Business Lending

Lending Express Opens Office in Silicon Valley

June 13, 2018 Tel Aviv-based Lending Express announced its entrance into the U.S. market yesterday. It opened an office in San Matteo, CA and has officially appointed Moshe Kazimirsky as VP of Strategic Partnerships and Business Development to support the new West Coast office.

Tel Aviv-based Lending Express announced its entrance into the U.S. market yesterday. It opened an office in San Matteo, CA and has officially appointed Moshe Kazimirsky as VP of Strategic Partnerships and Business Development to support the new West Coast office.

“After the immense success we’ve had in the Australian market, we knew that our platform was ready to take on the U.S.,” said Lending Express CEO Eden Amirav.

Lending Express initially launched its business in Australia in October 2016. The company provides an online marketplace that connects merchants to alternative funders. After only a year and a half, Amirav told deBanked that Lending Express is now the largest business of its kind in Australia – even though they only set foot on the continent a month ago.

Meanwhile, Lending Express has also been operating in the U.S. for months and has already partnered with leading online lenders like OnDeck, Kabbage and Fundbox, according to Amirav. Given the company’s experience in both the Australian and American markets, deBanked asked Amirav what he thought the differences were.

“In general, they are much more similar than people think,” Amirav said. “But in the U.S., people like to look around more.”

Generally, if an Australian merchant is approved, they will move forward with the deal right away, Amirav said. Lending Express offers a myriad of products on its platform, including equipment financing, invoice funding, business line of credit and merchant cash advance.

So far, Kazimirsky, who has worked in business development for other Silicon Valley technology companies, will be the only one in the new California office. But Amirav anticipates that the office with grow. The Lending Express office in Tel Aviv has 25 employees, many of whom – namely the account managers – start their day at 3 a.m. in order to speak to their Australian and American customers in different time zones.

Lending Express uses an algorithmic system called MatchScore to pair borrowers with lenders.

Second Annual Alternative Finance Bar Association Conference Draws Lawyers from Afar

June 11, 2018 Attorneys who represent alternative finance companies congregated in New York on Friday for the second annual conference of the Alternative Finance Bar Association (AFBA.)

Attorneys who represent alternative finance companies congregated in New York on Friday for the second annual conference of the Alternative Finance Bar Association (AFBA.)

They came for a day of learning about the latest legal developments pertaining to alternative finance, and MCA in particular. Seminars at the conference had names like: “Credit Facilities 101: What an Alternative Finance Company Can Expect,” “Syndication Relationships: Partner? Participant? Investor?” and “Bankruptcy Developments: The Rise of the Adversary Proceeding.”

“I think it’s like heaven for a new attorney in the MCA world,” said Judith Ramos, who is Corporate Counsel at McKenzie Capital in the Miami area.

Another attorney somewhat new to the MCA space and eager to learn more was Alexis Shapiro, General Counsel at Forward Financing in Boston.

“This was one stop shopping to learn about the latest legal developments in the MCA industry,” Shapiro said.

In one seminar, called “Updates on Recent Case Law,” attorney panelists Steven Berkovitch of ABF Servicing and Adam Stein and Christopher Murray of Stein Adler Dabah and Zelkowitz, discussed the positive impact of the Pearl Beta Funding v Champion Auto Sales decision in New York. They spoke about how judges have dismissed lawsuits against their MCA clients by referencing this decision, which establishes that MCA deals are not loans.

Murray reviewed the current climate with regard to MCA cases in New York, California, Texas and Utah. And one panelist emphasized the importance of simply being knowledgeable about the industry by relating a story of an MCA defense lawyer who, when asked by a judge about the interest rate on a particular MCA deal, fumbled and gave a percentage. (MCA deals do not have interest rates given that payments are subject to change over time).

Later, Gregory Nowak, a partner at Pepper Hamilton, entertained the crowd with a few jokes before diving into the details and the risks of syndication. The conference was held at New York offices of Pepper Hamilton, with expansive views of the Hudson River.

Later, Gregory Nowak, a partner at Pepper Hamilton, entertained the crowd with a few jokes before diving into the details and the risks of syndication. The conference was held at New York offices of Pepper Hamilton, with expansive views of the Hudson River.

“We are energized by the response of so many attorneys from different backgrounds in this emerging and evolving industry,” said one of founders of the AFBA, Lindsey Rohan, General Counsel at Platinum Rapid Funding Group in Long Island.

AFBA’s other founders are Kate Fisher, partner at Hudson Cook outside of Baltimore, Patrick Siegfried, Assistant General Counsel at Rapid Advance in Bethesda, MD, and Murray, attorney at Stein Adler outside of New York City.

Robert Cook, one of Hudson Cook’s founding partners, was at the conference. He told deBanked that he remembered back in 2006 when an investment bank client asked his firm to do due diligence on a merchant cash advance company.

Robert Cook, one of Hudson Cook’s founding partners, was at the conference. He told deBanked that he remembered back in 2006 when an investment bank client asked his firm to do due diligence on a merchant cash advance company.

“We didn’t know what that was,” Cook said. “The client looked around for a law firm that had experience with MCAs. They couldn’t find any. So they came back to us and said, ‘You’re going to have to learn.’”

More than a decade later, MCA is no longer so obscure and the AFBA has at least three more planned events in 2018. The next event will be a cocktail reception on October 24th.

For more information, contact: Tiffany@LRohanlaw.com

deBanked was also a sponsor of the second annual AFBA conference.

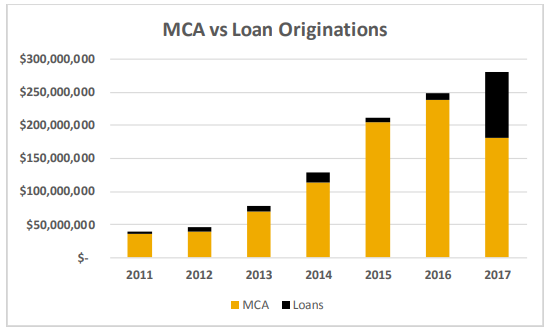

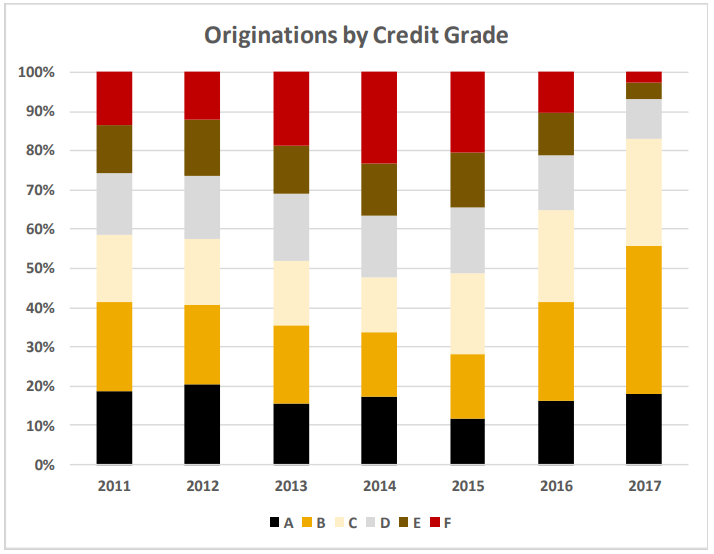

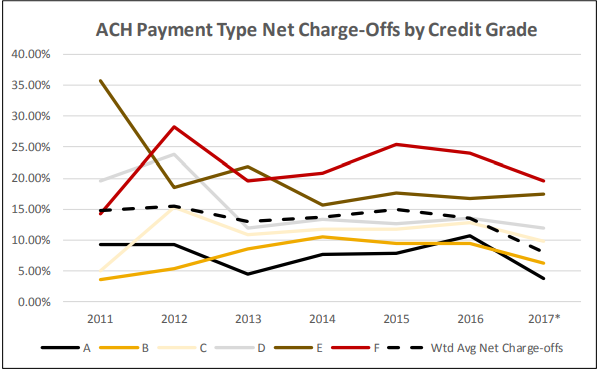

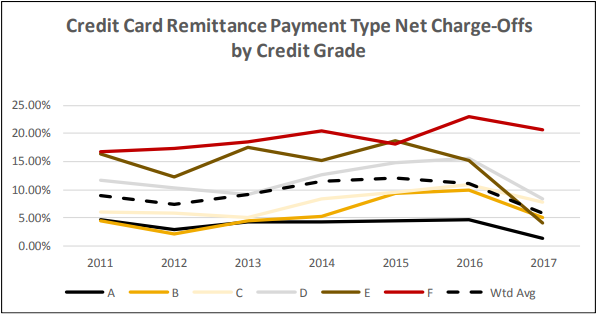

An Inside Look at Strategic Funding’s Portfolio

June 10, 2018A Kroll Bond Rating Agency report reveals interesting details about Strategic Funding Source’s $105 million securitization and also their business. Here are a few main takeaways:

Pool breakdown

60% MCA

40% Loans

Average original receivable balance per merchant: $40,705

Weighted Average FICO Score: 649

Weighted Average RTR Multiple: 1.35

Weighted Average Time in Business: 12.5 years

Weighted Average Gross Revenue: $1,729,709

Number of ISOs/referral partners: 1,300

In an earlier interview, Strategic Funding CEO Andrew Reiser said, “It’s certainly exciting to be able to meet the requirements of a securitization. Kroll is a very responsible agency and they put you through a lot of rigor to be able to meet [their] requirements and have a rated bond.”

US Business Funding Will Retain Name & Special Sauce in Wake of Fora Deal

June 8, 2018Fora Financial’s announcement yesterday that it acquired a sizable stake in US Business Funding (USBF) will create one of the “largest, broadest reaching direct sales organizations in the small business alternative lending space,” the company said in a statement.

USBF is a direct sales and marketing company of about 40 to 50 people. Fora Financial founder and CEO told deBanked that his company started working with USBF to obtain leads two years ago and that this acquisition has been in the works for between 12 to 18 months.

Jared Feldman, CEO, Fora Financial

Jared Feldman, CEO, Fora Financial“We were looking for a team that does direct sales and marketing that complements what we do,” Feldman said. “And they’re one of the best at [direct marketing] in the business.”

USBF is based in Santa Ana, CA, and has connected customers to financing since 2008, with an emphasis originally on equipment financing. In 2012, they started facilitating working capital deals and that now makes up 85 percent of the company’s business, according to its CEO Peter Ribeiro.

They provide financing solutions ranging from $10,000 to $10 million. Fora Financial, also established in 2008, is a New York-based funding company that funds MCA deals and provides small business loans up to $500,000.

Consistent with yesterday’s announcement, Feldman said that with Fora Financial and USBF combined, they will likely originate $400 million year. Feldman told deBanked today that, of this amount, about $300 million should come from direct sales.

“We’re more heavily weighted towards direct sales,” Feldman said.

Formerly a company of 100, the new entity will now include about 150 employees and will share resources like capital, technology and access to help with compliance, Feldman said. USBF will retain its name, location and all of its employees.

“We wouldn’t have done this deal unless Peter [USBF founder and CEO] and his team agreed to stay on,” Feldman said. “They have a fantastic brand and we want to avoid getting in their way. We just want to help them to continue doing what they do.”

Feldman said that while USBF will retain its name, “we’re now a combined entity with an east and west coast operation.”

Fora Financial acquired USBF because it did something unique, and Feldman said that Fora is looking for opportunities to acquire other companies that do uniques things in the financing space.

PeerIQ Report Shows Mixed Signs for Non-Bank Lending

June 7, 2018PeerIQ released its 2Q2018 Lending Earnings Insight Report today, presenting forward-looking insights into the FinTech & non-bank space.

The report said that CEOs and CFOs see tax reform as increasing consumers’ disposable income. However, “an increasing supply for credit and demand for credit, as well as re-normalization trends and increased competition are leading to higher charge-offs.”

Credit performance this quarter is mixed, the report says. The analysts observe improvements, yet also record low delinquencies from OnDeck, OneMain Holdings and FinTechs in particular. At the same time, LendingClub expects 31 bps lower charge-offs moving forward due to tighter credit standards. At Discover – which is typically a bellwether for personal loan performance – the net charge-off rate jumped 92 basis points year over year to 3.62 percent. This is the largest increase in several years.

According to the report, card issuers are increasing loan loss reserves at a higher rate than loan growth, indicating expectations of higher losses moving forward. The report also notes that banks are either partnering with FinTechs or investing in ramping up their technology capabilities in payments, lending, digital banking and wealth management.

Lenders are taking actions to pass rising rates on to borrowers to protect margins and investor returns, the report says. Lenders are also trying to reduce all-in funding costs by reducing the credit spreads on their securitizations.

On the brighter side, the report said that “FinTech and Non-Banks overall posted good revenue growth [in Q1 2018] in the range of 7% to 25% and most expressed optimism about the exceedingly good credit environment we find ourselves in.” Enova, OneMain Holdings and OnDeck saw some of the lowest charge-offs, with Lending Club indicating that expected charge-offs across grades would be up to 31 bps lower, according to the report.

Report Demonstrates How Online Lenders Benefit Economy

May 31, 2018 A report on “The Economic Benefits of Online Lending to Small Businesses and the U.S. Economy” was released yesterday, using data from 180,000 U.S. small businesses that represented nearly $10 billion in funding from 2015 to 2017.

A report on “The Economic Benefits of Online Lending to Small Businesses and the U.S. Economy” was released yesterday, using data from 180,000 U.S. small businesses that represented nearly $10 billion in funding from 2015 to 2017.

The report used data from five online lenders, including OnDeck, Kabbage and Lendio, and was sponsored by the Electronic Transactions Association (ETA), the Small Business Finance Association (SBFA) and the Innovative Lending Platform Association. The report was researched by three economists at NDP Analytics, an independent research firm.

One of the key findings was that the ten billion dollars funded from 2015 to 2017 by five of the top alternative small business lenders generated $37.7 billion in gross output and created 358,911 jobs and $12.6 billion in wages.

“I think the most important takeaway from this study is that small businesses are benefiting from a wide variety of choices in lending products,” said Jason Oxman, CEO of the ETA. “And, in particular, the online small business lenders have provided really a remarkable amount of working capital to small businesses in this country.”

Oxman told deBanked that he was surprised to learn from the report the percentage of borrowers that operate extremely small businesses. According to the report, 24 percent of online business borrowers operate businesses that have less than $100,000 in annual sales. And two-thirds of online business borrowers had less than $500,000 in annual sales.

“These are clearly small businesses,” Oxman said. “These are companies that obviously have capital needs and are getting those needs met by online small business lenders.”

New York State was a focus of part of the research. According to a press release for the report, data extracted from it indicated that “overall, the small business loans provided by online lenders [from 2015 to 2017] generated $2.5 billion in gross output and created 20,154 jobs with over $795 million in wages” for communities in New York State.

“We [organized the report] with New York in mind,” said Steve Denis, Executive Director at the SBFA. “We wanted to send a message to show how much of an impact the online lending industry had on the state.”

Other interesting data from the report include:

— 75 percent of U.S. businesses have less than 10 employees.

— 22 percent of small business owners use their personal savings to expand

— Online lenders offer loans to companies in all stages of their life cycle and the distribution of company age is relatively uniform.

“[Alternative small business lending] is creating a lot of economic activity,” Denis said. “We’re helping to create jobs, and we need to protect this tool. It’s a valuable resource for businesses…and this [report] demonstrates how important it is to the economy.”

IOU Planning for 25%-30% Originations Growth

May 29, 2018IOU Financial CEO Phil Marleau spoke confidently this afternoon on a public conference call to discuss the company’s first quarter performance. The company had a net income of $797,198 from the start of the year to March 31, which is notable because it produced a $995,085 loss during the same period last year.

On the call, Marleau said that the company plans to increase loan originations next year by 25 to 30 percent.

An analyst at TD Wealth asked if the company’s plan for a 25 to 30 percent increase in loan originations should produce a similar increase in earnings.

“We’re working on getting our numbers back on a growth trajectory,” Marleau said. [To do this…] we may need to increase marketing spend in order to increase the direct channel and the referral channel.”

Marleau explained that IOU Financial has three channels: the wholesale sales channel, which is responsible for the bulk of its business, the direct channel, which is driven by marketing, and the referral channel, which involves strategic partnerships with associations, payment processors, suppliers to small businesses and others. The company makes business loans of up to $300,000.

“We’re not going to lose sight of the bottom line,” Marleau said. “We’re not going to grow at the expense of profit.”

Another question came in asking what the status was on the company’s strategy of taking aggressive legal action against merchants that default on loans. President and Chief Operations Officer Robert Gloer answered this question by noting that once a lawsuit is filed against a merchant, it generally takes about a year for any money to be recovered. But the company has recovered money from defaults.

“We have started to see recoveries and we see that as a huge success,” Gloer said.

Another question dealt broadly with alternative financing in Canada as opposed to elsewhere, like the US. Marleau said that compared to the US, there is a lot less competition in Canada and that there are higher margins and usually fewer defaults.

IOU Financial is headquartered in Montreal and has an office in Kennesaw, GA.

Why Small Businesses Sought Financing in 2017, and Why They Were Denied

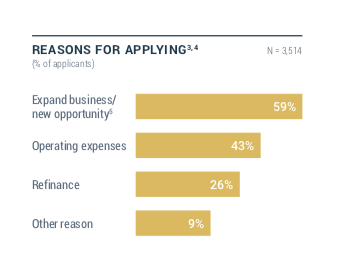

May 24, 2018 Nearly 60 percent of small businesses applied for financing in 2017 because they wanted to expand their business or pursue new opportunities, according to the latest report by the Federal Reserve. Forty-three percent of small businesses sought financing for operating expenses while 26 percent sought capital for refinancing. Nine percent had a different reason.

Nearly 60 percent of small businesses applied for financing in 2017 because they wanted to expand their business or pursue new opportunities, according to the latest report by the Federal Reserve. Forty-three percent of small businesses sought financing for operating expenses while 26 percent sought capital for refinancing. Nine percent had a different reason.

Of course, not all applications are funded. Forty-six percent of small businesses received all the financing they sought, 12 percent received most (more than 50 percent) of it, 20 percent received some (less than 50 percent) of the financing they desired and 23 percent were denied financing altogether.

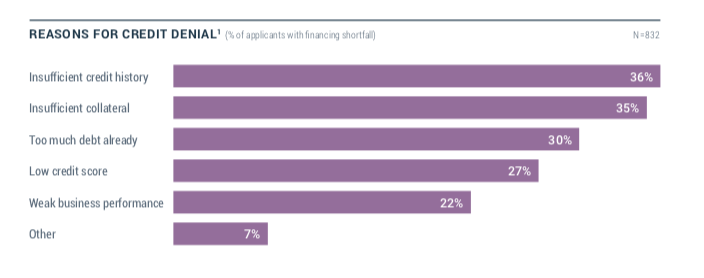

Of the reasons why merchants were denied funding, “Having insufficient credit history” ranked number one, according to the report. A very close second was “Having insufficient collateral,” followed by “Having too much debt already.” After that, in descending order, came “Low credit score,” “Weak business performance” and “Other.”

The “Having insufficient collateral” category does not apply for MCA financing, but the other categories do. According to Nick Gregory, founding partner at Central Diligence Group, which provides MCA underwriting services, “Having too much debt already” is perhaps the main reason why merchants seeking cash advances get declined.

“A lot of times the merchants are overleveraged,” Gregory said.

He explained that if a merchant also has something like two MCA arrangements (or positions) already, that merchant likely has taken on too many contractual obligations which will often be a reason to decline the application. In Gregory’s experience, another common reason for declining an MCA financing application is “Weak business performance.”

Contradictory to the Federal Reserve report’s top reason for denying financing to a small business borrower, Gregory said that “Having insufficient credit history” is seldom a reason to deny MCA financing. This disconnect likely comes from the fact that the report includes all types of small business financing, with MCA accounting for just seven percent. The number maybe seem small, but it continues to increase while small business applications for factoring have decreased.