Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Loan Brokers: Here’s How to Submit a Deal to a Licensed California Lender

February 24, 2016 Brokers that wish to submit deals to a licensed California lender must also be licensed in the state. This does not apply when the lender is lending via a chartered bank relationship or if the transaction itself is a purchase of future receivables (AKA a traditional merchant cash advance). QuarterSpot for example, recently became a licensed lender (#603-K646) and will be operational to lend in the state starting on March 7th, according to the company.

Brokers that wish to submit deals to a licensed California lender must also be licensed in the state. This does not apply when the lender is lending via a chartered bank relationship or if the transaction itself is a purchase of future receivables (AKA a traditional merchant cash advance). QuarterSpot for example, recently became a licensed lender (#603-K646) and will be operational to lend in the state starting on March 7th, according to the company.

While the process wasn’t easy, they want to make sure that brokers are abiding by the rules as well. To this end, QuarterSpot EVP Mike Green posted a link on the deBanked forum to the licensing form that brokers must complete to apply:

We will require our partners to submit their CFLL License as required by the State. Please send those in ASAP to partners@quarterspot.com

1. Licensing form outlining requirements for licensure – http://www.dbo.ca.gov/forms/Finance_Lenders/DBO_CFLL_1422.pdf

2. Article further explaining legislation – http://www.paulhastings.com/publications-items/details/?id=e867e669-2334-6428-811c-ff00004cbded

In addition to the 31 page application is the payment of a $25,000 Surety Bond. Suffice to say, the process and costs are probably not a good fit for a 2-man upstart loan brokerage with a razor thin budget working out of month-to-month office space. But for a moderately sized operation or bigger, being a licensed broker can potentially be a competitive advantage.

The reason that brokers don’t need to be licensed to send deals to lenders like OnDeck, is because OnDeck operates through a chartered bank relationship and is therefore exempt from licensing requirements. As always, ask an attorney for an opinion if you’re not sure or need help. A broker may be just as culpable for submitting a deal to an unlicensed lender as the lender would be for operating unlicensed.

You can check to see if a lender is licensed at http://www.dbo.ca.gov/fsd/licensees/ but keep in mind that the database is rarely updated (the last time was 2 months ago).

Other helpful information

Can California Lenders Pay Referral Fees to Unlicensed Brokers?

Getting a California Lender’s License

OnDeck Regains Their Swagger in Q4 Earnings Call – Lends $1.9 Billion in 2015

February 23, 2016 OnDeck’s chief executive Noah Breslow and chief financial officer Howard Katzenberg brimmed with confidence in their Q4 earnings call, assuring investors that it’s full steam ahead. After two previous quarters of profitability and getting no love from the market for it, they’re back to doing what they know best, growing.

OnDeck’s chief executive Noah Breslow and chief financial officer Howard Katzenberg brimmed with confidence in their Q4 earnings call, assuring investors that it’s full steam ahead. After two previous quarters of profitability and getting no love from the market for it, they’re back to doing what they know best, growing.

OnDeck loaned a record $557 million in Q4, an increase of 51% year-over-year. Despite market fears of an impending economic downturn, the company is just not seeing signs of the alleged doom in the performance of their loans. “We are not seeing weakness in our portfolio at this time,” Breslow said.

Later in the call they reemphasized that their early warning systems are not setting off any alarms. In fact, they said, origination growth is their main goal in 2016. “We currently believe we can grow annual originations by 45% to 50% in 2016,” Katzenberg said.

OnDeck reminded investors that their unique model is specifically built for economic downturns. Among their strengths are their short duration, pricing spreads and daily payments, they said. Those attributes (which are sometimes criticized by consumer groups today) will serve as the backbone of sustainability if the economy goes south.

Also coming back into the fold are outside brokers, which they refer to as “Funding Advisors.” OnDeck spent a lot of time recertifying those relationships in 2015 and the bulk of the effort associated with that is over, they said. The percentage of loans generated from brokers rose from 18.6% in Q3 to 20.1% in Q4.

They also rebuffed speculation that they were giving up their business model in favor of becoming a bank technology service. While they admitted finding value in the partnerships they’ve formed, particularly with JPMorgan Chase, their core business is and will continue to be lending to small businesses. According to Katzenberg, 2016 will have two key objectives however, “One, launching and refining our pilot program with Chase, and two, continuing to build out our infrastructure to add and support additional partners that understand the small business capital assets problem and are willing to invest in a great customer experience.” They expect to see bank service revenues really begin to scale in 2017 and 2018.

Breslow said in regards to the Chase deal, “Chase will be able to offer almost real-time approvals in the same or next day funding a dramatic improvement over a traditional loan process that might take weeks. Chase will hold the loans, which will be priced like bank products on their balance sheet and OnDeck will earn servicing and platform fees based on volume.”

Their 15+ Day Delinquency ratio was down.

Their partnerships with Minor League Baseball and Barbara Corcoran have been very successful.

They lent $1.9 billion in 2015 across the U.S., Canada, and Australia.

Steal A Deal, Go To Jail – MCA Broker Takes Fight Over Backdoored Deals To Law Enforcement

February 22, 2016 A suspicion over stolen deals has led to the arrest of a sales agent, deBanked has learned.

A suspicion over stolen deals has led to the arrest of a sales agent, deBanked has learned.

It’s yet another case of a deal slipping out the back door, one that resulted in handcuffs, according to multiple sources familiar with the matter. deBanked obtained evidence of the arrest, which happened earlier this month, and confirmed the identity of the individual charged.

A sales agent’s ill-fated meeting with law enforcement began when an MCA brokerage suspected their hard-fought applications were being rerouted to a third party by way of a New York based funding company they usually submit to, according to one source. To confirm these suspicions, they submitted at least one funding application that was tagged with a specially designated phone number that they possessed. The tactic would allow them to do a clean trace on their deal by seeing who called upon that number, multiple sources confirmed.

Sure enough, someone other than the funding company reached back out to them, not knowing it was a trap. Unfortunately, that call wasn’t conclusive enough to connect it to the funder, according to one source. The sales agent attempting to snatch the deal wasn’t employed by the funder and the funder wasn’t sure how the sales agent was getting the deal in the first place. Somehow this guy was getting data he wasn’t supposed to be getting and the funder wanted nothing more than to make sure their integrity remained intact, a source said.

The victimized brokerage set their sights on the rogue sales agent and together with the cooperation of the local police department, apparently staged a sting operation. The rogue agent allegedly attempted to sell the stolen deal data to an undercover cop who was assisting with the case.

The suspect was charged with criminal possession of computer related material, a Class E felony, and released on recognizance three days later, according to arrest records obtained by deBanked. The penalty for such a crime can earn an offender up to 4 years in prison.

The funding company and brokerage are reportedly both relieved to have gotten to the bottom of the issue. Notably, in this case of deals slipping out the back door, it was the alleged recipient of the stolen deals that was charged. The hole that allowed him to get those deals in the first place has apparently resolved itself, sources said.

In the September/October 2015 issue of deBanked Magazine, interviewed MCA brokers agreed that the industry should police itself when it comes to backdooring. One brokerage, although not one that was named in that article, apparently took that advice literally when they enlisted the police to assist them.

All the sources to this story agreed that the arrest should serve as a warning. Backdooring deals has to stop, they concurred.

—

The name of the accused and the names of the sources in this story were kept anonymous because it’s an ongoing criminal matter. The suspect is innocent until proven guilty.

OnDeck Loans Record $557 million in Q4, But Reports $4.6 Million Loss

February 22, 2016 OnDeck funded a record $557 million in Q4 2015, generating $67.6 million in revenue. That came at a cost because they reported a $4.6 million GAAP net loss.

OnDeck funded a record $557 million in Q4 2015, generating $67.6 million in revenue. That came at a cost because they reported a $4.6 million GAAP net loss.

All told however, they loaned $1.9 billion to small businesses in the U.S., Canada and Australia for the full year of 2015.

A record $201.9 million of loans were sold through OnDeck Marketplace® in Q4.

Provision for loan losses during the fourth quarter of 2015 decreased to $20.0 million, down from $20.4 million in the comparable prior year period. The Provision Rate in the fourth quarter of 2015 was 5.6% compared to 6.7% in the comparable prior year period.

OnDeck was up nearly 5% for the day in the hours before earnings were reported. The company has regained some public favor after a partnership with JPMorgan Chase was announced in December. Still, critics have pointed out that the company’s last few positive quarters were dependent on their ability to sell existing loans off their balance sheet to book the necessary revenue to show a profit.

OnDeck has seemingly now returned to their original plan, growth over profits.

In Q3, origination growth had slowed. They reported a profit of $3.7 million on $482 million worth of loans originated. During that quarter, reliance on third party brokers slowed, dipping to 18.6% of their deal flow, but OnDeck CEO Noah Breslow hinted that they may have reached a floor in that ratio. That channel could stabilize and even grow a little bit, he said.

Q4 indeed saw a resurgence to 20.1% from the brokers.

The effectiveness of direct mail marketing was hotly debated in the 2015 Q2 Q&A, but seemed to have relaxed in Q3.

OnDeck’s share price was still down by more than 50% from their IPO, a factor that has potentially contributed to the postponement of other online lending IPOs.

A Loan Bazaar Where You Can Literally Buy Loans for Pennies – FOLIOfn

February 22, 2016 Welcome to the true marketplace where you can trade debt on any level you like

Welcome to the true marketplace where you can trade debt on any level you like

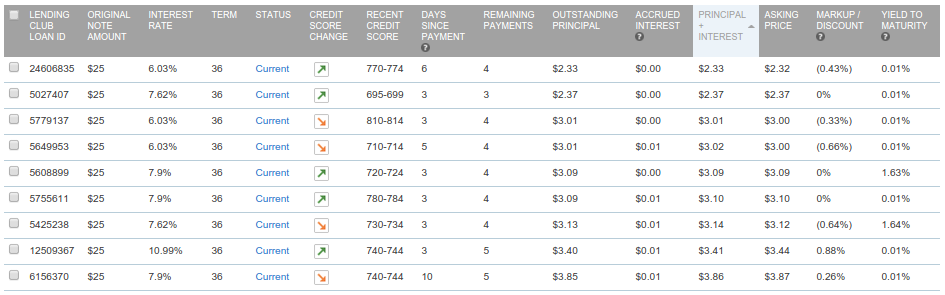

You haven’t experienced marketplace lending until you’ve entered the world of FOLIOfn. Operating as a secondary market for Lending Club and Prosper investors, the platform offers more than just liquidity for holders of 3-5 year consumer debt-backed notes. It’s a sort of anything-goes bazaar for loans, the kind of place where you can bet on a borrower making their last and final loan payment after having made 35 straight monthly payments with no problems.

For the price of 82 cents, an investor could literally buy the remaining 83 cent principal balance (their last payment) on a $25 3-year note.

Why invest in a borrower with no proven track record anyway? On FOLIOfn, you don’t have to. You can buy a note from someone else after the borrower has made their first few payments.

And what if you just want bigger? You can get that. Some investors are offering much larger loan pieces. You can even buy whole loans from them. Would you buy the entire remaining principal of a $6,000 loan paying 21% APR if you knew the buyer had already made all their payments in the first year on time? Somebody will make you that deal, but you’ll have to pay more than the outstanding principal balance to get it.

FOLIOfn has a bet for everyone. You can buy notes for example where the borrower’s FICO score has dropped by more than 200 points but is still surprisingly current on their loan. A drop by that much likely indicates that the borrower is delinquent on their other forms of credit, so you might want to get a discount on buying it. And yet, many investors list such loans at a premium, which could indicate that scarcity is a prevailing force.

The effects of scarcity are certainly evident on FOLIOfn, considering how many loans are up for sale on the platform in which no payments have been made yet because the loans are newly issued. With these, a different kind of loan speculator could hope to book a quick 5% gain in just 1 month by reselling a highly prized note to someone who seeks it. Do this over and over 12x a year and well… you could make a killing.

Millions of dollars worth of loans and loan pieces are being marketed at any one time. At the time this was written, there were more than 300,000 trades offered. Of course, they’re all ASKs. There’s no BIDs on FOLIOfn, which limits the efficiency of the marketplace and creates information asymmetry. Hence, a lot of the proposed trades are terrible and investors on industry forums are at times not shy about expressing their hope that a sucker buys them.

And just like one might expect at a bazaar, you don’t always know exactly what you’re going to get. Last year on the Lend Academy forum for example, investors pointed out that you could inadvertently buy notes that had already paid off. What was happening was that a note was being sold from one investor to another before Lending Club could process that the note had been paid off in full. If the investor paid a premium for it, they would immediately lose the premium and forfeit the future interest, causing a loss. The buyer would likewise take home a free premium.

Consider this conundrum. The note selling for 82 cents has a remaining principal balance of 83 cents that is coming due in less than a month, a bet that supposedly promises 1 cent profit (before the 1% Lending Club fee) if it works out. According to the borrower’s payment schedule however, they’re apparently only supposed to make one last payment of 76 cents, 7 cents less than the remaining principal officially stated on the account. If that’s correct, then a buyer’s best outcome is a loss of 6 cents (7 cents after the 1% Lending Club fee) and a worst case loss of 82 cents. It’s not uncommon for investors to notice and complain about these weird discrepancies (sometimes chalked up as rounding errors), but that’s the nature of the market. Confusing information is part of the trade.

To FOLIOfn’s credit, there is one cardinal rule, CAVEAT EMPTOR. The following is prominently displayed on top of the platform:

Notes are highly risky and only limited information is available about them. They are suitable only for investors whose investment objective is speculation. You could lose most or all of the money you invest in them. Folio Investing has no role in the original issuance of the Notes and is not responsible for and does not approve, endorse, review, recommend or guarantee the Notes or the accuracy, reliability, or completeness of any data or information about the Notes. See the Important Disclosures page for additional important information.

In the FOLIOfn loan bazaar, the numbers don’t always add up and the borrowers and traders are anonymous. Welcome to lending’s real marketplace, where it’s really hard to know much of anything.

Luckily, beginners only need bring pennies to start trading.

—

There’s actually something called The Penny Note Strategy (AKA The Toilet Note Strategy). You can read about it on Peter Renton’s blog.

Without Scalia, Media Outlets Reporting Marketplace Lenders Supposedly Doomed With Supreme Court Case (They’re Wrong)

February 18, 2016 Without Antonin Scalia, marketplace lending is apparently doomed, according to news outlets reporting on the matter. A high profile case (in the banking world anyway) known as Madden v Midland, is pending before the U.S. Supreme Court. Midland Funding seeks to reverse an appellate court ruling that said that interest rate preemption under the National Bank Act did not apply to them and thus they were subject to New York State’s usury laws.

Without Antonin Scalia, marketplace lending is apparently doomed, according to news outlets reporting on the matter. A high profile case (in the banking world anyway) known as Madden v Midland, is pending before the U.S. Supreme Court. Midland Funding seeks to reverse an appellate court ruling that said that interest rate preemption under the National Bank Act did not apply to them and thus they were subject to New York State’s usury laws.

According to BankRate.com’s reporting on the Scalia angle, “The U.S. Supreme Court has been asked to review a lower court decision that prevents marketplace lenders from getting around state usury laws by hooking up with banks headquartered in states that don’t have those rules.” But that’s not true at all. The case isn’t about marketplace lenders and the appellate court’s ruling isn’t currently preventing marketplace lenders from doing anything.

Midland Funding is a debt collector. Saliha Madden, a New York resident, obtained a bank issued credit card with an interest rate of 27% APR, racked up charges and didn’t pay them. The debt got written off and the bank sold the debt to Midland Funding. Midland continued to assess interest on the credit card debt while it attempted to collect. Saliha Madden sued on the basis that Midland was violating New York State usury laws. Midland Funding won and Madden appealed. Then a weird thing happened. The United States Court of Appeals for the Second Circuit held that in order “[t]o apply NBA preemption to an action taken by a non-national bank entity, application of state law to that action must significantly interfere with a national bank’s ability to exercise its power under the NBA.”

And from there began the somewhat justifiable panic in the marketplace lending industry. If a collector buying a charged-off debt from a bank can’t continue to enforce the terms as originally contracted, then could you make the same argument for loan platforms that buy newly issued loans? The answer is simply that you could make the argument. It’s not definitive. It’s one of those things that would likely have to be challenged in court by a borrower confident that a case involving a debt collector and a bank issued credit card somehow related to the matter between a marketplace lender and a borrower.

But there’s another problem in trying to make that link.

The Madden v Midland case involved a national bank and preemption under the National Bank Act. Many marketplace lenders such as Lending Club are not even conducting their business with national banks but with state-chartered banks. Their preemption ability falls under the Federal Deposit Insurance Act.

Lending Club did not shut their business down after the appellate court ruling and they didn’t stop lending in the states in which the Second Circuit has jurisdiction (New York, Connecticut and Vermont). Lending Club’s CEO Renaud Laplanche even expressed little worry about how it would impact their business when asked about it during their 2015 Q2 earnings call.

American Banker reported that “Scalia’s Death Is a Setback for Online Lenders in Key Court Fight.” But it’s really only a setback in the sense that a loss would peel away just one layer of the onion. Marketplace lenders weren’t going to suspend their operations regardless of whether or not the Supreme Court heard the case and regardless of whether or not Scalia was there to dissent.

Consider also that exporting home state interest rates using national and state chartered banks is only one system available to marketplace lenders. Square’s working capital program for example, is actually structured as a purchase of future receivables. There is no bank, no loan, and no preemption. An unfavorable Madden v Midland ruling would have no impact on that model or the dozens of merchant cash advance companies that offer similar products.

There’s also state by state licensing, which while costly and time consuming to set up, would at least allow marketplace lenders to lend in many states without relying on a bank or preemption. “I think the stronger business model is the state licensing model, as opposed to partnering up with a bank,” said Richard Eckman, a lawyer at Pepper Hamilton, to American Banker.

Even further distanced from this case are commercial marketplace lenders since state lending laws are generally less burdensome for business-to-business transactions.

And even if all else failed, a choice-of-law provision in a loan agreement can potentially decide which state’s law applies. Lending Club’s Laplanche said as much last year. “We continue to operate in the Second Circuit district where that decision was rendered, exactly as we did before and are relying on our choice of law provisions,” he said during an earnings call.

Scalia’s absence is at most a bummer for marketplace lenders. A win would only serve to tie up loose ends and finally put an end to bank charter model naysayers. Madden v Midland became so famous because the ruling was just so shocking. It practically begged the industry to take a look and wonder, what if? If this, then why not that? And if that, then who’s to say not this then? Even on deBanked, we’ve explored the nightmare scenario in which a well established system totally unravels and the world ends. The real world holds much more promise.

The real losers in an unfavorable Supreme Court ruling would be national banks and credit card companies. And that’s because if debt collectors can’t enforce their loan agreements, then they’re not going to buy that debt to begin with. And if debt collectors won’t buy that debt, then banks are going to have to figure out a better way to collect on their own, else they make even less risky lending decisions.

Something tells me though that banks would find a creative work-around for that anyway. Because if they didn’t, Madden v Midland would end up being a massive boon for marketplace lenders.

Imagine that.

DBRS Gives Marketplace Lenders High Marks

February 17, 2016After it was announced that new-age student lender Earnest had securitized $112 million worth of notes, another name returned to the forefront, DBRS. Founded in 1976 as Dominion Bond Rating Service, DBRS is a smaller ratings agency than Standard & Poor’s, Moody’s Investors Service and Fitch. Nonetheless, they rated Earnest’s senior notes an “A” which indicates they are of a “good” credit quality.

DBRS is a big name in the marketplace lending industry’s securitizations and they’ve historically doled out optimistic reports. In the case of SoFi for example, several tranches received AAA ratings in 2015, putting them on par with the United States Government in terms of safety.

Below is a list of some of the ratings stamped on new securitizations:

| Date | Company | Amount | DBRS Rating |

| 5/28/14 | OnDeck | $156,680,000 | BBB |

| 5/28/14 | OnDeck | $18,320,000 | BB |

| 10/20/14 | CAN Capital | $171,000,000 | A |

| 10/20/14 | CAN Capital | $20,000,000 | BBB |

| 2/10/16 | Earnest | $34,710,000 | A |

| 2/10/16 | Earnest | $70,240,000 | A |

| 2/10/16 | Earnest | $7,050,000 | BBB |

| 11/19/15 | SoFi | $154,903,000 | AAA |

| 11/19/15 | SoFi | $334,778,000 | AAA |

| 11/19/15 | SoFi | $46,691,000 | BBB |

| 8/4/15 | SoFi | $136,500,000 | AAA |

| 8/4/15 | SoFi | $250,800,000 | AAA |

| 8/4/15 | SoFi | $30,300,000 | BBB |

| 6/9/15 | SoFi | $146,676,000 | AA |

| 6/9/15 | SoFi | $235,445,000 | AA |

| 6/9/15 | SoFi | $29,780,000 | BBB |

| 2/3/15 | SoFi | $151,500,000 | AA |

| 2/3/15 | SoFi | $162,300,000 | AA |

| 11/10/14 | SoFi | $105,700,000 | AA |

| 11/10/14 | SoFi | $197,500,000 | AA |

| 7/15/14 | SoFi | $125,500,000 | A |

| 7/15/14 | SoFi | $125,500,000 | A |

| 12/24/13 | SoFi | $151,800,000 | A |

In the case of Earnest, the securitized loans represent borrowers with an average FICO score of 775 and an average annual income of $143,535. The average borrower is 32-years old. 81% of them have a graduate level degree.

Since Earnest launched two years ago, they’ve never had a loan go more than 60 days delinquent. That’s out of 5,580 borrowers which represents about $400 million in loans.

“100% of the pool contains refinancings of existing student loan debt,” the DBRS report says. “Loans are used to prepay a borrower’s existing eligible educational loan debt.”

While similar to SoFi’s prime customer base, DBRS explains that among Earnest’s weaknesses are their limited operational history and lack of data to gauge how their loans would perform during a recession.

Prosper Has Increased Its Estimated Loss Rates

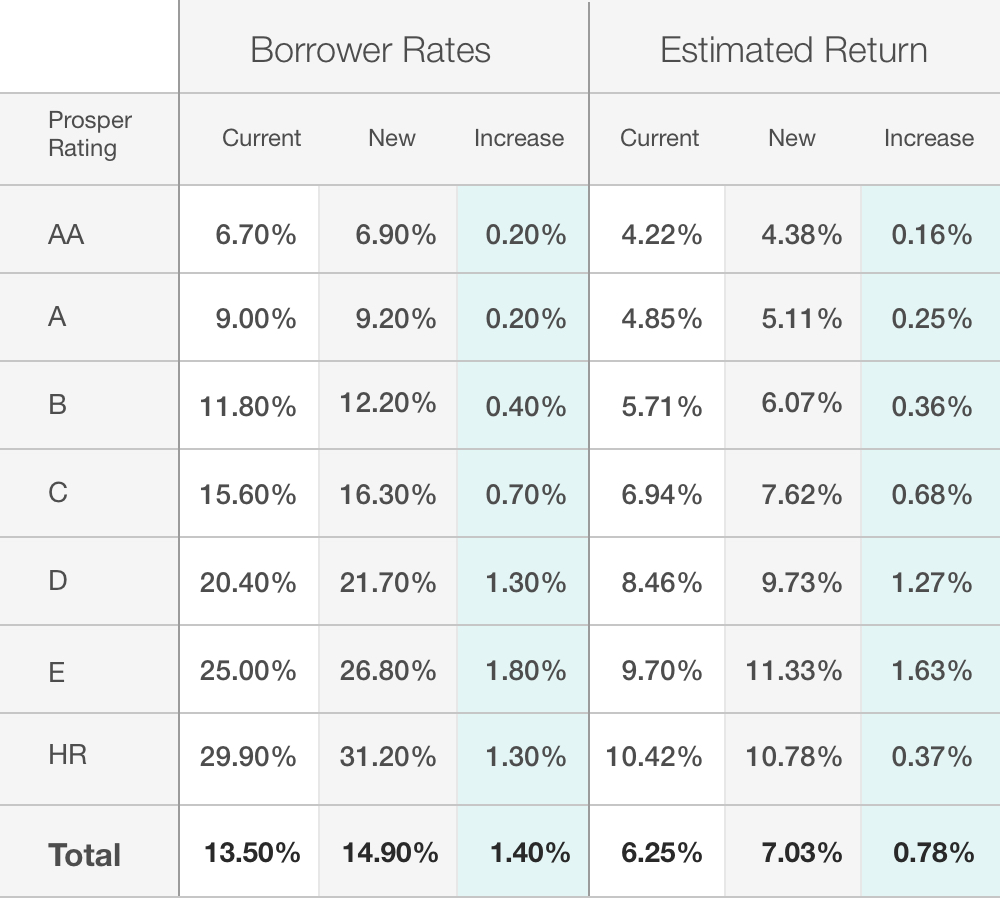

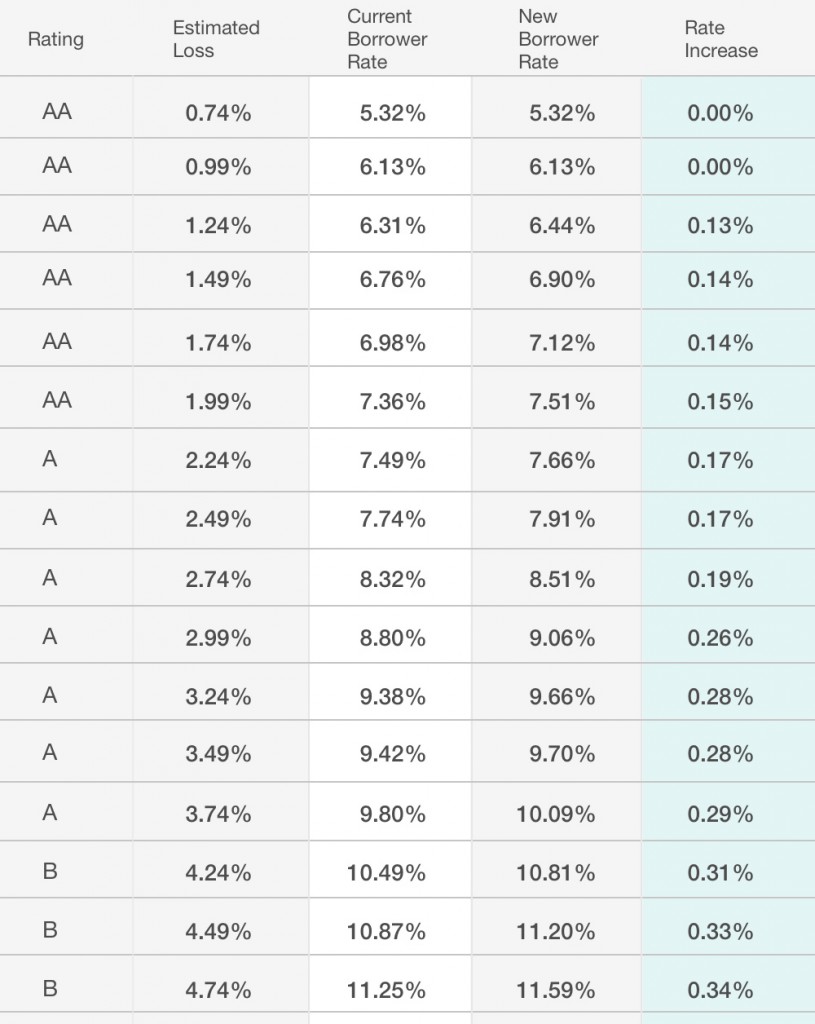

February 15, 2016“Effective today, Prosper has increased its estimated loss rates and the price charged for risk on the loans originated through the platform,” said an email to investors on Monday. “We believe this move ensures that our borrower payment dependent note and whole loan products remain competitive for our investors in the current turbulent market environment that we have witnessed since the beginning of 2016.”

Prosper is one of only two marketplace lending platforms in the US that is open to retail investors. Founded in 2005, the company has made over $5 billion in loans. They were surpassed by Lending Club in the race to dominate the market after being nearly destroyed by both the Great Recession and a class action lawsuit that claimed they sold unqualified and unregistered securities in violation of the California and federal securities laws. The suit was settled in 2013.

The going forward rate increase affects one category of high risk borrowers by as much as 199 basis points. Meanwhile, even prime borrowers will experience increases of up to 29 basis points.

These are the changes according to Prosper:

Estimated Aggregate Impact to Prosper Portfolio of Loss and Price Changes

Proposed Pricing Modifications for the Week of 2/15

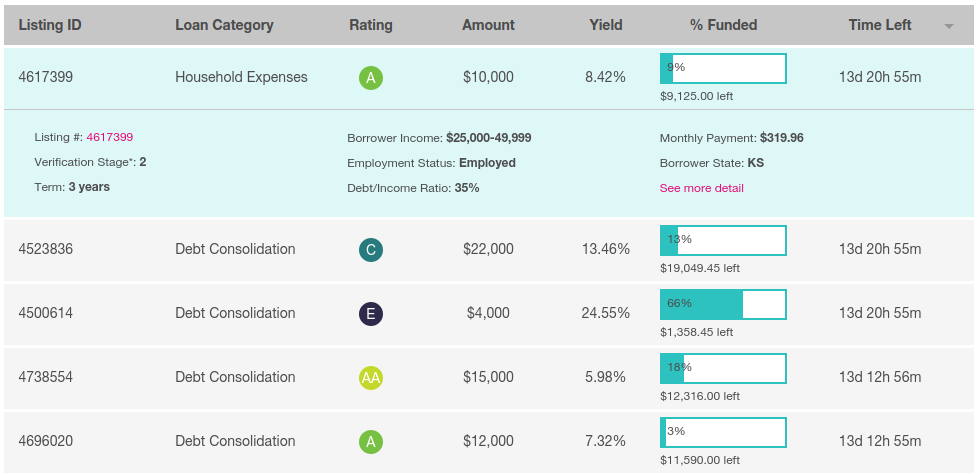

Last week, the company also refaced their entire site. As a Prosper investor, the new user interface greatly improves the user experience.