Story Series: ireland

Clearco to Invest €100 Million into Digital-First Irish Businesses

April 6, 2022 Clearco, the world’s self-proclaimed largest e-commerce investor that provides revenue-based financing capital solutions to e-commerce businesses, is making yet another move. Directed by CEO Michele Romanow, a star in the hit TV show “Dragon’s Den,” Clearco recently announced that it will be introducing its product to Irish founders and entrepreneurs. Upon continuation to support the 15+ % growth predicted in the Irish economy in 2022, the company plans to put €100 million into digital-first Irish businesses.

Clearco, the world’s self-proclaimed largest e-commerce investor that provides revenue-based financing capital solutions to e-commerce businesses, is making yet another move. Directed by CEO Michele Romanow, a star in the hit TV show “Dragon’s Den,” Clearco recently announced that it will be introducing its product to Irish founders and entrepreneurs. Upon continuation to support the 15+ % growth predicted in the Irish economy in 2022, the company plans to put €100 million into digital-first Irish businesses.

An international sales and business development hub has been developed in Dublin. The Clearco team currently consists of 75 members with a plan of adding 125 employees in the future. This will support Clearco’s plan to grow in Europe, North America and Asia Pacific in 2022.

This year Clearco plans to expand its products and services within current European operations and into new key markets across the continent. This includes Western Europe, Central Europe and the Nordic region.

Clearco has invested over $3.2 billion globally into 7,000+ businesses across three continents. Ireland is the fourth international market for Clearco. To be able to serve as many founders as possible internationally, the creation and development of its sales and development team is key.

Clearco has invested over $3.2 billion globally into 7,000+ businesses across three continents. Ireland is the fourth international market for Clearco. To be able to serve as many founders as possible internationally, the creation and development of its sales and development team is key.

Romanow stated “Clearco is excited to bring our revenue-based funding model to Irish founders. Ireland has one of Europe’s strongest economies and a dynamic start-up sector. We are confident that we will have a meaningful impact on the Irish e-commerce economy. Clearco is excited to establish this International Sales hub in Ireland to support our growth in the EMEA region. We’re impressed by the talent and tech skills here and I look forward to building the team to serve our growing customer base.”

Businesses in all 50 states have been funded by Clearco within the US market. However, over half of the company’s funding goes to businesses outside of California, New York, Illinois and Massachusetts, which received about 70%. Clearco believes the same trends will be seen in the Irish marketplace as they hope to help fund traditionally underserved communities.

Irish Lending is Making a Comeback Despite ILCU’s Request for Less Regulation

March 22, 2022 In what some have called the financial services capital of Europe, Ireland’s financial sector has been making a serious comeback since its pandemic-induced slumps. Despite a recent release from the Central Bank of Ireland (CBI) saying that small business lending was making a serious comeback, credit unions throughout the country are pleading with regulators to remove “handcuffs” and allow them to fund their local merchants.

In what some have called the financial services capital of Europe, Ireland’s financial sector has been making a serious comeback since its pandemic-induced slumps. Despite a recent release from the Central Bank of Ireland (CBI) saying that small business lending was making a serious comeback, credit unions throughout the country are pleading with regulators to remove “handcuffs” and allow them to fund their local merchants.

Current regulations enforced by the CBI limit both mortgage and small business lending to banks at 7.5% of the credit union’s total assets.

The Irish League of Credit Unions (ILCU) has said that credit unions are prevented from expanding into the mortgage market because of restrictive lending limits. While the effort comes across as a desire for credit unions to have more flexibility in mortgage options, small business lending has been tied into the deal and thus a part of the movement to get these regulations lifted.

According to the CBI’s data, net lending to small business owners in Ireland was €91m in the fourth quarter, reversing consecutive decreases from the previous two quarters. Estimated repayments by Irish SMEs were the lowest on record over the year as well, to the tune of €4.2 b.

As the data portrays, Irish lending is chugging its way back to normalcy. While the CBI appears to believe that the current system in place is working just fine, the credit unions are making a case that they can help speed up the Irish economy’s recovery process by being able to get a slice of the lending pie.

The ILCU recently responded to remarks made by minister of State Sean Fleming, who when speaking on credit union involvement in lending, encouraged their participation. “Credit unions should fill the gap left by the departures of Ulster Bank and KBC from the Irish market and start lending more mortgages.”

Fleming also included a claim that credit unions are “not doing enough of lending” in his remarks.

In response, ILCU deputy chief executive David Malone cited these regulations that the group has been fighting against as the cause for Fleming’s accusation.

“In order for credit unions to become community banks, and to really engage in the mortgage market, the ILCU is asking Minister Fleming to address the imbalance caused by the restrictive regulatory lending regime in his soon-to-be-published review of the policy framework within which credit unions operate,” said Malone.

Ireland has notably made some big moves in regards to supporting, financing, and government investing of fintech companies from both Ireland and abroad. As the country continues to come out of the financial hardships of the pandemic while also working in the contemporary European financial ecosystem, the CBI doesn’t appear to be lifting any regulation anytime soon, as long as lending numbers keep creeping back to normal.

Ireland is Funding Fintech Through Government Investment

November 2, 2021 The Irish government has taken a serious liking to fintech. With a broad history of being active in financial services, the nation believes they can attract companies from around the world to reap the benefits of employing Irish citizens, while also tapping a major source of export revenue through an up-and-coming industry.

The Irish government has taken a serious liking to fintech. With a broad history of being active in financial services, the nation believes they can attract companies from around the world to reap the benefits of employing Irish citizens, while also tapping a major source of export revenue through an up-and-coming industry.

With access to capital for small businesses just as difficult here as it is in the US, a new fintech company looking for start-up cash may be able to turn to Dublin to get a major investment, rather than dealing with a retail investor or a venture capital firm here in the states. Enterprise Ireland, the organzation that runs these programs, is trying to tempt fintech companies looking for a fresh start or an international expansion to start that process in Ireland.

“Enterprise Ireland is the trade development and venture capital arm of the Irish Government,” said Claire Verville, Senior Vice President of Fintech and Financial Services at Enterprise Ireland. “We are a semi state agency and our mandate is to help support indigenous Irish enterprise to grow and expand in global markets.”

Just like in the United States, it is extremely difficult for an Irish business to walk into a big bank and get a loan. It’s in these situations where the Irish government has decided to make a direct investment themselves. Through Enterprise Ireland, according to Verville, the Irish government can provide capital to startups across a range of areas, in exchange for things like loan repayment or government equity in the company.

“In addition to the kind of more traditional trade development stuff that you would see from any government promoting their indigenous businesses abroad, we do invest directly in companies through equity and participate directly as a [limited partner] in funds to funds.”

Verville spoke about how the Irish government has been looking to extend funding to fintech startups for some time. “Our fintech portfolio is over 200 companies now, we have been one of the most active investors in Europe in a long time. We are one of the most active global investors across all sectors, and we’re really focused on early stage capital for fintech.”

When asked about the decision making process that goes into Irish investments, Verville portrayed it the same as if it was a private firm making the same move. “We will vet like any other investment, make sure we’re comfortable with it, make sure that the business is verifiable, and that we understand the track record of the team,” she said.

When asked about the decision making process that goes into Irish investments, Verville portrayed it the same as if it was a private firm making the same move. “We will vet like any other investment, make sure we’re comfortable with it, make sure that the business is verifiable, and that we understand the track record of the team,” she said.

Through investing in fintech, Enterprise Ireland appears to believe they will give their small business owners better access to capital. If the industry can create a Euro-American hub in Ireland, the latest tech and funding innovations will develop there, giving access to that technology to Irish businesses first. If Irish small business lenders can use Irish technology to help an Irish merchant, everyone wins.

With financial innovation in Europe being leaps ahead of the US, Verville believes the Irish employees working in finance would be better suited to deal with some of these new innovations over Americans because of their familiarity with these systems that are already in place. She hinted at things like EMV cards being around in Ireland for years at the consumer level before they ever made it to the United States.

As far as incentive for profit, Enterprise Ireland isn’t concerned with the success of their investment from a financial perspective as other investment groups are. They instead focus on things like employment numbers and longterm sustainability for those jobs acquired through their efforts in investing in industries like fintech.

“Because we are attached to the government, we aren’t a money-making mission as far as venture capitalists go. We are focused on employment in Ireland, which is partly why it’s so important that the companies are founded in Ireland and that they are building their employee base in Ireland, and on export revenue.”

Verville spoke about how only when businesses in Ireland do well, Enterprise Ireland only does well, too. “We do make money off some of our investments, and that’s government money. We get our budget set by the government department every year, just like any other government agency.”

To be eligible for funding from Enterprise Ireland, a business needs to be based in Ireland, have an Irish LLC, and must have a significant amount of Irish employees. According to Verville, the Irish market is ripe for American small businesses, especially alternative finance.

Irish E-commerce Revenue-Based Funder Raises $76 Million Series A After First Year

May 27, 2021 An Irish revenue-based e-commerce financing platform called Wayflyer raised $76 million in a funding Series A round this past week. It has been a roaring first year for the small fintech, so far funding $150 million to online merchants. The firm just launched its cash advance product 14 months ago and raised $10.2M in a seed round only six months ago.

An Irish revenue-based e-commerce financing platform called Wayflyer raised $76 million in a funding Series A round this past week. It has been a roaring first year for the small fintech, so far funding $150 million to online merchants. The firm just launched its cash advance product 14 months ago and raised $10.2M in a seed round only six months ago.

Wayflyer offers e-commerce sales-based funding, without the need for collateral, from $10k up to $20M. They partner with firms across the UK, including a recent deal with the international athleisure brand Gym+Coffee.

Left Lane Capital led the round with investments from DST Global, QED Investors, Speedinvest, and Zinal Growth. The successful funding comes after the firm widened its credit facility by $100M to keep up with the demand for capital and a partnership announcement with Adobe Commerce.

The cofounders, Aidan Corbett and Jack Pierse came together in 2019. Back then, Corbett led an online marketing analytics firm called Conjura when Pierse, a former venture capitalist, proposed using analytic tech to underwrite what amounts to digital MCAs.

“Jack came to me and said, ‘You should stop using our marketing analytics engine to do these big enterprise SaaS solutions, and instead use them to underwrite e-commerce businesses for short-term finance,'” Corbett told Tech Crunch. “We just had our heads down and started repurposing the platform for it to be an underwriting platform.”

Launching in April 2020, Wayflyer funded $600,000 in the first month. In March of 2021 alone, the firm did about $36 million in advances.

“So, it’s been a pretty aggressive kind of growth,” Corbett said.

Governor Phil Murphy on Fintech in New Jersey

April 14, 2021 In a joint webinar between Choose New Jersey, FinTech Ireland, the New Jersey City University School of Business, and others, NJ Governor Phil Murphy kicked off the event by saying that his state’s object is nothing short of being the state of innovation, where new ventures can take shape, companies can expand, and people can raise a family.

In a joint webinar between Choose New Jersey, FinTech Ireland, the New Jersey City University School of Business, and others, NJ Governor Phil Murphy kicked off the event by saying that his state’s object is nothing short of being the state of innovation, where new ventures can take shape, companies can expand, and people can raise a family.

Murphy’s participation in Irish fintech collaboration was steeped in his commitment to international relations and business.

“The fintech business in particular is a big part of our economy,” Murphy said. “We’ve got proximity to New York City’s financial markets and as a result we’ve become sort of the perfect home for fintech companies. We have 145 fintech companies headquartered in New Jersey.”

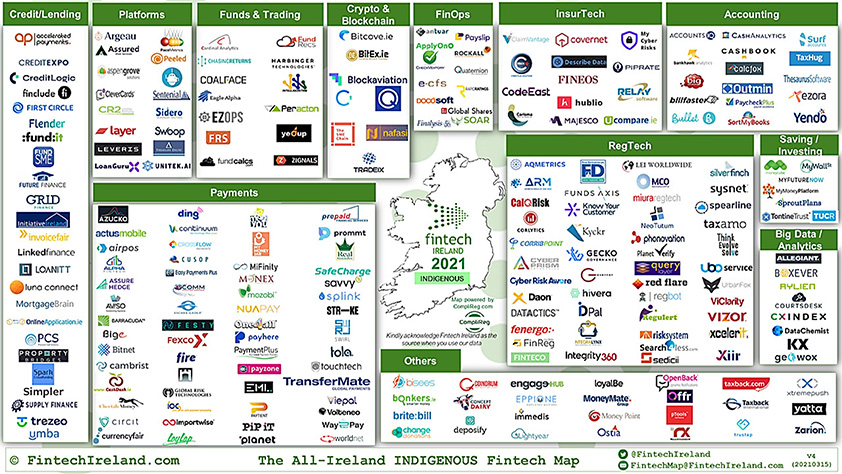

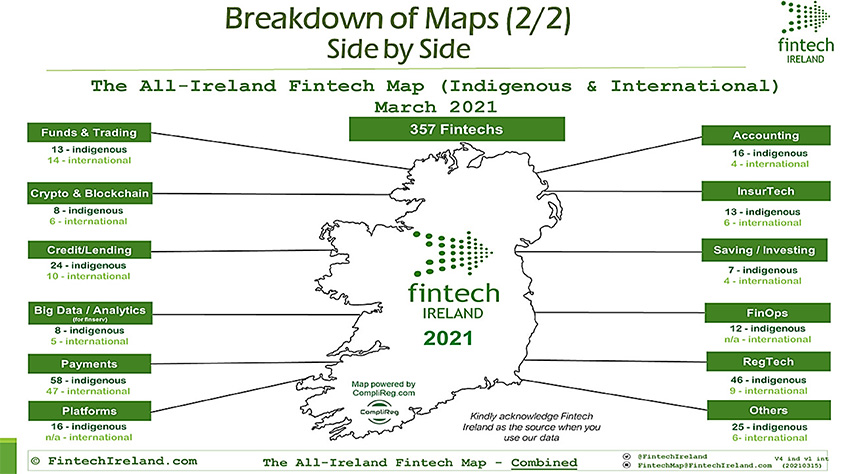

The island of Ireland, by comparison, is home to nearly 250 indigenous fintech companies, according to the latest Fintech Ireland map. Recently, Irish fintech companies ranked the United States and Canada as their #1 priority region for expansion.

New Jersey is hoping to benefit from transatlantic opportunities this might present.

“There’s no better place in America than to plant your flag here in New Jersey,” Murphy said. “To those who are considering [it], it’ll be the best decision you ever make.”

The Governor also revealed that his family is descended from Donoughmore, County Cork and that he hopes to make a state trip to the republic soon.

Ireland’s Fintech Industry May Be Coming to North America

March 16, 2021 Americans asked to name an Irish fintech company often say Stripe, the company founded by two Ireland-born brothers that is dual headquartered in San Francisco and Dublin. Recently valued at $95 billion, its financial backers include Sequoia Capital and the Irish government via the National Treasury Management Agency.

Americans asked to name an Irish fintech company often say Stripe, the company founded by two Ireland-born brothers that is dual headquartered in San Francisco and Dublin. Recently valued at $95 billion, its financial backers include Sequoia Capital and the Irish government via the National Treasury Management Agency.

Stripe’s Irish roots may not be a one-off. Though the Republic’s entire population (4.9M) is less than that of New York City (8.7M), it is home to nearly 250 indigenous fintech companies, dozens of which offer lending and payment products, according to the latest Fintech Ireland map. And many have expansion plans in the works.

Despite the close proximity to the UK, the United States and Canada tied for the #1 priority region that homegrown Irish fintech companies said they want to expand to, according to Fintech Ireland’s industry survey. The UK came in 2nd. The majority of Irish fintech companies actually said they prioritized expansion plans for the US and Canada even over expansion in their home country.

A flight from New York to Dublin can be shorter than a flight from New York to San Francisco and Ireland’s primary language is English. 7,000 people work in fintech in Ireland, the bulk of which are based in Dublin.

deBanked evaluated the market in-person during the Fall of 2019 and determined that there are many cultural and operational similarities to the US. A follow-up piece in May 2020 captured how the industry there was faring through the Covid pandemic.

Ireland’s Alternative Finance Industry and the Coronavirus

May 18, 2020 As the effects of the coronavirus continue to slow down the American economy, around the world, many countries remain in lockdown, with their businesses having been halted. Be it to the north, south, east, or west, of the United States, the results are the same: money has stopped flowing. As such, we took the opportunity to follow up with some of the businesses that featured in our coverage of alternative finance in Ireland last Fall, hoping to see what differed and what was the same in their responses to the pandemic.

As the effects of the coronavirus continue to slow down the American economy, around the world, many countries remain in lockdown, with their businesses having been halted. Be it to the north, south, east, or west, of the United States, the results are the same: money has stopped flowing. As such, we took the opportunity to follow up with some of the businesses that featured in our coverage of alternative finance in Ireland last Fall, hoping to see what differed and what was the same in their responses to the pandemic.

Despite differing in size and range of variety when compared to their North American counterparts, the Irish alternative finance and fintech industries have largely felt the same impacts from covid-19. Certain funders have stopped operations, others have become very cautious, and just like here, some businesses have turned to the government for help.

LEO, or Local Enterprise Offices, is an advisory network for small and medium-sized businesses, which provide guidance as well as offer capital. The Irish government has pointed to these as the point of contact for small businesses owners, with LEO providing microfinance loans of up €50,000. This figure being upped from the pre-coronavirus maximum of €25,000.

Rupert Hogan, the Managing Director of brokering company BusinessLoans.ie, explained that some businesses would be better going with LEO over banks and even some non-banks. Noting that non-bank lenders can’t compete with the rates offered by LEO and, just like in the US, banks can’t act with the speed that these business owners need.

Hogan, who describes the current situation as “The Great Lockdown,” said that banks “aren’t too helpful, even in the good times,” due to the high rejection rates that SMEs experience when looking for loans. In regards to merchant cash advances, he’s expecting, when the MCA companies reopen, that they’ll be funding at reduced rates, some doing as much as 50% less than their pre-coronavirus amounts.

Hogan, who describes the current situation as “The Great Lockdown,” said that banks “aren’t too helpful, even in the good times,” due to the high rejection rates that SMEs experience when looking for loans. In regards to merchant cash advances, he’s expecting, when the MCA companies reopen, that they’ll be funding at reduced rates, some doing as much as 50% less than their pre-coronavirus amounts.

Jaime Heaslip, Head of Brand Marketing at the MCA company Flender, explained that before the virus, the company was experiencing a period of productivity, with lending activity and amounts deposited being up from previous years. And despite the virus disrupting commerce, the former international rugby player noted that business owners are still coming to Flender for funds.

“We provide flexibility for people, there’s a lot of people coming to us to get contingency funds together,” he said over a phone call, commenting that as well as this, many businesses are looking for financing to move their operations online. “We’re trying to help SMEs get through this and provide as much help as possible.”

Beyond merchant cash advances, business continues to run, says Spark Crowdfunding’s Chris Burge. Being an investment platform, Spark is still active with businesses looking to get off the ground.

“We’ve actually found that we’ve still got a large amount of inquiries coming through,” the CEO and Co-Founder said. “Our pipeline of companies wanting to go onto the platform is very strong, and we’ve been engaging with them all and they’re very keen. They all need money, which, of course, hasn’t changed from before there was a crisis. And they still are needing money, they need that to expand as opposed to survive.”

When asked about changes made because of covid-19, Burge explained that their investor evenings have been disrupted. Previously an opportunity for the investors and investees on the digital platform to meet up personally and pitch each other, these 100-person gatherings are no longer an option. Instead, virtual webinars and assemblies are what Spark has started using to keep up communication between parties.

And on the subject of fundraising, Trezeo’s Garrett Cassidy said that it has become a nightmare under the pandemic. Disrupted communication channels and the inability to pitch to someone in the same room as you have been hurdles, but besides that, Cassidy assured me that Trezeo is still going strong.

Offering payment structures and benefit bundles to freelancers and the self-employed, Trezeo has seen some of its customer base drop off as unemployment sky-rocketed in the UK, its prime market. Despite this, as more and more people are beginning to go back to work, Cassidy says numbers are rising.

Offering payment structures and benefit bundles to freelancers and the self-employed, Trezeo has seen some of its customer base drop off as unemployment sky-rocketed in the UK, its prime market. Despite this, as more and more people are beginning to go back to work, Cassidy says numbers are rising.

“Now we’re starting to see earnings pick back up again, some of them were the ones who were off work who are now coming back to work. So it’s been interesting watching that but the reality is that they’re also scared. They’re out working every day delivering parcels or food, depending on which, and just working really hard. It’s the most important ones who are paid the least and that have the least protection.”

Looking ahead, Trezeo has been working with the UK’s Labour Exchange to establish a new program that would see the creation of channels to help pre-qualify workers for certain positions. These workers would be pooled, and employers would be able to choose from them, streamlining the hiring process for both sides.

“They need money in their pockets, somehow, quickly,” Cassidy said of workers, whether that be by returning to work safely, or through some government assistance program, the CEO is adamant that people need to stay solvent.

Altogether, Ireland’s alternative finance industry, like others the world over, has been hit hard by the coronavirus’s economic effects. With the country’s phased lifting of the lockdown being plotted out over the course of the summer, the island nation may not see as quick a return to commerce as certain American states, but its fintechs and non-banks hope to stick around, by hook or by crook, as the Irish say, by any means possible.

How GRID Finance’s Cash Advances Are Building Stronger Irish Communities

December 27, 2019

Five years ago, a small company in Dublin put Ireland’s fintech scene on the map by advising local SMEs to “get on the GRID.” GRID Finance, founded by Derek F Butler, introduced a peer-to-peer lending model to Irish businesses at a time when the industry was just beginning to form. From the beginning, the company’s secret sauce was the GRID Score, a proprietary credit score system that enabled the company to take on the difficult task of assessing the risk of SMEs.

Butler, who I sat down with in September at the company’s headquarters alongside Chief Marketing Officer Andrea Linehan, says the GRID Score is an SME’s “passport to the economy.”

It’s the upper tier that GRID caters to while providing a unique product within Ireland known as a cash advance. The setup is similar to Square and PayPal in the US in that the loans are repaid via a percentage of an SME’s credit/debit card transactions on a daily basis. The term of the loan is fixed and the costs are reasonable.

“The reality is that small business funding and financing is a high risk,” Linehan says.

“There’s no subprime market here,” Butler adds. “We’re trying to build a prime cash advance market versus a subprime one in the US.”

Like GRID’s competitors in the industry, Linehan believes that finance in Ireland will transition online. “Ireland is still dominated by two banks,” she says, referring to Bank of Ireland and AIB. The company, therefore, believes it has a good head start on the impending shift. But in the meantime, they’ve learned how important it is to be embedded in the local communities. To that end, GRID has an office in Limerick, Ireland’s third largest city with 95,000 people that’s located about 200km away from its headquarters in Silicon Docks.

Like GRID’s competitors in the industry, Linehan believes that finance in Ireland will transition online. “Ireland is still dominated by two banks,” she says, referring to Bank of Ireland and AIB. The company, therefore, believes it has a good head start on the impending shift. But in the meantime, they’ve learned how important it is to be embedded in the local communities. To that end, GRID has an office in Limerick, Ireland’s third largest city with 95,000 people that’s located about 200km away from its headquarters in Silicon Docks.

And their mission goes beyond providing funds. “If we can help get [SMEs] ready by giving them the tips to improve their financial health right now, let’s try and do that,” Butler says. “We want them to understand their financial health versus their cost of capital.”

While the company has sustained modest growth, Business Post reported earlier this month that GRID plans to raise €100 million in 2020 to provide even more loans through its platform.

Butler likens GRID’s mission to the MetLife Foundation, promoting financial health and building stronger communities. “We do a lot of work with the MetLife foundation because of the impact they have,” he says. “It’s why I launched GRID Finance.”