Strategic Funding Source Acquires Tyrian Bull

January 11, 2016Tyrian Bull CEO Joshua Jones announced earlier today that their company had been acquired by Strategic Funding Source. Both based out of NYC, Tyrian posted across social media that their “clients and partners will be able to take advantage of more financing options, while still benefiting from the same standards of transparency and integrity they have come to expect with Tyrian Bull.”

Tyrian Bull’s website already displays a “POWERED BY STRATEGIC FUNDING” label in the footer.

Merchant Cash Advance Predictions for 2016

January 10, 2016 I hate new year’s resolutions, as most of the time the people making them on January 1st have already broken them by the time January 10th comes around. The reason they’re broken quick and easy is because they aren’t goals, but rather wishful thinking. A goal is something that should fit within the S.M.A.R.T criteria, which is a goal that fits five general metrics:

I hate new year’s resolutions, as most of the time the people making them on January 1st have already broken them by the time January 10th comes around. The reason they’re broken quick and easy is because they aren’t goals, but rather wishful thinking. A goal is something that should fit within the S.M.A.R.T criteria, which is a goal that fits five general metrics:

- It must be specific

- It must be measurable

- It must be attainable

- It must be realistic

- It must be time-bound, or have some sort of deadline established

In other words, you don’t just randomly set goals, a goal has to first be done based upon critical thought, research, opportunity analysis and an examination of realistic outcomes, from there you set your objectives along with the step-by-step procedures to achieve them. Once this is done, you slap a deadline on each step-by-step procedure and continue to track your progression along the way.

I don’t set new year’s resolutions, I set new year goals and objectives. My goals and objectives for 2016 (in relation to our industry), will be based upon my predictions for the following 12 months. What do I see in my crystal ball for the year of 2016? This article will pinpoint my forecasts for our landscape this year. Some of you might agree and some of you might disagree, but nevertheless, these predictions ought to create a lot of quality discussion and debate.

“THE BIGGEST” WILL CONTINUE TO BE “THE BADDEST”

I’ve talked about the future of our industry before, with the belief that Strategic Networks will be the key going forward in terms of market dominance. These networks include the Center of Influence Network, the Mom and Pop Network and the Online Network. The Center of Influence Network includes other professionals such as banks, credit unions, merchant processors, etc., who have direct access to the prospective clients. The Mom and Pop Network is just a collection of random brokers from across the country that resell on a 100% commission basis. The Online Network is that of technology automation, especially the internet and how it will shape the market going forward in terms of communications, new lead generation, and more.

Well, the biggest funders on deBanked’s Official Business Financing Leaderboard will continue to dominate the industry in 2016, taking more market share and growing the market in general, based on their efficient utilization of Strategic Networks.

PRICING PRESSURE WILL INCREASE AND COMMISSIONS WILL DECREASE, ACROSS THE BOARD

For higher paper grade deals, I believe that the pressure on pricing for A+ Paper, A Paper and B Paper clients will continue to increase, which will cause many funders and lenders to just stop competing for them (due to no longer being able to compete), while others will find innovative ways to reduce their operational costs so they can reduce down their buy rates, passing the lower costs onto these clients to compete against alternatives from the traditional lending system or P2P lenders. This entire process might also cause the commissions for these higher paper grade deals to decrease as well.

C Paper, D Paper and E Paper commissions will go down as well, as most of the new funders and lenders will target these paper grades due to not being able to compete in the high paper grade markets. Due to the increased amount of players, this will put pressure on pricing which will have brokers slicing their commissions even for the lower credit graded merchants.

TO HELP COMBAT PRICING PRESSURES, MORE PRIVATE FUNDERS WILL WELCOME SYNDICATES

More private funders and lenders will offer syndication programs for their brokers, and do so in a much more efficient, streamlined and transparent way than most of the other syndication partners are doing currently. This will help reduce the risk for a lot of these private funders and lenders, which would assist in bringing down their pricing across the board, helping them stay competitive in a marketplace where new competitors will cause merchants to put more pressure on pricing.

MORE FUNDERS WILL RESTRICT BROKER ACCESS

You will see more funders and lenders start to restrict their working relationship with new brokers. Basically, instead of just signing up anybody with a pulse, I believe more funders and lenders will actually vet new brokers they are considering partnering with. This will come as a result of the funders getting fed up of dealing with unscrupulous acts, fraud and other actions from these new and/or rogue brokers, which does nothing but hurt their brand and online reputation.

FUNDERS AND LENDERS WILL FIGHT BACK AGAINST STACKING

More funders and lenders will fight back against stacking by doing as I suggested before, which is to add a page to their Funding Agreement that says if the merchant stacks, then the merchant is liable for additional fee such as $5,000 or $10,000 per stack. This is similar to how on the merchant services side, early termination fees (ETFs) are used so merchants stop switching their merchant accounts over every month to try and save “$5.” In addition, I believe more funders and lenders will just stop filing UCCs altogether unless they are filed only on merchants that breach their contracts. This means that those new funders who specialize in “stacking”, might have to come up with a new model, as these updated practices will make it so that they will have a difficult time finding new “clients” to market to.

THE MAJORITY OF NEW ENTRANTS WILL BE SLAUGHTERED

You will continue to see new brokers, funders and lenders enter the market, with many of the funders/lenders being nothing but brokers in secret who seek to backdoor deals. Nevertheless, most of these new entrants will be slaughtered in terms of burning through their savings and capital on outdated marketing strategies or trying to compete within Strategic Networks that are already dominated by the biggest funders/lenders/brokers in the marketplace. Most of these companies will be fly-by-night companies, exiting the market as fast as they came running in.

UCC RECORDS WILL STILL BE POUNDED

I believe the UCC as a marketing tool will continue to be utilized by most of the newer entrants, despite the fact that the UCC Boom is Over.

BACK-DOORING WILL SIGNIFICANTLY DECREASE

Back-dooring will decrease significantly as brokers smarten up by researching the partners they decide to work with beforehand, and not just sending over ISO Agreements to “anybody” that calls them up and says they might be able to do something for their deals that other funders can’t do. Also, brokers will stop functioning as a sub-broker as well, which makes no sense, and this will also assist with bringing down the back-dooring issue. The heart of the back-dooring issue is the broker’s laziness, it is their laziness in properly vetting the partners they choose to work with, as well as deciding to sub-broker on a deal instead of researching the players in the marketplace on their own so they have adequate platforms available for any type of merchant they receive.

INDUSTRY WIDE REGULATION WILL GET CLOSER

While we can pinpoint that this is already going on in California, I believe you will continue to see some type of industry wide regulation that will restrict access to new brokers and seek certain levels of ethics from current brokers. This might be from within the industry itself, or it might be forced upon us from some type of regulatory agency. I’m hoping we can do this ourselves and not bring in the Government.

MARKETPLACE LENDING AS A WHOLE WILL CONTINUE TO GROW

It’s been estimated that we will see over $100 billion globally in marketplace lending (consumer and commercial side) in 2016, and I agree with this metric. I believe our products will gain more mainstream attention and be accepted more as the “standard” rather than an “alternative”, based on the efficiency of how we deliver capital, versus the extensive and inefficient process of the traditional lending system.

Why You Shouldn’t Overlook Selling Merchant Processing

January 4, 2016 Prior to daily fixed payment business loans, there was the traditional merchant cash advance (MCA). The MCA, being the only option, required merchants to tie their need for working capital to that of their merchant accounts, either directly or indirectly, through the use of either split-funding or a lockbox account.

Prior to daily fixed payment business loans, there was the traditional merchant cash advance (MCA). The MCA, being the only option, required merchants to tie their need for working capital to that of their merchant accounts, either directly or indirectly, through the use of either split-funding or a lockbox account.

DIRECT OR INDIRECT?

Split-funding is a direct method that requires the merchant to convert their merchant account over to a chosen Independent Sales Organization (ISO), you could also refer to the ISO as a Merchant Service Provider (MSP). The MCA company contracts with an ISO/MSP who then manages the flow of the merchant’s daily credit card processing volume. A percentage is withheld and forwarded to the buyer of those receivables.

The lockbox is an indirect method to manage the flow of funds. Rather than withhold funds from the ISO/MSP, a separate FDIC insured account is established on the side for all credit card processing receipts to settle into initially, with a percentage of that volume going to the buyer and the remaining amount “swept” into the merchant’s operating account.

Nevertheless, whether directly or indirectly, the merchant account of the business owner was the foundation of the MCA approval and facilitation. Because many MCA companies also offer alternative business loans today with fixed payments, a lot of the new broker entrants do not believe that learning about the field of merchant processing is as important today as it was years ago. However, I disagree with this notion, as the purpose of our industry is the long term relationship with the client, and in many ways the traditional MCA product provides more “benefits and value” to the merchant over time than today’s business loan. Just as new broker entrants get to know all about the MCA, they should also get to know all about merchant processing.

OVER TIME, CAN THE MCA BE THE BETTER CHOICE?

The alternative business loan requires no merchant account conversion as it doesn’t tie the merchant account to the facilitation of the working capital transaction. With these loans, a percentage of gross revenues are approved with fixed terms up to 36 months on daily or weekly payments. The main benefit of this product over the MCA is the awareness of payment frequency and quantity upfront, thus, enabling the merchant to better allocate their cash flow.

However, while the traditional merchant cash advance requires the tie-in of the merchant account, there’s no fixed terms nor fixed payments as it correlates with the merchant’s sales cycle, where they deliver more during busy times, less during slow times.

When selling the merchant the long term aspects of the MCA, why not seek to get their MCA funded using the split-funding method rather than a lockbox? Doing so would provide an additional revenue stream within your client portfolio. To properly seek out this opportunity and be able to consult, convince and convert the merchant over to your MCA firm’s ISO/MSP Partner, you want to fully understand what merchant processing is all about.

WHAT IS MERCHANT PROCESSING?

A merchant account is an unsecured line of credit provided to a business from a registered ISO/MSP. The credit line enables the business to benefit from accepting Visa and MasterCard (V/MC) along with other major bankcards from their customer base, to experience the benefits of acceptance which includes better fraud management, higher average tickets, customer loyalty due to convenience, and more. V/MC are just registered card brands that manage a group of banks called “member banks”, which are banks apart of a listing of V/MC bank associations. The member banks pay V/MC dues and assessments to market their brands. You have different types of member banks, you have the Issuing Banks and then you have the ISO/MSP along with the Sponsoring Banks.

The Issuing Banks issue credit cards with credit limits to consumers after they meet credit criteria. On the processing side, you have the registered ISO/MSP and Sponsor Banks, which approve a merchant for a merchant account and process payments through a front-end authorization network, then settles them through a back-end network.

During the processing of a credit card transaction, there’s a couple of different fees that are charged. Interchange is one of the fees charged, which is how the Issuing Banks are paid. These are wholesale prices for every type of card that a merchant could potentially run at the point of sale, with new interchange pricing charts released in April and October of every year. The ISO/MSPs are paid when they mark-up interchange as well as through fees such as an annual fee, statement fee and batch fee.

WHY IS MERCHANT PROCESSING A UNSECURED LINE OF CREDIT?

The merchant account is indeed an unsecured line of credit, because when a merchant’s customer runs an order on their credit card for $500, the merchant would rather have that entire $500 upfront rather than waiting for the customer to pay off their credit card balance in full, which could potentially take years. As a result, the ISO/MSP deposits the amount in their bank account within 48 hours rather than having the merchant wait until their customer pays their credit card balance in full.

Now, if the merchant’s customer initiates a chargeback of the $500 transaction and the merchant loses the case, the $500 would have to be refunded by the merchant plus the costs of the chargeback which includes a chargeback fee and retrieval fee. If the ISO/MSP goes to get the $500 from the merchant and there’s no money in their account (let’s say the merchant has gone out of business), then the ISO/MSP who underwrote the merchant account is on the hook for the charge.

WHY SHOULD YOU SELL MERCHANT PROCESSING?

When using split funding for a merchant cash advance deal, if you switch over their processing to an ISO/MSP that your MCA firm currently split funds with, you are looking at collecting the long term residuals from the processing and the compensation from future merchant cash advance renewals. In addition, split funding is much more efficient than using a lockbox, as a lockbox usually adds 1-2 business days to the settlement process for everyone involved. Withsplit funding, the merchant can continue to receive their processing deposits as normal.

There are different types of payment processing technologies depending on what the merchant needs, if they need a stand-alone solution then that’s available in the form of a landline terminal, wireless terminal, computer software or virtual terminal. If the merchant needs a comprehensive solution then that’s also available in the form of point-of-sale systems or operational management technologies, both of which integrate merchant processing into the system and other operational aspects such as accounting, payroll, human resources, etc.

Why not just have the merchant switch over their processing to an ISO/MSP that your MCA firm currently split funds with, and collect recurring merchant processing residuals along with recurring income from merchant cash advance renewals? After all, recurring income is the lifeblood of our business.

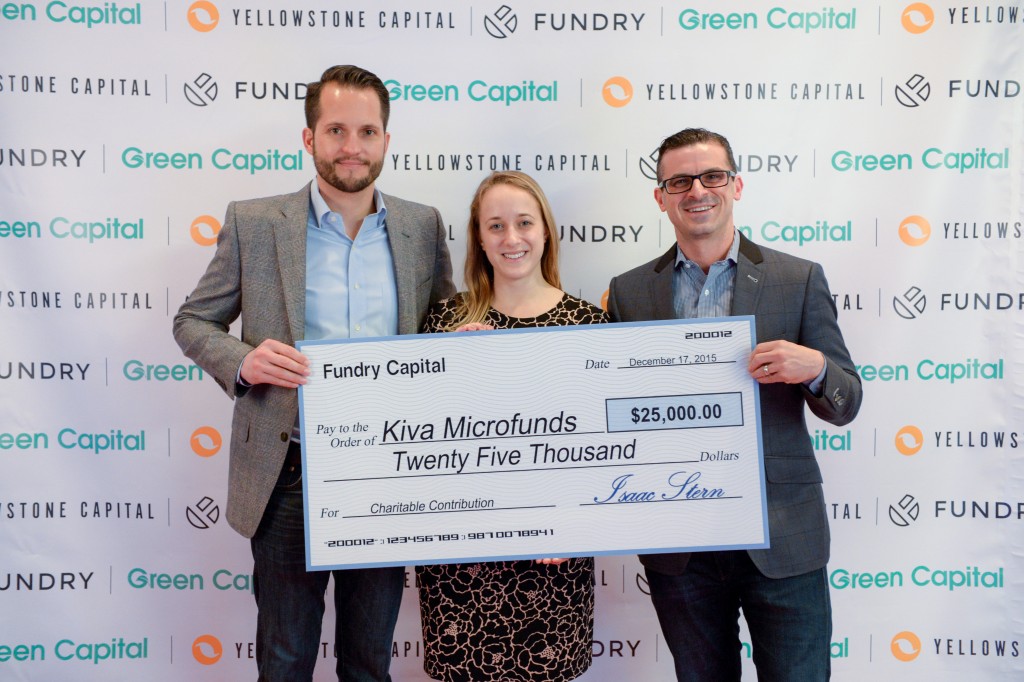

Fundry Donates $25,000 to Kiva at Red Carpet Event

December 22, 2015Fundry, the parent company of Yellowstone Capital and Green Capital, hosted a red carpet event last Thursday evening in New York City where they presented a donation of $25,000 to Kiva. Kiva is a non-profit organization with a mission to connect people through lending to alleviate poverty.

The event, which also celebrated their 2015 success, was attended by more than 300 people. All told, Fundry originated nearly half a billion dollars in small business funding for the year.

I Hate Sales, But I Love Business Development

December 21, 2015 I HATE SALES

I HATE SALES

I have always hated “sales”, which is funny seeing as though I have been in what most would call a “sales position” within our industry since January 2007, all on an independent (100% commission) basis as a one man show, with merchant services direct sales from 01/2007 – 04/2009 and merchant cash advance direct sales from 11/2009 – 09/2015. As a one man show, I did pretty good, getting myself into the middle class with a great net worth for my age, with an average monthly funding of $200k per month for the 70 months I sold the MCA product, while building a processing portfolio on the side on track to hit $200 million in total volume processed.

But nevertheless, I hate “sales”.

While most would consider my place in this industry (nearly 9 years) as a “sales” role, I would vehemently disagree, as I believe my role has been that of business development, not “sales.” I was an entrepreneur (or solopreneur due to being a one man show) and my focus was on building strategic relationships with merchants, vendors, and partners, with a clear-cut focus on creating long-term sustained value.

WHAT DO I REFER TO AS SALES?

I believe there are different variations of salespeople, from the cashier at the grocery store, to the person at the fast food drive-thru window, to the waiter, to most of the inside sales people across the country. I believe the majority of salespeople are simply order-takers.

- An order-taker is not a strategic thinker, innovator, researcher, nor creator. They are not seeking to solve complex problems by creating complex solutions, with complex pricing and implementation procedures, which simultaneously include complex supporting functions.

- An order-taker is someone that usually performs a routine task of helping a customer find a particular item or purchase a particular item. The order-taker’s knowledge of the business, the industry, and the customer is very limited. The order-taker is very robotic and nothing more than a regurgitator of information taken from people within the organization who have been given the “liberty” to think, innovate, research and create.

In a corporation, the individuals who are given the liberties to think and innovate are usually the CEO, CFO, or members of the marketing department, all of which are responsible for the strategic direction of the organization in terms of markets targeted, driving in prospective customers, creating the products to push to said prospective customers, how to manage the process of turning them from a prospective client to a current client, and all of the follow-up procedures that are a result. You can sum up the actions and responsibilities of these individuals into two words: business development.

SALESPEOPLE WILL BE REPLACED BY ROBOTS AND TECHNOLOGY

As we progress through the 21ST Century, developments in technology will in fact replace salespeople (order-takers). Their duties are so routine and robotic, that it’s much more efficient in a number of cases to just implement a robot instead, and save on the higher costs of labor. Or to put up an efficient website and allow the website to navigate the customers rather than a salesperson.

But those in business development can never be replaced by a robot.

WHAT IS BUSINESS DEVELOPMENT?

Those that are in Business Development are responsible for the building of strategic relationships with merchants, vendors, and partners, with a clear-cut focus on creating long-term sustained value. Long-term sustained value always comes in the form of new markets, new products and new processes, which manifests itself in the strategic role of CEO, CFO and Marketing Departments in corporations, but in smaller companies, this manifests itself in one word: entrepreneurship.

Entrepreneurship is all about taking a look at what’s currently happening and asking, how can this be done better? What segment of this market isn’t being catered to? How are the current solutions and products being pushed to this market inefficient? And how can I create better ones? How can I acquire new clients more profitably than competitors are?

That’s business development, which is different from being in “sales.”

BUSINESS DEVELOPMENT IS WHAT I DID

I often debate other professionals in our industry on commission points, as it comes up often today on how one should be making “8 – 10 points per deal” and if you aren’t making such level of points, they believe that you are doing something wrong.

My strategy was different, when I started selling the MCA product in very late 2009, my focus was solely on targeting A and B-Paper clients, which at the time there weren’t any pricing distinctions between low risk and high risk merchants. A merchant approved for an advance in general, was given the same high cost product, whether they had a 700 FICO or a 520 FICO.

My objective was to sell a more efficiently priced product to higher quality merchants, with great supporting functions in place to produce significantly low default rates, and a much higher than normal renewal rate. This strategy was completely different at the time than what the industry as a whole was doing in terms of the merchant cash advance product.

Over on the merchant processing side, my focus was to target higher risk merchants, which were more difficult to board and service, rather than targeting the same Card-Present mom/pop shops that everybody else was doing at the time who quite frankly, had no real needs for merchant processing nor the related technologies and value-added services associated as they already were “set.”

BUSINESS DEVELOPMENT IS WHAT YOU SHOULD DO

Some of you might not have the luxuries to think, innovate, and create, as you might be on a W-2 structure which puts you at the mercy of a “sales manager” who more than likely is using outdated marketing tactics (such as UCCs and Aged Leads) and encouraging you to sell a product that is not always the right fit.

Of course if you don’t achieve the established quotas, the sales manager will scold you by saying that you don’t belong in this industry, rather than looking at the main source of the problem, which is their outdated marketing tactics and uncompetitive solutions.

But for those of you who have such luxuries, I invite you to think, innovate and create. Be different. Be bold. Go after markets not talked about and solve the pain of others that have yet to be analyzed. Market different. Brand different. Sell solutions that others have yet to hear about.

Your bank account and career longevity will thank you later.

All in The Family (The MCA Kin)

December 20, 2015 FAMILY TIES

FAMILY TIES

During the holidays we get together with our family to reminisce on the good times, celebrate achievements, and be thankful for life’s fortunate moments. Most of the brokers within our space have families of their own to tend to during the holidays, which might include a large family gathering with relatives flying in from outside of the area, or it might just include a peaceful dinner with a small assembly.

But this has surely been the Year of the Broker, and what many of these new entrants might not realize is that the product we sell all year round (the merchant cash advance) has a family as well. While the MCA doesn’t exchange “gifts” with its kin, it sure does have a lineage that dates back to the 1600s, which makes the product something born out of a family of products, rather than something that seemingly just sprung up out of nowhere one day in 1998, by a company formerly known as AdvanceMe.

ALTERNATIVE FINANCE AND PURCHASING REVENUES HAVE BEEN AROUND A LONG TIME

- (The 1600s): The product is nothing but a purchase of future revenues or receivables, where a merchant is going to sell their receivables or future revenues to a purchaser, with a particular factor rate or “discount rate” applied to the transaction. This act is nothing new at all, as it has been around since the 1600s but didn’t become more common practice until around the 1800s in terms of the United States.

- (The Middle Of The 20th Century): The MCA is an alternative finance option from more boutique/niche firms, compared to the traditional products of terms loans and lines of credit from retail banks and credit unions. Alternative finance as a “comprehensive term” has been used in a mainstream fashion since the middle of the 20TH century, so this “act” is nothing new.

- (The Newborn): In other words, the merchant cash advance product is just the most recent “birth child” from a long and storied “family dynasty” of alternative financial services and revenue purchasers.

FAMILY GATHERING

The “family members” of the merchant cash advance include a variety of alternative financing vehicles that are popular and not as popular as others. For this article in particular, I wanted to discuss some of the more popular “family members” which include A/R Factoring, A/R Financing, P/O Financing, Equipment Leasing, Asset Based Lending and the Alternative Business Loan. This article will provide a general overview of each “family member”, which will serve as an introduction to a future article where I will go into specific sales strategies for many of the listings.

ACCOUNTS RECEIVABLE FACTORING

This product is based on a merchant having outstanding commercial receivables that are aged less than 60 – 90 days. With Factoring, the factor (buyer) is going to purchase the outstanding receivables from the merchant (seller), taking them off of the merchant’s balance sheet as an asset and onto the balance sheet of the factor. During the purchase, the factor advances about 80% of the amount purchased upfront to the merchant, with the remaining 20% coming after the merchant’s client base completes payment within 30 – 90 days, minus a discount fee of anywhere from 1% – 5%. Non-recourse factoring transfers the risk of the clients not paying the balances in full to the factor, while recourse factoring keeps the risk contained to the merchant.

ACCOUNTS RECEIVABLE FINANCING

This product is also based on a merchant having outstanding commercial receivables similar to Factoring, however unlike Factoring, there will be no purchase of the outstanding receivables but instead they will just be used as security/collateral for a financing arrangement.

PURCHASE ORDER FINANCING

This product is based on a merchant having outstanding purchase orders where a lender provides funds so a merchant can order materials to fulfill orders. Then once the orders are fulfilled, the lender collects a fee for service. This can also be done in the form of a vendor line of credit, where the lender opens a credit line with the vendor to allow the business to get materials needed to fulfill upcoming orders.

EQUIPMENT LEASING

This product basically allows a merchant in need of commercial equipment, technology, machinery, vehicles, tools, and furniture, to lease it rather than buying, as certain pieces go obsolete rather quickly and wouldn’t make sense for purchasing. The merchants are provided lease factor rates based on A-D credit grades, with options at the end of the lease to buy the unit(s) for $1.00, give them back, or start another lease period.

ASSET BASED LENDING

This product is based on a merchant having a particular type of pre-owned asset of appraised value, that could be used as security/collateral for a financing arrangement. The aforementioned Accounts Receivable Financing product can also be considered an asset based lending product, but also included are pre-owned pieces of equipment which could be used for sale-leasebacks or other items such as luxury vehicles, real estate, precious antiques and jewelry.

ALTERNATIVE BUSINESS LOAN

This product is similar to the merchant cash advance, as it’s based on a merchant having a particular consistent amount of monthly revenue, and approved as a percentage of annual gross revenue. The product can come from lenders that also offer merchant cash advance products or lenders who solely specialize in this alone.

AS A FINAL NOTE, MAKE SURE TO REMEMBER THE MCA’S VALUE

While the MCA is the baby in the family, don’t let its “youth” undermine its value. An MCA could potentially cost more than a loan, but a merchant might not be eligible for a loan or a loan might not be available fast enough to take advantage of a market opportunity. Merchants might not have assets available for collateral, eligible accounts receivable, and they might not issue invoices to customers on terms. That means merchants might have better luck with some family members than others just based on their business model or circumstances.

Happy Holidays.

Getting a California Lender’s License

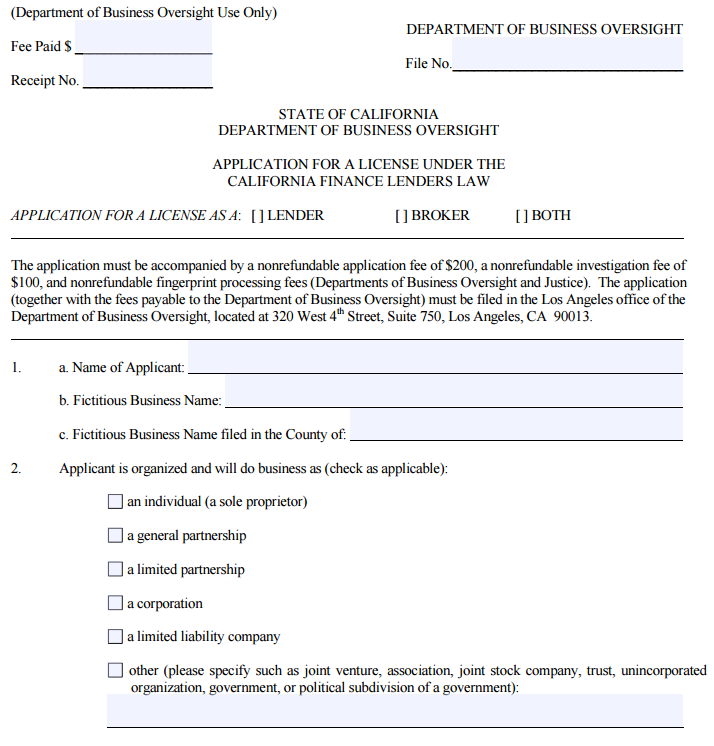

December 17, 2015Given the fact there have been a number of successful lawsuits against cash advance companies in California, many cash advance companies have decided to take a different route and get a lending license to provide loans to merchants in the state. If done correctly, this can allow companies to provide loans to merchants in California at roughly the same profit margins one could expect from a cash advance. Below I will discuss the process for obtaining a California lender’s license and some tips for making that process less painful.

To start, go to the California Department of Business Oversight and get the form titled “Application for a License Under the California Finance Lenders Law.” The application is long and detailed but don’t let that scare you. Most of the information you provide is really more related to letting the State know about your company and the main people that will be responsible for managing the lending operations. As you complete the form, one thing you do need to do is make sure you are very careful and meticulous as any small mistake will cause the application to be rejected making the process much longer.

To start, go to the California Department of Business Oversight and get the form titled “Application for a License Under the California Finance Lenders Law.” The application is long and detailed but don’t let that scare you. Most of the information you provide is really more related to letting the State know about your company and the main people that will be responsible for managing the lending operations. As you complete the form, one thing you do need to do is make sure you are very careful and meticulous as any small mistake will cause the application to be rejected making the process much longer.

The first part of the application requests basic information about your company and its officers. In filling out this and other parts of the application, it is essential to respond to all the questions. If you fail to miss just one response the application will be rejected. To that end, even if a question does not apply to you I find it better to respond “N/A” or “not applicable” rather than just leaving a blank. By doing that you force yourself to fill in every blank and therefore reduce the chances for missing a response resulting in a rejection of your application.

Also, you need to be very precise in your responses. I have experienced a situation where the examiner rejected an application because the name of the company was incorrectly spelled on the application. The name of the company was submitted on the application with “Inc” instead of the complete “Inc.” at the end of the company’s name. The examiners are very good at what they do and very thorough. You need to make sure the packet you submit is perfect and also that there are no inconsistencies in the document.

Another important point to remember is that the application requires you to name the person that will be responsible for running the location where the lending is occurring. The main requirement is that the person running the location must be physically present at the location. As a result, you could not manage a California office remotely from New York for instance. In another twist, if your principal location is out of state, you will need to get the license and fill out the main application for that out of state address. For the California location, you will need to fill out the short form application in addition to the main application and submit the short form application as part of the packet to allow the license to apply to the location in the state of California.

There are a number of exhibits you also have to provide as part of the process. Some of them are simple like a balance sheet for the company. It is acceptable that the company is new and has little in the way of assets. You just have to make sure you attach a balance sheet and that it is prepared in compliance with generally accepted accounting principles. I have seen times when the balance sheet was rejected because there was no line items for liabilities for instance, even though the company was new and therefore had none. It is probably wise to engage your accountant to make sure you submit a balance sheet that complies with those guidelines.

You also have to get a surety bond in the amount of $25,000. There are readily available bonding companies that specialize in providing these bonds. In addition, you need some other exhibits like a statement of good standing for your company, authorization for financial disclosure, social security number (on a separate exhibit), organizational chart and a few other documents. As with the rest of the application the key is to make sure you include everything they are asking for exactly as requested.

The most involved exhibit is the “Statement of Identity and Questionnaire.” That exhibit has to be filled out for each owner, officer and manager listed on the application. It requests detailed information going back 10 years for each person for items like residence address and work history.

In addition, there are a series of questions on topics such as whether the person has been involved in lawsuits, had any licenses revoked or declared bankruptcy. Fingerprints are also taken as part of the process. This part of the application is trying to vet the various people working for the company to make sure they are suitable to be in the lending business.

Once you have all the documents prepared, you need to put them together in a packet to send off to the Department of Business Oversight to be reviewed. Again, I cannot overemphasize how important it is to completely and accurately answer the questions and put the packet together. You need to make sure things are in the proper order and complete. Triple check the application for errors and to make sure that packet is presented in the best manner possible. You also need to determine the amount of fees to submit with the application. Then, send the package by overnight delivery to make sure you have proof of delivery.

So what happens next? Well there is usually a bit of a wait. Typically it takes 3 months or more to get a reply. If you have done your homework, you might get lucky and successfully get your license on the first try. If there are any deficiencies, you will get a response letter from the State detailing the items that need to be corrected in the application and a time frame in which you have to respond or the application is abandoned.

On the first go round, you are usually given at least 2 months so you should have plenty of time. Digest the things they want and provide the required information. The deficiency letters are very detailed so it should be easy to make the requested changes. Resubmit the requested items and wait for the next response. It could be in the form of another deficiency letter but it could be an approval of the license. Just keep on trying until you are finally successful.

That’s it, you are finally a licensed lender in California! But that is where the fun begins. You are subject to many laws in California and audits by the State. To get the right to operate as a licensed lender, you need to make sure you prepare your application correctly. Once you have done that, you need to get all your loan documents drafted in compliance with California law. Make sure you have adequate experience and professional help to take on those tasks.

The Broker’s Future Part Two

December 16, 2015THE ROBOTS ARE COMING

Merriam-Webster and Dictionary.com both agree, that a “robot” is a machine that is created to do the work of a person, carrying out a complex series of actions automatically, all controlled by a computer. Sometimes a robot can resemble a human being in likeness, but often times a robot is simply a piece of software, a piece of hardware, a piece of machinery, or a cloud based infrastructure called the internet (online networks). Professor Kaku is a futurist from City College of New York, a futurist is someone who makes what one would consider “fairly accurate” predictions about what the future holds and how these future events might emerge from present day events. Professor Kaku believes the following:

Merriam-Webster and Dictionary.com both agree, that a “robot” is a machine that is created to do the work of a person, carrying out a complex series of actions automatically, all controlled by a computer. Sometimes a robot can resemble a human being in likeness, but often times a robot is simply a piece of software, a piece of hardware, a piece of machinery, or a cloud based infrastructure called the internet (online networks). Professor Kaku is a futurist from City College of New York, a futurist is someone who makes what one would consider “fairly accurate” predictions about what the future holds and how these future events might emerge from present day events. Professor Kaku believes the following:

The job market of the future will consist of those jobs that robots cannot perform. Our blue-collar work is pattern recognition, making sense of what you see. Gardeners will still have jobs because every garden is different. The same goes for construction workers. The losers are white-collar workers, low-level accountants, brokers, and agents.

A RECAP OF PART ONE

Back in June 2015, I did an article for deBanked about the Broker’s Future, speculating if the good times were indeed over for the brokers as it pertains to their level of profitability and survivability going forward.

- I examined the 2000 – 2007 and 2008 – 2013 time periods, speculating that the “Era of the Broker” was indeed between the 2000 – 2013 period.

- Then, I examined the current time period which begins around the middle of 2014, that is seeing so much of a mass new entrance of brokers into the space, that deBanked had to compose a cover story on the phenomenon for the March/April edition of deBanked Magazine. The only issue with this current time period is that, in my sole objective opinion, we are in the “Era of the Strategic Networks”, and no longer in the “Era of the Broker.”

- I concluded the article in June with the following: those just now trying to come in and ride the wave will soon discover that just like with the Stock Market, the real money has already been made and most of the future returns are already capitalized.

AN INTRODUCTION TO PART TWO

My analysis shows that the current time period is all about Strategic Networks, which are mainly three networks to be exact, which include the following, all designed to produce competitive market advantages, positioning, strategies, qualified leads, etc:

- The Center Of Influence Network: this includes entities such as banks, credit unions, processors, accountants, VCs, credit bureaus, etc., that allow access to exclusive leads, exclusive data, equity financing, debt financing, mergers, etc.

- The Mom and Pop Network of random independent agents across the country who resell on a 100% commission basis, providing free marketing in a way that collectively they produce a significant amount of volume (even though individually most of the agents cannot make a living from this activity).

- The Online Network with exclusivity on the growing online marketplace of merchants seeking financing, education and options via the internet.

For Part Two Of The Broker’s Future, I want to focus in on The Online Network, which in my opinion will be one of the main destroyers of opportunities in our space for the majority of brokers going forward.

DEATH OF A B2B SALESMAN

For about $499, you can read a very comprehensive report from Forrester on the death of B2B salespeople. Forrester predicts that by 2020, over 1 million B2B salespeople will lose their jobs to the growing force of IT/Robotics, which includes various forms of technology, automation and of course the internet in general through E-commerce.

In relation to our industry of merchant services, merchant cash advance and alternative business loans, I don’t believe that we have to wait until 2020 to see significant changes, I believe these changes are already in full effect and the major players within our space are the ones that are truly capitalizing on The Online Network, giving them major exclusivity on the growing online marketplace of merchants seeking financing, education and options via the internet.

MERCHANT SERVICES HAS BEEN AFFECTED

The Online Network phenomenon has totally destroyed the feet on the street MLS (merchant level salespeople) over on the merchant services side. Before the rise of the Online Network, MLS were valuable to merchants as information on merchant processing, interchange, how the bankcard transactional process worked, etc., were not readily available and most banks did not handle direct sales of the service. So the MLS would park their car down the street, randomly walk into merchant locations, and provide the education via brochures, terminal samples, etc.

They would explain how the merchant processing process works, how accepting credit cards could boost sales through more impulse purchases and consumer convenience, and more. The MLS would then go over the different options of payment processing technology, commit the merchant to a 24 – 48 month lease of the technology, and make his/her commission off the leasing sales and eventually also off the residuals. However, the rise of the Online Network completely shattered this business model:

- The Online Network now allows the merchant to comprehend merchant services on his own, without the help of the MLS, by researching interchange and conducting his own “rate analysis”. The merchant can also now see the true cost of the processing equipment, thus to no longer sign up for leases for $100 a month for 24 months ($2,400) for a $350 terminal at best.

As a result, the MLS can no longer prospect on “rate savings” nor prospect based on the equipment such as through leases or even through free terminals anymore, due to the merchant’s knowledge that the terminal is worth $350 at best. As a result, the direct sales of merchant services has become a value-add to other services, requiring yesterday’s MLS to transform into something totally different such as a financing or payroll specialist, trying to convert merchant accounts over on the side, as part of the sale.

ALTERNATIVE LENDING HAS BEEN AFFECTED

The merchant cash advance and alternative business loan products are more popular today than they have ever been before, due mainly to the massive media attention that they have received with companies going public, CEOs landing interviews on major media outlets, talking heads debating the products across a number of media mediums, and more. 7 – 15 years ago (2000 – 2008), if you were to look up a product online called “merchant cash advance”, you would not have produced many search results. As a result, to inform and educate the merchant on the product, you needed an actual human being (a broker) to sit down and explain the nuances of said services referred to as “split funding”, “revenue purchases”, and “holdback percentages.”

Compare this to today, where a simple search for “merchant cash advances” gives you pages upon pages of articles, promotional ads that follow you across the internet, company websites, press releases, and more. The merchant can easily learn about the merchant cash advance as well as other new forms of alternative financing by going online and scrolling through the vast amount of information. They can educate themselves on the products, companies, and payback procedures. They can fill out a form and get 10 quotes from 10 companies within a couple of hours and in a lot of cases, receive funding from one of the companies by the next business day. The phenomenon is so big that companies in our space are now just referred to as “Online Lenders,” totally shunning the fact that many operate with traditional brick and mortar locations and still employ brokers to still resell the products like they did “in the old days”.

THE FUTURE

Based on my sole objective analysis, The Future is going to be all about the three networks of Strategic Partnerships, which includes The Online Network. Without a shadow of a doubt, those that control these networks will be the major players going forward, as they will have the leveraged resources, knowledge, experience, financing, and connections that the newer market entrants just do not have.

The 80/20 dynamic will continue, where 20% of the players produce 80% (or more) of the production, and the other 80% of the players will fight over the remaining 20% (or less) of the production, which just will not be enough to sustain profitability going forward.

As fast as these new entrants rush in, will be as fast as they burn out. Burning through their savings and retirement funds, and/or running up the utilization rate on their credit cards, trying to take advantage of a “market opportunity” that they “heard about”, but is pretty much already capitalized on, by those who have been here long before they came on the scene.