Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Two U.S. Senators Say ‘Not So Fast’ to OCC’s Plans for Limited Charter

January 10, 2017

Senator Sherrod Brown (D) and Jeffrey A. Merkley (D) both believe that the OCC does not possess the authority to grant the limited purpose charters it plans to move forward with. In a letter penned to Comptroller Thomas Curry on Monday, Brown and Merkley raise several concerns including that such charters would only blur the lines between banking and commerce, pointing out that an applicant need not necessarily be a fintech company to apply, nor need or want to accept deposits.

“As state banking supervisors have pointed out, because so many companies under an alternative charter would be exempt from the Bank Company Holding Act, nothing would ensure that both bank and currently impermissible non-bank activities were intermingled in one company, and that a commercial entity could not create or acquire an alternatively chartered company,” they write.

Brown and Merkley’s other concerns may be premature since the OCC is currently seeking information from the fintech industry on such issues in its official 13-question Request for Comment (found on the last pages of this document).

The full letter submitted to Comptroller Curry can be viewed here.

My Marketplace Lending 2017 Projections

January 8, 2017 LendIt co-founder Peter Renton has projected that there won’t be any new industry IPOs this year. While I don’t know if I’d say he’s wrong (a year is a long time), one thing that has changed since 2014 is a shift away from the “tech” label. When OnDeck went public, they positioned themselves as a technology company. Today, they more closely identify themselves as a non-bank commercial lender. Lending Club too was a “tech company.” Now they might be more appropriately characterized as an online consumer lender, especially since their competitors are traditional financial institutions like Discover Bank and Goldman Sachs. So the public markets in 2017 may not be ready for a tech company that can lend but they may be ready for a lending company that has tech. The difference is real.

LendIt co-founder Peter Renton has projected that there won’t be any new industry IPOs this year. While I don’t know if I’d say he’s wrong (a year is a long time), one thing that has changed since 2014 is a shift away from the “tech” label. When OnDeck went public, they positioned themselves as a technology company. Today, they more closely identify themselves as a non-bank commercial lender. Lending Club too was a “tech company.” Now they might be more appropriately characterized as an online consumer lender, especially since their competitors are traditional financial institutions like Discover Bank and Goldman Sachs. So the public markets in 2017 may not be ready for a tech company that can lend but they may be ready for a lending company that has tech. The difference is real.

On regulation, while a Trump presidency may mean that federal regulatory threats will subside, my projection is that the judiciary system will instead play a prominent role in 2017. Whether it’s state courts or federal courts, expect the rules of engagement in marketplace lending or merchant cash advance to become more clear than ever before.

I think it would be easy to predict consolidation in 2017, so more than that, I believe some companies will just wind down and others who arrived too late to the game will just move on to something else. That’s not necessarily a pessimistic outlook since this will give the more serious players a chance to flex their muscles and continue strong growth. This is a natural cycle in any industry that experiences a rapid growth phase.

There will be at least one black swan event. We don’t know what we don’t know.

Lastly, if you want to come up with your own predictions you should attend the 2017 LendIt Conference this March in NYC as it’s the best opportunity to take the temperature and size up the future. I have been to the last three annual LendIt USA conferences and in my opinion each has set the tone for the rest of the year.

You can get 15% off the registration price with Promo Code: Debanked17USA.

Merchant Cash Advance’s David and Goliath End an Era

January 5, 2017 Before there was Capify and CAN Capital, there was AmeriMerchant and AdvanceMe. Those are the original names of the two industry rivals whose history goes back more than 10 years. When I started working for an MCA company in 2006, I was taught two things, that AdvanceMe claimed to have a patent on merchant cash advance’s core feature and that AmeriMerchant’s CEO was leading the charge to have it invalidated. Back then, AdvanceMe had sued AmeriMerchant and several other companies for violating its automated payment patent and it was the biggest threat to the industry’s future at the time.

Before there was Capify and CAN Capital, there was AmeriMerchant and AdvanceMe. Those are the original names of the two industry rivals whose history goes back more than 10 years. When I started working for an MCA company in 2006, I was taught two things, that AdvanceMe claimed to have a patent on merchant cash advance’s core feature and that AmeriMerchant’s CEO was leading the charge to have it invalidated. Back then, AdvanceMe had sued AmeriMerchant and several other companies for violating its automated payment patent and it was the biggest threat to the industry’s future at the time.

A real life David and Goliath saga, it was only fitting that AmeriMerchant’s CEO was actually named David. His last name Goldin, he went on to win the lawsuit in such a big way, the story was featured in the New York Times. At that time in 2007, the Times quotes Goldin as saying, “It’s a victory against patent trolls. This has changed the landscape. The days of coming up with an obvious idea and patenting it and using legal extortion are over.”

With the patent invalidated, numerous entrepreneurs felt the coast was clear to start a merchant cash advance company, thus paving the way to become an industry that now originates more than $10 billion a year in funding to small businesses. AdvanceMe was a Goliath in that it held a virtual monopoly on MCA in the late 90s and early 2000s. They had such a huge head start on everyone, that they were still the largest MCA company in the US in 2014 (if you don’t count OnDeck which only does loans).

That era is coming to a close. AdvanceMe, today CAN Capital, suspended funding in late November of 2016 after internal issues were discovered, which resulted in mass layoffs and executive departures. And AmeriMerchant, today Capify, announced it is integrating its US operations with another industry rival, Strategic Funding Source (SFS), who will be managing all of their US customers going forward.

That era is coming to a close. AdvanceMe, today CAN Capital, suspended funding in late November of 2016 after internal issues were discovered, which resulted in mass layoffs and executive departures. And AmeriMerchant, today Capify, announced it is integrating its US operations with another industry rival, Strategic Funding Source (SFS), who will be managing all of their US customers going forward.

While CAN Capital’s ultimate fate is still yet to be determined, the end of Capify’s US presence is an M&A event, the first one of 2017. An insider at SFS said on a call that Capify’s international operations were not part of the deal in any way. Goldin will continue to run his company’s other offices such as Capify UK like normal. In the US however, more than twenty of Capify’s employees are being transitioned to work as SFS employees and to work from SFS’s office.

In the transaction’s announcement, Goldin is quoted as saying “we are very pleased to have put together a deal with Strategic Funding that will provide our customers a future source of important capital. As a company that shares our values of providing simple, transparent and responsible access to capital for small and mid-sized businesses, it was a logical transition.”

SFS, founded in 2006, and today one of the largest MCA funders in the nation, is a worthy successor. In a way, the more things in this industry change, the more things stay the same. As a testament to that, the antagonist of the 2007 NY Times story is Glenn Goldman, then the CEO of AdvanceMe and today the head of Credibly, another MCA competitor that also underwent a name change.

At the time, Goldman wrote to the Times, saying, “Although we feel vindicated that the court found clear infringement of our patent by each of the defendants, we respectfully disagree with the court’s findings on validity.”

Ironically, ACH is now the main payment mechanism for merchant cash advances, not split-processing, rendering the patent battle that took place a decade ago practically moot. It’s the end of an era.

My Three Year Anniversary of Investing on Lending Club’s Platform

January 3, 2017 It’s been three long years since the first month that I ever bought a Lending Club note and to commemorate the event, I decided to go back and see what I did and share what I’ve learned since then.

It’s been three long years since the first month that I ever bought a Lending Club note and to commemorate the event, I decided to go back and see what I did and share what I’ve learned since then.

In January 2014, I attempted to buy ten $25 notes for a total of $250, all of which were A and B-grade with 36 month maturities. Here’s what happened:

- Four of them paid off early

- Four of them are current and are just about to mature

- Two of the loans ended up not getting funded

So I actually only ended up getting $200 worth of notes and the results were great. But I didn’t stop there. I went on to buy more than $85,000 worth of Lending Club notes over the next two and a half years. The last note I ever bought was on June 8, 2016. If you’re wondering if I’ve made money, I have so far, but that still assumes a doomsday event doesn’t happen with the rest of my outstanding notes that will mature over the next few years.

Here are a few things I learned since the day I first started:

Reinvesting isn’t guaranteed

There is no guarantee that a similar new note will be available to replace one that just paid off. In the immediate post-Laplanche era, there were very few notes on the retail platform to buy and sometimes even none at all. Any number of major events could cause a situation like this to happen on a marketplace lending platform so you need to be prepared to manage idle cash should there be few or no suitable replacement notes.

Early payoffs can be very bad

This is related to reinvesting but can be bad all on its own. Lending Club charges retail investors a 1% penalty on outstanding principal whenever a borrower pays off their loan early (so long as the loan is 12 months old). Few people seem to be aware of this and it really makes no sense. Consider that as a retail investor you not only lose the interest you would make for the rest of the life of the loan on a good paying borrower, but you also get hit with a penalty on top of it even though you as the investor had nothing to do with the borrower’s decision. That sucks a lot. And potentially even worse, but plausible, what if there were no identical notes available to replace the ones lost to an early payoff? You lose three times.

Other platforms and banks are working against you

Banks like Discover and Goldman Sachs are actively working to steal Lending Club’s borrowers. And when they are successful, loans get paid off early, which hurts your investments. I’ve had nearly 1,000 of my borrowers pay off early on Lending Club for some reason or another already, so this is a major phenomenon.

Diversification isn’t just about the letter grades

Don’t put all your money in 1 note, but also don’t put all your money on 1 platform. Lending Club is still just a single company so you should only invest a small percentage of your investable assets on it. I have placed smaller experimental amounts on other platforms such as Prosper, StreetShares and Colonial Funding Network (Strategic Funding Source.) And yet, the bulk of my personal investments are actually in more traditional assets.

Holes in transparency

One of Lending Club’s biggest draws has been its transparency with investors but there’s still a lot of information that is withheld. When a borrower pays off early, investors aren’t told why or how it happened. Are borrowers really refinancing a credit card or are they taking the money and going to Vegas for the weekend? Investors don’t know and the true use of funds isn’t verified. Is the borrower broke? Lending Club focuses on a borrower’s credit profile, not on how much cash the borrower has in the bank, which could be $0 or negative. I’ve encountered plenty of investors that have argued that a borrower’s cash flow history is a non-factor or a burden on approval speed, but coming from a commercial financing background, I am still shocked that a consumer’s historical cash flow plays no role in getting a three-to-five year loan.

When a borrower stops paying, don’t expect to know why

A common theme in the collections notes of delinquent borrowers is the dreaded “Called. No answer,” line which can repeat for days, weeks, or months on end. Some borrowers will just stop paying and then never answer Lending Club’s calls again or they’ll ask that they “cease and desist” from making future calls. Was it financial hardship? You won’t always get the satisfaction of knowing, making it truly a numbers game.

This is a speculative investment

The value of your portfolio might not have volatile swings, but there are numerous risk factors that can impact performance. Only invest a small percentage of your investable assets.

It’s a nice investment option to have

Investing in notes backed by consumer loans is a great yield opportunity for retail investors in a low savings account rate environment. Despite the risks, retail investors don’t have many alternatives to earn a decent return outside of the stock market. Hopefully marketplace lending platforms don’t completely move away from retail investors.

deBanked’s Top 10 Most Read Stories of 2016

December 28, 2016

If 2015 was the year of the broker, well then 2016 was the year of readjusted expectations. The following are the top 10 most read stories of 2016 per our online analytics, some of which surprised even us. Either way, here’s what you read and shared on our website the most in 2016 in descending order:

10: Do Bank Statements Matter in Lending? Business Lenders and Consumer Lenders Disagree

A 2015 story, it was the 10th most read in 2016. One thing the lending revolution has taught us is that a borrower’s bank statements can mean everything or nothing at all.

9: Should I start an ISO with only $2,000?

Even though this was published two full years ago, it managed to be the 9th most read story of 2016. The short answer to this question is no, don’t start an ISO with such a small budget especially not in 2016 or 2017.

8: Lending Club Class Action Lawsuit Predicated on Madden v Midland Risk

A big story early in the year was Madden v Midland, and the impact an appellate court ruling could have on marketplace lenders who rely on chartered banks to make loans for them in 50 states. This particular post and related ones attracted a lot of readers in 2016.

7: Business Loan Brokers and MCA ISOs Call it Quits

For the first time ever, brokers and ISOs began to say farewell to an industry faced with oversaturation.

6: Merchant Cash Advance Accounting – A How To Guide

Published two full years ago, the merchant cash advance accounting guide managed to be the 6th most read article on deBanked in 2016. The article is meant for MCA funders bookkeeping, not for merchants who use merchant cash advances.

5: Lending Club Borrowers Are Paying Off Really Early – And There’s Something Weird About It

Lending Club’s loan borrowers pay off their loans early at a freakish level. I pondered this in a blog post in February and the trend has not changed. To date, I’ve had 975 borrowers pay off early, nearly double since the time this was published.

4: Platinum Rapid Funding Group Sets Annual Funding Record

An astounding amount of visitors were interested in Platinum Rapid Funding Group’s 2015 origination volume. An announcement that the company had originated $100 million in deals was the 4th most read story of 2016.

3: Merchant Cash Advance Definitely NOT a Loan, New York Judge Rules

Yet another post referencing Platinum Rapid Funding Group, was a decision issued in a New York trial court. In it, a judge opined at length about the nature of purchasing future receivables.

2: Shakeup at CAN Capital – CEO and 2 other Execs Put on Leave of Absence

Despite being less than a month old, this story on its own was the 2nd most read of 2016, technically followed by this one and this one, both also about CAN’s recent issues. We combined them into one story for the purpose of this list since they were all related to the same event.

1: The Closer – Meet the Yellowstone Capital Rep That Originated $47 Million in Deals Last Year

The #1 most read story on deBanked in 2016 was a profile about a salesman at Yellowstone Capital. Juan Monegro, who originated $47 million worth of deals in 2015, was also recently reported to have matched that number again in 2016.

Brief: The CFPB’s Unconstitutionality

December 28, 2016The Director of the consumer agency wields so much power that his authority actually violates Article II of the United States Constitution, according to the United States Court of Appeals for the District of Columbia Circuit which presided over PHH Corp v. CFPB. “In short, when measured in terms of unilateral power, the Director of the CFPB is the single most powerful official in the entire U.S. Government, other than the President,” the Court wrote. “Indeed, within his jurisdiction, the Director of the CFPB can be considered even more powerful than the President.”

Article II of the Constitution grants the President alone the authority to take care that the laws be faithfully executed. That means that Congress can’t even legally legislate another single individual to possess that amount of power even if they wanted to. But rather than order the dismantling of the CFPB, the Court suggested two remedies, either the director be overseen by the President of the United States or the single-directorship model be reconfigured to become a multi-member commission, a workaround that other executive agencies operate under.

Even though the agency is tasked to protect consumers, the Court recognized the potential for corruption when overseen by a single unaccountable person. “The CFPB’s concentration of enormous executive power in a single, unaccountable, unchecked Director not only departs from settled historical practice, but also poses a far greater risk of arbitrary decision-making and abuse of power, and a far greater threat to individual liberty, than does a multi-member independent agency,” the Court asserted.

Meanwhile, the CFPB has cast the decision aside as nonsense and has refused to comply, even going as far as to directly rebut it in another case shortly thereafter. In CFPB v. Intercept Corporation, the CFPB argued that the D.C. Circuit’s decision was “wrongly decided” and “not likely to withstand further review.” They’ve also asked the D.C. Circuit to rehear the case in part because they believe the decision “purports to override Congress’s explicit determination to create ‘an independent bureau’ to exercise regulatory and law enforcement authority in a particular segment of the economy.” The Court can simply deny to rehear the case.

One wild card to consider in this debate is that President-Elect Trump has pledged to repeal the Dodd-Frank Act, the law that created the CFPB to begin with. At the very least, Trump may feel it necessary to flex the power granted to him under Article II and subvert the directorship of the agency.

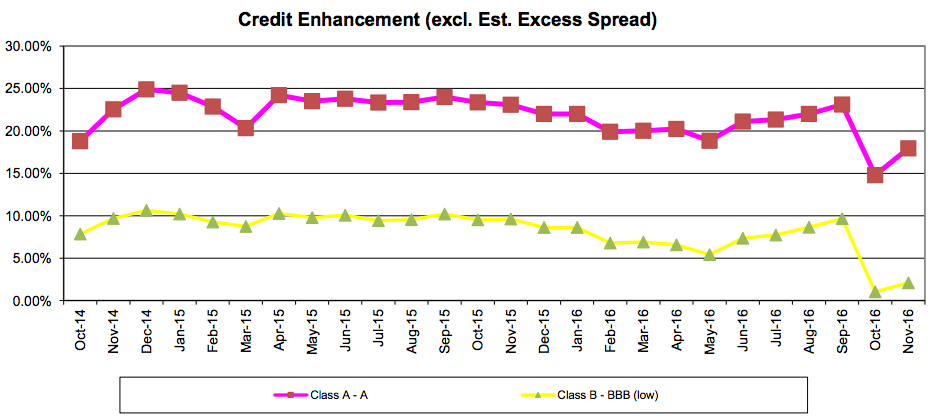

CAN Capital’s Collateral ‘Adjustment’

December 24, 2016Last month, CAN Capital disclosed that they had “self-identified that some assets were not performing as expected” on the same day that three of the company’s top executives were put on leave. Since then it’s been reported that a discrepancy arose when CAN’s old systems were not equipped to handle the shift from variable payment advances to fixed payment loans. This is notable given that CAN began doing fixed payment loans all the way back in April 2010.

The discrepancy found its way into CAN’s 2014 securitization. S&P Global Ratings recently reported on this that “there was a correction of previously misclassified assets that affected the results of the calculation of [the] adjusted performing asset balance” on CAN Capital Funding LLC Series 2014-1.

Ratings agency DBRS illustrates the collateral dip on CAN’s securitization once the classifications were reported correctly on Series 2014-1 below.

This is the first public glimpse into what CAN’s old systems got wrong and by how much.

The drop triggered a rapid amortization event, potentially causing liquidity issues for CAN, hence why new funding may be paused. The principal balance on the $200 million notes has dropped by nearly $70 million in the last two months, indicating big payouts.

The process to manage a rapid amortization event is described in the original DBRS ratings report. The implications aren’t good given that this appears to be brought on by misclassifying assets rather than a natural deterioration of loan performance.

Last week, CAN laid off nearly half of its employees as it tries to correct course.

Update: On December 25th, deBanked published a brief of a newly discovered lawsuit filed against CAN Capital on December 19th by an aggrieved shareholder alleging the company had failed to pay her a $150,000 settlement payment.

Broker Running Around Calling Himself a ‘Direct Lender’ Shut Down by CA Regulators

December 21, 2016A loan broker representing themselves to be a “direct lender,” was not a direct lender at all, according to witness testimony entered against Financial Services Enterprises DBA Pioneer Capital. The California Department of Business Oversight (DBO) noted in its case against Pioneer that “the evidence did not show that respondent actually funds loans itself, and did not include documentation of any loans actually consummated.”

The regulatory action, which was centered around whether or not the business loan broker was unlicensed in California ended unfavorably for Pioneer, with the DBO ordering the company to Desist and Refrain. You can read a good summary on LeasingNews by attorney Tom McCurnin: http://leasingnews.org/archives/Dec2016/12_21.htm#dbo