports that companies like PayPal and Intuit are ramping up their involvement in small business lending, Bobley said he sees larger entities in fintech as an opportunity for pricing transparency and better access to capital.

“I think the headline here is that financial services firms are recognizing that there’s a significant amount of businesses that used to be underserved,” Bobley said. “The bigger players are raising their eyebrows and want to get more involved, which in my opinion will be ultimately good for small business.”

And when it came time for Ocrolus to do its part for small business, Bobley said that more than 430,000 PPP applications of the 761,455 that were made using their partner network got approved, saving an estimated 1.5 million jobs.

“It’s always great when you know you can connect your work to a greater purpose for the community, so it’s really just a cool rewarding experience,” Bobley said. “It’s been fantastic, but we think we’re still in the early innings in terms of what we can do as a company- not just in small business lending but also in consumer mortgage and auto.”

Open Banking: Canada Might Not Be Able to Make Up for Lost Time

January 22, 2020

Over the last two years, open banking has become a matter of public conversation in Canada. Most would agree there is overwhelming support for the implementation of an open banking regime. So why has nothing concrete happened yet?

2019 turned out to be an exciting, yet painfully underwhelming year for open banking in Canada. The news media finally caught on to the movement and started publishing stories on the rise of robo-advisor apps, or how small and medium-sized businesses would be impacted, and so forth. Experts and industry leaders pitched in with a massive volume of op-eds, most of which were in support of open banking, and with many deploring Canada’s slowness. Some came to our podcast to discuss their perspective (spoiler: customer-centricity is a very big theme.)

Another telling sign of the importance of open banking is the fact that at the federal level, both the legislative and executive arms of the government have become actively engaged in the public conversation. The Senate of Canada’s committee on Banking, Trade and Commerce produced a well-researched report — perhaps the most valuable contribution to the conversation. This report calls for swift action on the part of the federal government to advance a regulatory framework for open banking. In parallel, the Department of Finance’s appointed advisory committee on open banking held a consultation with key stakeholders and should publish its own report in the near future.

Even to a casual observer, there was an obvious sense that Canada is ready to embrace open banking.

But here’s the thing: despite all this work and evidence of widespread support, Canada didn’t move the needle on open banking in any concrete way.

Who’s leading?

The UK has already implemented a comprehensive open banking regime, and continental Europe is close behind. Dozens more countries are working toward their own versions. Among the various geographies moving in this direction, some are opting for a government-led approach, the UK probably being the best example. Others, like the US, tend to be more market-driven. In Canada, the main stakeholders are still largely hesitant about where to strike the balance between the two approaches — and the result is that so far, both have failed to provide the leadership that would allow open banking to move forward.

The Department of Finance’s advisory committee was tasked to study the “merits of open banking”. This line of inquiry feels very old, and for good reason: to question whether we should have open banking or not is a false debate, and a time-wasting rabbit hole. The real question Canada should be asking itself when it comes to open banking is, “what is the objective we want to achieve here?”

Let’s take a few steps back to realize just how important this question is.

The UK had a very clear vision for their open banking regime. The Competition and Markets Authority had assessed that the oligopolistic dynamics of the banking sector were putting consumers at a disadvantage. Thus, the UK set on their open banking journey with a very precise objective in mind: make it easier for consumers to switch providers. While some take great pride in criticizing the UK’s implementation — stating that its objective was either wrong, too narrow, or poorly executed — the fact remains that they are ahead of the pack. And the UK’s leadership in this area still persists, with the Financial Conduct Authority now studying the question of extending the current open banking regime into a holistic open finance regime.

Meanwhile, in Canada, the government is trying to wrap its head around the big questions, such as the liability framework that should be put in place for an open banking regime to be viable. (In other words, in a system where financial services are decentralized, how do we go about making the consumer whole when something goes wrong?) However, without a decision on what end state we are looking to achieve with open banking, these conversations are doomed to keep looking exactly like they’re looking now: a bunch of market actors with conflicting interests pretending they know what’s best for consumers. Conversations happening in industry groups aren’t much more productive, with the “trench war” dynamics being the trend there as well.

Meanwhile, in Canada, the government is trying to wrap its head around the big questions, such as the liability framework that should be put in place for an open banking regime to be viable. (In other words, in a system where financial services are decentralized, how do we go about making the consumer whole when something goes wrong?) However, without a decision on what end state we are looking to achieve with open banking, these conversations are doomed to keep looking exactly like they’re looking now: a bunch of market actors with conflicting interests pretending they know what’s best for consumers. Conversations happening in industry groups aren’t much more productive, with the “trench war” dynamics being the trend there as well.

The irony is that the technical aspects of open banking can be dealt with easily. From a technical standpoint, financial data-sharing APIs have proven their effectiveness, and coming up with a shared technical standard should not be too difficult. The real challenge is coming up with a framework everyone — incumbents and new entrants alike — can rally behind, something industry groups have largely been ineffective at.

Canada’s highly concentrated financial services sector is a stable one, but incumbents are not likely to open themselves up to disruption. This is the part where bold political leadership is required.

The clock is ticking

Data sharing is nevertheless picking up, as 4 million Canadians (and counting) have made fintech apps a part of their financial lives. Consumers and businesses who want the benefits of on-demand data sharing must rely on the current generation of financial aggregators, like Flinks. This system may work as a de facto connectivity layer, but the lack of standards results in a clumsy patchwork of bilateral deals between aggregators and banks. It just isn’t a viable way to achieve an open banking regime that levels the playing field when it comes to data portability.

In its report, the Senate’s Committee on Banking, Trade and Commerce states that Canada “risks falling behind” if it fails to implement open banking, and that “without swift action, Canada may become an importer of financial technology rather than an exporter.” It is true that if we keep delaying open banking, our slowness will prove to be a very stingy and lasting price to pay for the Canadian society; this is why we need bold action now. We can’t afford the comfort of waiting until we’ve figured out the 100% perfect solution.

There’s nothing like a real-world example: 2020 opened with a seismic shift when financial giant Visa acquired Plaid, one of the largest US financial aggregators, for over five billion USD. This is hinting at a new phase where markets will consolidate around a few large players; Canada can either ride the tide or get towed under.

It’s time to be bold

In the end, what needs to happen for Canada to move forward with open banking?

Our financial services sector can be compared to those of the UK and Australia, where a few powerful banks control a very large portion of the market. In those two countries, open banking was designed to stimulate competition, and government action was necessary to get things moving.

Right now, the question politicians ought to ask shouldn’t be if — or even how — but why. A why will pave the way and provide a natural direction to sort out the how. In 2019, discussions around open banking lacked this fundamental feature: political leadership centered on a bold, ambitious, consumer-centric mission statement. A why.

So here’s one for 2020: open banking will increase consumers’ choice when it comes to financial services. That would be a good start — and while good is not perfect, it still beats nothing by a landslide.

Amazon Says Browser Extension No Longer Secure, Just After PayPal Acquired It

January 13, 2020Last week Politico reporter Ryan Hutchins noted on Twitter that Amazon has been alerting its website users who had installed Honey that the browser extension is no longer safe. The extension, which searches the web for sales coupons for items in your checkout basket and automatically applies them, was recently acquired by PayPal for $4 billion. The deal was agreed upon in November and completed last week. According to Hutchins, such warnings have been viewed by Amazon customers since just before Christmas.

Amazon is telling shoppers that the browser extension Honey — it gives you coupon codes and other ways to save — is malware.

Paypal bought Honey in November for $4 billion. That’s one extensive piece of Malware. pic.twitter.com/Di6I8RAX2X

— Ryan Hutchins (@ryanhutchins) December 20, 2019

Having been compatible for years without any security warnings from Amazon, critics have now raised the question over whether this was intentionally done to level competition between the two tech giants. Honey makes a profit by charging retailers a percentage of the sales made with the coupons that it finds, and with this now under PayPal’s umbrella, Amazon may no longer be comfortable taking that hit. Especially when its own Amazon Assistant offers a similar experience.

Having been compatible for years without any security warnings from Amazon, critics have now raised the question over whether this was intentionally done to level competition between the two tech giants. Honey makes a profit by charging retailers a percentage of the sales made with the coupons that it finds, and with this now under PayPal’s umbrella, Amazon may no longer be comfortable taking that hit. Especially when its own Amazon Assistant offers a similar experience.

Speaking to The Verge, an Amazon spokesperson said that “Our goal is to warn customers about browser extensions that collect personal shopping data without their knowledge or consent.” A charge against Honey that did not seem to stick for Hutchins, who continued on Twitter with, “That’s how all browser extensions work – including Amazon’s own extension.”

During the summer, a security vulnerability was found in the browser extension only to be quickly patched. Following the coverage of this latest security warning, a Honey spokesperson stated to Wired that “We only use data in ways that directly benefit Honey members – helping people save money and time – and in ways they would expect … Our commitment is clearly spelled out in our privacy and security policy.”

Google to Begin Offering Checking Accounts in 2020

November 16, 2019 This week Google announced that it plans to offer checking accounts to customers in 2020. The news comes after the release of the Apple Card, Apple and Goldman Sach’s controversial joint project, in August; this week’s release of Facebook Pay; and the mass exodus by payments companies from Facebook’s Libra Association last month.

This week Google announced that it plans to offer checking accounts to customers in 2020. The news comes after the release of the Apple Card, Apple and Goldman Sach’s controversial joint project, in August; this week’s release of Facebook Pay; and the mass exodus by payments companies from Facebook’s Libra Association last month.

Titled as Google’s ‘Cache’ project, the accounts will be the result of a partnership between the tech giant and a selection of banks and credit unions. Thus far, Citigroup and a credit union based in Stanford University have been confirmed as partners, with more to be announced. Speaking on the venture, Citigroup spokesperson Liz Fogarty said the “agreement has the potential to expand the reach and breadth of our customer base.” Whereas Joan Opp, President and CEO of Stanford Federal Credit Union, remarked that the deal would be “critical to remaining relevant and meeting customer expectations.”

As of yet, not much is known beyond these partners and that the checking accounts will be in some way “smart” according to Google spokesperson Craig Ewer. Whether or not there will be fees attached to the accounts, or who will be the target audience remain unsure. The latter especially given Google Pay’s poor take up in America.

As well as all this, it is equally unclear what exactly Google will be bringing to banking that is new. In his statement, Ewer said that “we’re exploring how we can partner with banks and credit unions in the US to offer smart checking accounts through Google Pay, helping their customers benefit from useful insights and budgeting tools while keeping their money in an FDIC or NCUA-insured accounts.” Such “insights” and “tools” are yet to be expanded upon and may give cause to alarm, as the company has recently come under fire for its questionable use of data after it was revealed that Google has secretly gathered the personal medical data of 50 million Americans from healthcare providers; and has recently been accused of using both human contractors and algorithms to tweak search engine results, potentially exhibiting favoritism as well as a willingness to change results related to at least one major advertiser.

When asked by CNBC about Google’s plans to enter finance, Senator Mark Warner (D) was apprehensive, remarking that “large platform companies have not had a very good record of protecting the data or being transparent with consumers.” Warner, who was a tech entrepreneur before entering politics, believes more regulation should be in place as the number of tech companies looking to enter finances continues to increase, saying, “once they get in, the ability to extract them out is going to be virtually impossible.”

Such comments come in the wake of Facebook CEO Mark Zuckerburg’s testimony to Congress last month, in which he told the representatives: “I view the financial infrastructure in the United States as outdated.” Just how outdated Zuckerburg and his contemporaries believe it to be will become clearer as more of these Big Tech-Wall Street hybrids are released.

Is Your Firm Ready for Machine Learning?

October 15, 2018Artificial intelligence such as machine learning has the potential to dramatically shift the alternative lending and funding landscape. But humans still have a lot to learn about this budding field.

Across the industry, firms are at different points in terms of machine learning adoption. Some firms have begun to implement machine learning within underwriting in an attempt to curb fraud, get more complex insights into risk, make sounder funding decisions and achieve lower loss rates. Others are still in the R&D and planning stage, quietly laying the groundwork for future implementation across multiple areas of their business, including fraud prevention, underwriting, lead generation and collections.

“It’s entirely critical to the success of our business,” says Paul Gu, co-founder and head of product at Upstart, a consumer lending platform that uses machine learning extensively in its operations. “Done right, it completely changes the possibilities in terms of how accurate underwriting and verification are,” he says.

While there’s no absolute right way to implement machine learning within a lender’s or funder’s business, there are many data-related, regulatory and business-specific factors to consider. Because things can go very wrong from a business or regulatory perspective—or both—if machine learning is not implemented properly, firms need to be especially careful. Here are a few pointers that can help lead to a successful machine learning implementation:

Using machine learning, funders can predict better the likelihood of default versus a rule-based model that looks at factors such as the size of the business, the size of the loan and how old the business is, for example, says Eden Amirav, co-founder and chief executive of Lending Express, a firm that relies heavily on AI to match borrowers and funders.

Machine learning takes hundreds and hundreds of parameters into account which you would never look at with a rule-based model and searches for connections. “You can find much more complex insights using these multiple data points. It’s not something a person can do,” Amirav says.

He contends that machine learning will optimize the number of small businesses that will have access to funding because it allows funders to be more precise in their risk analyses. This will open doors for some merchants who were previously turned down based on less precise models, he predicts. To help in this effort, Lending Express recently launched a new dashboard that uses AI-driven technology to help convert business loan candidates that have been previously turned down into viable applicants. The new LendingScore™ algorithm gives businesses detailed information about how they can improve different funding factors to help them unlock new funding opportunities, Amirav says.

Lenders and funders always have to be thinking about what’s next when it comes to artificial intelligence, even if they aren’t quite ready to implement it. While using machine learning for underwriting is currently the primary focus for many firms, there are many other possible use cases for the alternative lenders and funders, according to industry participants.

Lead generation and renewals are two areas that are ripe for machine learning technology, according to Paul Sitruk, chief risk officer and chief technology officer at 6th Avenue Capital, a small business funder. He predicts that it is only a matter of time before firms are using machine learning in these areas and others. “It can be applied to several areas within our existing processes,” he says.

Collection is another area where machine learning could make the process more efficient for firms. Machines can work out, based on real-life patterns, which types of customers might benefit from call reminders and which will be a waste of time for lenders, says Sandeep Bhandari, chief strategy and chief risk officer at Affirm, which uses advanced analytics to make credit decisions.

“There are different business problems that can be solved through machine learning. Lenders sometimes get too fixated on just the approve/decline problem,” he says.

“Most underwriters don’t have enough data to effectively incorporate AI, deep learning, or machine learning tools,” says Taariq Lewis, chief executive of Aquila, a small business funder. He notes that effective research comes from the use of very large datasets that won’t fit in an excel spreadsheet for testing various hypotheses.

Problems, however, can occur when there’s too much complexity in the models and the results become too hard to understand in actionable business terms. For example, firms may use models that analyze seasonal lender performance without understanding the input assumptions, like weather impact, on certain geographies. This may lead to final results that do not make sense or are unexpected, he says.

“There’s a lot of noise in the data. There are spurious correlations. They make meaningful conclusions hard to get and hard to use,” he says.

The more precise firms can be with the data, the more predictive a machine learning model can be, says Bhandari of Affirm. So, for example, instead of looking at credit utilization ratios generally, the model might be more predictive if it includes the utilization rate over recent months in conjunction with debt balance. It’s critical to include as targeted and complete data as possible. “That’s where some of our competitive advantages come in,” Bhandari says.

Underwriters also have to pay particularly close attention that overfitting doesn’t occur. This happens when machines can perfectly predict data in your data set, but they don’t necessarily reflect real world patterns, says Gu of Upstart.

Keeping close tabs on the computer-driven models over time is also important. The model isn’t going to perform the same all along because the competitive environment changes, as do consumer preferences and behaviors. “You have to monitor what’s going well and what’s not going well all the time,” Bhandari says.

Certainly, as AI is integrated into financial services, state and federal regulators that oversee financial services are taking more of an interest. As such, firms dabbling with new technology have to be very careful that any models they are using don’t run afoul of federal Fair Lending Laws or state regulations.

“If you don’t address it early and you have a model that’s treating customers unfairly or differently, it could result in serious consequences,” says Tim Wieher, chief compliance officer and general counsel of CAN Capital, which is in the early stages of determining how to use AI within its business.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

“AI will be transformative for the financial services industry,” he predicts, but says that doing it right takes significant advance planning. For instance, Wieher says it’s very important for firms to involve legal and compliance teams early in the process to review potential models, understand how the technology will impact the lending or funding process and identify the challenges and mitigate the risk.

To be sure, regulation around AI is still a very gray area since the technology is so new and it’s constantly evolving. Banking regulators in particular have been looking closely at the issues pertaining to AI such as its possible applications, short-comings, challenges and supervision. Because the waters are so untested, there can be validity in asking for regulatory and compliance advice before moving ahead full steam, some industry watchers say.

Upstart, for example, which uses AI extensively to price credit and automate the borrowing process, wanted buy-in from the Consumer Financial Protection Bureau to help ease the concern of its backers as well as to satisfy its own concerns about the legality of its efforts. So the firm submitted a no-action request to CFPB. The CFPB responded by issuing a no-action letter to Upstart in September 2017, allowing the company to use its model. In return, Upstart shares certain information with the CFPB regarding the loan applications it receives, how it decides which loans to approve, and how it will mitigate risk to consumers, as well as information on how its model expands access to credit for traditionally underserved populations.

The No-Action Letter is in force for three years and Upstart can seek to renew it if it chooses.

Theoretically firms could have a computer underwriting model constantly updating itself without having a human oversee what the model is doing—but it’s a bad idea, industry participants say. “I believe there are companies doing that, and it’s a risky thing to do,” says Scott M. Pearson, a partner with the law firm Ballard Spahr LLP in Los Angeles.

During review of the models—and before implementing them—people should carefully review the models and the output to make sure there’s nothing that causes intrinsic bias, says Kathryn Petralia, co-founder and president of Kabbage, which is one of the front-runners in using machine learning models to understand and predict business performance.

“If you’re not watching the machine, you don’t know how the machine is complying with regulatory requirements,” she says.

Kabbage has teams of data scientists regularly developing models that the company then reviews internally before deploying. The company is also in frequent contact with regulators about its processes. Petralia says it’s very important that firms be able to explain to regulators how their models work. “Machines aren’t very good at explaining things,” she quips.

As a best practice, Pearson of Ballard Spahr says lenders and funders shouldn’t use any machine learning model until it’s been signed off on by compliance. “That strikes a pretty good balance between getting the benefits of AI and making sure it doesn’t create a compliance problem for you,” he says.

While AI has many benefits, industry participants say alternative lenders and funders need to be mindful of how it can be applied practically and effectively within their particular business model.

Craig Focardi, senior analyst with consulting firm Celent in San Francisco, contends that the classic FICO score continues to be the gold standard for credit decisions in the U.S. He warns firms not to get overly distracted trying to find the next best thing.

“Many fintech lenders have immature risk management and operations functions. They’re better off improving those than dabbling in alternative scoring,” he says, noting that data modeling is an entirely separate core competency.

Indeed, Lewis of Aquila cautions underwriters not to view AI as a silver bullet. “AI is just one tool out of many in the lenders’ toolbox, and our industry should use it and respect its limitations,” he says.

Did UCC Lead Generators Overload NY State’s System?

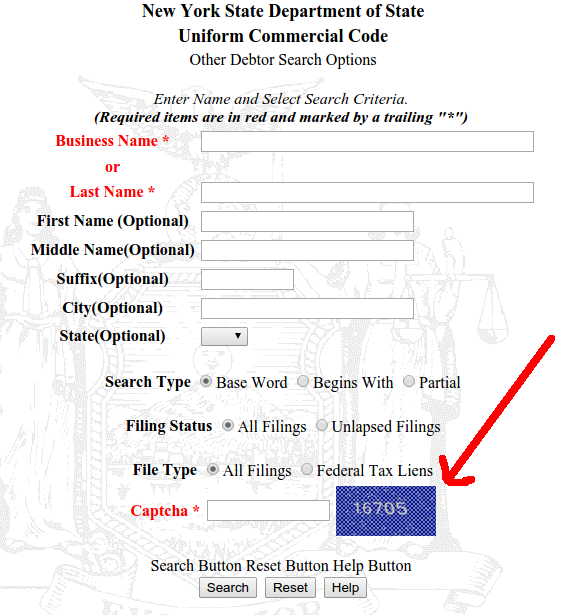

April 4, 2017 In the small business finance industry, New York State is known as one of the friendliest places to conduct a UCC search. You can not only search by debtor, but also by secured party, and get just about everything you need to create a list of prospects for free.

In the small business finance industry, New York State is known as one of the friendliest places to conduct a UCC search. You can not only search by debtor, but also by secured party, and get just about everything you need to create a list of prospects for free.

But the State’s website isn’t exactly a pillar of technological achievement. Indeed, the UCC Lien Search welcome page makes clear that searchers will need to be using Netscape Navigator 4.0 or higher and that version 3.0 of Internet Explorer or lower is not supported. Those browser iterations were released in 1997 and 1996 respectively, before some in the business finance industry were even born.

And the online system built for Windows 3.1 users didn’t seem to be doing so well over the last few months. Routine manual searches that I occasionally conduct were leading to error messages and crash pages instead of results. Were UCC lead generators querying the system to death?

Last week, New York took the entire UCC system down for “maintenance” and when it finally came back up, a tool to combat automated queries had been installed.

Curiously, this has only been implemented for secured party searches and other debtor search options. Standard debtor search options remains unchanged.

As Captchas are designed to thwart automated queries, could this be a sign that lead generators were crashing the system?

To check it out yourself, it’s best to be using Windows 95 or higher. Typewriters and Etch-A-Sketch users may experience performance issues.

OnDeck CEO Noah Breslow Talked Tech Worker Shortage in Canada on BloombergTV

March 22, 2017On BloobergTV Canada, OnDeck CEO Noah Breslow explained what he thought the country could do to boost innovation. The discussion stemmed from Canada’s decision to set aside C$800 million over the next four years to carry out that objective.

Breslow said that since Canada has excellent schools, those graduates can be nurtured into forming businesses and creating business investment opportunities. He also said that vocational training towards today’s new working-style job would be beneficial as well, whether it’s jobs for people who can design the latest algorithm or people who can build systems and data centers or can rack servers together.

When asked if perhaps government intervention was not the answer to achieve this, Breslow said that there are two ends of that spectrum, and where he believed intervention could be helpful was in the formation and talent development and formation incubation stage of companies. For later-stage companies, it was probably not appropriate, he said.

Breslow also expressed his belief that a permissive immigration policy is important and that there should be less friction to bring in skilled workers to Canada.

You can watch the full video below to hear the rest: