Related Headlines

| 07/31/2020 | States sue to block Madden rule fix |

| 11/18/2019 | OCC proposes rule to fix Madden |

| 09/19/2019 | Madden decision is "unfathomable" |

| 03/11/2019 | Settlement reached in Madden v Midland |

| 08/30/2017 | Madden v Midland update |

Stories

OCC Believes It’s Time To Fix Madden Issue Once And For All

November 18, 2019 If a bank makes a legal loan to a consumer and then later sells the debt to a third party, the terms of the loan are still legal right?

If a bank makes a legal loan to a consumer and then later sells the debt to a third party, the terms of the loan are still legal right?

“Yes” should be the obvious answer, but in 2015 a federal appeals court said “no.” The case was Madden v. Midland Funding LLC, which started as a credit card debt owed by a consumer to Bank of America at 27% interest and ended as an allegedly illegal loan once the debt was sold to Midland Funding.

The ruling, which deBanked has covered extensively, shook the consumer and business loan markets in New York, Connecticut, and Vermont with its jurisdictional reach. Midland Funding appealed the ruling to the United States Supreme Court but the Court declined to hear the case.

Congress attempted to bring clarity to the lawfulness of the practice with a bill called the Protecting Consumers’ Access to Credit Act of 2017 but failed when the approved House bill never even came up for a vote in the Senate.

On Monday, the Office of the Comptroller of the Currency (OCC) proposed a rule to clarify the “Valid When Made” Doctrine that had been pierced in Madden. “This proposal will address confusion about the effect of a transfer on a loan’s valid interest rate, including confusion resulting from a recent decision from the U.S. Court of Appeals for the Second Circuit (Madden v. Midland Funding, LLC),” OCC wrote in a statement.

A 60-day public comment period will be open once the proposal is published in the Federal Register. To find out how to comment on the rule, click here.

Mad Over Madden

March 15, 2018 In a dispute that reflects the nation’s rigid political polarization, a piece of legislation pending before Congress either corrects a judicial error or condones “predatory lending.” It depends upon whom one asks. Either way, the proposed law could affect the alternative small-business funding industry indirectly in the short run and directly in the long term by addressing the interest rates non-banks charge when they take over bank loans.

In a dispute that reflects the nation’s rigid political polarization, a piece of legislation pending before Congress either corrects a judicial error or condones “predatory lending.” It depends upon whom one asks. Either way, the proposed law could affect the alternative small-business funding industry indirectly in the short run and directly in the long term by addressing the interest rates non-banks charge when they take over bank loans.

The easiest way to understand the controversy may be to trace it back to a ruling in 2015 by the United States Court of Appeals for the Second Circuit in New York. The case of Madden v. Midland Funding LLC started as claim by a consumer who was challenging the collection of a debt by a debt buyer, says Catherine Brennan, a partner in the law firm Hudson Cook LLP.

“Debt buyers like Midland are sued on a regular basis,” Brennan notes. “That’s a common occurrence.” What’s uncommon is that the appellate court affirmed the idea that the loan debt that Midland sought to collect from Madden became usurious when Midland bought it. The court ruled that because Midland wasn’t a bank it was not entitled to charge the interest the bank was allowed to charge, she maintains.

Under the ruling, non-banks that buy loans can’t necessarily continue to collect the interest rates banks charged because non-banks are generally subject to the limits of the borrower’s state, according to the Republican Policy Committee, an advisory group established by members of the House of Representatives in 1949. Banks can charge the highest rate allowed in the state where they are chartered, which could be much higher than allowed in the borrower’s state.

“So it undermines the concept that you determine the validity of a loan at the time the loan is made,” Brennan says of the decision in the Madden case. The “valid-when-made” doctrine – a long-established principle of usury law – states that if a loan is not usurious when made it does not become usurious when taken over by a third party, published reports say. In 2016, the U.S. Supreme Court declined to hear the Madden case, which in effect upheld the appellate court ruling.

In response, both houses of Congress are considering bills that would ensure that the interest rate on a loan originated by a bank remains valid if the loan is sold, assigned or transferred to a non-bank third party, the Republican Policy Committee says.

On Feb. 14, 2018, the House passed its version of the proposal, H.R. 3299, the Protecting Consumers’ Access to Credit Act of 2017, or the “Madden fix,” as it’s known colloquially. The vote was 245 to 171, mostly along party lines with 16 Democrats joining 229 Republicans to vote in favor. The Senate version, S. 1642, had not reached a vote by press time.

“It’s not a revolutionary concept,” Brennan says of the proposed law. “It had been understood prior to Madden that you determine usury at the time the loan is originated, and that should be restored.”

As the alternative small-business funding industry continues to mature it could benefit from the legislation, Brennan predicts. In the future, alt funders may begin to buy or sell more debt, which would make it subject to the state caps if the legislation fails to pass, she says.

The proposed law would also benefit partnerships in which banks refer prospective borrowers to alternative funders because it would eliminate uncertainty and would thus improve the stability of the asset, Brennan continues. “I would think anyone in the commercial lending space would want to see the Madden bill pass,” she contends.

Stephen Denis, executive director of the Small Business Finance Association, a trade group for alt funders, agrees. While most of the SBFA’s members don’t work with bank partners, the trade group has supported the lobbying efforts of other associations and coalitions representing financial services companies directly affected, he says. “We are concerned on behalf of the broader industry because we all work closely together and everyone has the same goal of making sure that we’re providing capital to small businesses,” he maintains.

That goal of keeping funds available to entrepreneurs also motivates the sponsor of H.R. 3299, Rep. Patrick McHenry, R-N.C., who’s chief deputy whip of the House and vice chair of the House Financial Services Committee. His interest in crowdfunding, capital formation and disruptive finance is fueled by events he experienced in his childhood, when his father attempted to operate a small business but struggled to find financing, according to the Congressman’s website.

Although H.R. 3299 passed in the House with mostly Republican votes, it attracted bipartisan co-sponsors in that chamber. They are Rep. Gregory Meeks, D-N.Y.; Rep. Gwen Moore, D-Wis., and Rep. Trey Hollingsworth, R-Ind. The Senate version of the legislation is sponsored by Sen. Mark R. Warner, D- Va.

Although H.R. 3299 passed in the House with mostly Republican votes, it attracted bipartisan co-sponsors in that chamber. They are Rep. Gregory Meeks, D-N.Y.; Rep. Gwen Moore, D-Wis., and Rep. Trey Hollingsworth, R-Ind. The Senate version of the legislation is sponsored by Sen. Mark R. Warner, D- Va.

But opponents of the proposed law aren’t feeling particularly bipartisan and argue vehemently against it, Brennan contends. “There’s been a lot of misinformation put out there by consumer advocates saying this would somehow embolden payday lending in all 50 states,” she says. “It’s simply not true.”

Payday lenders aren’t banks, so the proposed legislation would not apply to them and thus would not enable them to avoid interest caps imposed by borrowers’ states, Brennan notes, adding that some states don’t even allow payday consumer lending.

Consumer advocates are spreading propaganda because they oppose interest rates they consider high, Brennan continues. Advocates are incorrectly conflating payday lending with marketplace lending, she maintains.

The latter is defined as partnerships where non-banks sometimes work with banks to operate nationwide platforms, mostly online and sometimes peer-to-peer, she says, noting that examples include LendingClub and Prosper.

There’s no evidence marketplace lenders would astronomically increase their interest rates if the president signs into law a bill that resembles those now before Congress, Brennan says. It wasn’t happening before Madden, she notes, and banks involved in those partnerships operate under strict guidance of the Federal Deposit Insurance Corp. (FDIC) or the Office of the Comptroller of the currency, depending upon their charters.

But consumer advocates haven taken to the warpath, Brennan reports. Opponents of the legislation call partnerships between banks and non-bank lenders by the derogatory term “rent-a-bank schemes.” But it’s lawful to create such relationships because the FDIC oversees them, she asserts.

Just the same, the House is considering H.R. 4439, a bill to ensure that in a bank partnership with a non-bank, the bank remains the “true lender” and can set the interest rate, Brennan notes. If the bill becomes law, it would clear up the conflict that has arisen in inconsistent case law, some of which has defined the non-bank as the true lender, she says.

Meanwhile, opponents of H.R. 3299 and S. 1642 have written a letter to members of Congress, urging them to vote against the bills. The letter, drafted by the Center for Responsible Lending (CRL) and the National Consumer Law Center (NCLC), was signed by 152 local, state, regional and national organizations. Most of the signers belong to a coalition called Stop the Debt Trap, says Cheye-Ann Corona, CRL senior policy associate.

The bills create a loophole that enables predatory lenders to sidestep state interest rate caps, Corona maintains. That’s because non-banks are actually originating the loans when they work in tandem with banks, she says. The non-banks are using banks as a shield against state laws because banks are regulated by the federal government. If the legislation passes, non-banks would not have to observe state caps and could charge triple-digit interest rates, she contends.

“This bill is trying to address the issue of fintech companies, but there is nothing innovative about usury,” Corona says. “They are just repackaging products that we’ve seen before. A loan is a loan. These lenders don’t need this bill if they are obeying state interest-rate caps.”

The lenders disagree. In fact, a trade group formed by OnDeck, Kabbage and Breakout Capital calls itself the Innovative Lending Platform Association, according to a report in the Los Angeles Times. The article cites the need for small-business capital but questions whether the loans are marketed fairly.

Innovative or not, lenders offering credit with higher interest rates could condemn consumers to a nightmare of debt, according to the letter from the CRL and NCLC to Capitol Hill. “Unaffordable loans have devastating consequences for borrowers – trapping them in a cycle of unaffordable payments and leading to harms such as greater delinquency on other bills,” the letter says.

However, alt funders say their savvy small-business customers understand finance and thus don’t need much government protection from high interest rates. But the CRL doesn’t adhere to that philosophy, Corona counters. “Small businesses are at risk with predatory lending practices,” she says, maintaining that some alt funders charge interest rates of 99 percent.

Small-business owners plunged themselves into hot water by borrowing too much in anecdotal examples provided by Matthew Kravitz, CRL communications manager. In one example, an entrepreneur found himself automatically paying back $331 every day. He overestimated his future income and now says he feels like hiding under the covers every morning.

Corona also dismisses the idea that high risk calls for high interest rates to compensate for high default rates. When interest rates rise to a level that borrowers can’t handle, no one wins, she maintains.

The right to charge higher interest rates could also encourage lenders to loosen their underwriting criteria, Corona warns. That could result in shortcuts reminiscent to the practices that gave rise to the foreclosure crisis and the Great Recession, she says, adding that, “we don’t want to see that happen again.”

The Madden Decision, Three Years Later

February 18, 2018

At first, reversing the 2015 Madden v. Midland Funding court decision, which continues to vex the country’s financial system and which is having a negative impact on the financial technology industry, seemed like a fairly reasonable expectation.

The controversial ruling by the Second Circuit Court of Appeals in New York, which also covers the states of Connecticut and Vermont, had humble roots. Saliha Madden, a New Yorker, had contracted for a credit card offered by Bank of America that charged a 27% interest rate, which was both allowable under Delaware law and in force in her home state.

But when Madden defaulted on her payments and the debt was eventually transferred to Midland Funding, one of the country’s largest purchasers of unpaid debts, she sued on behalf of herself and others. Madden’s claim under the Fair Debt Collection Practices Act was that the debt was illegal for two reasons: the 27% interest rate was in violation of New York State’s 16% civil usury rate and 25% criminal usury rate; and Midland, a debt-collection agency, did not have the same rights as a bank to override New York’s state usury laws.

In 2013, Madden lost at the district court level but, two years later, she won on appeal. Extension of the National Bank Act’s usury-rate preemption to third party debt-buyers like Midland, the Second Circuit Court ruled, would be an “overly broad” interpretation of the statute.

For the banking industry, the Madden decision – which after all involved the Bank of America — meant that they would be constrained from selling off their debt to non-bank second parties in just three states. But for the financial technology industry, says Todd Baker, a senior fellow Harvard’s Kennedy School of Government and a principal at Broadmoor Consulting, it was especially troubling.

“The ability to ‘export’ interest rates is critical to the current securitization market and to the practice that some banks have embraced as lenders of record for fintechs that want to operate in all 50 states,” Baker told deBanked in an e-mail interview.

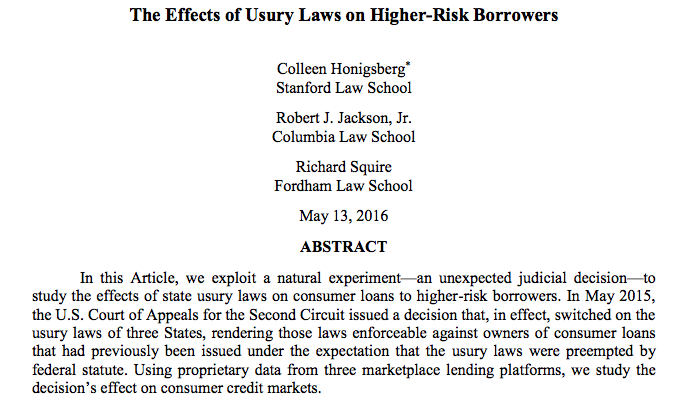

A 2016 study by a trio of law professors at Columbia, Stanford and Fordham found other consequences of Madden. They determined that “hundreds of loans (were) issued to borrowers with FICO scores below 640 in Connecticut and New York in the first half of 2015, but no such loans after July 2015.” In another finding, they reported: “Not only did lenders make smaller loans in these states post-Madden, but they also declined to issue loans to the higher-risk borrowers most likely to borrow above usury rates.”

With only three states observing the “Madden Rule,” the general assumption in business, financial and legal circles was that the Supreme Court would likely overturn Madden and harmonize the law. Brightening prospects for a Madden reversal by the Supremes: not only were all segments of the powerful financial industry behind that effort but the Obama Administration’s Solicitor General supported the anti-Madden petitioners (but complicating matters, the SG recommended against the High Court’s hearing the case until it was fully resolved in lower courts).

Despite all the heavyweight backing, however, the High Court announced in June, 2016, that it would decline to hear Madden.

That decision was especially disheartening for members of the financial technology community. “The Supreme Court has upheld the doctrine of ‘valid when made’ for a long time,” a glum Scott Stewart, chief executive of the Innovative Lending Platform Association – a Washington, D.C.-based trade group representing small-business lenders including Kabbbage, OnDeck, and CAN Capital — told deBanked.

Even so, the setback was not regarded as fatal. Congress appeared poised to ride to the lending industry’s rescue. Indeed, there was rare bipartisan support on Capitol Hill for the Protecting Consumers’ Access to Credit Act of 2017 — better known as the “Madden fix.”

Introduced in the House by Patrick McHenry, a North Carolina Republican, and in the Senate by Mark Warner, Democrat of Virginia, the proposed legislation would add the following language to the National Bank Act. “A loan that is valid when made as to its maximum rate of interest…shall remain valid with respect to such rate regardless of whether the loan is subsequently sold, assigned, or otherwise transferred to a third party, and may be enforced by such third party notwithstanding any State law to the contrary.”

Just before Thanksgiving, the House Financial Services Committee approved the Madden fix by 42-17, with nine Democrats joining the Republican majority, including some members of the Congressional Black Caucus. Notes ILPA’s Stewart: “We were seeing broad-based support.”

But the optimism has been short-lived. The Madden fix was not included in a package of financial legislation recently approved by the Senate Banking Committee, headed by Sen. Mike Crapo, Republican of Idaho. Moreover, observes Stewart: “Senator Warner appears to have gotten cold feet.”

What happened? Last fall, a coast-to-coast alliance of 202 consumer groups and community organizations came out squarely against the McHenry-Warner bill. Denouncing the bill in a strongly worded public letter, the groups — ranging from grassroots councils like the West Virginia Citizen Action Group and the Indiana Institute for Working Families to Washington fixtures like Consumer Action and Consumer Federation of America – declared: “Reversing the Second Circuit’s decision, as this bill seeks to do, would make it easier for payday lenders, debt buyers, online lenders, fintech companies, and other companies to use ‘rent-a-bank’ arrangements to charge high rates on loans.”

The letter also charged that, if enacted, the McHenry-Warner bill “could open the floodgates to a wide range of predatory actors to make loans at 300% annual interest or higher.” And the group’s letter asserted that “the bill is a massive attack on state consumer protection laws.”

Lauren Saunders, an attorney with the National Consumer Law Center in Washington, a signatory to the letter and spokesperson for the alliance, told deBanked that “our main concern is that interest-rate caps are the No. 1 protection against predatory lending and, for the most part, they only exist at the state level.”

But in their study on Madden, the Stanford-Columbia-Fordham legal scholars report that the strength of state usury laws has largely been sapped since the 1970s. “Despite their pervasiveness,” write law professors Colleen Honigsberg, Robert J. Jackson, Jr., and Richard Squire, “usury laws have very little effect on modern American lending markets. The reason is that federal law preempts state usury limits, rendering these caps inoperable for most loans.”

While the battle over the Madden fix has all the earmarks of a classic consumers-versus-industry kerfuffle, the fintechs and their allies are making the argument that they are being unfairly lumped in with payday lenders. “Online lending, generally at interest rates below 36%, is a far cry from predatory lending at rates in the hundreds of percent that use observable rent-a-charter techniques and that result in debt-traps for borrowers,” insists Cornelius Hurley, a Boston University law professor and executive director of the Online Lending Policy Institute. Because of fintechs, he adds: “A lot of people who wouldn’t otherwise qualify in the existing system are getting credit.”

A 2016 Philadelphia Federal Reserve Bank study reports that traditional sources of funding for small businesses are gradually exiting that market. In 1997, small banks under $1 billion in assets –which are “the traditional go-to source of small business credit,” Fed researchers note — had 14 percent of their assets in small business loans. By 2016, that figure had dipped to about 11 percent.

The Joint Small Business Credit Survey Report conducted by the Federal Reserve in 2015 determined that the inability to gain access to credit “has been an important obstacle for smaller, younger, less profitable, and minority-owned businesses.” It looked at credit applications from very small businesses that depend on contractors — not employees – and discovered that only 29 percent of applicants received the full amount of their requested loan while 30 percent received only partial funding. The borrowers who “were not fully funded through the traditional channel have increasingly turned to online alternative lenders,” the Fed study reported.

The ILPA’s Stewart gives this example: A woman who owns a two-person hair-braiding shop in St. Louis and wants to borrow $20,000 to expand but has “a terrible credit score of 640 because she’s had cancer in the family,” will find the odds stacked against when seeking a loan from a traditional financial institution.

But a fintech lender like Kabbage or CAN Capital will not only make the loan, but often deliver the money in just a few days, compared with the weeks or even months of delivery time taken by a typical bank. “She’ll pay 40% APR or $2,100 (in interest) over six months,” Steward explains. “She’s saying, ‘I’ll make that bet on myself’ and add two additional chairs, which will give her $40,000-$50,000 or more in new revenues.”

In yet another analysis by the Philadelphia Fed published in 2017, researchers concluded that one prominent financial technology platform “played a role in filling the credit gap” for consumer loans. In examining data supplied by Lending Club, the researchers reported that, save for the first few years of its existence, the fintech’s “activities have been mainly in the areas in which there has been a decline in bank branches….More than 75 percent of newly originated loans in 2014 and 2015 were in the areas where bank branches declined in the local market.”

Meanwhile, there is palpable fear in the fintech world that, without a Madden fix, their business model is vulnerable. Those worries were exacerbated last year when the attorney general of Colorado cited Madden in alleging violations of Colorado’s Uniform Consumer Credit Code in separate complaints against Marlette Funding LLC and Avant of Colorado LLC. According to an analysis by Pepper Hamilton, a Philadelphia-headquartered law firm, “the respective complaints filed against Marlette and Avant allege facts that are clearly distinguishable from the facts considered by the Second Circuit in Madden.

“Yet those differences did not prevent the Colorado attorney general from citing Madden for the broad-based proposition that a non-bank that receives the assignment of a loan from a bank can never rely on federal preemption of state usury laws ‘because banks cannot validly assign such rights to non-banks.’”

Should the Federal court accept the reasoning of Madden, Pepper Hamilton’s analysis declares, such a ruling “could have severe adverse consequences for the marketplace and the online lending industry and for the banking industry generally….”

Madden v Midland Won’t Be Heard By The US Supreme Court

June 27, 2016

The US Supreme Court has decided not to hear the case of Saliha Madden v Midland Funding.

This was to be expected after US Solicitor General Donald Verrilli filed a devastating brief last month on behalf of the United States government that argued the US Court of Appeals for the Second Circuit was incorrect in its ruling. There is “no circuit split on the question presented,” he wrote, and “the parties did not present key aspects of the preemption analysis” to the lower courts.

Vincent Basulto, a partner at Richards Kibbe & Orbe LLP in New York, said “While it is not expected that other circuits will adopt the reasoning of the Second Circuit, in part due to the arguments made by the Solicitor General, the appellate decision stands as good law in NY. The case will return to the district court for further consideration of other issues and there is reason to believe that the outcome there may be favorable for the financial services industry due to a choice of law issue which remains to be decided.”

US Solicitor General Verrilli resigned three days before the Supreme Court’s decision, but his brief on the case will likely be cited for years to come.

“For the foreseeable future,” Basulto added, “parties can be expected to structure their arrangements in an attempt to distinguish the Madden decision from their transaction, though it is not clear how best to do that.”

Madden v Midland Has Already Hurt Riskier Borrowers, Study Finds

May 28, 2016 If you thought the Madden v Midland decision was a future risk for marketplace lenders alone, think again. According to a joint study by law professors from Stanford, Columbia and Fordham, one group is already suffering as a result of the decision, people with lower FICO scores.

If you thought the Madden v Midland decision was a future risk for marketplace lenders alone, think again. According to a joint study by law professors from Stanford, Columbia and Fordham, one group is already suffering as a result of the decision, people with lower FICO scores.

Since the Second Circuit’s decision only affected borrowers in New York, Vermont and Connecticut, researchers were able to monitor behavioral changes there against other states. They used data from three of the nation’s top marketplace lenders.

In the Second Circuit’s jurisdiction, approved borrowers showed a significant increase in annual incomes, years of employment and FICO scores compared to other districts. Specifically, growth was concentrated among borrowers with FICO scores over 700. Approvals for borrowers with scores below 644 “virtually disappeared” while literally zero loans were issued to borrowers with FICO scores below 625.

“Madden’s effect on loan volume grows as the borrower’s FICO score falls,” the data reveals.

But even though lenders became afraid of the usurious implications in these states, borrowers did not take the Madden decision as a signal to stop payment. “[We] are unable to find any evidence of strategic delinquencies,” researchers concluded after a series of tests.

We find, consistent with basic economic theory, that the sudden enforceability of usury laws had the greatest impact on higher-risk borrowers. In a market where consumer loans are generally increasing in volume, the Madden decision disproportionately affected loan volume for borrowers with the lowest FICO scores.

Read the full study titled, The Effects of Usury Laws on Higher-Risk Borrowers

Second Circuit Incorrect on Madden Case, US Solicitor General Opines

May 25, 2016

Given the Madden v Midland decision, does the National Bank Act continue to have preemptive effect after the national bank has sold or otherwise assigned the loan to another entity?

This question was presented to the US Solicitor General, the person appointed to represent the federal government of the United States of America in Supreme Court cases. The US Supreme court had asked the Solicitor General to weigh in before deciding to take on the case. And the answer is in:

The US Court of Appeals for the Second Circuit was incorrect in its ruling, the federal government believes.

Nevertheless, the US Supreme Court should not even hear the case, they say, because there is “no circuit split on the question presented” and “the parties did not present key aspects of the preemption analysis” to the lower courts. Put simply, “The court of appeals’ decision is incorrect,” they explain, and the heart and soul of preemption itself has never been in question.

The message from the US Solicitor General is clear, carry on friends, nothing to see here with Madden v Midland.

The US Supreme Court could still opt to hear the case but that is very unlikely at this point. Lawsuits filed against alternative lenders such as Lending Club in recent months had used the Madden ruling as evidence to support usury complaints. The connection between a case where a debt collector bought a charged off credit card debt from a bank (which is what Madden was about) and the business model of Lending Club was already weak, but several plaintiffs hoped to use it as a stepping stone. The Solicitor General’s opinion could likely derail attempts by other plaintiffs to cite Madden.

Of notable mention is that many of today’s alternative lenders have relationships with state chartered banks that are covered under the Federal Deposit Insurance Act, not the National Bank Act which the US Supreme Court was asked about. While the two laws are very similar, it did put alternative lenders at an additional arm’s length from Madden.

You can read the Solicitor General’s full brief here.

Read revious posts about this case:

3/22/16 Plot Twist: Obama Administration to Comment on Madden v Midland

3/2/16 Lending Club Class Action Lawsuit Predicated on Madden v Midland Risk

2/26/16 Lending Club Shifts Fee Arrangement With WebBank

2/18/16 Without Scalia, Media Outlets Reporting Marketplace Lenders Supposedly Doomed With Supreme Court Case (They’re Wrong)

11/15/15 Madden v. Midland Appealed to the US Supreme Court

8/13/15 Madden vs. Midland Funding, LLC: What does it mean for Alternative Small Business Lending?

8/13/15 Madden v. Midland Appeal Rejected

8/8/15 Renaud Laplanche on Madden v. Midland

7/28/15 Blyden v. Navient Corp: A Glimpse of a Post-Madden Future?

6/11/15 Legal Brief: Madden v. Midland Funding

Plot Twist: Obama Administration to Comment on Madden v Midland

March 22, 2016

The U.S. Supreme Court wants to know what the Obama administration thinks of the Madden v Midland case.

The potential impact of Madden v Midland on marketplace lending was finally starting to fade away until the U.S. Supreme Court made an unexpected move yesterday. “The Solicitor General is invited to file a brief in this case expressing the views of the United States,” the docket states. At issue is the scope of preemption under the National Bank Act (i.e. can you buy a loan issued by a nationally chartered bank that legally circumvented state usury laws at the time it was originated and still enforce the interest rate?)

The Solicitor General is responsible for arguing cases on behalf of the U.S. government in the U.S. Supreme Court. The position is appointed by the President and confirmed by the Senate. That seat is currently filled by Donald B. Verrilli, Jr., an Obama appointee and the man credited with saving Obamacare. He was the attorney that helped persuade the Supreme Court to treat the individual mandate of the Patient Protection and Affordable Care Act as a tax and not as an exercise of Congress’s power under the Commerce Clause.

Any brief filed is bound to become politically significant since the Obama Administration is on its way out. Therefore any views it expresses in the next few months may not be the same views of the next administration scheduled to be sworn in ten months from now.

Madden v Midland will have no bearing on merchant cash advances and little if any bearing on commercial marketplace lenders. That’s because most not only work with state chartered banks instead of nationally chartered banks, but also face more favorable state usury laws since they do not lend to consumers.

Lending Club Class Action Lawsuit Predicated on Madden v Midland Risk

March 2, 2016UPDATE: This case is unrelated to another class action filed against Lending Club on April 6th

Lending Club is the latest publicly traded online lender to get hit by a shareholder class action lawsuit (OnDeck was first). Filed in the Superior Court of the State of California, plaintiff alleges in the complaint that Lending Club misleadingly concealed the fact that:

- Lending Club had an unsustainable business model that was predicated on it being able to issue loans with extremely high and/or usurious rates across the country

- that their loan investors would not be able to enforce the extremely high and/or usurious rates imposed by Lending Club because they violated state usury laws

- that without the extremely high and/or usurious rates, the loans generated through Lending Club’s marketplace would not be attractive to investors because the loans had very high credit risk and were subject to issues concerning insufficient documentation

- that a substantial portion of its loans were issued with rates in excess of those allowed by applicable state usury laws

The action seeks “recovery, including rescission, for innocent purchasers who suffered many millions of dollars in losses when the truth about Lending Club emerged and the its stock price plummeted.”

Among the Defendants is former US Treasury Secretary Larry Summers.

The complaint alleges that the truth about Lending Club began to emerge after “the Second Circuit affirmed [in Madden v Midland] that the business model used by Lending Club was not valid because loans sold by banks to non-banks, third parties (such as Lending Club and its investors) are not exempt from state usury laws that limit interest rates.”

–In actuality, no such affirmation was made. Lending Club does not specifically use Midland Funding’s business model and the case was not about Lending Club, nor was Lending Club mentioned in it.

“Specifically, the Second Circuit observed that assignees and third-party debt buyers could not rely on the National Bank Act to export interest rates that were legal in one state but usurious in another, to the states where those rates were impermissible,” the complaint states.

–Perhaps, but Lending Club’s bank makes loans under the Federal Deposit Insurance Act, not the National Bank Act.

As supporting evidence, the complaint cites statements from Moody’s analysts, Morgan Stanley, Cross River Bank CEO Gilles Gade, and Lending Club CEO Renaud Laplanche himself in a quarterly earnings call.

While the impact of Madden v Midland has been seriously overblown, Lending Club’s stock has no doubt taken a beating since its IPO. The complaint states a loss of 43% from the original offering price. Among the defendants are:

- LendingClub Corporation

- Renaud Laplanche

- Carrie Dolan

- Daniel Ciporin

- Jeffrey Crowe

- Rebecca Lynn

- John J. Mack

- Mary Meeker

- John C. (Hans) Morris

- Lawrence Summers

- Simon Williams

- Morgan Stanley & Co. LLC

- Goldman, Sachs & Co.

- Credit Suisse Securities (USA) LLC

- Citigroup Global Markets Inc.

- Allen & Company LLC

- Stifel, Nicolaus & Company, Incorporated

- BMO Capital markets Corp.

- William Blair & Company, L.L.C.

- Wells Fargo Securities, LLC

NOTE: This case is unrelated to another class action filed against Lending Club on April 6th

See Post... madden february 02, 2017 clarifying that “freedom of religion” is not “freedom of worship”expressing different religions accepted, ability to believe any religion anyplace anytime, ability to worship in designated places., , i once learned, “those who matter don’t mind, those who mind don’t matter., , now understand, matter exists anyplace, anytime. those who are like min... |

Lending Club Shaking Up Fee Model... madden v. midland funding llc reshapes the lending landscape, the state-level interest rate caps would hold. wsj notes that the ruling is at least one reason why the companys shares have been sliced nearly in half in a little over a year since the firms initial public offering.", , "lending club said friday (feb. 26) that it will boost the fees paid out to webbank, which is owned by steel partners holdings. wsj noted that the conglomerate will have its financial interests tied more to the repayment of the loan because the fee gets paid out... |

See Post... madden v. midland decision and what, if any consequences of that are yet to be determined., , and then there are lenders who are members right here on this very forum that don't use a chartered bank to issue the loans but actually comply with the laws of each individual state. some will require formal licenses and others don't. these lenders too are already strictly adhering to usury laws., , lastly, there are companies on here that strictly buy future receivables who are not lenders and should never be referred to as such. if they know how to properly run their business and vet their contracts, then they too adhere to usury laws. , , i'm not talking to you specifically ktk at all, just using this as an opportunity to bring up something i've noticed with other people i've talked to. if you are reselling any kind of funding product, at the very basic fundamental level, you need to know what it is (loan or purchase) and all of the legality b... |