Shopify Launches Merchant Cash Advance Program

April 27, 2016

Shopify (NYSE:SHOP), the online storefront software company that went public a year ago, announced today that it has formally launched a merchant cash advance product.

“For many merchants, securing capital is a frustrating and time-consuming process,” said Saad Atieque, Product Manager at Shopify. “With Shopify Capital, we’re giving entrepreneurs a simple, fast, and convenient way to secure financing to invest in their business. Similar to our payments and shipping solutions, Shopify Capital represents one more way Shopify can help entrepreneurs strengthen their business operations.”

The company’s release referred to it specifically as a merchant cash advance. “During the pilot program, merchants used Shopify Capital merchant cash advances to buy equipment and inventory, launch new products, hire more employees, and add new channels and products.”

Although Shopify is headquartered in Canada, the program will initially only be available to small businesses in the US.

The company closed yesterday at $31.47, nearly twice its $17 initial public offering.

Transact 16 Photos

April 26, 2016Did you miss Transact 16? It was a little bit different this year for a particular group of regular attendees that have historically relied on credit card processors to “split” transactions. Merchant cash advance as it is known (or was known) has officially evolved into something else. You can read more about that here.

In the meantime, here’s a few photos from the show:

Don't forget to stop by Booth 564 @ETATRANSACT #TRANSACT16 & ask TJ/Maria/Jim how we can help you do great things! pic.twitter.com/Gixc6WJNfV

— RapidAdvance (@Rapid_Advance) April 21, 2016

Where are the rest of the pictures you ask? You should know by now that what happens in Vegas stays in Vegas.

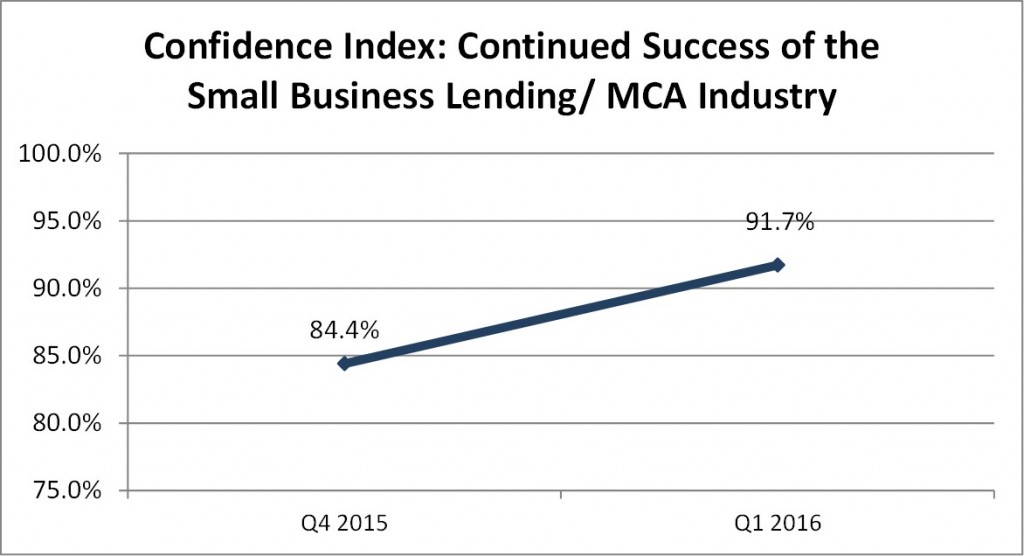

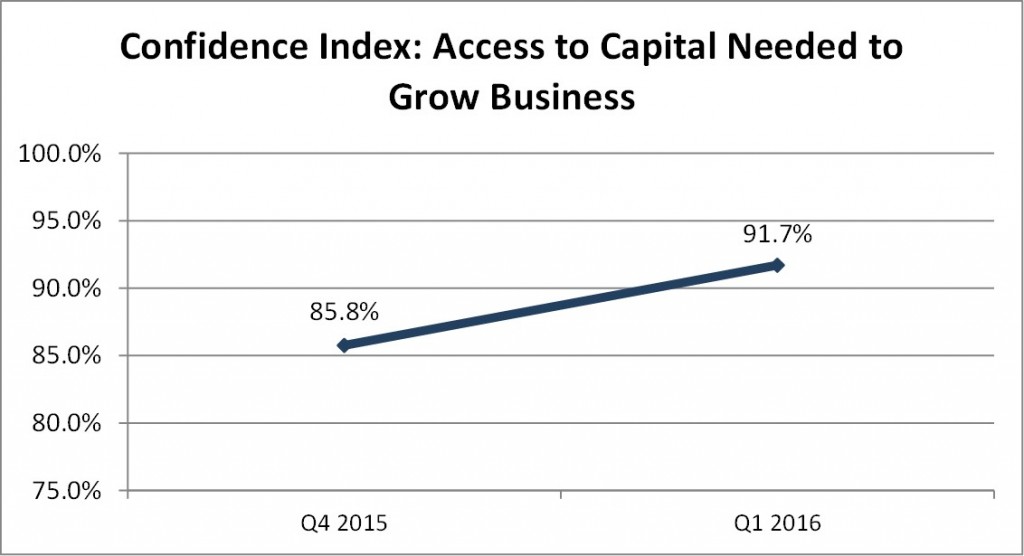

Small Business Lending and Merchant Cash Advance Industry Confidence On The Rise

April 25, 2016A fresh survey of industry captains revealed that their confidence is actually increasing.

Late last year, deBanked and Bryant Park Capital teamed up to produce the first ever comprehensive industry report on merchant cash advance and small business lending. More recently, eligible participants took a narrower survey to gauge their confidence in Q1 2016 and that was compared to results measured in Q4 2015.

The results were striking. Despite the apparent end of a euphoric love affair between investors and marketplace lenders earlier this month at LendIt, those on the small business side are still feeling very optimistic.

Confidence among industry captains increased from 84.4% in Q4 2015 to 91.7% in Q1 2016.

Confidence among industry captains in their ability to access capital needed to grow their business increased from 85.8% to 91.7%.

The 2015 comprehensive report is available for $495. Please contact sean@debanked.com for more information.

Having Problems With Leads? Don’t Feel Alone

April 24, 2016

Having problems with leads? Don’t feel alone. Funders and lead providers say response rates to offline marketing have been cut in half while the price of pay-per-click campaigns has skyrocketed. They blame intense competition in an increasingly crowded field of funders, market saturation by lead generation companies, better email spam filters and comparison shopping by small-business owners who are becoming more savvy about how much they need to pay for merchant cash advances and loans.

Clicks that cost $5 each seven years ago now command a price of nearly $125, says Isaac Stern, CEO of Yellowstone Capital LLC, Green Capital and Fundry. “Pay-per-click marketing has gotten out of control,” he laments. “So you need a hefty, hefty budget to compete in that world.” He reports spending $600,000 to $700,000 a month on internet marketing, compared to $100,000 monthly on direct mail.

Even when the price of individual clicks isn’t measured in hundreds of dollars, the cost of the multiple clicks required to create a lead can mount up, according to Michael O’Hare, CEO of Blindbid, a Colorado Springs, Colo.- based provider of leads. If it takes 15 clicks that cost $25 each to obtain a lead, that comes to $375, he notes. Still, some companies manage to use key words that cost $8 or so per click to get decent leads for less than $100, he says.

While the cost of pay per click is exploding, the response to direct mail marketing is declining precipitously, says Bob Squiers, who owns the Deerfield, Fla.-based Meridian Leads. The percentage of small-business owners who respond to advertising they receive in the mail has fallen from 2 percent just a few years ago to 1 percent now, partly because they receive so many mailings from so many more lead-generation companies, he says. “There weren’t too many people doing direct mail into this space five years ago,” he notes. His company’s leads range in price from pennies to $60, he says.

While Blindbid and Meridian both specialize in finding leads by sending out direct mail pieces and then qualifying the respondents in phone conversations, one of their competitors, Lenders Marketing, takes a different approach, according to Justin Benton, sales director for the Camarillo, Calif.-based company. Benton’s data-driven method combines his company’s databases with the databases of financial institutions. He cultivates relationships with the banking industry’s executives to facilitate that process, he says, and his company does not make phone calls to qualify leads.

But placing too high a value on data gives rise to two problems, the way O’Hare views the search for leads. First, analyzing the data creates plenty of challenges, he says. Second, human beings just aren’t rational enough in their decision-making to fit data-driven profiles or cohorts, he maintains. “The holy grail is to find some algorithm that will predict that a merchant needs funding, and they can then find these people through massive data,” he says with skepticism.

Whatever path a company takes to finding and verifying leads, it pays to establish three elements before classifying them, O’Hare says. First, prospects should qualify financially for credit or advances. Second, prospects should demonstrate a genuine interest in obtaining funding, as opposed to less-than-serious “tire kicking.” With both of those characteristics in place, O’Hare informs prospects they can expect to hear from funders.

Blindbid also wants to guide the expectations of the funders who are calling the leads, O’Hare says. To that end, the vendor invites funders to listen to recordings of the phone calls it makes to qualify leads. Just the same, funders should bear in mind that they may not receive the same reception when they contact the lead, he cautions. “We see it all the time, he says. “We speak to the merchant in the morning and they’re pleasant. Then in the afternoon when they speak to the funder or the broker, the merchant is grumpy.”

Retailers’ mood swings aside, funders can soon gauge the quality of the leads they’re buying. “You can’t judge a lead on cost, Squiers admonishes. “Judge them by performance.” However, performance fluctuates according to the funder’s sales skills, product offering and product knowledge, he maintains.

Meanwhile, the problems plaguing the lead business should prompt funders to become creative in their approach to finding prospects. That’s why even vendors who make their living selling leads encourage funders to search for prospects on their own. “We always advise generating your own leads,” says Benton. “The only leads you can truly count on are the ones you generate yourself.”

Meanwhile, the problems plaguing the lead business should prompt funders to become creative in their approach to finding prospects. That’s why even vendors who make their living selling leads encourage funders to search for prospects on their own. “We always advise generating your own leads,” says Benton. “The only leads you can truly count on are the ones you generate yourself.”

Knowing where to look for leads can require a thorough grasp of what’s happening in a particular market. “You can look at what industries are hot,” O’hare suggests. The trucking business is heating up, for example, because so many truckers need funding to buy expensive equipment to meet new requirements for electronic logs, he says. Meanwhile, the recession has wracked the martial arts industry, so dojos might require funding for marketing to help them recover, he notes.

Understanding every industry in that much detail isn’t practical, so lead generation companies urge funders to specialize in just a few niches. Building a network of customers who know each other can result in referrals, Benton observes. It also soothes skeptical prospects, he notes. “Once you say I’ve worked with Fred down at Tony Roma’s – they can feel more comfortable, especially if you’ve done it in the same city,” he maintains.

Whether leads arise internally or come from a vendor, funders have to work them properly to succeed in closing deals, lead-generating companies agree. “The real key is being consistent and persistent,” Benton says. “Research has shown the average lead is called 1.3 times, so once you make that second call you are ahead of the curve.” He advocates that funders use their CRM system by taking copious notes on their calls, setting up nurture campaigns and following up with leads in an organized manner.

And don’t forget that at least some prospects are getting pummeled with calls. “A lot of brokers are carpet bombing – they’re on the phone all day,” says O’Hare. “I talked to one guy who said he makes 400 or 500 calls a day on a manual dial. I’d like to do a video of that.

Alternative Small Business Financing Company Secures $70 Million

April 22, 2016Brean Capital has successfully helped an alternative small business financing company secure $70 million. While the name was purposely undisclosed, sources say it was a Delaware-based company.

According to the announcement, “the financing round consists of a $50 million senior credit facility provided by a multi-billion dollar credit fund, and a $20 million equity investment from a middle-market private equity sponsor.” Proceeds from the transaction will be used by the Company to execute its strategic growth plan.

Brean Capital served as exclusive financial advisor to the Company.

Splits Glitz or Fritz? – Transact 16 highlighted strange chapter in merchant cash advance history

April 21, 2016

It’s Opposite Day in the alternative business funding industry. Lenders are splitting card payments and merchant cash advance companies are doing ACH debits.

Jacqueline Reses was not an odd choice for Transact 16’s Wednesday morning keynote. Square, the company she works for, has continued to be a hot topic in the payments world for years. But what was striking is that Reses heads the lending division, the group that allows merchants to pay back loans through their future card sales. If that sounds very merchant-cash-advance-like, it’s because that’s exactly the product they used to offer before changing the legal structure behind them.

Split-payments, not ACH payments, have literally propelled Square and PayPal to the top of the charts of the alternative business funding industry. One individual on the exhibit hall floor posited that Square’s ability to originate loans through their payments ecosystem was the company’s real value; Payments itself was secondary. It’s a testament to the opportunities that split-payments affords to (as I argued 3 years ago on the ETA’s blog) a company well positioned to benefit from it.

Meanwhile, the companies at Transact that one would have historically described as merchant cash advance companies have mostly transitioned away from split-payments to ACH. Essentially, Square and PayPal embraced splits as an incredible strength while yesterday’s merchant cash advance companies viewed splits as a handcuff that limited scalability. The payment companies became merchant cash advance companies and the merchant cash advance companies became something else entirely, a diverse breed of loan and future receivable originators operating under a label people are now calling “marketplace lenders.” But even Square and PayPal, arguably the two companies at Transact doing the most split-payment transactions, claim to make loans, not advances.

Merchant Cash Advance as anyone knew it previously is dead

Ten years. That’s the average age of the small business funding companies that exhibited at Transact this week. They are but the last remaining players that probably considered the debit card interchange cap imposed by the Durbin Amendment of Dodd-Frank as being among the most significant legislation that affected their businesses.

A senior representative for one credit card processor told me at the conference that their biggest gripe with new merchant cash advance ISOs today is that they know almost absolutely nothing about merchant accounts. It’s not that they know less, they know nothing, he said.

One company was notably absent from the floor this year, OnDeck. They’ve since embraced the marketplace lending community as their home, just as many others have.

Nine years ago, I overheard a very influential person say that the first company to be able to split payments across the Global, First Data and Paymentech platforms would be crowned the “winner” of the merchant cash advance industry and by extension the wider nonbank small business financing space.

If one were to define the winner as the first company from that era to go public, well then those 3 platforms played no role. OnDeck was the first and they relied on ACH payments the entire way. They also refer to themselves these days as a nonbank commercial lender. If that doesn’t sound very payments-like, it’s because it’s not.

What cause is being Advanced?

At least four coalitions are currently advocating on the marketplace lending industry’s behalf, the Coalition for Responsible Business Finance, the Marketplace Lending Association, the Small Business Finance Association, and the Commercial Finance Coalition. The Transact conference is put on by the Electronic Transactions Association whose tagline is “Advancing Payments Technology.” In an age where new merchant cash advance ISOs know nothing about payments, it’s no wonder there’s a growing disconnect.

Could Transact now be one of the best kept secrets?

A few people from companies exhibiting say that they believed they stood a better chance to land referral relationships from payment companies by being there and that there was still a lot of value in landing those deals. Partnerships like these may be why the average exhibitor has been in business for 10 years while today’s new companies relying solely on pay-per-click, cold calling, or handshakes are falling on hard times.

Some payment processors acknowledged that merchant cash advance companies were still a good source to acquire merchant accounts, though the process by which that happens is not the same as it used to be. A lot of it is referral based now, according to one senior respresentative for a card processor. The funding company funds a deal via ACH and then refers them to the payment guy to try and convert that as an add-on. The residual earnings may not be as good as they used to be but that’s because they don’t have to do any work in this circumstance. In a sense, funders are still leading with cash but instead of the boarding process being mandatory, it’s an entirely separate sale that sometimes works and sometimes doesn’t. In that way, small business funding companies can be a good lead source for payments companies.

When I asked the senior representative if they really had success closing merchant accounts just off of a referral from a funding company, he looked at me incredulously, and said, “you used to do this, of course we do. that’s how this whole industry started.”

“What industry?” I asked.

What industry indeed…

Square Capital’s Jackie Reses Reveals Why They Really Gave Up Merchant Cash Advances

April 14, 2016 At Lendit, Bloomberg Reporter Emily Chang asked Square Capital head Jacqueline Reses to explain the real reason behind Square’s shift from merchant cash advances to loans.

At Lendit, Bloomberg Reporter Emily Chang asked Square Capital head Jacqueline Reses to explain the real reason behind Square’s shift from merchant cash advances to loans.

Reses said that it was not a customer issue, but an investor one. “This industry and this conference more than anyone understands the nuance between MCAs and loans,” she said. “From an investor side, that’s really where the savings are between the form of an MCA and the form of a loan, in that there’s an actual repayment date.”

Reading between the lines, she seemed to be saying that investors like certainty and exact terms whereas the traditional merchant cash advance product was harder to sell off or securitize because they lack a defined element of time.

Fast loan approvals shouldn’t be criminalized

Referring to the criticism that online lenders have been getting recently for their fast approvals, Chang specifically asked if companies like OnDeck were approving loans too quickly.

Reses responded, “I don’t think the ability to execute something quickly, smoothly, transparently, should be criminalized as something that requires oversight, and so I think being good at something should be well regarded.” She later added, “I think the notion that credit decisions being swift is a problem is just misguided.”

Transparency

Reses used the word “transparency” several times but in explaining such did not reference the disclosure of Annual Percentage Rates even once. Instead she mentioned the importance of spelling out the total dollar cost to the merchants, subtly reconfirming the findings that are coming from many other alternative lenders.

Was the move from MCA just about investors though?

Read our initial assessment and expanded theory.

Watch the full “fireside chat” video below:

Becoming a ‘Certified’ Merchant Cash Advance Professional is Just Around The Corner

April 11, 2016

Update: 11/4/16 – THE ONLINE COURSE IS HERE. The final version offers test takers the chance to earn a certificate in MCA Basics, specifically the characteristics that make loans different from purchases of future receivables.

A survey conducted last year by deBanked has contributed to the development of a training and certification course for merchant cash advance salespeople. Co-produced by Hudson Cook LLP, deBanked, and other industry veterans, sales representatives that offer the merchant cash advance product will have the opportunity to learn from an online tutorial complete with training videos and quizzes to achieve a new standard of educational excellence.

Being able to expertly understand and communicate the differences between loans and purchases is among the courses’s main goals. Funders and ISOs can supplement their own training procedures with the course. Those that complete and pass it should expect to receive a certificate.

While it’s not ready to go live just yet, Hudson Cook partner Robert Cook, says he will be available at the Lendit Conference should anyone wish to discuss or share their input. He can be reached at rcook@hudco.com.