Articles by Srividya Kalyanaraman

It’s Here: Artificial Intelligence Changes MCA Broker’s Business, Improves Bank Underwriting and Debt Collection

November 22, 2016In this age of man versus the machine, the case for artificial intelligence and machine learning does not need many vociferous advocates.

Some predict that revenues from fintech startups using AI and predictive models is set to jump by 960 percent or to $17 billion by 2021. We might be closer to that number than we think, considering 140+ AI startups raised a total of $958M in funding in Q3’16, alone.

While healthcare, cybersecurity and advertising are frontiers of AI innovation, the growth and momentum of big data in finance (spurred by online lending) is fast bringing fintech to the forefront. In lending, specifically, data has become the new currency. It’s not so much that lenders didn’t use data for decision making earlier, but the data available then, wasn’t as rich or as extensive. A loan approval decision that just required a decent FICO score and assessment of character has expanded to include data points like a business’ social media presence, reviews, and owners’ background history.

Today, artificial intelligence in fintech has grown to tackle cybersecurity threats, act as a personal assistant, track credit scores and perform sentiment analysis to predict risk — making automated underwriting just the tip of the iceberg for what artificial intelligence and machine learning can do for the financial services industry. deBanked spoke to three fintech upstarts that have taken AI beyond underwriting.

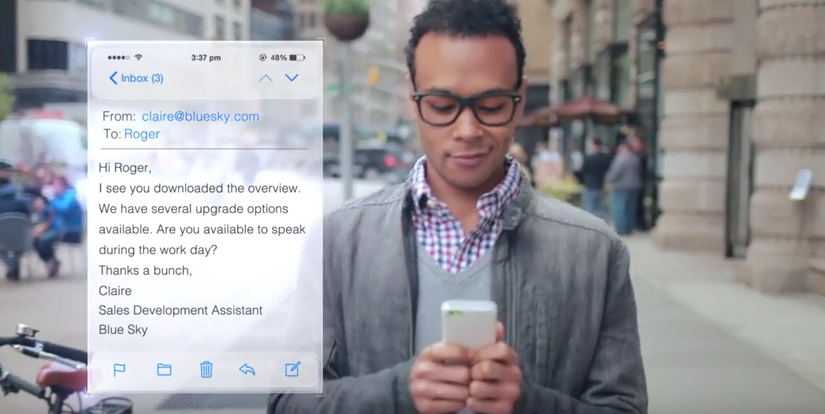

AI Assist

When Roman Vinfield started his ISO, Assure Funding in early 2015 with 16 openers, five chasers and three closers, little did he know that a business intelligence software would replace 85 percent of his staff for the same productivity. He stumbled onto Conversica, a AI-powered virtual sales assistant and was convinced to give it a try.

When Roman Vinfield started his ISO, Assure Funding in early 2015 with 16 openers, five chasers and three closers, little did he know that a business intelligence software would replace 85 percent of his staff for the same productivity. He stumbled onto Conversica, a AI-powered virtual sales assistant and was convinced to give it a try.

“I hadn’t heard anything like an artificial-intelligence sales assistant,” said Vinfield. “The results we got within a month of using it were unbelievable.” Within the first month, Vinfield made $35,000 in revenues by spending just $4,000 and eventually reduced his staff of 24 to 4 people. He was so sold on its potential for the merchant cash advance industry that after prolonged negotiations, he secured the rights to be the exclusive reseller of the software, and called it AI Assist. The software is now used by leading MCA companies like Yellowstone, Bizbloom and GRP Funding.

While Conversica’s clientele includes auto and tech giants like Oracle, Fiat, Chrysler and IBM, for the financial services industry, it’s marketed and sold to MCA and lending companies through AI Assist. It integrates easily with CRM software like Salesforce and creates a virtual sales assistant avatar that tracks old leads and reestablishes engagement. In the lead generation race, where a 3-5 percent response rate could be considered good, the response rate for Conversica has been 38 percent.

Designed to be akin to a human sales assistant, Conversica’s technology can determine a lead’s interest based on the response and set up a conversation with the sales department to follow up. “Your Conversica virtual assistant is an extremely consistent, personable and tireless worker. She doesn’t get sick and never needs a break. She never gets discouraged, and she improves with each engagement,” says the AI Assist website.

True Accord

True Accord

Personal chat assistants for money management and sales is one of the popular modes of AI implementation in fintech, given it’s scalability in lending for functions like debt collection. One company that does this, is True Accord. True Accord, similar to AI Assist uses automation software to schedule and send messages to customers by the company’s “Automated Staff”

The San Francisco-based company was founded by Ohad Samet who has over 11 years of machine learning experience in finance. The idea came to Samet while he was working as a chief risk officer at payments and e-commerce company Klarna, underwriting loans worth $2 billion. “While working at Klarna, I realized how big a piece debt collection is and I did not like the way it was done,” said Samet. “I needed machine learning to change it.”

Samet founded True Accord in 2013 to develop a debt collection AI assistant and today the company works with leading banks, credit card companies and food delivery services and has collected over half a billion dollars. It establishes targeted communication with the customer less frequently than traditional collection agencies and allows customers to pay their dues over mobile, which accounts for 35 percent of collections for the company.

“We humans don’t want to accept it but the reality is that, when it comes to scale, machines make better decisions than humans,” said Samet. “Machines are consistent, they are not tired, not angry, don’t fight with the significant other and all of this makes for better accuracy, better cost structure and better returns of scale.” While this might be true, building an efficient, compatible and compliant model is harder than it might seem.

James.Finance

Since AI tools do not come in a one-size-fits-all package, its application can be as varied as the range of companies that use it. Building an AI framework that aligns with a company’s targets while being compliant to regulatory mandates can be an uphill task.

Since AI tools do not come in a one-size-fits-all package, its application can be as varied as the range of companies that use it. Building an AI framework that aligns with a company’s targets while being compliant to regulatory mandates can be an uphill task.

Recognizing this opportunity, James.Finance, a Portugal-based startup is using artificial intelligence to help financial institutions like banks build their own credit scoring models. Founder and CEO Pedro Fonseca, describes James as a “narrow AI” for a specific purpose of guiding risk officers to build machine learning models that follow regulatory compliance.

The startup works with consulting agencies or partners to reach out to banks. It offers a trial run of the software, which it calls a ‘jumpstart,’ where a risk officer is provided with James’ technology and in 24 hours, he or she will have to beat it with their in-house AI software.

“And we are consistently able to beat the models,” said Fonseca. The company won the startup pitch at Money 20/20 in Copenhagen earlier this year after receiving an uproarious response in Europe. Fonseca wants to divert his attention to the US’s fragmented banking market, which is dotted with smaller banks and credit unions. “The US is a perfect target for us. We are looking to work with local consultancies that know the problems of a bank intimately.”

As these entrepreneurs vouch for it, the current state of AI use in fintech is just the tip of the iceberg. And anything man can do, machines can do faster and better, right?

Funders Prep for the Holiday Rush

November 1, 2016

As the year draws to a close sending everyone into a dizzying holiday frenzy, funders are prepared to fire on all cylinders to fuel their retail customers with cash.

The last quarter is crunch time for funders alike, who start preparing months in advance — designing new products, marketing and selling them. deBanked spoke to a few to find out what business looks like at this time of the year and what’s in store for 2017.

For some, Christmas comes in August

At South Dakota-based Expansion Capital Group, the holiday prep started as early as August. “We think demand is going to be very strong and to accommodate for it, we started 60 days early,” said Marc Helman, director of strategic partnerships. The company launched four new products in August for a wide spectrum of borrowers — longer term products for existing customers and starter offers for new companies and those with challenged credit.

Since the demand peak is cyclical, most funders who have been around a while have the drill down to a science. For NYC-based funder Hunter Caroline, demand spikes up close to the tax extension period, in September and October. “We sit down with our marketing team, see which clients ramp up this time of the year and focus our sales efforts in that direction,” said Cody Roth, managing partner at Hunter Caroline. During the holiday season the company turns its attention to customers in mom and pop retail, restaurants, liquor stores and gift stores in small towns.

“We weigh a lot into seasonal businesses and have certain hybrid programs,” Roth said. “We collect a little bit more during the busy season and keep it down during the slow time.” For this year specifically, the two-year-old firm is pushing invoice factoring, purchase order financing and unsecured loan products apart from its usual business loan offering of up to $4 million for 24 months.

Plan, pilot, pivot

Q4 is also the time when companies plan and strategize for the year ahead. And for loan marketplace Bizfi, a lot of changes are in the offing. The company appointed John Donovan, a 30-year veteran in the payments and alternative finance industry as its new CEO. And while on track to approach nearly $600 million of fundings this year, Bizfi also decided to cut ties with some non-performing ISOs to increase efficiency. “We just told around a hundred sales offices we could not do business with them anymore to use resources for our own funding channels that have better conversion rates,” said Stephen Sheinbaum, founder and president of Bizfi.

Holiday Hangover

The holiday season is arguably one of the busiest times of the year for merchants, but it doesn’t have to be so for funders. Jason Reddish, CEO of New Jersey-based Total Merchant Resources advises all his clients to take the money when they don’t need it, asking clients to borrow early, put away the money and by November, have the capital pay for itself through the peak season. “The oldest problem with credit is that you get as much as you want when you don’t need it,” Reddish remarked. “You have access to cheap and the most flexible money when you don’t need it.”

The company tries to structure deals that way for some of its retail clients who see high holiday demand.“We see a pretty big spike going into the holidays and then there is a holiday hangover where they are absorbing all the money they borrowed,” Reddish remarked. “Until the hangover wears off in February and we get busy again.”

All things considered, funders are on their marks for the holiday. Will it be bright for them?

Remember When? Funders Talk About Their First Deals

October 14, 2016

It’s hard to forget the firsts, especially first deals — they set precedents, lay down the groundwork for policies and establish a starting point for legacy.

For funders and lenders, their first deal can be significant in establishing client relations, setting priorities for credit policies and as we found out, teaching them valuable lessons.

First Steps..Baby Steps

First Steps..Baby Steps

John D’Amico’s first bet was a small cafe in Carmel, Indiana that his company GRP Funding advanced $25,000 to, eight years ago. Reviewed on credit card sales, GRP looked at the business’ cash flow and deemed it a good risk to take, D’Amico recollected.

“That business model seems so far and long ago,” he said. “OnDeck was not a company at that point and loan products were not talked about. It was only advances.”

Would he still feel confident doing the same deal today? “Yes, that deal is still there to be had today. But you want to make sure that you’re not stacked.”

#LifeLessons: Don’t get comfortable, stay updated with the times and evolve and keep the credit risk policies fresh.

Small Can Be Significant

Small Can Be Significant

The first check, Jersey City-based World Business Leaders cut was for $7,000, back in 2011.

Chief revenue officer, Alex Gemici recalled that it was an African arts store run by a woman in Virginia Beach who paid back the loan in full and came back three months later for an additional loan of $12,000.

“We believed her story and went by our lending policy and the deal fit the bill.”

#LifeLessons: We could make a big difference even with a small loan.

Not All Firsts Are Good

Not All Firsts Are Good

But not everyone has a smooth start. For New York City-based company, Cardinal Equity, the first deal was a bump on the road.

The auto dealership in New Jersey that it advanced $250,000 to in 2011 defaulted on the second renewal. Although Arty Bujan, managing member at Cardinal Equity still thinks auto dealerships are a “nightmare,” his company still funds them but with very strict scrutiny, looking for ones with a steady revenue stream and a good amount of time in the business.

#LifeLessons: There’s always risk

Dear Funders: Don’t Dial ‘M’ for Marketing

October 7, 2016

Imagine you own a small donut shop in Arizona and receive an email saying, “Hello, I have heard your chocolate donuts are amazing and the most popular item. I work for XX, and we provide small business loans, do reach out to us if you’re looking to take it a step further.”

Versus

Getting yet another envelope in a deluge of mails with a bank-check-like promotional ad for a preposterous amount that startles you for a hot second before it ends up in the paper shredder.

One of these methods is free, personalized and subtle. And no points for guessing which one.

Gone should be the days where funders indiscriminately send out email blasts or cold call merchants offering working capital. But are they?

A year ago, a Wall Street Journal article said,

“A big reason online lenders make heavy use of mail, they said, is that it is still more effective than other types of direct marketing. Across all industries, the overall response rate for direct-mail overtures is 3.7%, compared with 0.1% for both email and social-media marketing campaigns, according to a recent report from the Direct Marketing Association, an industry group.”

Mintel Comperemedia, a database which tracks advertising data highlighted the use of technology as being the paramount shift in marketing for the financial services industry. But is the transition from analog to digital underway?

For some companies, it is. New York-based SOS Capital does not have a sales team and does all of its marketing on social media. The company sends no direct mailers, limits email blasts and instead scouts for small businesses on Facebook, LinkedIn and Yelp.

With more small businesses ramping up their social media presence, discovering leads has not only become easier but also cheaper. “Small business presence on Facebook is growing every day and finding them there can save you a lot of money,” said David Obstfeld, CEO and co-founder of SOS Capital. “Facebook is not explored by most funders but we have had great success.” The company spent $6,500 marketing to SMBs on Facebook and had 120 conversions over a period of two months.

How does that compare with the conventional methods of direct mail campaigns, email blasts and phone calls?

According to Justin Benton, sales director at leads generation firm, Lenders Marketing, it could cost about $100,000 to send out a million emails to active, verified accounts and as much as a dollar for a nice direct mail, including printing and postage.

“Even though it’s cost prohibitive for some folks and some others think that it’s past its prime, direct mail still wins,” said Benton who urges his clients to consider social media marketing which he says can be “virtually free.”

Discovering companies on sites like LinkedIn and Yelp can offer insights into the business and target customers better. “Calling a lead once and saying the words, ‘business loans’ or ‘working capital loans’ does not work, you need to understand the business,” Benton added.

Digital marketing can also help one keep better track of leads and reinvest in the ones that work. “It’s important to have a leads scoring system,” Benton said. The opposite of that, to him, looks like “Making a gumbo from scratch but you have no idea how you did it and cannot recreate it.”

Competition among financial companies will eventually force them to get more creative with their marketing tactics. Like Partners Funding for example, an MCA funder that markets to ISOs, uses incentives as baits. “If the ISOs fund three deals over $50,000, we reward them with extra points or give them marketing dollars,” said Michael Jenssen, ISO sales manager at Partners Funding, which sticks to marketing through email blasts, calls and exhibiting at trade shows.

Ultimately, the road to a lasting relationship with clients is paved with effective marketing. And the line between pushing call to action and being pesky is quite fine. “Funders have been using the same marketing campaigns and it’s making the clients sick,” said Obstfeld. “There are only so many mailers one can receive. They have to be creative about marketing to people without annoying them.”

For Obstfeld, the value in pursuing businesses through channels like Facebook is having more control over deals and interacting with the merchants directly, without any interference from ISOs. “It’s not just about saving money but the control over the deal. When there is no ISO involved, there is no stacking involved.”

The transition to moving all marketing online might be slow but inevitable. Until then, using bank check imagery to promote big pre-approvals will be more than just gags.

Entire Industries Still Unbankable Despite Big Data Boom

September 28, 2016

The use of data and technology for assessing risk shows promise for new borrowers, safer bets and fewer delinquencies. Big data has been credited for overhauling traditional lending models and ushering in a new crop of lenders that do not shy away from risky businesses and low credit scores. But has it been successful in narrowing the list of industries previously ineligible to even be considered? And perhaps there’s a bigger story, that some lenders still maintain a list of industries they cannot or will not lend to despite the boom in data. deBanked checked the temperature on restricted lending practices today with three lenders and here’s what we found.

Jersey City-based World Business Lenders whose average loan size is $150,000 does not lend to startups. According to chief revenue officer, Alex Gemici, startups usually don’t have revenues to justify payments. “Startups fail the ‘ability to pay’ test,” he said.

The restricted industries for WBL are the usual-suspects that fall in the federal legality grey areas like Marijuana related businesses and adult entertainment websites and weapon manufacturers that the company takes a moral stance against. Gemici said that the company has never lent to these industries and will evaluate the policy only if the need arises.

Apart from these WBL also classifies certain establishments as ‘high risk,’ either prone to defaults or without a steady cash flow like car dealers, childcare services, gas stations, real estate speculators, stock brokers, insurance brokers etc. which the company lends to with increased scrutiny and tighter checks.

Often, the risk appetite of a company depends on how long it has been in business and its funding track record. For instance, San Diego-based National Funding is 17 years old but is gun shy when it comes to lending to auto dealerships, thanks to sustained losses. “We don’t lend to auto dealerships because they already have enough MCA plans out there,” said CEO Dave Gilbert. “It’s too risky to be in that environment without being tied to actual assets, we have had too many losses.”

Often, the risk appetite of a company depends on how long it has been in business and its funding track record. For instance, San Diego-based National Funding is 17 years old but is gun shy when it comes to lending to auto dealerships, thanks to sustained losses. “We don’t lend to auto dealerships because they already have enough MCA plans out there,” said CEO Dave Gilbert. “It’s too risky to be in that environment without being tied to actual assets, we have had too many losses.”

Government agencies, membership organizations (usually, non profit), insurance brokers, online dating services, weapon manufacturers, credit repair services, gambling and ticket sales websites are also industries the company does not lend to.

However, construction companies, oil companies, transportation and industries with high subsidies like solar businesses are what National Funding considers high risk and will finance cautiously, by tightening the credit window, advancing smaller amounts, demanding higher FICO scores and increasing scrutiny on cash flows.

Irrespective of whether a company automates underwriting, few contest the need for rich and varied data for calculating risk and approving a loan. Kennesaw, Georgia-based IOU Financial, which recently started lending in Canada, has a proprietary ‘Risk Logic’ score for underwriting which includes credit data, financial and non-financial accounts, public records, transactional data and a business owner’s personal credit information.

Despite this, it restricts lending to businesses with seasonal cash flow like tax prep services, industries that invoice out for larger orders including manufacturing, and marijuana dispensaries. IOU also does not lend to industries where it has faced high delinquencies in the past, like oil refinery service related industries and supply chain service providers that are subject to fluctuations in commodity prices.

And if OnDeck, the touted leader in deploying big data for underwriting prohibits 60 industries in five different categories including blood and organ banks, payroll companies and its own kind — non-bank financial companies, has big data really changed underwriting?

Funding The Great White North

September 13, 2016

As of last year, 98 percent of Canada’s employers were small businesses compared to 0.3 percent (2,933) large companies. Given this and what we know about Canada’s banking oligarchy, dominated by five large banks, it was inevitable that American alternative lenders would go looking for greener pastures in Canada.

When OnDeck set foot in the country two years ago, it accelerated the alternative lending movement by offering loans up to $150,000 CAD. But OnDeck wasn’t the first to discover the Canadian market. Merchant cash advance companies such as Principis Capital and AmeriMerchant (today Capify) have been there since 2010. Principis actually draws close to 15 percent of its business volume from Canada. But the credit that’s due to OnDeck is for expanding the horizons of small businesses who have been conditioned to think that lending begins and ends with banks. The crop of Canadian alternative lenders who do not otherwise have the resources for similar blitzkreig marketing are pleased with the industry’s promotion in general.

“We are happy that some of the bigger US players are coming up here and they are spending millions of dollars on advertising,” said Bruce Marshall, vice president of British Columbia-based Company Capital. “These companies raise awareness of the industry to a higher level and with us being a smaller company, we can ride on their coattails,” he said.

Company Capital has been operating as a balance sheet lender for five years and has provided term loans, working capital loans, merchant cash advances and ‘cash lines’ which are similar to lines of credit. For lenders such as Company Capital which makes loans in the range of $30K – $50K, the presence of bigger players like OnDeck saves them from consumer education-oriented marketing campaigns. “We cannot compete with the advertising of big companies but it works in our favor of creating awareness and becoming more mainstream,” Marshall noted.

And this not only helps the Canadian companies but also smaller US companies that feel comfortable entering a market with a leader. OnDeck’s presence nudged Chad Otar, founder and managing partner of New York-based commercial finance brokerage Excel Capital Management into considering Canada as a viable market. “We saw OnDeck go there and thought that there is some kind of money we can make,” he said.

But for OnDeck, Canada might just as well be another large US state. Most American companies including OnDeck, Principis Capital and Excel Capital run their Canadian operations remotely, treating it much like an extension to their US business with similar products.

But for OnDeck, Canada might just as well be another large US state. Most American companies including OnDeck, Principis Capital and Excel Capital run their Canadian operations remotely, treating it much like an extension to their US business with similar products.

“Our range of business is virtually the same in Canada as in the US. We don’t need to have an operation center there,” said Jane Prokop, CEO of Principis Capital. The company approaches Canada just like the US with accounts and customer service being handled in a similar fashion. “It’s a very manageable extension of the US market,” Prokop said. “It’s a smaller market so someone who enters Canada cannot expect the same kinds of volume as in the US.”

It also certainly helps to be spread across the same time zones and in such close proximity where a majority of the country also speaks the same language. If it was that easy though, shouldn’t we have seen more companies doing this?

“The fundamentals of the Canadian market are different. Our banks are established and trusted and in general do quite a good job, so the opportunity for market expansion is different than in the US,” said Jeff Mitelman, CEO of Thinking Capital, one of the country’s first alternative lenders.

Prior to Thinking Capital, Mitelman founded and ran Cardex, Canada’s first ISO which offered lending products with payment services. And that competitive edge helped him recently to partner with payment solution company Everlink to expand its customer base and offer loans online. The company previously secured credit facilities worth $125 million from two of the biggest banks in the country, The Canadian Imperial Bank of Commerce and Nova Scotia.

Picking up the same strategy, some American companies decided to bank on these big banks (pun intended) for their success. For instance with Kabbage, it made sense to license its automated platform to Nova Scotia Bank and to rely on them to deploy capital while Kabbage provides the technology and customer experience. “We saw that Canada is ripe for technology but the differences in regulation among other things made us go the partner route,” said Peter Steger, head of business development at Kabbage.

The advantages of having an incumbent customer base, the brand equity and the supply of capital usually outweighs the costs and inconveniences of maneuvering in an unfamiliar business environment that only a few firms have the bandwidth for, some companies contended.

Secondly, there is a lack of reliable and robust data necessary for making lending decisions. Since only a handful of large financial institutions dominate the landscape, the data reported is limited to a small number of players and the outputs from credit bureaus may not be sufficient for making a credit decision. “The availability and access to government and financial data is scarce in Canada compared to other markets,” said Jeff Mitelman. “Most of the data relationships that fintech companies rely on, need to be developed on a one-to-one basis and is often proprietary information.”

Having the data presented in the right format can save a lot of underwriting time. Companies in Canada find the government and financial data available to be scanty and in less than ideal form. David Gens, CEO of Vancouver-based Merchant Advance Capital noted that Canadian merchants are slower to adopt technology which adds to the woes of online lenders. “Believe it or not, some Canadian merchants still use fax,” he said.

Even as the country plays catch up, Canadian lenders consider the market to be large enough for many players. “At this time, education is more important than competition,” said Mitelman.

Canada’s geographical dispersion and regional differences however are peculiar. The four provinces of Quebec, Alberta, Ontario and British Columbia make up 86 percent of the population and the greater part of the economic activity. And Quebec is often avoided, in part because of the bilingual mandate that requires businesses to advertise and produce materials in French. OnDeck and Company Capital both do not operate there, for example.

Canada’s geographical dispersion and regional differences however are peculiar. The four provinces of Quebec, Alberta, Ontario and British Columbia make up 86 percent of the population and the greater part of the economic activity. And Quebec is often avoided, in part because of the bilingual mandate that requires businesses to advertise and produce materials in French. OnDeck and Company Capital both do not operate there, for example.

The cultural differences can also determine how customer relationships are handled, and being a part of that culture has given Canadian companies an upper hand. “It does definitely help to have a home advantage in terms of understanding the local peculiarities,” said David Gens. “Marketing to Canadian merchants is also different — being aggressive might not work very well here and they like to know they are dealing with someone nearby.”

For financial brokers such as Otar, Canadian usury laws can appear restrictive. As per Canadian interest rate rules, Under Section 347 of the Criminal Code (Canada), interest rates exceeding 60 percent per annum are termed “criminal rates of interest” and “interest” in the Criminal Code is broadly defined as a broad range of fees, fines and expenses which includes legal expenses.

“US lenders have had to change their way of doing business. Since, APR is less here, if your product is a loan contract, you will be restricted and you will have to service low risk for low rates,” said David Gens.

Even so, the business emerging out of Canada may now be supplemental for American lenders and the potential for growth beneficial to diversification.

Does SoFi Want $500 Million for Global Expansion?

September 8, 2016Online lender SoFi is looking to raise $500 million in equity capital to fund new projects and possibly expand to international markets.

The San Francisco-based lender is in talks with investors and maybe just weeks away from finalizing the deal, according to The Wall Street Journal. If the deal goes through, it might be one of the biggest fintech deals of the year, said the report.

SoFi has had an eventful year so far, to say the least. Led by ex-Wells Fargo executive Mike Cagney, the company laid plans in the beginning of the year to start a dating app to appease millennial borrowers, started a hedge fund to buy loans, made a bunch cheeky, controversial commercials, appointed Deutsche Bank’s ex CEO Anshu Jain to its board, made unusual hires, funded $1 billion in student loans and got knee deep in mortgages. SoFi’s strategy since inception has been to stay relevant for its borrowers at every stage of their lives, starting with student loans, personal loans, all the way through to a mortgage.

One of the fastest growing private lending companies, SoFi’s backers include marquee investors like Peter Thiel, Prosper Loans’ President Ron Suber, Discovery Capital, Softbank and Morgan Stanley.

Caution! Politics Ahead: Amazon Breaks Student Loan Ties With Wells Fargo

September 7, 2016Was it easy come and easy go for the Amazon-Wells Fargo partnership?

Not long after the two companies signed a multiyear contract to market private student loans to Amazon Prime Student subscribers, the ecommerce giant retreated after finding itself in a political soup.

Caught in the crossfire between the two bastions of private and federal student loans, the partnership ended rather abruptly after The Institute for College Access & Success, or Ticas, a nonprofit focused on higher education and student-loan issues called the partnership an attempt to dupe students.

“This is the kind of misleading private loan marketing that was rampant before the financial crisis. It is a cynical attempt to dupe current students who are eligible for federal students loans with a record low 3.76% fixed interest rate into taking out costly private loans with interest rates currently as high as 13.74%,” said TICAS in a statement issued last week, “Amazon and Wells Fargo are trumpeting a 0.5% discount while burying the sky-high rates on these private loans and without noting that they lack the consumer protections and flexible repayment options that come with federal student loans.”

This was exacerbated by the CFPB’s allegations that the bank engaged in illegal student loan practices — by misleading borrowers on partial payments, charging certain consumers late fees for payments made on the last day of the grace period and failing to correct inaccurate information on credit reports of borrowers. Wells Fargo, the second-largest private student lender neither denied nor admitted to the charges but however, settled the matter for $4.1 million.

The partnership was an one up for private student lending especially against growing private entrants like SoFi and CommonBond. With it being undone, what’s next?