Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

“Predatory Lenders” Slammed as Bill to Ban Confessions of Judgment Nationwide Advances

November 14, 2019

(Bloomberg is majority owner of Bloomberg News parent Bloomberg LP)

Rep. Nydia Velázquez (D) celebrated the advancement of a bill on Thursday that aims to outlaw confessions of judgment (COJs) in commercial finance transactions nationwide. HR 3490, dubbed the Small Business Lending Fairness Act, made its way through the House Financial Services Committee on a vote of 31-23. The next step will be a floor vote.

Velázquez made direct references to a Bloomberg News story series published last year about “predatory lending” and a NY Times article about Taxi medallion loans as her basis for supporting it. Velázquez said that New York had become a breeding ground for “con artists” that relied on COJs to prey on mom-and-pop businesses. The congresswoman singled out New York because of recent taxi medallion loan outrage and the state’s alleged reputation as a “clearing house” for obtaining fast easy judgments against debtors nationwide. New York took a major step to change that practice earlier this year through a new law that only allows COJs to be filed in the state against New York residents. HR 3490 seeks to prevent them from being filed in every state, including New York.

Ironically then, the bill is at odds with the new New York law in that Velázquez’s bill, if it became federal law, would go so far as to prevent New York’s own courts from entering a COJ against New York’s own residents, if it resulted from a commercial finance transaction.

Ironically then, the bill is at odds with the new New York law in that Velázquez’s bill, if it became federal law, would go so far as to prevent New York’s own courts from entering a COJ against New York’s own residents, if it resulted from a commercial finance transaction.

While momentum in the House could be perceived as a partisan initiative unlikely to survive the Senate, the bill has in fact garnered a degree of Republican support, recently through Rep. Roger W. Marshall, a co-sponsor of the bill, and originally by Senator Marco Rubio who initially sparked the call to action in the Senate last year.

The Financial Svcs Committee approved my bill to end "Confessions of Judgment", contracts that allow for unfair, predatory small business loans & that have been linked to #taximedallion crisis in NYC.

On to the House floor!

Read More: https://t.co/xHaYnLKme4@NYTW @FSCDems

— Rep. Nydia Velazquez (@NydiaVelazquez) November 14, 2019

A co-author of the COJ-centric Bloomberg News stories was quick to take the credit for the advancement of Velázquez’s bill.

the bill was drafted in response to our series Sign Here to Lose Everythinghttps://t.co/lrfIW3P0yi

— Zeke Faux (@ZekeFaux) November 14, 2019

Brian Holloway, America’s #1 Most Requested Motivational Team Builder, to Speak at deBanked CONNECT Miami

November 13, 2019

Salespeople, are you ready for…

Total Market Domination?!?!

Stanford All-American, 5 time NFL All-Pro, and All-Star front line competitor Brian Holloway will be speaking at deBanked CONNECT Miami on January 16th, two weeks before the Super Bowl takes place just down the road. deBanked CONNECT is taking place at the Loews in South Beach. Last year’s event was completely SOLD OUT.

Stanford All-American, 5 time NFL All-Pro, and All-Star front line competitor Brian Holloway will be speaking at deBanked CONNECT Miami on January 16th, two weeks before the Super Bowl takes place just down the road. deBanked CONNECT is taking place at the Loews in South Beach. Last year’s event was completely SOLD OUT.

About Brian Holloway

The New England Patriots made a good decision in choosing Brian Holloway as a first-round draft pick, as he became the 6’7” powerhouse at the core of the 1985 New England Patriots Super Bowl team. In 1986, Brian Holloway was elected by his peers to forge a new direction in NFL policy, becoming the youngest Vice-President of the NFL Player’s Association at age 23. Brian Holloway retired from the NFL in 1992 after eight distinguished seasons with the Patriots and two with the Los Angeles Raiders.

Today, Brian Holloway is an international motivational speaker and renowned corporate trainer, mobilizing companies and organizations in search of peak productivity, helping them achieve new levels of excellence. He understands how to transform thinking within organizations and challenge the competitive spirit of diverse work teams. His Silicon Valley roots launched him beyond his Hall of Fame career in the NFL to become one of the most requested business intelligence consultants in America.

Today, Brian Holloway is an international motivational speaker and renowned corporate trainer, mobilizing companies and organizations in search of peak productivity, helping them achieve new levels of excellence. He understands how to transform thinking within organizations and challenge the competitive spirit of diverse work teams. His Silicon Valley roots launched him beyond his Hall of Fame career in the NFL to become one of the most requested business intelligence consultants in America.

He has traveled over 10,000,000 miles and been hired by over 279 Fortune 500 Companies, and now entering his 15th year working with Apple. Other clients include; HP, Exxon, Harvard Business School, Wal-Mart, Nike, ESPN, Verizon, Bank of America, Ford, Sprint, Cisco Systems, Honeywell, State Farm, AIG, Reebok, Daimler Chrysler, Best Buy, Wachovia Bank, and more.

Brian Holloway’s stories and case studies are scenes from his own life. Entertaining, motivating and instructional, Brian Holloway uses multi-media technology along with actual NFL game footage to showcase critical points on competitive excellence. These powerful, high-impact presentations have immediate take-home value for everyone — athlete and non-athlete alike.

Register below or visit www.debankedmiami.com

Costs, Losses Soar At StreetShares

November 12, 2019 StreetShares increased revenue by nearly 40% year-over-year, according to the company’s latest fiscal year 2019 filing, but costs soared and increased by almost 90%.

StreetShares increased revenue by nearly 40% year-over-year, according to the company’s latest fiscal year 2019 filing, but costs soared and increased by almost 90%.

StreetShares reported a staggering $12.3M loss on only $4.4M in revenue. That loss was much wider than the previous year’s loss of $6.5M on $3.2M in revenue.

Whereas startups may spend heavily on sales and marketing as they prioritize growth and scale, StreetShares’ primary cost, as in prior years, continues to be payroll. The company spent approximately $7 million in payroll and payroll taxes in fiscal year 2019.

The margin by which payroll exceeds revenue is increasing (157% in FY ’19 vs 144% in FY ’18). For comparison purposes, payroll expense makes up less than 25% of revenue for StreetShares rival IOU Financial.

StreetShares’ source of funds has shifted away from institutional investors and professional investors to retail investors. Retail investors only provided 43.89% of funds in FY ’18 but provided 86.72% of funds in FY ’19.

Retail investors, permissible under Regulation A, do not invest in individual loans but rather they lend money to StreetShares for which the company can use for lending or for “general corporate purposes” or “other products at the discretion of the company.” In return retail investors receive a fixed 5% annual return.

As of May 2019, the company reported that 80% of funds they lend out go to US veteran small businesses. A veteran small business is defined as “a company that is at least 25% owned by a veteran or military spouse or has a veteran or military spouse as the co-guarantor.”

Who Exactly Got Paid In Knight Capital’s Sale… And How Much? ($27.8M)

November 6, 2019

Update 11/7/19 9:05 AM: Ready Capital Corporation confirmed this morning that Knight Capital’s total sale price was $27.8M. $10M was in stock.

When Ready Capital Corporation acquired Knight Capital last week for $10 million in stock and an undisclosed amount of cash, questions abounded over who directly benefitted from the sale and how much cash was actually exchanged.

Documents later submitted by Ready Capital revealed that Knight Capital was owned by a San Jose, CA-fund named Len Co, LLC. Len Co began lending to Knight Capital in 2014 and later converted a large principal balance into a major equity investment in Knight in early 2018.

Several months later, Len Co’s primary creditor forced Len Co into Chapter 7. Shares in Knight, being a major asset of Len Co, became a talking point of that proceeding, ultimately propelling Knight into the hands of an eager buyer, Ready Capital Corporation.

The stock in the sale was therefore almost entirely paid out to the Estate of Len Co, LLC (640,205 of the 658,771 Ready Capital Corporation shares to be precise). This being the case was a reflection of the predicament Len Co was in, not necessarily that there was anything adverse about Knight.

On May 31, the bankruptcy court presiding over Len Co approved a proposed sale of Knight Capital to a confidential buyer for a grand total of $25 million, via $10 million in stock and a whopping $15 million in cash to be completed by December 31, 2019.

The buyer was identified as a publicly traded company. Assuming no better bids were received by Mid-August, the company would be sold for the $25 million under the terms offered to the publicly traded buyer. The court reaffirmed it on August 15th.

In October, Ready Capital Corporation announced that they had acquired 100% of Knight Capital in a deal for $10 million in stock and an undisclosed amount of cash.

Update: After this story was posted, Ready Capital confirmed on a morning earnings call that the sales price was slightly more than $25M and was finalized at $27.8M.

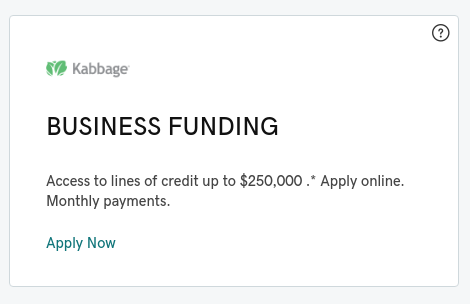

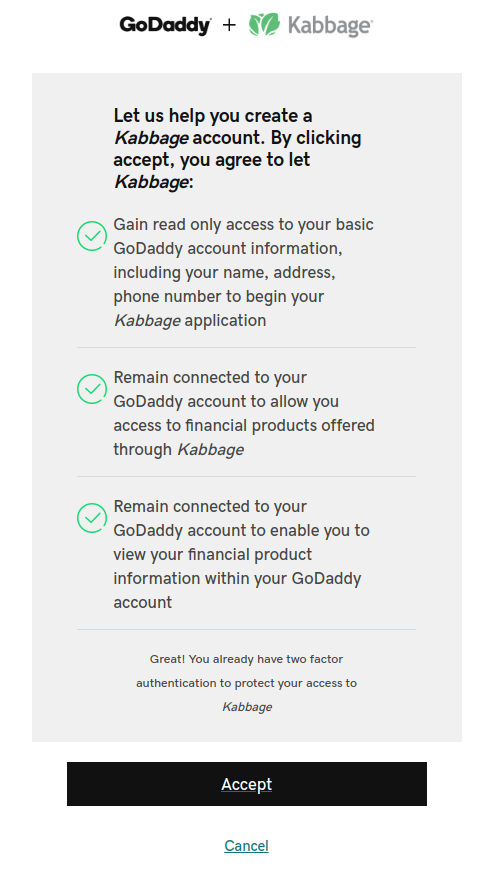

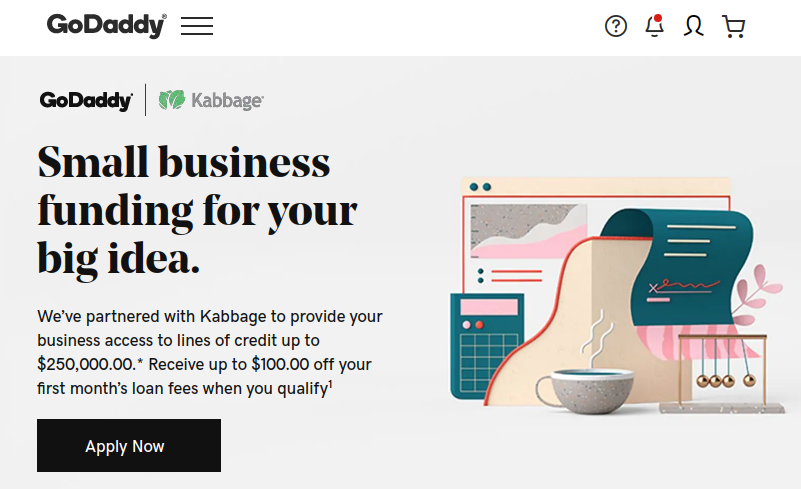

GoDaddy Now Offers Kabbage Business Lines of Credit To Its Customers

November 4, 2019 A curious thing popped up in my Godaddy account dashboard on Monday. Underneath the section to manage my domains, a “Deals from GoDaddy Partners” box offered me $300 in Free Yelp Ads on one side and a business line of credit from Kabbage up to $250,000 on the other.

A curious thing popped up in my Godaddy account dashboard on Monday. Underneath the section to manage my domains, a “Deals from GoDaddy Partners” box offered me $300 in Free Yelp Ads on one side and a business line of credit from Kabbage up to $250,000 on the other.

The Kabbage offer is brand new, according to a joint announcement that came out the same day publicizing a “strategic partnership” between the two companies.

By clicking on it, I found that GoDaddy customers can transmit their account information to Kabbage by clicking a button to begin the loan application process. If a loan is approved, GoDaddy customers save up to $100 on their first monthly loan fee, the website states.

While a simple web domain may only cost around $10 a year, Kabbage has suggested that funds be used for other purposes like staffing up for the busy holiday season, purchasing additional inventory or equipment, or applying it toward digital marketing initiatives.

Borrowers will be able to access the Kabbage dashboard from their Godaddy accounts, an FAQ says.

Below are some screenshots:

Janene Machado Appointed Director of Programs for PCMA’s New York Chapter

November 4, 2019 DeBanked’s Director of Events, Janene Machado, has been appointed the Director of Programs for Professional Convention Management Association’s (PCMA) New York Chapter. Machado will oversee the Program Committee for a three-year term (January 2020 – December 2022). The Committee is responsible for deciding on the topics, programming, logistics, and speaker invitations for the New York Chapter events.

DeBanked’s Director of Events, Janene Machado, has been appointed the Director of Programs for Professional Convention Management Association’s (PCMA) New York Chapter. Machado will oversee the Program Committee for a three-year term (January 2020 – December 2022). The Committee is responsible for deciding on the topics, programming, logistics, and speaker invitations for the New York Chapter events.

PCMA, a volunteer driven organization, is the world’s largest, most respected and most recognized network of business events strategists with more than 7,000 members and activities in 30 countries.

Machado has overseen and directed deBanked’s exceptional events including CONNECT and Broker Fair since joining the company in July 2018. The volunteer position with PCMA will be in addition to her continuing to work for deBanked.

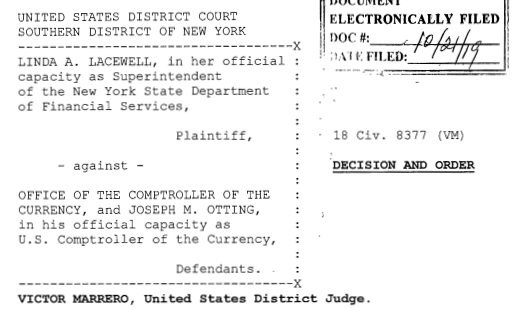

Federal Judge Rules New York’s “Win” Against OCC’s Fintech Charter Nullifies The Fintech Charter Concept Entirely

October 21, 2019 The Office of the Comptroller of The Currency took a gamble with a federal judge in a lawsuit brought by the New York Department of Financial Services (DFS) and lost. On Monday, Judge Victor Marrero ruled that the OCC must “set aside” its special purpose (fintech) national bank charters entirely, not just for those with a nexus to New York.

The Office of the Comptroller of The Currency took a gamble with a federal judge in a lawsuit brought by the New York Department of Financial Services (DFS) and lost. On Monday, Judge Victor Marrero ruled that the OCC must “set aside” its special purpose (fintech) national bank charters entirely, not just for those with a nexus to New York.

The outcome is a byproduct of a ruling issued on May 2nd where the OCC had sought to dismiss the challenge from the onset. DFS was somewhat victorious then in that the case was allowed to proceed, be litigated, and eventually tried. But the OCC felt the case was lost before it had begun because “the Court [had already] ruled on the issue of the law at the heart of the case: whether, under the National Bank Act, OCC has the authority to issue special purpose national bank charters to financial technology companies that do not accept deposits.”

The Court made it clear, that “OCC does not have the authority because the relevant language in the National Bank Act unambiguously defines ‘the business of banking to include deposit-taking.”

The Court made it clear, that “OCC does not have the authority because the relevant language in the National Bank Act unambiguously defines ‘the business of banking to include deposit-taking.”

As a result, OCC negotiated with DFS to reach an agreed upon final judgment in DFS’s favor. The only remaining question was to what level of defeat the OCC would concede. OCC argued a judgment should preclude only New York companies from applying for a fintech charter while the DFS argued it should apply beyond New York’s borders to all 50 states.

On Monday, the judge went with DFS’s version, pointing out that ordinarily prevailing on an Administrative Procedure Act claim, as OCC had indeed consented to judgment on, would mean that the agency’s order would be vacated, not that the plaintiff would win some special relief.

It is hereby ordered, adjudged and decreed that:

OCC’s regulation 5 C.F.R. 5.20(e)(1)(i), is set aside with respect to all fintech applicants seeking a national bank charter that do not accept deposits.

DFS Superintendent Linda A. Lacewell issued an official comment on the ruling:

This decision makes the financial well-being of consumers from New York and around the country a priority. It reflects the rational conclusion that DFS and other state banking regulators have the expertise to provide the strict supervisory oversight and enforcement of anti-money laundering and consumer protection statutes and regulations that non-depository financial service providers are required to follow. The decision stops OCC’s attempt to usurp state authority by establishing a federal fintech regulatory framework at the expense of consumers. Going forward, DFS will continue to be a fierce advocate for consumers in New York and nationwide.

The Broker: Funding Businesses The Irish Way

October 10, 2019 I’m sitting in the lobby of The Marker Hotel, a 5-star 7-story property on the edge of Dublin’s Grand Canal Dock. Here in Ireland’s major tech hub, I’m waiting for a self-identified corporate finance broker by the name of Rupert Hogan, the managing director of BusinessLoans.ie. Outside of our email exchanges, I don’t really know what to expect. I’ve met brokers from the US, Canada, Mexico, UK, and Hong Kong, but never Ireland.

I’m sitting in the lobby of The Marker Hotel, a 5-star 7-story property on the edge of Dublin’s Grand Canal Dock. Here in Ireland’s major tech hub, I’m waiting for a self-identified corporate finance broker by the name of Rupert Hogan, the managing director of BusinessLoans.ie. Outside of our email exchanges, I don’t really know what to expect. I’ve met brokers from the US, Canada, Mexico, UK, and Hong Kong, but never Ireland.

When he arrives, he doesn’t disappoint. Hogan is full of energy and enthusiasm. He has a natural charisma and friendly manner that’s well-suited for a relationship-based business. It just so happens that SME finance in Ireland is still heavily reliant on person-to-person contact and Hogan is at the forefront of helping potential borrowers look beyond the bank for their financing needs.

SMEs are looking for speed and ease in the loan process, Hogan says. Historically, business owners would call on their bank for financing, invoking the sanctity and reliability of decades-old personal relationships, but Hogan explains that relationships between SMEs and banks just aren’t what they used to be. “[SMEs] feel like they’re going to get the runaround,” he says.

That’s where he comes in. And it could be any kind of business, he explains. Hogan jumps from a call with an import/export business to one in retail, followed by one with an agricultural equipment company. He has to understand a bit about them all no matter what it is, to figure out a proper financial solution. BusinessLoans.ie doesn’t charge for their service but they do receive a commission from the financial company if a deal closes.

That’s where he comes in. And it could be any kind of business, he explains. Hogan jumps from a call with an import/export business to one in retail, followed by one with an agricultural equipment company. He has to understand a bit about them all no matter what it is, to figure out a proper financial solution. BusinessLoans.ie doesn’t charge for their service but they do receive a commission from the financial company if a deal closes.

“Corporate” finance may evoke images of big city corporations engaged in international commerce but Hogan’s company can connect SMEs with as little as €5,000 through an unsecured business loan or merchant cash advance. Invoice Financing, leasing, and trade finance are also tools at his disposal. It’s not all small, however, as he hands me a rate sheet for one lender that will go up to €25M. Interest rates on these products when compared with their American and UK brethren are quite reasonable, and suggest also that the target clientele is not subprime.

As we sit there drinking coffee, Americano style in my honor, an executive for a local SME lender happens to spot him while passing by. After they exchange pleasantries, Hogan explains to me that he submits deals to that lender through their online broker portal. And so I ask him if doing everything online has become the standard in Ireland.

“It’s getting there,” he says, while acknowledging there’s still a ways to go with the population that’s conditioned to handling their financial dealings offline. The company’s domain name is perhaps perfectly positioned to capture that transitioning audience. When businesses decide to look for a loan online, he explains, “I hope they go to BusinessLoans.ie”