Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Merchant Cash Advance APR Debate (Sean Murray v Ami Kassar)

November 24, 2015The other day, Inc. writer and loan broker Ami Kassar took some time out of his day from taking photos of his shadow in the park to engage me in a debate about the use of APRs in future receivable purchase transactions. He was apparently very bothered by my analysis of Square’s merchant cash advance program which has transacted more than $300 million to date.

To clarify my position here, I am indeed in favor of transparency, so long as it’s intelligent transparency. Coming up with phony percentages based on estimates and applying them to transactions where they don’t make sense is not transparency. Similarly, advocating that merchant cash advance companies and lenders alike move away from a dollar-for-dollar pricing model to one that requires the seller or borrower to do math or hire an accountant is also not transparency.

Even a Federal Reserve study that attempted to prove merchant cash advances were confusing inadvertently proved that APRs in general were confusing. If someone doesn’t know how to calculate an APR, then it’s unreasonable to assume that they could work backwards from an APR to determine the dollar-for-dollar cost of capital. In effect, APR is a surefire way to mask the trust cost despite arguments to the contrary.

My unplanned debate with Ami Kassar on twitter is below:

Sorry Ami. The only thing unclear is your argument.

Beat The $3,000 Capital Loss Cap in Marketplace Lending

November 24, 2015 Because interest on platforms like Lending Club is counted as normal income and the losses as capital losses, you can only deduct a maximum loss amount of $3,000 if you don’t have capital gains from other investments. That can be an expensive mistake for an investor with a large portfolio who isn’t paying attention. For instance, if you earned $20,000 in income through Lending Club but had $10,000 in losses from defaults, you’d actually be taxed on $17,000, not on the difference between the two. In, Is the Premium Gone in Peer-to-Peer Lending?, I wrote that there’s a whole lot of risk in marketplace lending and not a whole lot of yield to compensate for it, especially when considering the poor tax treatment.

Because interest on platforms like Lending Club is counted as normal income and the losses as capital losses, you can only deduct a maximum loss amount of $3,000 if you don’t have capital gains from other investments. That can be an expensive mistake for an investor with a large portfolio who isn’t paying attention. For instance, if you earned $20,000 in income through Lending Club but had $10,000 in losses from defaults, you’d actually be taxed on $17,000, not on the difference between the two. In, Is the Premium Gone in Peer-to-Peer Lending?, I wrote that there’s a whole lot of risk in marketplace lending and not a whole lot of yield to compensate for it, especially when considering the poor tax treatment.

It’s surprisingly easy to rack up thousands of dollars in defaults in a single year even if you spread the risk around through small $25 increments. I know this because I’m teetering on the fence of it just on Lending Club alone. I had approximately $2,600 in charge-offs so far for 2015 at the end of October. Anything beyond $3,000 I can’t offset against my gains so there’s little sense in investing any more money.

Unless…

There is one way to build a significant portfolio without breaking the threshold, invest in the low risk loans. Of the 246 A-grade loans I’ve invested in, so far none of them have ever defaulted. Of the 675 B-grade loans, only 9 of them have already defaulted. Compare that to the 52 G-grade loans I’ve participated in where 11 have defaulted. It might interest you to know that the average time remaining to maturity on those G-grade loans is about 3 years. That means 21% of them have already gone bad and there’s still another 3 years left to go. While these stunningly high risk loans might return in yield for what they lack in performance, they’re a great way to build a capital loss mountain, something that could cause significant damage once you exceed $3,000.

By investing in low risk loans and staying below the capital loss cap, you can invest substantially more. Illogical as it may seem, a big lower yielding portfolio can earn more than a higher yielding one because of the tax treatment if you do not have outside investments with capital gains.

If you are a small investor looking to play with $5,000, none of this will likely be relevant to you, but if you were looking to place $100,000 or more, you might want to remember this phrase in marketplace lending, lower yield is more.

Read more about the capital loss rules and Lending Club on the LendAcademy blog.

Merchant Cash Advance is The Real Square IPO Story

November 22, 2015 Square’s debut on the New York Stock Exchange is being talked about as one of the more consequential IPOs of 2015. As a mobile payments company famous for both losing money and its founding by Jack Dorsey, Twitter’s CEO, the $2.9 billion valuation pales in comparison to its rival First Data that went public just a month before. First Data, which was founded in 1971, is worth five times more than Square with a market cap of $14.7 billion to Square’s $2.9 billion. But it’s Square that everyone’s talking about and not necessarily in a positive way. Cast as the poster child for runaway private market valuations in Fintech, Square’s Series E round just a year before had supposedly increased its worth to $6 billion.

Square’s debut on the New York Stock Exchange is being talked about as one of the more consequential IPOs of 2015. As a mobile payments company famous for both losing money and its founding by Jack Dorsey, Twitter’s CEO, the $2.9 billion valuation pales in comparison to its rival First Data that went public just a month before. First Data, which was founded in 1971, is worth five times more than Square with a market cap of $14.7 billion to Square’s $2.9 billion. But it’s Square that everyone’s talking about and not necessarily in a positive way. Cast as the poster child for runaway private market valuations in Fintech, Square’s Series E round just a year before had supposedly increased its worth to $6 billion.

Robert Greifeld, the CEO of Nasdaq, had warned people just weeks earlier about the validity of private market valuations. “A unicorn valuation in private markets could be from just two people,” he said. “Whereas public markets could be 200,000 people.”

And while Square’s IPO was relatively well-received, closing at 45% above its offered price, there’s an entire story beyond payments hidden in the company’s financial statements under the label of “software and data products.” That’s code for merchant cash advance, the working capital product they offer to customers that currently makes up 4% of the company’s revenue.

“Since Square Capital is not a loan, there is no interest rate,” states the company’s FAQ. That echoes what dozens of other merchant cash advance companies have been saying for a decade. “You sell a specific amount of your future receivables to Square, and in return you get a lump sum for the sale,” marketing materials explain.

Lenders that don’t approve of this receivable purchase model are lobbying politically against it, some of whom are well-known. Lending Club for example, is a signatory to the Responsible Business Lending Coalition’s Small Business Borrowers Bill of Rights (SBBOR), committing themselves to things like transparency and the disclosure of APRs even for non-loan products.

But disclosing an APR on a receivable purchase merchant cash advance transaction is not only impossible since there is no time variable, but would violate the spirit of the contract even if estimates were used to fill in the blanks. Nonetheless, Fundera CEO Jared Hecht, whose marketplace platform has also signed the SBBOR told Forbes in September that “small business owners have been sold by pushy salespeople, hiding terms, disguising rates and manipulating customers into taking products that aren’t good for them.”

But disclosing an APR on a receivable purchase merchant cash advance transaction is not only impossible since there is no time variable, but would violate the spirit of the contract even if estimates were used to fill in the blanks. Nonetheless, Fundera CEO Jared Hecht, whose marketplace platform has also signed the SBBOR told Forbes in September that “small business owners have been sold by pushy salespeople, hiding terms, disguising rates and manipulating customers into taking products that aren’t good for them.”

Ironically, Fundera’s own merchant cash advance partners have not made any such pledge to disclose APRs. No one’s commitment is verified anyway. “Neither Small Business Majority nor any other coalition member independently verifies that any of these signatory companies or entities in fact abide by the SBBOR,” the group’s website states. This isn’t to say that their intent is misguided, there’s just very little substance to it below the surface.

For example, while the coalition has made some subtle and not so subtle digs about merchant cash advances over fairness and transparency, it’s the lending model used by some of the SBBOR’s signatories that is being challenged by the courts right now. Because of Madden v. Midland, Lending Club’s practice of using a chartered bank to originate loans could potentially be in jeopardy. The ruling was just appealed to the U.S. Supreme Court. At the heart of the issue is the ability to usurp state usury caps through the National Bank Act. For a company that has pledged to offer non-abusive products, it’s ironic that their model relies on preemption of state interest rate caps all the while reassuring their shareholders that there’s no risk because of their Choice of Law fallback provision. In truth, Lending Club uses a state chartered bank and not a nationally chartered bank and thus would be somewhat shielded in an unfavorable Supreme Court ruling.

Those concerned in years past that receivable purchase merchant cash advances were full of regulatory uncertainty had shifted towards the model that Lending Club uses since it was perceived to have more nationally recognized legitimacy. However, with that model seriously challenged, old school merchant cash advances are once again looking pretty good. That’s probably why publicly traded Enova International Inc. (NYSE:ENVA) bought The Business Backer this past summer. And it’s why Square skated through their IPO without much resistance to their merchant cash advance activities.

The story of Square was either that it was overvalued, that CEO Jack Dorsey couldn’t handle running two companies, that they were losing money, or that their deal with Starbucks was a mistake. Meanwhile Square has processed $300 million worth of merchant cash advances, a product that doesn’t disclose an APR since it’s not a loan. “Nearly 90% of sellers who have been offered a second Square Capital advance cho[se] to accept a repeat advance,” their S-1 stated.

“If our Square Capital program shifts from an MCA model to a loan model, state and federal rules concerning lending could become applicable,” it adds. And right now partly due to Madden v. Midland, the loan model looks pretty shaky. Square proved many things when they went public on November 19th and one was that merchant cash advances are just the opposite of what critics have argued in the past.

Battery Ventures’ general partner Roger Lee told Business Insider, “the [Square Capital] product itself will have unique advantages in the market, and it’s a big market.”

Lending Club Narrowly Avoids Major Transparency Flop

November 18, 2015After many months of Lending Club warning that they would be REMOVING borrower credit data from note listings, they have completely reversed course and ADDED fifteen new credit attributes. On Peter Renton’s LendAcademy forum, one member speculated that this move was made to compete with Prosper for the attention of institutional investors. If true, that would be entirely misguided.

Almost exactly one year ago, Lending Club announced that they were cutting the amount of data points available to investors from 100 to 56. Renton, a marketplace lending evangelist and founder of the LendIt conference, gave it a negative spin in his blog:

It is pretty obvious by now that I don’t like these changes. For quite some time now Lending Club has been reducing the amount of transparency for investors. Now, some changes I completely understood such as removing the Q&A with borrowers and even the removal of loan descriptions. But removing data that investors have been using to make investment decisions is a step too far in my opinion.

I think Lending Club need to ask themselves if they are a true marketplace connecting borrowers and investors in a transparent fashion or whether they are more of a loan origination platform that makes products available to investors. They are certainly moving more towards the latter, I think, and that is a shame for everyone.

The move was seen by many as a way to stop investors from trying to reverse engineer their models and beat their grading system for above average yields. While understanding that perspective, it is mind boggling that they had planned to remove more data points and make the loans on the platform even less transparent. And here’s why…

Lending Club is a key signatory to the Small Business Borrower’s Bill of Rights, a group of political activists that claim innovative small business lending can only achieve its potential “if it is built on transparency, fairness, and putting the rights of borrowers at the center of the lending process.” With transparency being a focal point of their agenda there, one might find their attempts to reduce disclosure and eradicate transparency a bit hypocritical.

Lending Club is a key signatory to the Small Business Borrower’s Bill of Rights, a group of political activists that claim innovative small business lending can only achieve its potential “if it is built on transparency, fairness, and putting the rights of borrowers at the center of the lending process.” With transparency being a focal point of their agenda there, one might find their attempts to reduce disclosure and eradicate transparency a bit hypocritical.

Investors on Renton’s forum who had for months anticipated Lending Club to remove more data points, also viewed it negatively. “I’d have to think hard on whether to continue investing in LC notes without those credit fields — it would be very much like gambling rather than investing,” wrote Fred back on July 8th.

A similarly named user, Fred93, communicated that these data points were all investors had to go off. “We can’t shake a borrower’s hand, feel the firmness of his grip, the sweatiness of his palm. We can’t look a borrower in the eye. We live or die by a handful of numbers, which we hope mean something, on the average,” he wrote.

Clearly some investors weren’t thrilled with the proposed changes. All the while, Lending Club’s co-signatories had been promoting the transparency pledge through speeches, TV appearances, public relation events, and press releases. To be fair, The Small Business Borrowers Bill of Rights is aimed at transparency between business borrowers and sources offering business financing. Lending Club’s planned removal of data was targeted at investors in their consumer notes. It sounds different enough until you consider that 72% of Lending Club’s loans originated in 2014 were funded by investors vastly less sophisticated than the commercial businesses they have pledged to protect. That’s because that money came from consumers, many of whom are unaccredited and went through no screening process. Instead, these investors are presented with a prospectus as if they were buying a stock or bond and stuck with the risk whether they understand it all or not.

These consumers who are legally presumed to be unsophisticated are the very same people that Lending Club planned to reduce disclosures to, all the while heavily promoting to them that they roll over their retirement savings onto their platform. That logic is the very definition of insanity. Obfuscating the reasoning behind certain scoring grades to these investing consumers would be nothing short of unconscionable and would reasonably invalidate any pledge they’ve made towards transparency in other areas.

Lending Club has for now avoided a major flop by reversing course after having added 15 new pieces of data for investors.

While some investors speculated the move had to do with pressure from Lending Club’s institutional investor base. The more likely reason is increasing scrutiny from federal regulators. Less than two weeks ago for example, the FDIC warned banks about marketplace lending and advised them to perform their own underwriting on the loans they buy and not to rely on originator scoring models. A summary of their letter specifically said:

Some institutions are relying on lead or originating institutions and nonbank third parties to perform risk management functions when purchasing: loans and loan participations, including out-of territory loans; loans to industries or loan types unfamiliar to the bank; leveraged loans; unsecured loans; or loans underwritten using proprietary models.

Institutions should underwrite and administer loan and loan participation purchases as if the loans were originated by the purchasing institution. This includes understanding the loan type, the obligor’s market and industry, and the credit models relied on to make credit decisions.

Before purchasing a loan or participation or entering into a third-party arrangement to purchase or participate in loans, financial institutions should:

– ensure that loan policies address such purchases,

– understand the terms and limitations of agreements,

– perform appropriate due diligence, and

– obtain necessary board or committee approvals.

These guidelines conflict with Lending Club’s long sought after goal of getting investors to trust their A-G scoring grades. The banking regulator is advising banks to basically disregard them. “The institution should perform a sufficient level of analysis to determine whether the loans or participations purchased are consistent with the board’s risk appetite and comply with loan policy guidelines prior to committing funds, and on an ongoing basis,” the more complete memo reads. “This assessment and determination should not be contracted out to a third party.”

A law firm with specialized knowledge of the industry, criticized the FDIC’s move when they wrote on their website, “Ironically, given the Treasury Department’s recent request for information, which supported marketplace lending and focused in part on how the federal government could be supportive of the innovations in marketplace lending, we now have a federal banking agency that is creating roadblocks to having banks participate in this dynamic and rapidly growing space.”

Asking banks not to rely on marketplace scoring models alone hardly seems like a roadblock, especially when the models are tucked away in algorithmic obscurity, have hardly been around for very long, and would decide the fate of depositor money. And if this directive indeed contributed to Lending Club’s transparency reversal, then it couldn’t have been any more well-timed.

Asking banks not to rely on marketplace scoring models alone hardly seems like a roadblock, especially when the models are tucked away in algorithmic obscurity, have hardly been around for very long, and would decide the fate of depositor money. And if this directive indeed contributed to Lending Club’s transparency reversal, then it couldn’t have been any more well-timed.

Whether or not the added data points will make any difference to the performance of investment portfolios is irrelevant. If unaccredited investors and/or depositor money are the source of marketplace loan funding, then Lending Club has a responsibility to disclose as much as possible, no matter how little value they believe certain pieces of information are worth. The 15 additional points are a welcome announcement. The question going forward should be, what else can they disclose?

As a company that pledged so strongly to protect corporations from transparency issues in the developing commercial finance market, they should be trying twice as hard to protect the unsophisticated consumers that invest in the loans they approve and make available for investing. Some of these consumers are prodded into putting their retirement funds on the platform and we all know some people will irresponsibly place their entire retirement portfolio in it. The “Number of credit union trades” a borrower has might not unlock the secret to better investing performance but if it’s something Lending Club knows, the investing public deserves to know it too, if only in the name of transparency which they have so committed themselves to uphold…

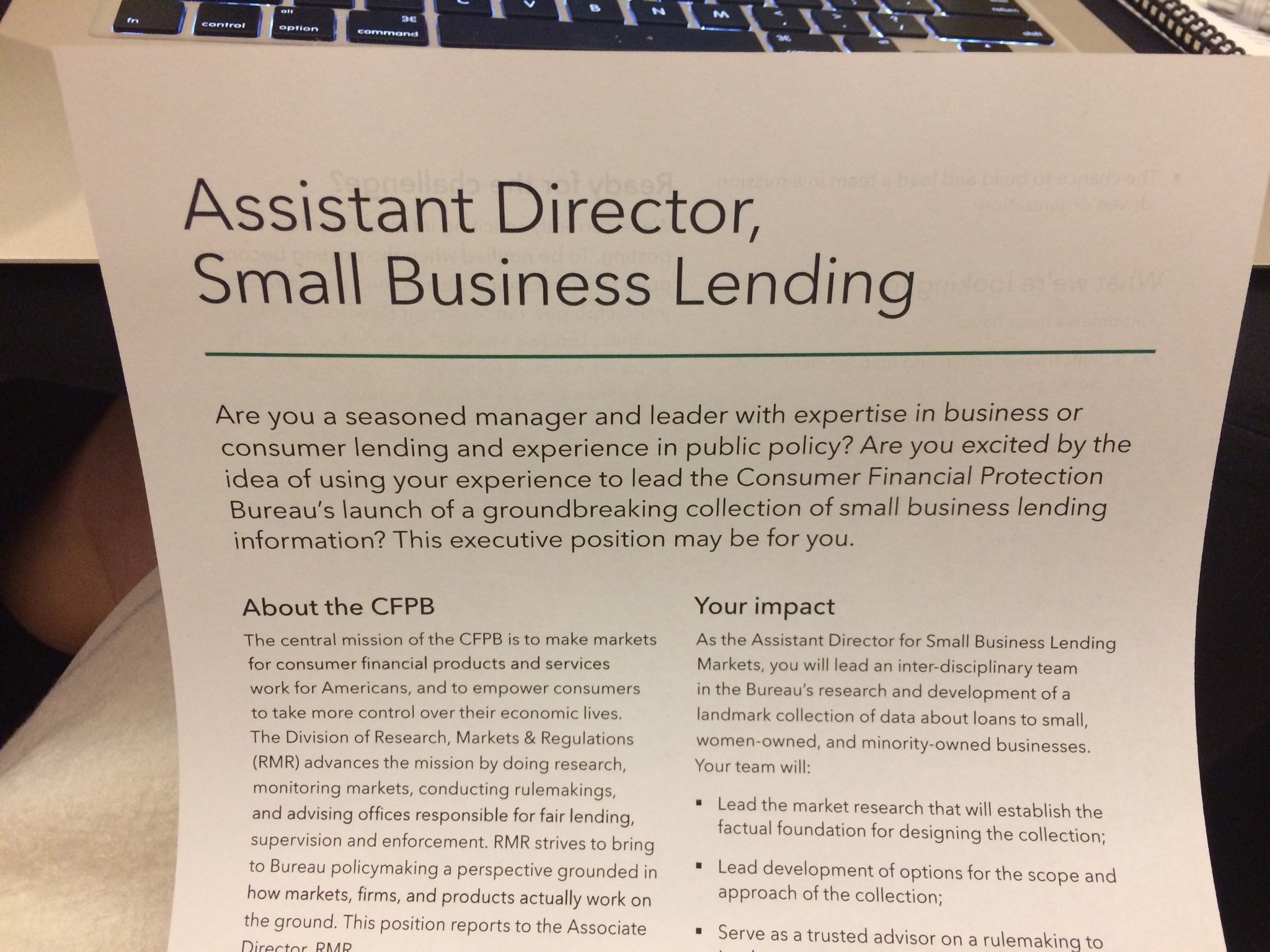

The Clock is Ticking: CFPB Blankets Small Business Banking Conference

November 17, 2015At the Small Business Banking conference in Nashville, the CFPB is making its presence known by peppering attendees with this handout:

While not surprising considering they have been advertising this position on LinkedIn, it shows a concerted effort to not only recruit, but also to subtly inform everyone that their involvement is just around the corner.

What is alarming is that the assistant director for small business lending is said to play a role in rulemaking. As you may not be aware, the CFPB has legislative power that can bypass Congress even though it’s part of the executive branch.

Would you like to play a proactive role to protect the industry, improve its reputation, and educate government policy makers? Now is the time to consider joining the Coalition for Responsible Business Finance.

Contact:

CRBF Executive Director Tom Sullivan

c/o Nelson Mullins Riley & Scarborough

101 Constitution Avenue, NW

Washington, DC 20001

(202) 905-2571

Learn more at: http://www.responsiblefinance.com/

Madden v. Midland Appealed to the US Supreme Court

November 15, 2015The Madden v. Midland decision has been appealed to the US Supreme Court and the future of non-bank lending potentially hangs in the balance. The introductory statement reads as follows:

This case presents a question which is critical to the operation of the national banking system and on which the courts of appeals are in conflict. The National Bank Act authorizes national banks to charge interest at particular rates on loans that they originate, and the Act has long been held to preempt conflicting state usury laws. The question presented here is whether, after a national bank sells or otherwise assigns a loan with a permissible interest rate to another entity, the Act continues to preempt the application of state usury laws to that loan. Put differently, the question presented concerns the extent to which a State may effectively regulate a national bank’s ability to set interest rates by imposing limitations that are triggered as soon as a loan is sold or otherwise assigned.

Several attorneys have said off the record that the likelihood the US Supreme Court would actually hear the case is about 100 to 1, because the issue lacks sex appeal. Gay Marriage, Obamacare, these are the type of things that make their way through the system.

Nevertheless, the petition argues the matter at hand:

The Second Circuit vacated the judgment, holding that the National Bank Act ceased to have preemptive effect once the national bank had assigned the loan to another entity. App., infra, 1a-18a. In so holding, the Second Circuit created a square conflict with the Eighth Circuit, and its reasoning is irreconcilable with that of the Fifth Circuit. The Second Circuit also rode roughshod over decisions of this Court that provide broad protection both for a national bank’s power to set interest rates and for its freedom from indirect regulation. And it cast aside the cardinal rule of usury, dating back centuries, that a loan which is valid when made cannot become usurious by virtue of a subsequent transaction.

The Second Circuit, of course, is home to much of the American financial-services industry. And if the Second Circuit’s decision is allowed to stand, it threatens to inflict catastrophic consequences on secondary markets that are essential to the operation of the national banking system and the availability of consumer credit. The markets have long functioned on the understanding that buyers may freely purchase loans from originators without fear that the loans will become invalid, an understanding uprooted by the Second Circuit’s decision in this case. It is no exaggeration to say that, in light of these practical consequences, this case presents one of the most significant legal issues currently facing the financial-services industry. Because the Second Circuit’s decision creates a conflict on such a vitally important question of federal law, and because there is an urgent need to resolve that conflict, the petition for a writ of certiorari should be granted.

Brian Korn, a partner at Manatt, Phelps and Phillips, told the LendAcademy blog in an interview that the Court could rule on the motion at any time and that it takes 4 out of 9 justices to agree to accept the case.

The plaintiff, Madden, has until December 10, 2015 to file a response to the petition.

Industry Message Boards Crack Down on Anonymous Deal Grabbers

November 11, 2015 Industry message boards, including deBanked’s, have begun taking a stronger stance against anonymity to facilitate transparency and protect users. While anyone can still register with their personal addresses, a corporate email address must be provided in the course of soliciting business. Industry participants have reached a general consensus that soliciting deals while hiding behind a free email address raises a red flag.

Industry message boards, including deBanked’s, have begun taking a stronger stance against anonymity to facilitate transparency and protect users. While anyone can still register with their personal addresses, a corporate email address must be provided in the course of soliciting business. Industry participants have reached a general consensus that soliciting deals while hiding behind a free email address raises a red flag.

With hundreds of legitimate vendors to choose from, there should be little need to transact with users that lack basic things such as a company name, office address and phone number.

“I’m bombarded with probably 10 emails every day of the week from a supposedly new lender that wants my business, and they’re really just a broker shop like we are,” said Cheryl Tibbs, in the September/October issue of deBanked Magazine. She warned that fake funders can steal deals and pocket the entire commission. They solicit deals in online forums, by email message or over the phone, and then they offer the deals to companies that really do function as direct funders, she said.

While no online forum was specified in the story, at least two forums have responded by cracking down on anonymity by suspending or banning violators.

While no online forum was specified in the story, at least two forums have responded by cracking down on anonymity by suspending or banning violators.

The age of the gmail funder is coming to a close. Don’t buy leads from HotLeads4u69@hotmail.com and definitely don’t syndicate with a company that has no known address.

Income Inequality Perpetuated by Low Interest Savings Accounts (GOP Debate)

November 11, 2015The losers of Tuesday night’s GOP debate were Dodd-Frank, the CFPB and the big banks. Hours after I linked to a CFPB job listing for a small business lending fairness assistant director, former Hewlett-Packard CEO Carly Fiorina told America that the CFPB is the beginning of socialism. Government creates the problem and then proposes a solution to the problem it creates, she argued.

Senator Ted Cruz added that the government is in bed with the big banks and it’s leading to the elimination of community banks. As a consequence, he said, small businesses can’t get loans. Two months ago, B. Doyle Mitchell Jr, the CEO of Industrial Bank, who spoke on behalf of the Independent Community Bankers of America made a similar argument during a House Small Business Committee hearing. He said, “I really feel like we’re getting away from helping people and making sure that we make the loans that Washington agrees with and I think that needs to change.”

In the debate, Senator Rand Paul offered his own twist on what’s wrong with the banking system and that’s the inability for poor people to get the same rate of return as rich people. Too little interest is earned by holding money in savings accounts, he argued, and “now we’re even talking about negative interest.”

Three weeks ago, CNBC reported that Narayana Kocherlakota, president of the Minneapolis Fed was in favor of the Fed pushing rates below zero. Really low interest rates can encourage people not to save or just to spend the money, Senator Paul warned, with the result being that the poor are stuck in the cycle of being poor.

According to Jana Randow on Bloomberg, who wrote about the subject of negative interest rates, “if banks make more customers pay to hold their money, retail clients may put their cash under the mattress instead.”

Not mentioned during the debate was marketplace lending where retail investors have the opportunity to earn Wall Street yields. CNBC recently reported that Lending Club and Prosper investors are earning between 5%-9% a year. While it’s true that Wall Street firms now dominate investor demand, there is still enough availability for individuals to literally share the wealth.

Not mentioned during the debate was marketplace lending where retail investors have the opportunity to earn Wall Street yields. CNBC recently reported that Lending Club and Prosper investors are earning between 5%-9% a year. While it’s true that Wall Street firms now dominate investor demand, there is still enough availability for individuals to literally share the wealth.

The story of marketplace lending might have its roots in the sharing economy, technological disruption, or making markets more efficient, but to Senator Paul’s point, it also presents America’s lower income individuals to build wealth like the rich. Putting your money in an account earning less than 1% interest will keep you poor. Putting it under the mattress will also keep you poor. And spending your money might make you look rich but that will indeed keep you poor. The big banks in effect keep the poor poor by presenting their customers with those three options.

The solution to income inequality (other than by moving to cities and states run by republicans as Paul suggested) is to offer the same opportunities to the poor as the rich have access to. Marketplace lending allows the average American worker to earn the same yield that Goldman Sachs would find attractive. Maybe one of the republican candidates will bring that up in the next debate.

Jeb Bush (if he can hang in the race) has invested on the Lending Club platform, which we learned when he disclosed his historical tax returns and could possibly speak from his own experience.