MPR Authored

Here Comes Lending Club

October 17, 2013 As highlighted in BusinessWeek, Lending Club has finally entered the small business lending market. Some of you might say, “bahh… so what!” but you should be paying attention. Lending Club recently got a valuation of $1.55 billion when Google bought a piece of them back in May. To put that in perspective, that’s about 15x the enterprise valuation that RapidAdvance got in its acquisition by Rockbridge Growth Equity. A monster has entered the ring and it doesn’t matter if it’s peer-to-peer lending, because they’re targeting the same market. What Lending Club does isn’t much different than what the typical merchant cash advance industry does these days anyway. Both thrive on syndication, though one relies on a handful of partners and the other relies on tens of thousands of partners. Both are bank loan alternatives and both can get you funded within days.

As highlighted in BusinessWeek, Lending Club has finally entered the small business lending market. Some of you might say, “bahh… so what!” but you should be paying attention. Lending Club recently got a valuation of $1.55 billion when Google bought a piece of them back in May. To put that in perspective, that’s about 15x the enterprise valuation that RapidAdvance got in its acquisition by Rockbridge Growth Equity. A monster has entered the ring and it doesn’t matter if it’s peer-to-peer lending, because they’re targeting the same market. What Lending Club does isn’t much different than what the typical merchant cash advance industry does these days anyway. Both thrive on syndication, though one relies on a handful of partners and the other relies on tens of thousands of partners. Both are bank loan alternatives and both can get you funded within days.

Back in 2009, the only short term financing opportunities small businesses had was merchant cash advance. There really wasn’t anything else. There were banks or there was merchant cash advance… and banks weren’t lending. Now there’s a whole spectrum of bank loan alternatives and to say that they operate in markets that don’t compete with each other is crazy.

There was a time when folks said Kabbage was not a competitor in the merchant cash advance space. Now they’re synonymous with merchant cash advance financing, have patents that specifically use the merchant cash advance terminology, and they fund brick and mortar businesses. On Deck Capital supposedly wasn’t a competitor back in 2007 because they did loans with fixed daily ACH. On Deck wanted only the high credit merchants that wouldn’t settle for a cash advance and now they compete head to head with everyone else.

The market is all over the place with pricing and structures. Factors range from 1.09s to 1.50s. Deal terms range from 6 weeks to 24 months. For those already annoyed that there has been downward pressure on rates for high quality clients because of what it has done to margins, you may have more to worry about with Lending Club.

I’ve personally referred consumer loan deals for a commission to Lending Club in the past and they went pretty smoothly. They said if they approve a loan, it will basically fund within days. They don’t have any worry about approved loans not raising enough capital to be funded from syndicates/investors/participants. They said almost every approved loan funds. They also charge between 6.5% and 29.99% APR and make loans with terms of 3-5 years. Try competing against that.

Now I don’t know what repayment time frame will be offered on their business loans, but I do know that they’re used to making loans for very low interest over a much longer term than a merchant cash advance company. Something tells me that they won’t stray too far from that and they’re going to disrupt the market (the premium market anyway) on price and time frame more than a few other companies already have.

Granted, I will admit that Lending Club on the consumer side generally only approved applicants with higher than 680 FICO and a low debt-to-income ratio and I don’t think they’ll change that. That means they won’t be a competitor initially for a large chunk of the market. Lending Club will probably butt heads with On Deck Capital, NewLogic Business Loans, and all the premium 12 month programs floating around out there.

Peer-to-peer lending is part of the broader merchant cash advance industry. Deals fund quickly, the capital is unsecured, there’s little paperwork involved, and the deals are syndicated. Hence, Lending Club is now a competitor.

Being owned by Google also can’t hurt. Lending Club is typically ranked at or near the top of the 1st page for the search query, “unsecured business loans.” Coincidence?

Get ready for Lending Club. They won’t be the last billion dollar plus company to throw their hat in the ring.

—

Note 1: An edit was made to correct Rapid’s valuation as an enterprise valuation, which one insider noted can be substantially different than a raw equity valuation. That makes Lending Club likely a lot more valuable in comparison.

Note 2: I initially reported that Lending Club owned Dealstruck.com. This is not correct. Dealstruck.com has previously been reported to be the Lending Club of the small business space in the characteristic way of how they structure deals, but they are not actually part of Lending Club. Thanks to Darrin Ginsberg of Super G Funding for pointing out my mistake.

More on DailyFunder about this topic: http://dailyfunder.com/showthread.php/451-lending-club

The Entrepreneur

October 13, 2013 They paint their faces, they unsheathe their swords. They look fearless even if they are in fact full of fear. Some wear a full body of armor and others have no armor at all.

They paint their faces, they unsheathe their swords. They look fearless even if they are in fact full of fear. Some wear a full body of armor and others have no armor at all.

We’ve all seen them, but they are not easily understood. The entrepreneur storms the castle not because he believes he will be victorious in doing so, but because he believes the castle must be stormed. He does it with a purpose and intent that is all his own. Some do it for riches and some for recognition. Others do it simply to change the status quo.

Call it an innate desire for conquest in modern times. An empire of widgets or influence is not much different than the empires of land and resources of yore. When an entrepreneur looks in the mirror, he sees his blood, his sweat, his tears. He sees scars that others cannot. Eyes burning, jaw clenched, he reminds himself that he will not go quietly into the night.

There is an acknowledgement that even if the worst should happen and the pursuit fails, that all has not been in vain, that it was a great honor to have gone down trying than to have not tried at all. One should imagine each failed startup contributing to a greater purpose, as felled warriors being greeted by the ancient valkyries of Valhalla.

Every entrepreneur has that first moment. The moment where they finally take the plunge and risk it all. It’s a moment they can’t take back and wouldn’t even if they could. Completely surrendering to the risk of total failure to pursue self-created success is an event that forever changes a man’s psyche. So empowered is that individual when they exchange their hard hat and workman’s gloves for a battle axe and chainmail. It’s as if pandora’s box opens and all at once they learn that they and they alone control their destiny.

Metal clangs, horses neigh. The entrepreneur roars and charges ahead. The crowd wonders, “why does he do it?” and the enemy wonders the same. Sword unsheathed, gaze steady, fearless looking even if full of fear. Not everyone can be like them. Some wear armor and others not at all. They come from all different backgrounds and circumstances. They storm the castle not because they believe they will be victorious, but because they believe the castle needs to be stormed. They do it because they must do it, because there is no going back. They do it for riches, for recognition, for change, for passion, for happiness, for love, for the challenge, for conquest, for their honor…

Are you an entrepreneur?

Were You at the WSAA Conference?

October 9, 2013We didn’t make it to the Western State Acquirers Association Conference this year, but Merchant Cash Group did and they were nice enough to send over some photos from the show:

Merchant Cash Advance companies are going to a lot more conferences than they used to. At the Money2020 Conference in Vegas right now for example, Kabbage, Strategic Funding Source, On Deck Capital, and Capital Access Network are not only in attendance, they’re sponsors.

Update: Strategic Funding Source let us repost their photos on twitter of Money2020:

Come and find us #money2020 pic.twitter.com/560EDbTM2J

— Strategic Funding (@SFSCapital) October 7, 2013

Is a Merchant Cash Advance conference in the cards for the future? I floated this idea before back in April 2012 and I’ve heard other people mention it too.

Is PayPal’s Working Capital Program a Mistake?

October 5, 2013 A few weeks ago, PayPal announced the launch of their Working Capital program as a way to help small businesses in need. They classify it as a loan but the explanation for how it works is textbook merchant cash advance. A percentage of each PayPal sale is withheld and applied as a reduction to the merchant’s balance. PayPal joining the booming merchant cash advance/alternative lending market is really no surprise. After all, RapidAdvance just got acquired by the same group that owns Quicken Loans. We’re in a new era of alternative finance.

A few weeks ago, PayPal announced the launch of their Working Capital program as a way to help small businesses in need. They classify it as a loan but the explanation for how it works is textbook merchant cash advance. A percentage of each PayPal sale is withheld and applied as a reduction to the merchant’s balance. PayPal joining the booming merchant cash advance/alternative lending market is really no surprise. After all, RapidAdvance just got acquired by the same group that owns Quicken Loans. We’re in a new era of alternative finance.

PayPal is respected as a payments company but are they ready for the high risk world of merchant cash advance financing? Critics are not so sure. Industry insiders have watched dozens of funding providers jump into the market with aggressive rates, attempt to undercut the competition, and acquire a lot of marketshare. The results are usually disastrous.

For years, journalists believed that the high cost of capital provided by non-bank lenders was fueled by the desire for immense profit. They didn’t understand the risks involved or realize that some funding providers weren’t even turning a profit at all. Last year, Opportunity Fund, a non-profit small business lender revealed that to make loans at 12% APR would fail to even cover costs. The for-profit sector of the industry charges factor rates (different than Annual Percentage Rates) between 1.14 and 1.50, not including fees. I explained this variance once before in The Fork in the Merchant Cash Advance Road.

So did PayPal learn anything from an industry that has been in existence for 15 years? It doesn’t look like it:

Doing some simple math (Total to be repaid / Loan Amount), the factor rates range from 1.04 to 1.12, figures that will probably only make sense if their average client has greater than 720 FICO, many years in business, and is virtually perfect on paper and in reality. Perhaps PayPal knows that and will decline 95% of applications or perhaps they believe their clients will buck the trend. I mean, is it possible that a corporate monster like PayPal could make a boneheaded mistake?

A 1.04 deal? Seriously? This has disaster written all over it. There are some people that believe that the losing proposition is intentional…

You can follow the discussion about this on DailyFunder.

Google Penguin 2.1 Takes Swing at Merchant Cash Advance Industry

October 5, 2013 If you noticed a shuffle in search rankings for industry keywords last night, it’s because Google unleashed Penguin 2.1.

If you noticed a shuffle in search rankings for industry keywords last night, it’s because Google unleashed Penguin 2.1.

Penguin 2.1 launching today. Affects ~1% of searches to a noticeable degree. More info on Penguin: http://t.co/4YSh4sfZQj

— Matt Cutts (@mattcutts) October 4, 2013

Penguin focuses on spammy or purchased backlinks so if you did one or the other, you probably got harmed. Given the high cost of traditional marketing and Pay-Per-Click Internet Marketing, many funders, ISOs, and lead generators have turned to SEO to boost their visibility in organic search. Whether undertaken by inside employees or outside contractors to do the job, there is no doubt that building links has been part of the strategy. Some have had major success in rising up through Google’s search results but most haven’t. It’s not easy getting to page 1, but if you get there, don’t celebrate. You won’t be there forever.

Less than two weeks ago on DailyFunder, someone took to the board to pat themselves on the back for ranking #2 for the keyword: merchant cash advance. Wikipedia is #1. They admitted it took a lot of hard work over the course of 8 months. Last night they were thrust back to position #65. That’s on page 7 where they will never be found. 8 months of work for 2 weeks of ranking. You might be saying, “Well my SEO guy will just roll with the punches and get us right back.” Unfortunately with Penguin, it doesn’t work that way. Penguin is basically a permanent penalty, an algorithmic barricade to prevent you from ever ranking for your keywords again. According to a poll on Search Engine Roundtable, only 7% of respondents claimed to have made a full recovery after Penguin 2.0. Most SEOs would advise that you torch your domain, buy a new one and start a whole new website. That’s not exactly an easy thing for a big brand or company to do.

There’s a flaw in all the SEO being done in the merchant cash advance industry anyway and that’s the notion of being on page 1 to begin with. If you read David Amerland’s Google Semantic Search, he explains that “there is no longer a first page of Google”. The results you see on the first page of Google depend completely on whether or not you’re using a desktop or mobile device, what zip code you’re accessing the internet from, what you’ve searched for in the past, and whether you’re logged into your gmail account. And if you use Google+, then forget it! The first page results for someone that uses Google+ are ultra personalized. To rank on their first page, they’ll pretty much need to follow you socially first.

So if you’re thinking about ranking higher in search as a means to generate more leads, you sure as heck better understand how the results work these days. What you see on your screen is not what I see on mine. A site that’s #65 for me, may be #4 for you.

The other angle of Google’s foray into Semantic Search is their desire to be an answer engine, not a search engine. Google wants to answer questions for searchers without them having to click a link. Here’s an example of Merchant Processing Resource acting in that role:

What is voice authorization you ask? Boom! Answered! No need to click anything. That’s where search is going. What this means for companies that are trying to get customers is that they either need to become the absolute authority within their industry or they need to throw in the towel and do Pay-Per-Click.

When I search for merchant cash advance from my desktop in NYC, 7 out of the top 10 results are not company pages, which is astounding considering how much effort companies are putting in to rank high for this keyword. I see:

- 1 Wikipedia

- 4 News articles

- 1 Press release

- 1 Youtube video

Did you get hit by Penguin 2.1? Are you optimized for Semantic Search?

Previous merchant cash advance SEO articles:

- Your Merchant Cash Advance Press Release May be Hurting You 8/8/13

- Is Google Your Only Web Strategy? 12/31/12

- The Other 93% 7/13/12

- Google Penguin Kills Survivors 5/6/12

- The SEO War Continues 4/4/12

- The SEO War for Merchant Cash Advance 2/12/12

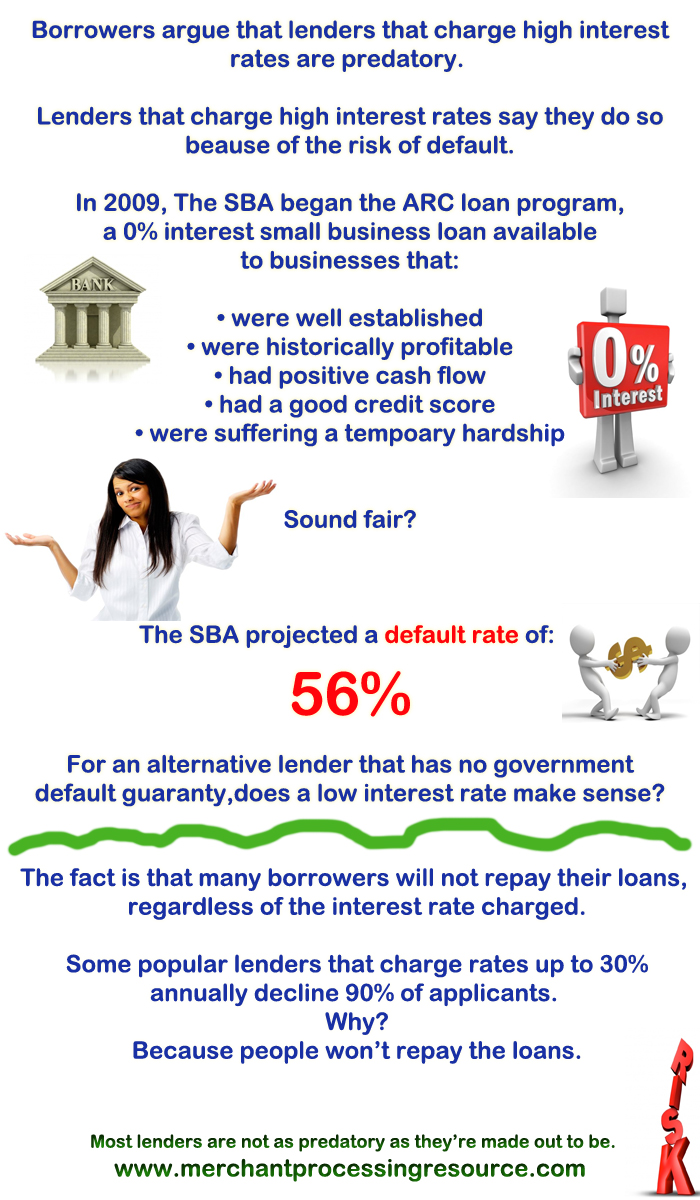

Pop Quiz: Would No Interest Mean No Defaults?

September 21, 2013Bring interest rates down to zero and nobody would default right??? Every single borrower has a risk of delinquency or default irrespective of the interest rate. Everyone.

Read the now defunct ARC Loan procedural guide:

SBA’s ARC Loan Procedural Guide

RapidAdvance Becomes Part of The Quicken Loans Family

September 18, 2013This is a follow up to the RapidAdvance/Rockbridge Growth Equity announcement a couple days ago. We now know that RapidAdvance got an enterprise valuation in excess of $100 million. RapidAdvance will become part of the Quicken Loans Family of Companies. Jeremy Brown will be continuing his role as CEO. I share his feelings on this transaction being especially historic because it is the first non-distressed acquisition of a merchant cash advance company. See the letter that was e-mailed below:

Loans for Likes

September 17, 2013How Kabbage is building a social media marketing empire

Take a look at what Kabbage has cooked up:

Like Kabbage on twitter or Facebook and your approval amount gets extended automatically. This helps Kabbage accomplish two goals:

1. Spread awareness about their brand to the followers of the people Liking and following them.

2. Identify the public social media accounts the business is using so it can monitor what they’re doing.

You can learn about how Kabbage feels about businesses that aren’t using social media in the patent’s summary. Under Description, Section 2:

You can learn about how Kabbage feels about businesses that aren’t using social media in the patent’s summary. Under Description, Section 2:

Social networking is growing at an exponential rate and businesses that are not exploiting social networking sites such as FACEBOOK and LINKEDIN are considered falling behind the times.

So why is this a patentable invention? A merchant’s approval amount is increased automatically by an algorithm that checks to see if a merchant performed the action of Liking or Following. So if you think that’s a great idea and want to do something similar, you’re a bit late. Better Call Saul… I mean Kabbage to license the use of such technology. It works as such:

The above aspects can be obtained by a system that includes (a) approving, by a cash provider, a user for a cash line wherein the user is permitted to receive cash up to the cash line; (b) causing an offer to be displayed on an electronic output device associated with a user’s computer, the offer being to increase the cash line when the user takes a particular action comprising associating the user’s social networking account with the cash provider; (c) determining that the user has taken the particular action; and (d) automatically increasing the cash line.

The term merchant cash advance is explicitly used twice in the patent but it also goes to cover any kind credit line or loan being program. This is actually an incredible patent to be in possession of because it’s such a great idea. Imagine telling a merchant approved for 5k, that they will get an extra $200 just for following you on twitter and another $200 just for liking you on facebook. It may not seem like much on a $250,000 deal but Kabbage does a lot of smaller sized advances where the $400 combined approval bump is a sweet incentive for merchants.

Marketing in this industry is expensive and this is one of the more innovative models I’ve seen.