Less Than Perfect — New State Regulations

You could call California’s new disclosure law the “Son-in-Law Act.” It’s not what you’d hoped for—but it’ll have to do.

That’s pretty much the reaction of many in the alternative lending community to the recently enacted legislation, known as SB-1235, which Governor Jerry Brown signed into law in October. Aimed squarely at nonbank, commercial-finance companies, the law—which passed the California Legislature, 28-6 in the Senate and 72-3 in the Assembly, with bipartisan support—made the Golden State the first in the nation to adopt a consumer style, truth-in-lending act for commercial loans.

The law, which takes effect on Jan. 1, 2019, requires the providers of financial products to disclose fully the terms of small-business loans as well as other types of funding products, including equipment leasing, factoring, and merchant cash advances, or MCAs.

The financial disclosure law exempts depository institutions—such as banks and credit unions—as well as loans above $500,000. It also names the Department of Business Oversight (DBO) as the rulemaking and enforcement authority. Before a commercial financing can be concluded, the new law requires the following disclosures:

The financial disclosure law exempts depository institutions—such as banks and credit unions—as well as loans above $500,000. It also names the Department of Business Oversight (DBO) as the rulemaking and enforcement authority. Before a commercial financing can be concluded, the new law requires the following disclosures:

(1) An amount financed.

(2) The total dollar cost.

(3) The term or estimated term.

(4) The method, frequency, and amount of payments.

(5) A description of prepayment policies.

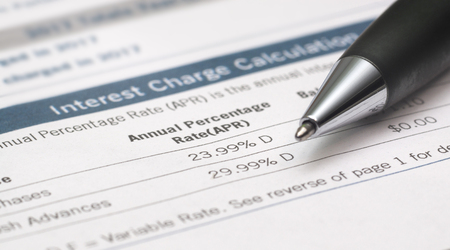

(6) The total cost of the financing expressed as an annualized rate.

The law is being hailed as a breakthrough by a broad range of interested parties in California—including nonprofits, consumer groups, and small-business organizations such as the National Federation of Independent Business. “SB-1235 takes our membership in the direction towards fairness, transparency, and predictability when making financial decisions,” says John Kabateck, state director for NFIB, which represents some 20,000 privately held California businesses.

“What our members want,” Kabateck adds, “is to create jobs, support their communities, and pursue entrepreneurial dreams without getting mired in a loan or financial structure they know nothing about.”

Backers of the law, reports Bloomberg Law, also included such financial technology companies as consumer lenders Funding Circle, LendingClub, Prosper, and SoFi.

But a significant segment of the nonbank commercial lending community has reservations about the California law, particularly the requirement that financings be expressed by an annualized interest rate (which is different from an annual percentage rate, or APR). “Taking consumer disclosure and annualized metrics and plopping them on top of commercial lending products is bad public policy,” argues P.J. Hoffman, director of regulatory affairs at the Electronic Transactions Association.

The ETA is a Washington, D.C.-based trade group representing nearly 500 payments technology companies worldwide, including such recognizable names as American Express, Visa and MasterCard, PayPal and Capital One. “If you took out the annualized rate,” says ETA’s Hoffman, “we think the bill could have been a real victory for transparency.”

The ETA is a Washington, D.C.-based trade group representing nearly 500 payments technology companies worldwide, including such recognizable names as American Express, Visa and MasterCard, PayPal and Capital One. “If you took out the annualized rate,” says ETA’s Hoffman, “we think the bill could have been a real victory for transparency.”

California’s legislation is taking place against a backdrop of a balkanized and fragmented regulatory system governing alternative commercial lenders and the fintech industry. This was recognized recently by the U.S. Treasury Department in a recently issued report entitled, “A Financial System That Creates Economic Opportunities: Nonbank Financials, Fintech, and Innovation.” In a key recommendation, the Treasury report called on the states to harmonize their regulatory systems.

As laudable as California’s effort to ensure greater transparency in commercial lending might be, it’s adding to the patchwork quilt of regulation at the state level, says Cornelius Hurley, a Boston University law professor and executive director of the Online Lending Policy Institute. “Now it’s every regulator for himself or herself,” he says.

Hurley is collaborating with Jason Oxman, executive director of ETA, Oklahoma University law professor Christopher Odinet, and others from the online-lending industry, the legal profession, and academia to form a task force to monitor the progress of regulatory harmonization.

For now, though, all eyes are on California to see what finally emerges as that state’s new disclosure law undergoes a rulemaking process at the DBO. Hoffman and others from industry contend that short-term, commercial financings are a completely different animal from consumer loans and are hoping the DBO won’t squeeze both into the same box.

Steve Denis, executive director of the Small Business Finance Association, which represents such alternative financial firms as Rapid Advance, Strategic Funding and Fora Financial, is not a big fan of SB-1235 but gives kudos to California solons—especially state Sen. Steve Glazer, a Democrat representing the Bay Area who sponsored the disclosure bill—for listening to all sides in the controversy. “Now, the DBO will have a comment period and our industry will be able to weigh in,” he notes.

While an annualized rate is a good measuring tool for longer-term, fixed-rate borrowings such as mortgages, credit cards and auto loans, many in the small-business financing community say, it’s not a great fit for commercial products. Rather than being used for purchasing consumer goods, travel and entertainment, the major function of business loans are to generate revenue.

A September, 2017, study of 750 small-business owners by Edelman Intelligence, which was commissioned by several trade groups including ETA and SBFA, found that the top three reasons businesses sought out loans were “location expansion” (50%), “managing cash flow” (45%) and “equipment purchases” (43%).

The proper metric to be employed for such expenditures, Hoffman says, should be the “total cost of capital.” In a broadsheet, Hoffman’s trade group makes this comparison between the total cost of capital of two loans, both for $10,000.

Loan A for $10,000 is modeled on a typical consumer borrowing. It’s a five-year note carrying an annual percentage rate of 19%—about the same interest rate as many credit cards—with a fixed monthly payment of $259.41. At the end of five years, the debtor will have repaid the $10,000 loan plus $5,564 in borrowing costs. The latter figure is the total cost of capital.

Compare that with Loan B. Also for $10,000, it’s a six month loan paid down in monthly payments of $1,915.67. The APR is 59%, slightly more than three times the APR of Loan A. Yet the total cost of capital is $1,500, a total cost of capital which is $4,064.33 less than that of Loan A.

Meanwhile, Hoffman notes, the business opting for Loan B is putting the money to work. He proposes the example of an Irish pub in San Francisco where the owner is expecting outsized demand over the upcoming St. Patrick’s Day. In the run-up to the bibulous, March 17 holiday, the pub’s owner contracts for a $10,000 merchant cash advance, agreeing to a $1,000 fee.

Once secured, the money is spent stocking up on Guinness, Harp and Jameson’s Irish whiskey, among other potent potables. To handle the anticipated crush, the proprietor might also hire temporary bartenders.

When St. Patrick’s Day finally rolls around—thanks to the bulked-up inventory and extra help—the barkeep rakes in $100,000 and, soon afterwards, forwards the funding provider a grand total of $11,000 in receivables. The example of the pub-owner’s ability to parlay a short-term financing into a big payday illustrates that “commercial products—where the borrower is looking for a return on investment—are significantly different from consumer loans,” Hoffman says.

SBFA’s Denis observes that financial products like merchant cash advances are structured so that the provider of capital receives a percentage of the business’s daily or weekly receivables. Not only does that not lend itself easily to an annualized rate but, if the food truck, beautician, or apothecary has a bad day at the office, so does the funding provider. “It’s almost like the funding provider is taking a ride” with the customer, says Denis.

SBFA’s Denis observes that financial products like merchant cash advances are structured so that the provider of capital receives a percentage of the business’s daily or weekly receivables. Not only does that not lend itself easily to an annualized rate but, if the food truck, beautician, or apothecary has a bad day at the office, so does the funding provider. “It’s almost like the funding provider is taking a ride” with the customer, says Denis.

Consider a cash advance made to a restaurant, for instance, that needs to remodel in order to retain customers. “An MCA is the purchase of future receivables,” Denis remarks, “and if the restaurant goes out of business— and there are no receivables—you’re out of luck.”

Still, the alternative commercial-lending industry is not speaking with one voice. The Innovative Lending Platform Association—which counts commercial lenders OnDeck, Kabbage and Lendio, among other leading fintech lenders, as members—initially opposed the bill, but then turned “neutral,” reports Scott Stewart, chief executive of ILPA. “We felt there were some problems with the language but are in favor of disclosure,” Stewart says.

The organization would like to see DBO’s final rules resemble the company’s model disclosure initiative, a “capital comparison tool” known as “SMART Box.” SMART is an acronym for Straightforward Metrics Around Rate and Total Cost—which is explained in detail on the organization’s website, onlinelending.org.

But Kabbage, a member of ILPA, appears to have gone its own way. Sam Taussig, head of global policy at Atlanta-based financial technology company Kabbage told deBanked that the company “is happy with the result (of the California law) and is working with DBO on defining the specific terms.”

Others like National Funding, a San Diego-based alternative lender and the sixth-largest alternative-funding provider to small businesses in the U.S., sat out the legislative battle in Sacramento. David Gilbert, founder and president of the company, which boasted $94.5 million in revenues in 2017, says he had no real objection to the legislation. Like everyone else, he is waiting to see what DBO’s rules look like.

“It’s always good to give more rather than less information,” he told deBanked in a telephone interview. “We still don’t know all the details or the format that (DBO officials) want. All we can do is wait. But it doesn’t change this business. After the car business was required to disclose the full cost of motor vehicles,” Gilbert adds, “people still bought cars. There’s nothing here that will hinder us.”

With its panoply of disclosure requirements on business lenders and other providers of financial services, California has broken new legal ground, notes Odinet, the OU law professor, who’s an expert on alternative lending and financial technology. “Not many states or the federal government have gotten involved in the area of small business credit,” he says. “In the past, truth-in-lending laws addressing predatory activities were aimed primarily at consumers.”

The financial-disclosure legislation grew out of a confluence of events: Allegations in the press and from consumer activists of predatory lending, increasing contraction both in the ranks of independent and community banks as well as their growing reluctance to make small-business loans of less than $250,000, and the rise of alternative lenders doing business on the Internet.

In addition, there emerged a consensus that many small businesses have more in common with consumers than with Corporate America. Rather than being managed by savvy and sophisticated entrepreneurs in Silicon Valley with a Stanford pedigree, many small businesses consist of “a man or a woman working out of their van, at a Starbucks, or behind a little desk in their kitchen,” law professor Odinet says. “They may know their business really well, but they’re not really in a position to understand complicated financial terms.”

The average small-business owner belonging to NFIB in California, reports Kabateck, has $350,000 in annual sales and manages from five to nine employees. For this cohort—many of whom are subject to myriad marketing efforts by Internet-based lenders offering products with wildly different terms—the added transparency should prove beneficial. “Unlike big businesses, many of them don’t have the resources to fully understand their financial standing,” Kabateck says. “The last thing they want is to get steeped in more red ink or—even worse—have the wool pulled over their eyes.”

California’s disclosure law is also shaping up as a harbinger—and perhaps even a template—for more states to adopt truth-in-lending laws for small-business borrowers. “California is the 800-lb. gorilla and it could be a model for the rest of the country,” says law professor Hurley. “Just as it has taken the lead on the control of auto emissions and combating climate change, California is taking the lead for the better on financial regulation. Other states may or may not follow.”

California’s disclosure law is also shaping up as a harbinger—and perhaps even a template—for more states to adopt truth-in-lending laws for small-business borrowers. “California is the 800-lb. gorilla and it could be a model for the rest of the country,” says law professor Hurley. “Just as it has taken the lead on the control of auto emissions and combating climate change, California is taking the lead for the better on financial regulation. Other states may or may not follow.”

Reflecting the Golden State’s influence, a truth-in-lending bill with similarities to California’s, known as SB-2262, recently cleared the state senate in the New Jersey Legislature and is on its way to the lower chamber. SBFA’s Denis says that the states of New York and Illinois are also considering versions of a commercial truth-in-lending act.

But the fact that these disclosure laws are emanating out of Democratic states like California, New Jersey, Illinois and New York has more to do with their size and the structure of the states’ Legislatures than whether they are politically liberal or conservative. “The bigger states have fulltime legislators,” Denis notes, “and they also have bigger staffs. That’s what makes them the breeding ground for these things.”

Buried in Appendix B of Treasury’s report on nonbank financials, fintechs and innovation is the recommendation that, to build a 21st century economy, the 50 states should harmonize and modernize their regulatory systems within three years. If the states fail to act, Treasury’s report calls on Congress to take action.

The triumvirate of Hurley, Oxman and Odinet report, meanwhile, that they are forming a task force and, with the tentative blessing of Treasury officials, are volunteering to monitor the states’ progress. “I think we have an opportunity as independent representatives to help state regulators and legislators understand what they can do to promote innovation in financial services,” ETA’s Oxman asserts.

The ETA is a lobbying organization, Oxman acknowledges, but he sees his role—and the task force’s role—as one of reporting and education. He expects to be meeting soon with representatives of the Conference of State Bank Supervisors (CSBS), the Washington, D.C.-based organization representing regulators of state chartered banks. It is also the No. 1 regulator of nonbanks and fintechs. “They are the voice of state financial regulators,” Oxman says, “and they would be an important partner in anything we do.”

The ETA is a lobbying organization, Oxman acknowledges, but he sees his role—and the task force’s role—as one of reporting and education. He expects to be meeting soon with representatives of the Conference of State Bank Supervisors (CSBS), the Washington, D.C.-based organization representing regulators of state chartered banks. It is also the No. 1 regulator of nonbanks and fintechs. “They are the voice of state financial regulators,” Oxman says, “and they would be an important partner in anything we do.”

Margaret Liu, general counsel at CSBS, had high praise for Treasury’s hard work and seriousness of purpose in compiling its 200-plus page report and lauded the quality of its research and analysis. But Liu noted that the conference was already deeply engaged in a program of its own, which predates Treasury’s report.

Known as “Vision 2020,” the program’s goals, as articulated by Texas Banking Commissioner Charles Cooper, are for state banking regulators to “transform the licensing process, harmonize supervision, engage fintech companies, assist state banking departments, make it easier for banks to provide services to non-banks, and make supervision more efficient for third parties.”

While CSBS has signaled its willingness to cooperate with Treasury, the conference nonetheless remains hostile to the agency’s recommendation, also found in the fintech report, that the Office of the Comptroller of the Currency issue a “special purpose national bank charter” for fintechs. So vehemently opposed are state bank regulators to the idea that in late October the conference joined the New York State Banking Department in re-filing a suit in federal court to enjoin the OCC, which is a division of Treasury, from issuing such a charter.

Among other things, CSBS’s lawsuit charges that “Congress has not granted the OCC authority to award bank charters to nonbanks.”

Previously, a similar lawsuit was tossed out of court because, a judge ruled, the case was not yet “ripe.” Since no special purpose charters had actually been issued, the judge ruled, the legal action was deemed premature. That the conference would again file suit when no fintech has yet applied for a special purpose national bank charter— much less had one approved—is baffling to many in the legal community.

“I suspect the lawsuit won’t go anywhere” because ripeness remains a sticking point, reckons law professor Odinet. “And there’s no charter pending,” he adds, in large part because of the lawsuit. “A lot of people are signing up to go second,” he adds, “but nobody wants to go first.”

Treasury’s recommendation that states harmonize their regulatory systems overseeing fintechs in three years or face Congressional action also seems less than jolting, says Ross K. Baker, a distinguished professor of political science at Rutgers University and an expert on Congress. He told deBanked that the language in Treasury’s document sounded aspirational but lacked any real force.

“Usually,” he says, such as a statement “would be accompanied by incentives to do something. This is a kind of a hopeful urging. But I don’t see any club behind the back,” he went on. “It seems to be a gentle nudging, which of course they (the states) are perfectly able to ignore. It’s desirable and probably good public policy that states should have a nationwide system, but it doesn’t say Congress should provide funds for states to harmonize their laws.

“When the Feds issue a mandate to the states,” Baker added, “they usually accompany it with some kind of sweetener or sanction. For example, in the first energy crisis back in 1973, Congress tied highway funds to the requirement (for states) to lower the speed limit to 55 miles per hour. But in this case, they don’t do either.”

Last modified: December 22, 2018