Business Lending

Ready Capital Was The Biggest PPP Lender By Volume in Round 1 of PPP Funding

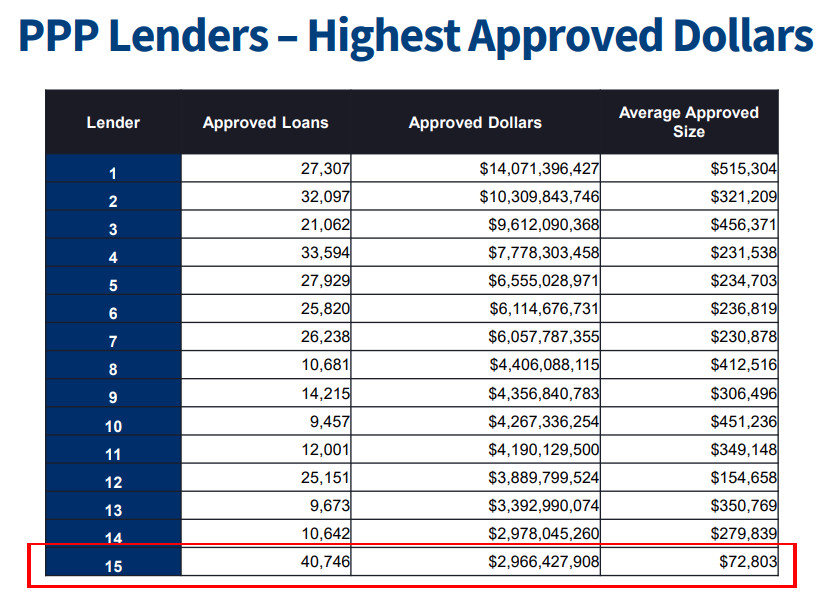

April 22, 2020 Ready Capital, a multi-strategy real estate finance company and one of the largest non-bank SBA lenders in the country, was the top PPP lender by loan volume in the country. Company CEO Thomas Capasse appeared on Fox Business yesterday and announced key statistics that aligned with data published by the SBA. By dollars, Ready Capital was the 15th largest PPP lender.

Ready Capital, a multi-strategy real estate finance company and one of the largest non-bank SBA lenders in the country, was the top PPP lender by loan volume in the country. Company CEO Thomas Capasse appeared on Fox Business yesterday and announced key statistics that aligned with data published by the SBA. By dollars, Ready Capital was the 15th largest PPP lender.

“As a leading non-bank, SBA lender, there’s 14 of us, we’re number two in terms of originations last year,” Capasse said on Fox Business, “we focused broadly, we don’t have deposit relationships, so we open our doors broadly to in particular the smaller mom and pop, the local deli, the pizzeria, the nail salon, so just in terms of the numbers, round one of the PPP, we approved 40,000 loans which is number one in the US, it was about $3 billion in total approvals. And our average balance was only $73,000 versus $230,000 for the average in round one.”

Among Ready Capital’s channels for acquiring PPP loan applications is Lendio, who reported consistent figures (a rough average of $80,000 per PPP loan facilitated), and high volume. Lendio has said on social media that they have been working with several partners, Ready Capital among them.

Ready Capital’s Capasse reasoned that their speed could probably be attributed to an affiliated fintech lender. “We are maybe more efficient than some of the banks because we have an affiliated fintech lender which is able to create online portals and processes to work in a more efficient manner and that enabled us to not only process these loans more efficiently but also to provide broad access to the program, to the smaller business owners.”

The company acquired Knight Capital, a small business finance provider, late last year.

United Capital Source CEO Jared Weitz Appeared on Fox News

April 21, 2020This week, Jared Weitz, CEO of United Capital Source, appeared on Fox News to talk about the PPP, EIDL, and small business lending. Video below:

Lendio Facilitated More Than 4% of All PPP Transactions

April 21, 2020 Lendio processed $5.7 billion of the $342 billion funded to businesses through the Paycheck Protection Program. With this amount going to just over 70,000 business owners, the Utah company facilitated 4.2% of the total 1.66 million deals through its platform.

Lendio processed $5.7 billion of the $342 billion funded to businesses through the Paycheck Protection Program. With this amount going to just over 70,000 business owners, the Utah company facilitated 4.2% of the total 1.66 million deals through its platform.

“The last few weeks have been an all-out brawl, from solving technical issues to deciphering legislation to managing expectations to dealing with incredible frustration,” Lendio CEO Brock Blake wrote in a recent Forbes article. “In this unprecedented time of crisis and need, there is nothing I would rather be doing than helping small business owners. My co-founder and I started a business on the idea that fueling small businesses fuels the American dream. Now the focus is on saving it.”

While not a direct lender, Lendio utilizes its platform to connect businesses owners with those lenders authorized by the SBA who can provide them with PPP money.

With the national average loan size of PPP money being $206,000, Lendio undercut this amount, instead having an average loan amount of less than $100,000. And with 28 million small businesses in the country, Blake is hoping to continue facilitating loans through this model of high quantity, smaller loan deals once more money is allocated to the program. Joining the chorus that is calling for additional PPP funds, Blake suggests that it could take nearly $850 billion in total to allow American small businesses to weather covid-19, as well as a rethinking of the program so that money can be moved quicker.

“There’s a lot we have learned over the past two weeks as a nation, as an industry, and as business owners. It’s important to take a closer look at the good, the bad, and the ugly of the Paycheck Protection Program, and most importantly, what needs to be done next … Much of the reason why I have been so vocal about the participation of fintech lenders is due to the fact that these lenders’ super power is processing smaller loan amounts at a higher volume. Community banks, on the other hand, specialize in processing large amounts at a lower volume; this is not what Main Street needs right now.

“The fact that fintech and non-bank lenders have been approved to participate in the distribution of PPP loans will make a world of difference if and when more funds are appropriated. Small businesses would have benefited more had these lenders been approved earlier in the process (most of them weren’t approved until the money had actually run out), but they can take heart knowing that more high-tech options will be available in the next phase.”

Small Business Group Advocates For Community Anchor Loan Program (CAP) In Wake Of PPP Wind Down and Possible Refresh

April 17, 2020 At last tally, more than 800,000 small business PPP applications have gone unfunded since the program reached its limit, many of which are genuine mom-and-pop shops that employ less than 25 people.

At last tally, more than 800,000 small business PPP applications have gone unfunded since the program reached its limit, many of which are genuine mom-and-pop shops that employ less than 25 people.

Congress is considering another round of additional PPP funding but Americans may be worrying that such funds will once again go into the hands of some of America’s largest chains. (44.5% of the $349B PPP funds went toward loans over $1 million)

Outspoken successful businessman Mark Cuban has proposed a solution, a lottery system next time around to improve the chances that smaller businesses get their share of the pie. While the public debates the merits of such an approach, one organization (the SBFA) is calling for something much more direct, a targeted fix via a Community Anchor Loan Program (CAP) that would appropriate $10 billion for businesses that were PPP-eligible for loans under $75,000 but did not receive funds.

Deployment of this capital under CAP can and should be administered by non-bank alternative lenders with proven success with this particular small business market, they say.

The proposal also calls for 25% of the funds to specifically be allocated for minority, women, and veteran-owned and agricultural businesses.

In a letter the SBFA submitted to Congress earlier this week, the organization said:

“Women and minority-owned businesses are historically smaller and employ fewer people and, in some communities, are under-banked without the established relationships required to secure a PPP loan. Small farms and agricultural businesses are important to communities and often have trouble qualifying for traditional financing.”

The Small Business Finance Association is a non-profit advocacy organization whose mission “is to take a leadership role in ensuring that small businesses have access to the capital they need to grow and thrive.”

Online Lenders Are Waiting On The Bench For The PPP To Be Refreshed

April 16, 2020 This week proved mixed for many fintech and non-bank lenders who received approval from the SBA to issue Paycheck Protection Program funds, only for the $349 billion allotted to the program to run dry almost immediately afterwards.

This week proved mixed for many fintech and non-bank lenders who received approval from the SBA to issue Paycheck Protection Program funds, only for the $349 billion allotted to the program to run dry almost immediately afterwards.

On Wednesday evening Senator Marco Rubio tweeted that the funds would run short, leaving at least 700,000 small businesses who applied in purgatory without PPP financing. But more money may be made available, as Treasury Secretary Steven Mnuchin said in a statement on Wednesday that “We urge Congress to appropriate additional funds for the Paycheck Protection Program – a critical and overwhelmingly bipartisan program – at which point we will once again be able to process loan applications, issue loan numbers, and protect millions more paychecks.”

BlueVine, OnDeck, Funding Circle, PayPal, Intuit, and Square were among the group of non-bank lenders who were recently approved. While unfortunately late to the party, these businesses will be well-positioned to quickly roll out funding once further PPP money is allocated.

“Millions of small businesses need relief more than ever right now, and providing that relief quickly and diligently is our top priority,” BlueVine CEO Eyal Lifshitz told deBanked. “While most PPP lenders have limited their efforts to existing customers, our aim is to support and protect all small businesses. Using our data and engineering resources, we want to ensure both existing customers and other small businesses seeking relief, are aware of and have access to PPP loans. We will remain a trusted advisor to small businesses and work to get fast capital solutions to those in need.”

Lifshitz’s comment echoes concerns that have plagued the SBA since the announcement of these funds: that its systems, and the processes of the banks it works with to issue this money, are outdated and insufficient to face a financial crisis of this magnitude and speed. Now weeks into the program, businesses are reporting a lack of communication from both their bank and the SBA; and, most importantly for many, no PPP funds in their accounts.

Clearbanc Launches Runway in Response to Covid-19

April 16, 2020 This month Clearbanc announced its latest product, Runway, in response to the impact of the novel coronavirus. Having historically served the needs of those businesses that are seeking funds for digital marketing, with Runway Clearbanc is expanding into capital for more generalized purposes in the face of covid-19.

This month Clearbanc announced its latest product, Runway, in response to the impact of the novel coronavirus. Having historically served the needs of those businesses that are seeking funds for digital marketing, with Runway Clearbanc is expanding into capital for more generalized purposes in the face of covid-19.

“All companies are concerned about one thing and that thing is runway: ‘how many months do I have left and how do we extend that?’ Clearbanc CEO Michele Romanow explained. “So we built this really cool product, where you can give us a little bit of information and we can show you how much runway you have today at your current economics, and then how much we could extend that runway.”

Open to e-commerce, D2C, and enterprise SaaS businesses, Runway has already begun issuing funds. Amounts begin at $10,000 and can run up to $10 million, with monthly cash injections being an option if Clearbanc deems it suitable. Fees range from 6-12% and funding is equity-free.

“These is no playbook for the current economic crisis and recovery, and every founder needs more insight and options to navigate this incredibly difficult time. In addition, venture capital is even harder to come by. Capital is the most important tool to sustain and grow a business, and is now needed more than ever.”

That’s All Folks? – The PPP Money Is Already Gone

April 15, 2020

Update 4/16/20: The SBA has put up an official statement on its website that says “The SBA is currently unable to accept new applications for the Paycheck Protection Program based on available appropriations funding. Similarly, we are unable to enroll new PPP lenders at this time.”

A number of fintech companies have just joined the Paycheck Protection Program, but they’re a tad late to the PPParty. On Twitter, Senator Marco Rubio, one of the co-sponsors of the CARES ACT that developed this program, confirmed the rumors that the well had run dry. “Sadly it appears #PPP will grind to a halt tonight as the limit on $ allocated to guarantee #PPPloans about to be hit.”

Sadly it appears #PPP will grind to a halt tonight as the limit on $ allocated to guarantee #PPPloans about to be hit.

Now 700000 small business applications are in limbo & no new loans will be made until the game of chicken in Congress ends & additional $ approved.

Inexcusable

— Marco Rubio (@marcorubio) April 15, 2020

Here’s the math

Congress approved $349 billion to guarantee #PPP

At 2pm today had over $300 billion in approved #PPPloans

Need $10 billion to cover fees & processing

When we reach $339 billion limit PPP will stop until they end with the ridiculous games & approve more funds

— Marco Rubio (@marcorubio) April 15, 2020

The SBA has often made reference to total funds “approved” when calculating its numbers rather than loaned out, so if you’re a business that has already been approved, then presumably funds have already been allocated for your business and you will still receive them. But if your application is pending, well it’s possible that funding may require additional congressional authorization. That however, as noted by Rubio’s remarks, will require some political compromise.

Update: 4/16 8 AM: Senator Rubio said on Fox Business that the PPP program was now frozen after having reached its limit and has stopped.

We’ll update this as more information becomes available.

Small Business Credit Survey Proves Itself to Be a Blast From the Past

April 15, 2020 Over a month into a nationwide lockdown and it can prove hard to remember what things were like before this. The ease of going to a restaurant and sitting in, the buzz of attending a packed concert, or even the unappreciated experience of not having to maintain six feet between yourself and whoever is beside you.

Over a month into a nationwide lockdown and it can prove hard to remember what things were like before this. The ease of going to a restaurant and sitting in, the buzz of attending a packed concert, or even the unappreciated experience of not having to maintain six feet between yourself and whoever is beside you.

As well as these small joys, for many small business owners the prospect of growth is a memory, as the latest Federal Reserve Small Business Credit Survey highlights. Released in March, the report is a summary of how small business owners acted and felt towards credit in 2019, as well as how they viewed their future in 2020.

While that’s certainly a grim reminder, the report featured an interesting question which appears prescient in the wake of the impacts of covid-19. “What actions would your business take in response to a 2-month revenue loss” was put to the 5,514 respondents, which were composed of owners of businesses that employed between 1 and 499 employees (coincidentally the same range for PPP loan eligibility). And the answers highlight the extent of the trouble which many small business owners currently find themselves in.

33% said they would lay off employees, 34% reported that they would rely on debt, and just 37% stated that they would reduce salaries of the owner(s) or employees. As well as these hypothetical decisions, 17% of respondents said they would shut down and 47% noted that they would use the owner’s personal funds to ride out the storm, worrying numbers given the current situation.

And while these responses prove eerie in light of what was to come, other answers reflect the optimism that 2019 yielded. 69% of firms expected revenue to increase in 2020, 44% expected their number of employees to grow, and 56% reported revenue growth on from 2018.

Outdated as the report is, it acts as an artifact of sorts: reminding the industry of what can come before the fall, and how even when things are good, many businesses are a few steps removed from serious trouble.