Still Reviewing Paper Bank Statements? Stop

June 26, 2015 Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Technology has made it easier to create authentic looking documents and the rise in online lending seems to be bringing out the worst in people. Somebody in a desperate situation might not have the guts to look a banker in the eye and hand him a stack of fraudulent documents but they might roll the dice with somebody over the Internet they’ll never have to meet.

The fakes aren’t obvious anymore. Anyone can go online and buy doctored documents from professionals. The business is booming on Craigslist for example where fraudulent documents can be made to order in under an hour.

In the Miami area, fraud hucksters are even beginning to offer deals such as buy 2 fake documents, get 1 free.

Industry-wide, funding companies are complaining that attempted fraud is out of control. One broker recently took to the dailyfunder forum to share her frustration. “I can spot them a mile away!!! 2 different deals submitted this week with fraudulent statements!!!,” she vented.

Other brokers chimed in, sharing their stories such as a merchant whose doctored statements were only noticed because ATM withdrawals were listed with odd amounts like $90.83.

Oddly, nobody seems to be reporting this fraud to the authorities. It all seems to get swept under the rug as business as usual. Orchard co-founder David Snitkoff for example, was asked just last month about the rate of marketplace lending fraud and he apparently said, “No worries, none to date.” He seemed to be implying that fraudulent applicants are getting screened out. But that doesn’t mean people aren’t trying.

Seven months ago, merchant cash advance underwriter Pierre Mena wrote in detail about the challenges he faces in detecting fraud. He said:

Some of the more well hidden fraud can usually be found by comparing the summary page and last page of the bank statement to other statements. Typically, most banks and some credit unions offer you a snapshot of the starting balance, which should generally match up with the ending balance of the previous month. If it doesn’t, you should look for any transactions from the previous month that did not settle until the current month. If there is none, this is usually a red flag indicating that the merchant forgot that statements are continual time series financial data whose totals carry on to the following month.

-Pierre Mena, Rapid Capital Funding

A lot of these issues can be easily overcome by simply disregarding paper statements altogether. Microbilt’s instant bank verification tool for example, will allow you to pull the most recent 90 days worth of transaction data directly from the banks themselves. Funders using these automated checks swear by their effectiveness and the capability is essential for any company that wants to scale.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

Cultural differences play a role in this according to Gil Zapata, the founder of Florida-based Lendinero. Zapata recently wrote that latino business owners over the age of 45 are not accustomed to doing business over the Internet, email, fax, or phone. “This group has a high level of distrust in doing business via the Internet,” he said.

So is there a middle ground? On the dailyfunder forum, Chad Otar, a managing partner of Excel Capital Management said that he tells merchants they can change their online banking passwords after a verification. And Andy McDonald of Yellowstone Capital wrote that verifying the bank data is beneficial for the merchants too. “It protects the merchant by allowing us to check their account to make sure our pulls aren’t going to bounce,” he wrote in a thread back in April. He also added that he comes across 2-3 applications PER DAY with altered statements.

Humans can only do so much. Pierre Mena actually wrote, “Some of these statements are doctored so well that you may have to zoom in upwards of 300% to find a comma that should actually be a period to separate dollars from cents.” At this point, an instant bank verification would probably work wonders.

Online business lender Kabbage might have the best model. On their website, applicants are instructed to enter their email address followed by their bank account username and password. Their system will analyze their bank transactions and if eligible, will then ask the applicant for their first and last name. It flies in the face of all the pushback that funders claim merchants give them over data privacy and security.

Four months ago Kabbage announced they were already up to funding $3 million per day. Obviously there is an entire segment of small business owners that are sucking up whatever concerns they had about bank verifications in order to get the capital they need.

The majority of the small business financing industry is still relying on paper statements and probably shouldn’t be. If you have to zoom in upwards of 300% to find a comma that should actually be a period and if con artists are offering discounts for bulk orders of fraudulent statements, it may be time to throw in the towel and join the rest of the world in using the Internet…

Dear Brokers, Investors Love You Too

June 25, 2015Hedge funds, private equity, and family offices have been all hot and bothered by lending marketplaces and direct funders for a while now, but there’s a new sexy stud that everybody wants to take to the dance, the brokers that originate the deals. An entire segment of the industry still calls them ISOs (Independent Sales Organizations) and in 2015, nobody can seem to shut up about them.

One minute brokers are being fingered as the source of the industry’s moral decline and the next minute they’re the lifeblood of it all.

Ever since World Business Lenders began acquiring broker shops and converting them into franchisees, the institutional investors suddenly woke up.

They’re Buying Brokers? BUT WHY?!

Over the years, dozens of funders have opened for business and then realized they don’t know how to get deals or where to get them from.

It’s not a build-it-and-they-will-come industry anymore. As much as certain people try to berate brokers, it’s widely believed that they still control up to 50% of the industry’s deal flow. Institutional investors examining portfolios have taken notice that some funders are successful only because they have a loyal group of broker shops. So if the brokers make the funder, then why not court the brokers?

And so they’re doing just that…

If you’re brokering less than a million a month though, you’re not really investment material yet. There’s thresholds. The more volume you produce, the more options at your disposal.

At this size, you’re really just a couple of dudes (or dudettes) sitting in a room with phones. There’s not enough action to get anyone excited. There may be some potential to get an investor to co-syndicate with you, but that’s it.

$1 Million/month to $4 Million/month

Congratulations, you’re not just a bunch of dudes anymore. If you’re using decent software, hopefully you can print out the necessary reports to woo investors. At this level you’re eligible for co-syndication, an advance rate to fund your own deals, or to be rolled up as a franchisee. If you’ve got a criminal record or have been banned by the SEC, then forget it though.

$4 Million+

If you’re not already funding your own deals at this point, you’re going to be encouraged to by an investor. They’ll want to set you up on a platform that they trust and participate in the funding in some way. You can get a credit facility. You’re also acquisition material. Funders and investors have little interest in acquiring a couple of dudes sitting in a room because there’s no actual assets to value. At $4 million a month and more, there may potentially be something beyond just the dudes running the company and therefore something to consider. If you can’t pass a criminal background check though, then forget it. And if you’re running scrappy like a $200k/month shop, then they’re not really going to be able to help you. It doesn’t help if you’re stack-heavy either.

But just because you do the volume, that doesn’t mean you can just show an investor an Excel spreadsheet and hope that they’ll fork over millions of dollars in return. You have to run your shop like a professional, not a dude (or dudette of course). And if you think you meet that criteria, that’s great news, because investors want to talk to you really badly.

But just because you do the volume, that doesn’t mean you can just show an investor an Excel spreadsheet and hope that they’ll fork over millions of dollars in return. You have to run your shop like a professional, not a dude (or dudette of course). And if you think you meet that criteria, that’s great news, because investors want to talk to you really badly.

Last year, every banker I sat down with told me they were looking to invest in the next OnDeck or CAN Capital. And what happened was, you had 200 bankers competing for the same handful of deals. This year, the conversations are all about brokers.

“Who wants to become a funder?”

“Who needs money to syndicate?”

“Who is serious about growing their broker shop?”

Did someone say Year of the Broker?

It damn sure is. If you’re funding more than a million a month, don’t rely on stacking, don’t have a criminal record, have actual reporting systems (not Excel), and want to be a funder or participate in more deals, then there’s a group of investors that are ready and willing to swipe right.

You might not be the next OnDeck and that’s okay. If you’ve got the flow, you can get the dough. <3 😉

Coming to the Rescue: Consolidation Can Save Merchants

June 24, 2015 In the last 18 months, funders have begun offering consolidations that combine more than one advance. First, the funders buy out the merchant’s existing advances. Then funders lower the percentage collected from a merchant’s card receipts or debited by ACH. Sometimes, consolidation can even include an infusion of cash for the merchant.

In the last 18 months, funders have begun offering consolidations that combine more than one advance. First, the funders buy out the merchant’s existing advances. Then funders lower the percentage collected from a merchant’s card receipts or debited by ACH. Sometimes, consolidation can even include an infusion of cash for the merchant.

“Consolidations are a way to help merchants avoid defaulting,” said Chad Otar, managing partner at New York-based Excel Capital. Consolidation works if the buyout price is low enough and the terms allow enough room to handle the obligation.

“It can free up some cash and give the merchant some room to breathe, sustain the business and avoid taking on more debt,” he noted.

It’s helpful to think of consolidation as the equivalent of refinancing a house, according to Stephen Halasnik, managing partner at Payroll Financing Solutions, a Ridgewood N.J.-based direct lender. Payroll has been offering the service for about six months, he said.

Brokers and funders can benefit from consolidation because it puts a merchant back on track towards long-term sustainability, said a broker who requested anonymity. Moreover, the broker said that one in three of the potential deals he sees have multiple advances outstanding, which means companies could lose an alarming chunk of market share by declining too many potential funding candidates. “That’s what I believe the catalyst was to opening the doors to consolidation,” he contended.

SECRET TO SUCCESS

Success in consolidation lies in finding merchants worthy of another chance, said Otar. Clients who have taken two or three advances but stick to the new plan and stop stacking advances from other brokers have a reasonably good chance of succeeding, he said. His company can work with a merchant that has as many as three advances outstanding if they have sufficient revenue.

Otar provided the example of a merchant who’s diverting 20% of his gross revenue to three advances. Together, the advances have led to a total of $50,000 in future revenues sold. If the merchant generates enough monthly revenue to qualify for $100,000, Excel can buy out the three advances, provide the merchant with $50,000 in cash, and lower the payment to 8% to 12% of gross revenue. “All of a sudden they have all this cash flow to play with that really wasn’t there,” he said of merchants in that situation. “They tend to do really well.”

Halasnik of Payroll Financing Solutions offered the example of a trucking company that had taken three advances and was delivering a total of $1,138 a day on average to the funders. Payroll bought out the three funders and is charging the trucker $615 a day.

One of Payroll’s clients needed to repair a commercial vehicle but already had too many advances and couldn’t get another, Halasnik said. Payroll consolidated the positions and lowered the payment, enabling the merchant to save enough money in two weeks to have the vehicle fixed.

To qualify for a consolidation, the merchant has to meet the “50% Rule” by netting 50% of what Excel is offering, Otar said. Between 40% and 50% of the distressed merchants that the company considers for consolidation meet that criterion, he said. An additional 30% of the merchants can meet that standard in the near future, once they’re further along on their agreements.

Under the 50% Rule, a merchant that is still obliged to deliver $70,000 and qualifies for $100,000 would not be a candidate for consolidation, Otar said. In that situation, a merchant can wait until he has delivered more of the sold revenues to the funders and then get a consolidation, he said. “In the meantime, don’t take on any more debt,” Otar tells the merchants. That too could impact their ability to sell additional revenue streams in return for cash upfront down the road.

Some merchants combine debt and advances, seeking advances only after maxing out their credit lines, said Otar. More commonly, however, it’s a matter of stacking advances, he said. “When we see there are three, four, five, six, seven cash advances out, that’s a merchant we tend to stay away from,” he noted.

Some merchants combine debt and advances, seeking advances only after maxing out their credit lines, said Otar. More commonly, however, it’s a matter of stacking advances, he said. “When we see there are three, four, five, six, seven cash advances out, that’s a merchant we tend to stay away from,” he noted.

Brokers should also bear in mind that every deal’s different, cautioned Steven Kamhi, who handles business development and ISO relationships at Nulook Capital, a Massapequa, N.Y.-based direct funder. “It has to be the right deal,” he advises.

Brokers can identify distressed merchants within the first two minutes of a phone conversation when they say things like, “I need the money right now,” Otar said. Looking at the paperwork, the broker can see within 10 minutes whether the potential client is hard-pressed.

Asking the right questions helps reveal distress quickly, sources said. That can include asking how many advances the merchant has outstanding, how much in future sales they still have to deliver and how much revenue they’re grossing monthly. Asking what company advanced them cash can reveal a lot if they’re working with less-reputable companies.

Listening’s under-rated, too. Merchants sometimes explain that they’re coming up with more ways of making money and are, therefore, making themselves a better bet for sustainability, Otar said.

OTHER WAYS OF HELPING

Brokers can make deals more palatable to some distressed merchants by deducting payments weekly instead of daily, Otar said. “It’s something I’m seeing a big migration toward,” he noted. “It’s a big selling point.” Manufacturers and contractors don’t have customers swiping cards every day and especially appreciate the change. More widely spaced payments can also fit better with some clients’ seasonal cash flow.

Besides consolidation, brokers can help distressed merchants by providing traditional accounts-receivable financing, which can prove particularly helpful for manufacturers and construction companies, Otar said.

Suppose Customer A owes a contractor $100, Otar said by way of example. The contractor can get $90 from the factor, and the factor collects the $100 from Customer A. The client pays the cost of the financing upfront but reduces the waiting time to receive the cash and avoids daily or monthly payments.

Accounts-receivable financing costs merchants much less than a cash advance, Otar noted. But putting the deal together takes longer than approving an advance, and merchants in immediate need of cash might not be able to wait.

In another example of helping merchants, Payroll had a client who was a bicycle shop owner with good credit and equity in a home, so it granted him an advance that gave him time to go to a bank and get a home equity loan. “I counseled him to do that and then buy us out,” Halasnik said.

PREVENTING DISTRESS

On the sales side of the business, brokers can help distressed merchants by preventing stacking from occurring in the first place, sources said. Otar recommended, “listening to the customer, understanding the business and offering a product that is going to benefit the customer in the long run.” That way, the broker positions himself to work with the client for years, not two or three months. “At the end of the day, they appreciate that,” he said.

Halasnik relies on his experience as a small-business owner who has operated a printing company, staffing company and nurse registry to help him understand aspects of a client’s business that people from a purely financial background might not fathom.

Brokers seeking long-term relationships should know a client’s business well enough to advise against taking on more financial obligations when the time isn’t right, agreed Payroll’s Halasnik. However, after the broker urges caution, the decision rests with the business owner, he maintained. “We are on the same page as the client,” Halasnik said. “We are looking out for their best interest because, ultimately, we have to get paid back.”

THE CASE AGAINST CONSOLIDATION

Some members of the industry prefer to avoid the consolidation trend. “The guy’s already shown that he’s going to go and take three or four advances,” said Isaac Stern, CEO of New York-based Yellowstone Capital. “Doesn’t history just show he’s going to do the same thing over again?”

Some members of the industry prefer to avoid the consolidation trend. “The guy’s already shown that he’s going to go and take three or four advances,” said Isaac Stern, CEO of New York-based Yellowstone Capital. “Doesn’t history just show he’s going to do the same thing over again?”

When a merchant’s overextended, he should wait before taking another advance, Stern said. But when some merchants are denied another advance, they immediately seek out another funder, he maintained.

Yellowstone has put together a few consolidations but chooses not to create too many, Stern said. Some merchants find themselves a month or two away from going out of business unless they can find a source of cash, he observed. “They’ve been declined for that last credit card, and things are getting really rough,” he said.

Some members of the industry advocate coming together to improve standards and provide training. Wall Street’s testing and licensing could serve as an example, suggested one source. Background checks could also help root out unethical players, he noted.

But creating a training and certification infrastructure would prove a formidable task, according to Stern. The industry would have a hard time agreeing upon who should head a trade association to administer the standards, he said. He views the industry as a collection of Type A personalities – sometimes defined as ambitious, over-achieving workaholics – who would resist consensus. “It’s a nice idea, but I don’t see it working,” he said.

REASON TO BELIEVE

Though industry players are contending with some distressed merchants, Stern noted that the average credit score of his company’s clients is beginning to rise as the economy improves.

Though statistics on distressed merchants aren’t readily available, other industry veterans feel they’re not encountering as many now as a year ago. However, they said they may see fewer cases of distress because bigger players are beginning to offer consolidations.

“A year ago, nobody would consider doing it,” a broker said of consolidation. But as funders become more open to the product when they see competitors using it to gain market share. “It’s becoming more mainstream,” he said.

How brokers market their services can also determine how many distressed merchants they encounter, sources said. Using the same prospect lists that competitors use can lead to calling on overextended clients, they maintained.

Whatever the number of distressed merchants may be, stacking sometimes makes sense, said Halasnik. What if a client needs $30,000 to win a contract, and a funder is willing to provide only $15,000, he asked rhetorically. Perhaps another funder will put in $15,000, too.

Problems arise, however, if the two funders don’t know the merchant has made two deals because they happened the same day. It’s the kind of situation that sours some members of the alternative-funding community to consolidation. As Halasnik put it: “You’re dealing with somebody who’s in trouble. It’s the highest risk a lender could take.”

Merchant Cash Advance: Do You Know What You’re Selling?

June 22, 2015 Continuing on with the Year of The Broker discussion, I want to now shift focus to the continued wave of new broker entrants that are not receiving sufficient training. I don’t believe that it’s so much the fault of the brokers, as it’s the fault of the companies they are reselling for. Those companies usually fail to provide a structured training regime. Training provided to new broker entrants is typically centered around the memorization of sales scripts, the practice of outdated rebuttals, and the repetition of lines that can end up sounding very canned and robotic.

Continuing on with the Year of The Broker discussion, I want to now shift focus to the continued wave of new broker entrants that are not receiving sufficient training. I don’t believe that it’s so much the fault of the brokers, as it’s the fault of the companies they are reselling for. Those companies usually fail to provide a structured training regime. Training provided to new broker entrants is typically centered around the memorization of sales scripts, the practice of outdated rebuttals, and the repetition of lines that can end up sounding very canned and robotic.

If I had to recommend new age sales training, I’d have to go with my favorite, which is Diagnostic Selling, promoted by the likes of Jeff Thull from Prime Resource Group (www.primeresource.com). Thull explains that as the sales consultant, you should be a valued source of business advantage for your client, rather than just a person that goes through a series of sales material regurgitation. You should have access to products, services, platforms, big data, knowledge, key players, new solutions, forecasts, trends, etc., that the merchant does not have access to, which allows them to see you as a “valued extension” of their organization. This leads to not just new client acquisition, but the real key to making money in our space, and that’s client longevity.

In order to truly achieve this level of sales consultancy, it’s important that you truly understand the products being sold because, firstly, you want to be able to distinguish between the products you are selling so that you can provide a valued consultation. You might find yourself selling one product when you should be referring another. Secondly, understanding these products is important from a regulatory standpoint as the legal connotations of the products must be disclosed properly or mistakes in disclosure, marketing, or funding agreements could become costly.

If you are an independent broker in the alternative commercial lending space, you are usually going to be selling one or multiple of the following products:

- The Merchant Cash Advance

- The Alternative Business Loan

- Equipment Leasing

- Accounts Receivable Factoring

- Accounts Receivable Financing

- Purchase Order Financing

To begin, let’s discuss the Merchant Cash Advance…

Product Value Points

Don’t Let The Critics Win

Critics of the product focus mainly on its high cost and it can be very expensive, but when used properly the product is a great leveraging tool.

Critics fail to shed light on the value of the product in terms of the merchant’s usage. Going back to that Growth Investment example, if the product had not been available, then what were the other sources available for the merchant to take advantage of the growth opportunity? In actuality, there were no other credible sources. Had the Merchant Cash Advance not been available, that investment would not have been made, and a ton of national, state and local economic activity would not have taken place, such as:

- The Equipment Manufacturer’s sale of the equipment

- The Merchant’s generation of $300,000 in revenue based on having the equipment

- The Purchaser’s revenue from borrowing costs incurred from the client using the advance

- My individual commission

- Then all of the federal, state and local taxes that would have been paid as a result

All of that economic activity vanishes if said transaction does not take place. Despite the high cost of the product, the fact is that this transaction would have been a win across the board for all parties involved including the Manufacturer, the Client, the Purchaser, Myself, as well as the Federal/State/Local Government. The true value of business capital, no matter if it’s conventional or alternative, is that the capital should produce enough new revenues so that it truly pays for itself.

Wall Street Has a New Landlord

June 20, 2015 “You stole my deal bro!”

“You stole my deal bro!”

“No I didn’t. The merchant hated your offer,” replies back a 25-year old dressed in a dark pinstripe suit with no tie.

He then takes a pull from his half-smoked cigarette and continues, “The guy wanted 90k and you offered him twenty. I was at least able to get him fifty. What’d you think was going to happen?”

I walk past the two who eye me suspiciously and am quickly out of hearing range of their conversation. They were strangers, but I know exactly what they were talking about. Walking around the neighborhood here, I feel oddly at home.

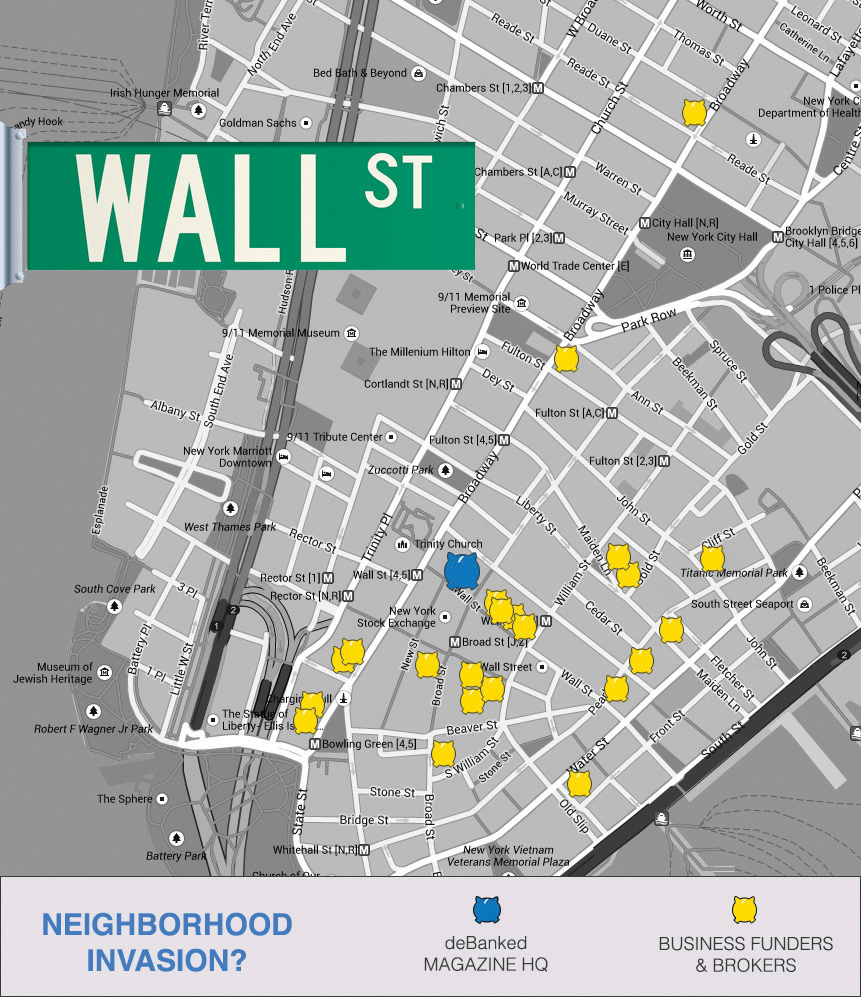

This is Wall Street, a new stronghold for the small business financing industry. Midtown has traditionally been the epicenter for merchant cash advance companies, but somewhere along the way, new players started opening up their shops in lower Manhattan.

As a born and bred New Yorker, I never really saw a need to visit the actual street of Wall Street. To my knowledge, it was simply emblematic of high finance, not really a physical place anymore.

But earlier this year when I signed a lease at 14 Wall Street, I would be thrust into the middle of America’s biggest breeding ground for financial brokers and learn once and for all that the ebb and flow of Wall Street isn’t exactly gone, just transformed.

From my office up on the 20th floor, I can see into the windows of the top five stories of the New York Stock Exchange building. The floors appear to be set up for traders, with long white continuous desks peppered with large monitors on both sides. Everyone sits and stares intensely at their screens, pressing buttons on their keyboard at rapid fire pace. Nobody runs around screaming orders anymore.

Outside, tour guides tell excited onlookers about the stock exchange’s past. It’s a historical landmark, a place to learn about history, not necessarily witness it. The spirit is still alive though in a zombified made-for-the-cameras kind of way. OnDeck recently kicked off their IPO there and so too did Lending Club.

Outside, tour guides tell excited onlookers about the stock exchange’s past. It’s a historical landmark, a place to learn about history, not necessarily witness it. The spirit is still alive though in a zombified made-for-the-cameras kind of way. OnDeck recently kicked off their IPO there and so too did Lending Club.

While tourists dance around aimlessly and upload photos to facebook to show they were there, men and women in the office floors above them are engaged in a different kind of dance. Packed in elbow to elbow with phones glued to their ears, commercial financing brokers shout large numbers at an accelerated pace.

Often lacking luxury amenities such as windows, brokers on Wall Street are weathering the heat and lack of oxygen to move money to Main Streets all across America.

When they come out for air to breathe, the tourists move out of their way, as if they’ve suddenly become aware that people are actually trying to get some work done down here.

The little strip of Broad Street between Wall Street and Exchange Place is kind of like a schoolyard for the merchant cash advance industry. War stories are exchanged, cigarettes shared and dreams dreamed. One day, I’m going to start my own ISO and I’ll do it differently because…

You can walk in any direction. The industry can be found on Broad Street, William Street, Pine Street, and Broadway. It’s on Water Street, Rector Street, Maiden Lane, and Fulton Street. It extends outward almost infinitely to Midtown, Brooklyn, Queens, Long Island, Staten Island, The Bronx, Westchester, Orange County, and New Jersey.

You can walk in any direction. The industry can be found on Broad Street, William Street, Pine Street, and Broadway. It’s on Water Street, Rector Street, Maiden Lane, and Fulton Street. It extends outward almost infinitely to Midtown, Brooklyn, Queens, Long Island, Staten Island, The Bronx, Westchester, Orange County, and New Jersey.

And while there are hubs in the outer parts, the most unique experience by far is down here on Wall Street, where you’re infinitely more likely to overhear professionals shouting “ACHs” and “stacks” than “puts” and “calls.”

Although the guides teach tourists that Wall Street as they imagined it to be is dead, Wall Street itself can never die.

Every now and then a pedestrian will look up at the offices above and wonder if the magic of fast-talking finance still exists. Is that world gone forever?

Not quite…

The stockbrokers may be gone, but there’s a new landlord. Wall Street belongs to the small business financing industry now.

The Challenges in Offering Financing to Latino Businesses

June 20, 2015 The number of minority-owned businesses jumped nearly 46% from 2002 to 2007, according to the Minority Business Development Agency. The growth rate is three times as much as for U.S. businesses as a whole. These businesses increased 55% in revenues over that five-year period. There are a number of minority groups within this category. Latino businesses are leading the way. Latinos are the fastest growing ethnic group in the United States today. Like it or not these numbers are likely to increase due to economic blocs. The U.S. has created a number of free trade agreements with Mexico, Central America and South America. Latinos are our next door neighbors.

The number of minority-owned businesses jumped nearly 46% from 2002 to 2007, according to the Minority Business Development Agency. The growth rate is three times as much as for U.S. businesses as a whole. These businesses increased 55% in revenues over that five-year period. There are a number of minority groups within this category. Latino businesses are leading the way. Latinos are the fastest growing ethnic group in the United States today. Like it or not these numbers are likely to increase due to economic blocs. The U.S. has created a number of free trade agreements with Mexico, Central America and South America. Latinos are our next door neighbors.

The SBA is the largest guarantor in the U.S. and does not offer any specific minority business loan program to Latinos. The U.S. Hispanic Chamber of Commerce offers advice to Latino business owners, but does not offer any loans. Traditional banks continue to maintain stringent guidelines for all businesses. Alternative finance companies and online lenders have a long way to go to tap into this

niche market.

Alternative lenders, online lenders and peer-to-peer lenders can cater to this niche market, but it requires a lot of resources and knowledge. We can categorize Latino businesses into one broad category. However, as a Hispanic entrepreneur, my experience has been that the Latino business community is complex in nature.

Latino Businesses by Age Groups

There are two types of Latino entrepreneurs. The older generation tends to be within the age range of 45 to 70 years old. These business owners are not accustomed to doing business over the Internet, email, fax, or phone. Online lenders may have difficulties in retrieving information from these clients. This group has a high level of distrust in doing business via the Internet. The majority of our clients within this age group are accustomed to doing business face to face. This sales and marketing strategy can be very expensive for lenders, unless you have a team of field agents. The younger generation of this group is made up of Latino entrepreneurs in the age range of 25 to 45. This group is more accustomed to using online banking and online systems. Forbes recently reported that, “With a median age of 28 years old, the timing is ripe for organizations/brands to make a firm commitment to the Hispanic consumer.”

Family Decisions and Delayed Gratification

Despite the age category, many Latino businesses are family-based. Based on my experience, the decision making process is made among family members. You could offer a $50,000 loan at a cost of factor of 1.30 to the husband and he may need to consult with his wife and his children before he signs his John Hancock. This makes the decision-making

process challenging.

Manuel Cosme Jr., the chair of the National Federation of Independent Businesses (NFIB) Leadership Council in California and co-founder of Professional Small Business Services in Vacaville, California has said, “Family plays a big role in Hispanic culture, so naturally it plays a big role in Hispanic-run businesses.”

Trust Factors

Even if you have a Latino staff or bilingual staff, Latino business owners need to trust you in order to gain their business. You will need to build good rapport with these businesses to get them to fill out a loan application and send it via fax, email or online. Latinos are accustomed to traditional banking methods and brick and mortar businesses.

“When we looked at online US Hispanics in 2006, there were four main roadblocks to US Hispanic e-Commerce adoption: 48% of online Hispanics did not want to give out personal financial information; 46% wanted to be able to see things before buying; 26% had heard about bad experiences purchasing online; and 23% did not have access to a credit or debit card,” says Roxana Strohmenger, Director in charge of Data Insights Innovation at Forrester. These are some of the challenges that we face by conducting our business in a digital manner.

According to mediapost.com, only 32% of online Hispanics use the Internet for their banking needs. In order for online lenders to succeed with this marketplace, U.S. banks need to do more to market to Hispanics online. Alternative lenders need to understand that there are barriers to entry in this marketplace.

Social Media

The Pew Research Center conducted a study that clearly indicates the usage of social media by Hispanics. Accordingly, 80 percent of Hispanic adults in the U.S. use social media and the same study revealed that Latino Internet users admitted to using Facebook as the leading social platform. A lot of business owners love to show the storefront, their family working in their businesses, and other images. You should consider Facebook as part of your overall marketing strategy to tap into this marketplace.

Going overseas

Going overseas

Another option to consider is going overseas. CAN Capital set up an operation in Costa Rica mostly for their business processing services. In fact, we at Lendinero decided to do something different that no one else is doing. We set up the majority of our operations in Central America, consisting of outbound agents, digital marketers, programmers and loan analysts. There are great benefits to having a full bilingual staff overseas and the cost of personnel is less expensive. At the same time, there are huge challenges. Since I am of Hispanic descent, it was easier to set up our operation in a Latin American country. However, there are cultural differences and you have to take into account the economic and political conditions of each country. Setting up a corporation can take 1 to 3 months and it is more expensive than the U.S.

The labor pool is huge, but finding the right people can be a challenge. In addition, training agents, processors, and support staff can be time consuming and you may run for a few months before you begin to see a profit. If your staff did not live in the U.S., you need to train them on U.S. culture, the economy, and other topics.

Furthermore, Internet speed and Internet services can be a challenge. Be prepared to pay a high cost for Internet. And labor laws are not like the U.S. If you fire an employee, you will be forced to pay unpaid vacation and a severance. In addition, you have to take other costs into consideration such as travel costs, lodging, auto leasing, and more.

Lastly, if you don’t know people in the country you plan on setting up in, an outsourced business processing service will charge you more money for rent and other services knowing that you are coming from the U.S. It is highly recommended you pair up with a native or someone who has done business in the countries you consider.

In summary, the Latino business community continues to lack financing. This niche market needs to be educated on the revolutionary paradigm shifts in business lending and online lending. If you can obtain these clients, they are clients for life. Once you obtain them as a client, they are loyal. They will not leave you.

The Official Business Financing Leaderboard

June 20, 2015A handful of funders that were large enough to make this list preferred to keep their numbers private and thus were omitted.

| Funder | 2014 |

| SBA-guaranteed 7(a) loans < $150,000 | $1,860,000,000 |

| OnDeck* | $1,200,000,000 |

| CAN Capital | $1,000,000,000 |

| AMEX Merchant Financing | $1,000,000,000 |

| Funding Circle (including UK) | $600,000,000 |

| Kabbage | $400,000,000 |

| Yellowstone Capital | $290,000,000 |

| Strategic Funding Source | $280,000,000 |

| Merchant Cash and Capital | $277,000,000 |

| Square Capital | $100,000,000 |

| IOU Central | $100,000,000 |

*According to a recent Earnings Report, OnDeck had already funded $416 million in Q1 of 2015

| Funder | Lifetime |

| CAN Capital | $5,000,000,000 |

| OnDeck | $2,000,000,000 |

| Yellowstone Capital | $1,100,000,000 |

| Funding Circle (including UK) | $1,000,000,000 |

| Merchant Cash and Capital | $1,000,000,000 |

| Business Financial Services | $1,000,000,000 |

| RapidAdvance | $700,000,000 |

| Kabbage | $500,000,000 |

| PayPal Working Capital* | $500,000,000 |

| The Business Backer | $300,000,000 |

| Fora Financial | $300,000,000 |

| Capital For Merchants | $220,000,000 |

| IOU Central | $163,000,000 |

| Credibly | $140,000,000 |

| Expansion Capital Group | $50,000,000 |

*Many reputable sources had published PayPal’s Working Capital lifetime loan figures to be approximately $200 million in early 2015, but just a couple months later PayPal blogged that the number was more than twice that amount at $500 million since inception. The print version of deBanked’s May/June magazine issue stated the smaller amount since it had already gone to print before PayPal’s announcement was made.

Legal Brief: Madden v. Midland Funding

June 11, 2015Madden v. Midland Funding, 2015 U.S. App. LEXIS 8483 (2nd Cir. May 22, 2015).

This is an interesting case for the alternative lending industry that deals with the interplay between the National Banking Act and New York State’s usury laws.

This is an interesting case for the alternative lending industry that deals with the interplay between the National Banking Act and New York State’s usury laws.

The plaintiff borrower opened a credit card account with a national bank, Bank of America (“BoA”). BoA sold the account to another national bank, FIA. FIA subsequently sent a change of terms notice stating that, going forward, the plaintiff’s account agreement would be governed by the law of Delaware, FIA’s home state. FIA later charged off the account and sold it to a third-party debt purchasing company, Midland. FIA did not retain any interest in the account after selling it to Midland and Midland was not a national bank.

Midland attempted to collect on the account and sent the plaintiff a demand letter indicating that there was a 27% interest rate on the account. Plaintiff sued Midland, alleging violations of the Fair Debt Collection Practices Act and New York’s criminal usury laws. New York law limits effective interest rates to 25 percent per year. The parties agreed that FIA had assigned plaintiff’s account to Midland and that the plaintiff had received FIA’s change in terms notice. Based on the agreement, the trial court held that the plaintiff’s state law usury claims were invalid because they were preempted by the National Bank Act.

The National Bank Act supersedes all state usury laws and allows national banks to charge interest at the rate allowed by the law of the bank’s home state. Midland argued that, as FIA’s assignee, it was permitted to charge the plaintiff interest at a rate permitted under Delaware law. FIA was incorporated in Delaware and Delaware permits interest rates that would be usurious under New York law.

On appeal, The Second Circuit Court of Appeals noted that some non-national banks, such as subsidiaries and agents of national banks, might enjoy the same usury-protection benefit as a national bank. However, third-party debt buyers, such as Midland, are not subsidiaries or agents of national banks. Midland was not acting for BoA or FIA when it attempted to collect from the plaintiff. Midland was acting for itself as the sole owner of the debt. For this reason, the Second Circuit held that Midland could not rely upon National Bank Act preemption of New York State’s usury laws.