Story Series: ireland

Flender Makes BIG Mark in Ireland’s SME Lending Market

November 26, 2019 Ireland can seem like a small place, so much so that on my way to meeting with Colin Canny, Flender’s Head of Partnerships, I quite literally bumped into Flender’s co-founder & CEO Kristjan Koik who was walking through Dublin’s Silicon Docks. I recognized Koik from the who’s who catalogue of executives I had compiled before traveling abroad to explore the Irish fintech scene. He was cordial and polite. And yet through his demeanor I sensed there was more, that there was a story to be told even if it was not ready to be shared.

Ireland can seem like a small place, so much so that on my way to meeting with Colin Canny, Flender’s Head of Partnerships, I quite literally bumped into Flender’s co-founder & CEO Kristjan Koik who was walking through Dublin’s Silicon Docks. I recognized Koik from the who’s who catalogue of executives I had compiled before traveling abroad to explore the Irish fintech scene. He was cordial and polite. And yet through his demeanor I sensed there was more, that there was a story to be told even if it was not ready to be shared.

The following month Flender would reveal remarkable news, a new €75 million funding line, bringing their total to €109 million raised since the company’s founding in 2015. The company is backed by Eiffel Investment Group, Enterprise Ireland, entrepreneur Mark Roden and former Ireland rugby player Jamie Heaslip.

This large amount of funding, even by UK or US standards, makes Flender stand out, and so when I finally meet with Canny on that warm Fall day in September, I’m pretty thankful he afforded me the time.

Flender, Canny explains, is derived from Flexible Lender. The pamphlet he produces and hands to me says that their idea is simple, to provide businesses with the funding they need and ensure the application process is fast, easy, and transparent.

Application details for products like term loans and merchant cash advances require the usual stips like historical bank statements, a profit & loss statement, and a balance sheet. But there’s also a section quintessentially Irish, that is that it can be beneficial to submit your last 2 years herd numbers if you’re a farmer, complete with your last 12 months Milk Reports and property acreage figure.

Canny explains that Flender is not a high-risk fall-back lender, but rather the opposite. “Our credit process is extremely tight,” he says, “in line with banks.” And with good rationale, seeing that the company is still somewhat reliant on a peer-to-peer funding model. More than half of individual peers on the platform are Irish but Canny says that it’s not unusual for non-residents including Americans to lend on the platform as well.

Canny explains that Flender is not a high-risk fall-back lender, but rather the opposite. “Our credit process is extremely tight,” he says, “in line with banks.” And with good rationale, seeing that the company is still somewhat reliant on a peer-to-peer funding model. More than half of individual peers on the platform are Irish but Canny says that it’s not unusual for non-residents including Americans to lend on the platform as well.

Canny says the Irish market is very “community based.” The transparency of the marketplace aligns with that characterization. Like other peer-to-peer small business lenders in Ireland, borrower identity is publicly accessible on the platform, as are the terms of the loan. Anyone can view the business name of a prospective borrower on the website, the address, a bio, and even their “story.”

Flender taps several marketing channels like Google Adwords, radio, direct sales, and even brokers. Canny says they generate an underwriting decision in as quick as 4-6 hours and fund a business in as little as 24 hours. Borrowers like the product so much that many renew. Seventy percent of the SMEs in the country are peer-to-peer bankable, Canny explains, creating a wide playing field to target.

Meawnwhile, CEO Kristjan Koik told the Irish Times that the top 3 banks in Ireland have 92 percent of the SME lending marketshare so there is still a ton of opportunity for non-banks like Flender to grab hold of.

As for how the massive credit line impacts them going forward? Koik told the Times that they would be cutting interest rates by up to 1 percent across their various loan products. Interest rates now start as low as 6.45% and terms range up to 36 months.

As Canny and I part ways I present one final question, will Flender be expanding abroad? I get no definitive answer. He was cordial and polite, and yet I sensed through his demeanor that there was more, perhaps even a story in the works that was not yet ready to be shared.

Salaries For All, Even For Gig Workers

October 16, 2019 “If we don’t solve the problems, there’s just a nightmare coming.”

“If we don’t solve the problems, there’s just a nightmare coming.”

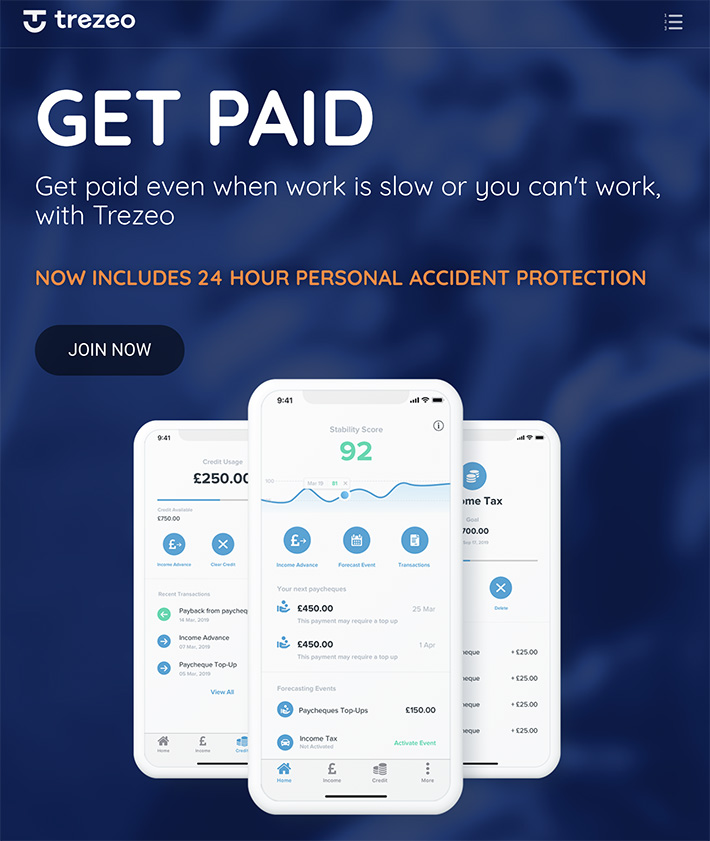

This is how Trezeo’s CEO and Co-founder Garrett Cassidy views the work that he and his company are doing. Created in 2016 with the aim to provide support to self-employed people via income smoothing, Trezeo offers workers whose income streams may be irregular the opportunity to have structured and regular paydays similar to those who earn a salary. And with the number of self-employed in the UK currently at approximately five million, as well as projections showing that the majority of US workers will be freelancers by 2027, the company sees its efforts as essential to solving future problems. “There’s a lot of noise around the gig economy,” Cassidy asserted. “But the world is moving that way and we’re very much like ‘that’s fine, you can push back all you want, it’s going that way and we need to create the services that will work for these people.’”

The way it works is that Trezeo serves as an alternative lender, offering regularly paid funds to the customer’s account in exchange for their income that comes in at a later date. A major difference between it and other alternative lenders though is that Trezeo does not charge interest on these advances, instead collecting its revenue from a weekly membership fee of £3.

“We want to allow them to build their own financial resilience and also start looking a bit more useful for traditional financial institutions to engage with,” Cassidy explained. “Our ultimate vision is if you choose to be freelance or self-employed why should you cut yourself off from financial security, why should you trade flexibility for security, and, therefore, that’s the whole ethos of the income smoothing.”

Beyond this service Trezeo has plans to include additional features, such as an income verification system that would help workers be approved for large loans, like mortgages, from banks; as well as an opt-in pension, where instead of being committed to paying a fixed amount each pay cheque, customers could pay 5% of their total income for that period. Trezeo has already gotten the ball rolling with such expansions with the release of its personal accident and disabilities insurance, which covers customers for £300 per week for six months in the case that they are unable to work.

While it may sound as if self-employed and freelance workers are signing up for Trezeo to be their surrogate employer, Cassidy is quick to emphasize that this is instead a new system built to reflect the opportunities presented by technology, distant but reminiscent of the employment structures that came before.

“We’re trying to recreate [the structure] in a way so that a self-employed person controls it and over time can decide what they want … We’re not trying to make them employees, we’re very careful about that, but we’re trying to make it an employee-like experience for them so that they can very easily manage their finances and see them like an employee traditionally would … Platforms are making it easier for people to take the choice of flexibility.”

Speaking to Cassidy in Trezeo’s Irish office in the National Digital Research Centre, an early stage investor in tech companies, we’re snuggly located close by St. James’s Gate Brewery, where the cobbled streets are filled with the nutty and barley-laden smell of Guinness being brewed.

From here is where the development team operates, whereas the risk, sales, and marketing teams work from their London office, with the UK being their only market at this time. However Cassidy assured me that the company is looking interestedly abroad to Western Europe and America with plans to expand.

“This is a very big niche globally,” Cassidy remarked. “And as we’ve gone along, we’ve realized how much of an impact we can have.”

The Broker: Funding Businesses The Irish Way

October 10, 2019 I’m sitting in the lobby of The Marker Hotel, a 5-star 7-story property on the edge of Dublin’s Grand Canal Dock. Here in Ireland’s major tech hub, I’m waiting for a self-identified corporate finance broker by the name of Rupert Hogan, the managing director of BusinessLoans.ie. Outside of our email exchanges, I don’t really know what to expect. I’ve met brokers from the US, Canada, Mexico, UK, and Hong Kong, but never Ireland.

I’m sitting in the lobby of The Marker Hotel, a 5-star 7-story property on the edge of Dublin’s Grand Canal Dock. Here in Ireland’s major tech hub, I’m waiting for a self-identified corporate finance broker by the name of Rupert Hogan, the managing director of BusinessLoans.ie. Outside of our email exchanges, I don’t really know what to expect. I’ve met brokers from the US, Canada, Mexico, UK, and Hong Kong, but never Ireland.

When he arrives, he doesn’t disappoint. Hogan is full of energy and enthusiasm. He has a natural charisma and friendly manner that’s well-suited for a relationship-based business. It just so happens that SME finance in Ireland is still heavily reliant on person-to-person contact and Hogan is at the forefront of helping potential borrowers look beyond the bank for their financing needs.

SMEs are looking for speed and ease in the loan process, Hogan says. Historically, business owners would call on their bank for financing, invoking the sanctity and reliability of decades-old personal relationships, but Hogan explains that relationships between SMEs and banks just aren’t what they used to be. “[SMEs] feel like they’re going to get the runaround,” he says.

That’s where he comes in. And it could be any kind of business, he explains. Hogan jumps from a call with an import/export business to one in retail, followed by one with an agricultural equipment company. He has to understand a bit about them all no matter what it is, to figure out a proper financial solution. BusinessLoans.ie doesn’t charge for their service but they do receive a commission from the financial company if a deal closes.

That’s where he comes in. And it could be any kind of business, he explains. Hogan jumps from a call with an import/export business to one in retail, followed by one with an agricultural equipment company. He has to understand a bit about them all no matter what it is, to figure out a proper financial solution. BusinessLoans.ie doesn’t charge for their service but they do receive a commission from the financial company if a deal closes.

“Corporate” finance may evoke images of big city corporations engaged in international commerce but Hogan’s company can connect SMEs with as little as €5,000 through an unsecured business loan or merchant cash advance. Invoice Financing, leasing, and trade finance are also tools at his disposal. It’s not all small, however, as he hands me a rate sheet for one lender that will go up to €25M. Interest rates on these products when compared with their American and UK brethren are quite reasonable, and suggest also that the target clientele is not subprime.

As we sit there drinking coffee, Americano style in my honor, an executive for a local SME lender happens to spot him while passing by. After they exchange pleasantries, Hogan explains to me that he submits deals to that lender through their online broker portal. And so I ask him if doing everything online has become the standard in Ireland.

“It’s getting there,” he says, while acknowledging there’s still a ways to go with the population that’s conditioned to handling their financial dealings offline. The company’s domain name is perhaps perfectly positioned to capture that transitioning audience. When businesses decide to look for a loan online, he explains, “I hope they go to BusinessLoans.ie”

How Ireland’s Spark Crowdfunding Got its Start

October 5, 2019 “We’ve not invented anything new,” Chris Burge, CEO of Spark Crowdfunding, tells me. “We saw the rise of crowdfunding in Europe, the states, and the world and we thought, ‘well why doesn’t Ireland have one?’”

“We’ve not invented anything new,” Chris Burge, CEO of Spark Crowdfunding, tells me. “We saw the rise of crowdfunding in Europe, the states, and the world and we thought, ‘well why doesn’t Ireland have one?’”

We’re in the lobby of a Dublin hotel drinking coffee, right around the corner from Spark’s offices on South William Street. There are at least three other professional meetings going on over variations of hot drinks, the room serving as a haven from the uniquely cold-yet-clammy weather outside.

Burge tells me about how he came to be in alternative finance. An engineer by trade, Burge entered the field after both him and his business partner had found the traditional process of investing to be wanting. “Both of us had invested in the past and had found it cumbersome, long-winded, and expensive,” leading them to explore more accessible, less unwieldy options.

Thus, from such a hole in the market sprung Spark Crowdfunding. Offering equity investment options from as low as €100, Burge sought to streamline the investment by offering it via an online platform from which members can view pitch videos, pitch decks, and detailed documents.

Established in early 2018, the company saw its first big success in August of that year with Fleet, an Irish business that allows cars owners to rent their vehicles to the public from their driveways as well as gas stations. Asking for €275,000, Fleet received this and more, with the total amount invested reaching €385,000.

Established in early 2018, the company saw its first big success in August of that year with Fleet, an Irish business that allows cars owners to rent their vehicles to the public from their driveways as well as gas stations. Asking for €275,000, Fleet received this and more, with the total amount invested reaching €385,000.

Allowing for choice when deciding which investors to choose from and how much to take from who, Burge says that flexibility is key to their platform and likens it to Dragons’ Den with much more than five potential investors.

And with bank loans for small businesses becoming increasingly more difficult to access, Spark is positioned similarly to crowdfunding in the US. “Where a company would have previously gone to Allied Irish Bank or Bank of Ireland to borrow €100,000 in order to get their business off the ground, they’re now finding it very difficult and nigh impossible as well to get these loans, so we found that a lot of companies are coming to us to do this.” In addition to such an investment, startups in Ireland may receive extra funding from Enterprise Ireland, a government organization that provides aid to indigenous businesses and will match investments up to a point so long as the company meets certain requirements.

Accompany this with the lack of regulation in the crowdfunding space in Ireland and it would appear that the industry is set to expand.

And on the topic of expansion, Burge is keeping most of his cards to himself. “We know that Ireland is a small country compared to the rest of Europe, or compared to the rest of the world, so there’s a limited amount of stuff that we can do here, and so do we want to grow? Yes. Are we going to go to the states? Probably not. But the rest of Europe? Yes, absolutely. Have we picked out a few countries? Yes, we have.”

How Linked Finance is Linking Irish SMEs With Quick Loans

October 1, 2019 Google Maps was convinced that I was already at my destination, but that didn’t make sense because I was still sitting in my cramped Airbnb rental apartment in Dublin and hadn’t left to go anywhere yet. “Oh man please tell me Google works in Ireland,” I said to myself while glancing at the time and counting how many minutes I’d be late to my first meeting.

Google Maps was convinced that I was already at my destination, but that didn’t make sense because I was still sitting in my cramped Airbnb rental apartment in Dublin and hadn’t left to go anywhere yet. “Oh man please tell me Google works in Ireland,” I said to myself while glancing at the time and counting how many minutes I’d be late to my first meeting.

I was on my way to Linked Finance, a peer-to-peer SME lender based in Dublin. Their office was uncannily close to where I was staying on Liffey Street Lower, just steps away from the Ha’penny Bridge. So close in fact, that Google Maps believed that I was going to and from the same location. I breathed a sigh of relief at the realization and ventured the short distance to the elevator that promised to deliver me to the inner universe of Irish fintech.

Alan Fagan, the company’s head of marketing, greeted me at the door. Fagan joined the company in 2015, two years after its founding. As we walk in, I notice the prominent display of the Linked Finance logo amid an ocean of eye-popping orange. The look, the feel, suddenly I feel transported to the tech scene in San Francisco. The accents overheard in the background, however, suggest I am most definitely in Ireland.

Alan Fagan, the company’s head of marketing, greeted me at the door. Fagan joined the company in 2015, two years after its founding. As we walk in, I notice the prominent display of the Linked Finance logo amid an ocean of eye-popping orange. The look, the feel, suddenly I feel transported to the tech scene in San Francisco. The accents overheard in the background, however, suggest I am most definitely in Ireland.

We sit down. Tea is offered. I decline. Fagan gets right into it and he sings a familiar song, that it can take a very long time for a business to get a bank loan.

It can take up 8 weeks to get funded, he says. “SMEs are the biggest employer in the country,” he explains, while hinting that facilitating loans to this demographic is as much a patriotic endeavor as it is a business one.

The nation’s Central Statistics Office puts the number of active enterprises in the private business economy at over 250,000. As of June, Linked Finance had made more than 2,100 loans for a grand total of more than €100 million.

Fagan gives me a demonstration of the platform, where individual investors (or peers) can see the name and location of the businesses whose loans are available to fund. An investor can even sort the listings by county, of which there are 26 in the Republic. Linked Finance does the underwriting, something they can do within 1 day, Fagan says.

The underwriting is tight. “We’re not a lender of last resort,” Fagan explains. They put themselves on the same (or better) credit risk footing as banks and claim that they’re able to assess risk and provide funds in a much more efficient manner. “We feel we do it better than banks,” Fagan says.

Most loans close quickly, thanks in part to their Autobid tool. Investors can be from anywhere so long as they’re over 18 and have a European Union bank account. Annual interest rates on the loans range from 6% to 17.5%.

Fagan says that although they are an online lender, many borrowers in Ireland still appreciate personal relationships. They can accommodate applicants that prefer a personal walk-through by a real person and that it can actually leave a memorable impression on their customers.

Marketing is done via a variety of direct methods but also through channel partners like accountants and financial advisors. A big name asset manager, Paris-based Eiffel Investment Group, with €1.5B under management, is among the loan investors on the Linked Finance platform.

I keep waiting for the caveat, an obstacle or twist in the model so inherently Irish, that somebody like me from half a world away would never truly grasp. But there isn’t one. The market is overtly familiar, yet more reminiscent of the UK than the States. Ireland lacks the robust regulatory framework of both countries, however. Despite that, the government does not appear to be holding the industry back. In June, Paschal Donohoe, the Minister for Finance, the government official responsible for all financial and monetary matters of the state, said “availability of credit is a key consideration for all businesses, and I am aware of the role peer to peer lending is playing in broadening competition in the SME finance market.”

Indeed, such competition has made credit more available in markets abroad.

As our time together winds down, I mindlessly attempt to plot my trip back. “Siri, take me home,” I speak into my phone. The Maps app opens and then loads to reveal a double entendre. It seems I am already very much there.