Business Lending

Democrats Call for Interest-Free Loans for Small Businesses Affected by Coronavirus

March 2, 2020 The leaders of the Democratic Party in the Senate and House, Chuck Schumer and Nancy Pelosi, respectively, have released a joint statement outlining their perspective on providing emergency funding to combat the coronavirus, otherwise known as covid-19. Among the provisions listed is a demand that “interest-free loans are made available for small businesses impacted by the outbreak.”

The leaders of the Democratic Party in the Senate and House, Chuck Schumer and Nancy Pelosi, respectively, have released a joint statement outlining their perspective on providing emergency funding to combat the coronavirus, otherwise known as covid-19. Among the provisions listed is a demand that “interest-free loans are made available for small businesses impacted by the outbreak.”

The statement comes at a point when the government has yet to confirm the amount of funds dedicated to treating and preparing against covid-19. Schumer has proposed devoting $8 billion, and House Minority Leader Kevin McCarthy has said that even $2 billion would be too little, opting instead for $4 billion. McCarthy has agreed with the Democrat leaders, saying that emergency funds should be not be stolen or transferred from other funds or emergency allotments. This position goes up against President Trump’s request for $1.25 billion from various existing funds, including $535 million from the Ebola preparedness fund.

Republican Senator Tom Cole expressed his uncertainty regarding the request, saying that “I just don’t think we should be penny-wise and pound-foolish on that.”

As well as calling for interest-free loans, the statement requests assurances that Trump will use the funds purely to fight covid-19 and other infectious diseases, that eventual vaccines will be available and affordable for all, and that state and local authorities will be reimbursed for costs incurred while assisting the federal response.

It is unsure whether or not these loans will actually come into play. While there does appear to be bipartisan cooperation within the House and Senate, the government seems to only have begun taking the virus seriously this week after it spread from China to Iran and Italy, and the first infection from an unknown source in America was diagnosed in California.

“We’re coming close to a bipartisan agreement in the Congress as to how we can go forward with a number that is a good start,” Pelosi told reporters in her weekly press conference. “We don’t know how much we will need. Hopefully, not so much more because prevention will work. But nonetheless, we have to be ready to do what we need to do.”

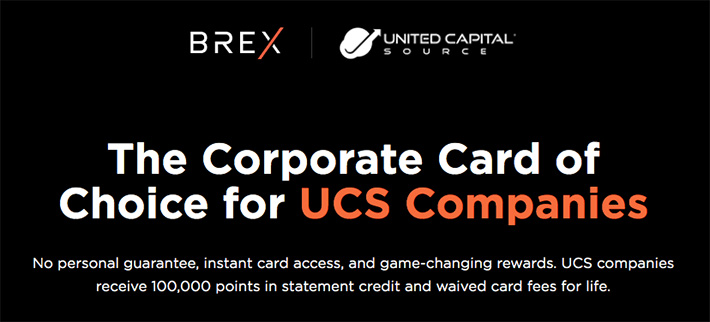

United Capital Source Partners with Brex to Offer Deal on Card

February 21, 2020U nited Capital Source has partnered with Brex on a deal that will see UCS customers receive bonuses upon sign-up for a Brex Corporate Card. Such rewards include 100,000 points in statement credit and waived card fees for life.

nited Capital Source has partnered with Brex on a deal that will see UCS customers receive bonuses upon sign-up for a Brex Corporate Card. Such rewards include 100,000 points in statement credit and waived card fees for life.

“We really wanted to start to offer business credit cards to our clientele. We believe that as we’re helping people solve their lending or funding issues, it’s also helpful to solve any problems that they face when running their day-to-day business,” UCS Founder and CEO Jared Weitz told deBanked in a call. “The key point that we really love about Brex which we’re offering to our clients is a 60-day, no-interest float on expenses. And that’s really helpful for folks when you’re making weekly and bi-weekly payrolls, when you’re purchasing inventory, and when you have folks that pay you every 30 or 45 days.”

The news comes as companies from various backgrounds are beginning to offer debit, credit, and charge cards. Apple, BlueVine, and challenger banks such as N26 and Varo are now all offering cards of some kind to their customers.

In Weitz’s view, this is the next step for the industry. With tech becoming more and more ingrained in finance, the convergence between the two fields is inevitable and ultimately beneficial for brokers.

“They’re already doing it on the personal side. And I think that once these tech-enabled companies start to get business data on their clients’ trends in their business account, they’ll be able to offer other products to them as well. For me, as a broker, if someone says, ‘Hey, does that make you nervous?,’ honestly, I don’t believe so. Because I think it opens up the sources for me to send deals to … I’m not a lender, so I’m not competing against them. I’m someone that would send them business. So when I look at them, I say this is just a new potential partner for me, a new opportunity.”

CAN Capital Brings On Edward Dietz as Chief Compliance Officer & General Counsel

February 5, 2020 CAN Capital is continuing its executive hiring spree into 2020 with the news that it has brought on Edward Dietz as its latest Chief Compliance Officer and General Counsel. After providing legal expertise to Marlin Business Services Corporation for nine years and working as an associate for two law firms in Wisconsin and Pennsylvania previous to this, Dietz will oversee CAN’s compliance with all federal and state lending, banking, and securities laws.

CAN Capital is continuing its executive hiring spree into 2020 with the news that it has brought on Edward Dietz as its latest Chief Compliance Officer and General Counsel. After providing legal expertise to Marlin Business Services Corporation for nine years and working as an associate for two law firms in Wisconsin and Pennsylvania previous to this, Dietz will oversee CAN’s compliance with all federal and state lending, banking, and securities laws.

“Having worked with Ed and knowing his skill set and the many intangibles that he brings to CAN, I feel fortunate that he’s leading our legal and compliance efforts,” noted CEO Edward Siciliano in a statement. “Ed’s just what we needed as we position CAN for growth and to lead a new era of small business lending.”

Having graduated from the University of Michigan Law School in 2004, Dietz has nearly two decades of legal experience.

Speaking on the news, Dietz said that he “could not be more excited to join a company and a team that believes so deeply that its people and its culture are the keys to harnessing the company’s growth potential.”

Kabbage Introduces Customized Short Term Loans

February 4, 2020 Today Kabbage, the Atlanta-based fintech company that has been funding businesses since 2009, announced its latest product: customized short-term loans that are a result of the combination of Kabbage Payments and Kabbage Funding.

Today Kabbage, the Atlanta-based fintech company that has been funding businesses since 2009, announced its latest product: customized short-term loans that are a result of the combination of Kabbage Payments and Kabbage Funding.

The loans, which run for the length of 3-45 days, are best suited to those businesses who need funding to cover issues in cash flow caused by the unpredictability of revenue, says Kabbage’s Head of Income Products Abraham Williams. “Rent and payroll are on set days every month, but getting paid is variable. We’ve done loans for 6, 12, and 18 months, and we’ve seen that people pay those off sooner, so we saw a need to have a short-term loan to fill gaps in cash flow.”

The terms of such loans will be decided upon by making use of the aggregate data that Kabbage has access to. With its customers providing a number of data points, such as their Amazon account, banking details, payment processes, and social media accounts, Kabbage is in “a really unique position because of the way that we make decisions on loans for small businesses,” notes Williams. “We can really see a very complete picture of a business, which can be different than how other people are essentially underwriting and assessing risk for loans.”

Two options are available for repayment: a traditional balloon payment to be paid at the end of the 45-day period, or a percentage of each sale made using Kabbage Payments going towards repayment. The latter of these provides more flexibility, with merchants being able to choose the percentage of each sale that is to go toward Kabbage and, as well as this, the fee attached to the Kabbage Payments option is smaller.

With the fee’s amount and terms being dictated by aggregated data, Kabbage is describing them as “dynamic,” providing individualized offers. Fees begin at 0.1% with the minimum amount to be borrowed being $500 and the maximum set at 10% of a merchant’s available line of credit for the short-term.

Goldman Sachs-Amazon Deal to Offer Small Business Loans in the Works

February 3, 2020

Tech giant Amazon is reportedly in talks with Goldman Sachs to offer business loans to those small and medium sized merchants operating on its marketplace, according to sources that the FT describes as “two people briefed on the discussions with the online retailer.” One of these sources said that it could launch as soon as March.

The news comes after CEO David Soloman spoke at the bank’s Investor Day recently, explaining that Goldman would be pursuing a “banking-as-a-service” model this year that would see the bank white labeling their products for third parties to use. As well as this, Solomon commented on a shareholders call last week that the bank is seeking to increase revenues from new channels such as consumer banking and wealth management.

One such channel is Goldman’s partnership with Apple last summer that saw the launch of Apple Card, a credit card solely available to Apple’s +100 million users in the US. The card’s launch was lauded by Solomon; and according to Business Insider, cardholders had $736 million in loan balances by the end of September, one month after the card was released to the public.

The Apple and Amazon deals highlight how Wall Street banks are employing and partnering with Big Tech to leverage advantage over fintechs, and ultimately gain access into markets that are historically not domains of the uber rich. Traditionally a bank that catered to elites, Goldman Sachs has been edging its way into consumer and small business banking ever since the launch of Marcus, its personal banking platform.

Amazon has been offering loans to merchants on its platform since 2011, using algorithms to determine which sellers would be best positioned to receive and repay a loan. Having previously partnered with Bank of America to finance such loans, the terms of these were for 12 months or less, with amounts funded ranging from $1,000 to $750,000. According to the FT, Amazon had $863 million in outstanding SMB loans on its balance sheet as of the end of 2019.

The digital nature of Amazon’s marketplace would accommodate Goldman Sachs’ neglect of brick-and-mortars stores, which have historically been a waypoint for small- and medium-sized businesses seeking finance.

LendIt Chairman and Co-founder Peter Renton described Goldman’s progression in the fintech space as “impressive,” noting that the speed at which it has been operating isn’t to be overlooked: “I thought something like this would happen but not in such a short space of time. Apple Card was only six months ago.”

As well as this, Renton was wary of how expansive the deal would be, admitting skepticism of it being a large project for either company. Given how both Amazon and Goldman have shown themselves to be selective in who they provide financing for, this assessment may prove correct.

The Scoop Behind Sprout Funding’s Acquisition of Jet Capital

January 25, 2020 News from North Texas this month as Dallas-based Sprout Funding announced its acquisition of Jet Capital. The move comes as Sprout seeks to expand its technical operations.

News from North Texas this month as Dallas-based Sprout Funding announced its acquisition of Jet Capital. The move comes as Sprout seeks to expand its technical operations.

“Sprout built a reputation as a group that funds a lot of its own internal deals, and Jet had spent a lot of time, energy, and money on their tech platforms,” Sprout’s CEO and Founder Brad Woy told deBanked. “So while we were really good on the sales and marketing side, they seemed to be a little bit more advanced in their tech and reporting, and we brought those two things together.”

Almost all of Jet’s employees will be joining Sprout, with the exception of one person who chose to go their separate way following the merger.

Jet’s COO Allan Thompson spoke kindly of the purchase, saying in a statement that “There is a great cultural alignment in addition to the obvious benefits of combining our technology, processes and people. The result will provide increased capabilities for Sprout and opportunity for all of our customers and partners.”

The financial terms of the acquisition were not disclosed.

Quarterspot is Shifting Its Business Focus

January 22, 2020Last week, several industry insiders reported receiving an email from NY-based company Quarterspot that said their agreement had been terminated.

The contents stated that the company is “shifting its business focus and will no longer be originating loans, but will continue to service currently outstanding loans.”

deBanked has confirmed that to be true. More information may be reported as it becomes available.

deBanked CONNECT MIAMI 2020 Photos

January 21, 2020View a selection of deBanked CONNECT MIAMI photos here

View every official deBanked CONNECT MIAMI 2020 photo on facebook

Ready for deBanked’s biggest event of the year? Broker Fair returns to New York City on May 18th

REGISTER NOW BEFORE EARLY BIRD PRICING EXPIRES