Marketplace Lending

OnDeck Appoints Former GE Exec to Board

June 6, 2016OnDeck appointed Daniel Henson to its board, the company said on Monday.

Henson spent 30 years at General Electric, holding positions at GE Capital and ran the company’s commercial lending business globally in addition to managing GE Capital’s lending and leasing business through the 2008 financial crisis.

“Dan ran one of the largest commercial lending operations in the U.S. and his deep experience in strategic growth initiatives, process excellence and risk management will be a tremendous asset for OnDeck as we continue providing small businesses in the U.S., Canada and Australia with the capital they need to succeed,” said CEO Noah Breslow.

New York-based OnDeck netted a loss of $12 million in Q1 this year and also predicted a full-year adjusted EBITDA loss of between $41 million and $49 million. Online lenders have been battling turbulent times with increased scrutiny on business practices, portfolio performance and rising delinquencies.

‘We Serve a Fragmented Market That is Ripe for Disruption,’ says Patch of Land CEO

June 3, 2016$484 million: That’s how much real estate crowdfunding platforms attracted in 2015, which was three times of that the previous year. There are an estimated 125 such portals and the new SEC rule which allows non accredited investors some leniency to invest in these projects. To demystify real estate crowdfunding, deBanked spoke to Patch of Land’s CEO Paul Deitch to unravel the concept, measure the momentum of investor interest and the regulatory environment. Here are excerpts from the interview.

What’s on the horizon for Patch of Land this year?

Now that Patch of Land’s model is proven, we will be adding complimentary products for the real estate entrepreneur and investor, accompanied by a broadening of funding strategies. For example, we recently launched the new midterm loan product that addresses the opportunity in the $4 trillion single-family rental space.

How is the investment momentum different from that in ‘08-’09?

One of the biggest changes between then and now has been the enactment of the JOBS Act, which actually came about as a result of investment conditions in ‘08-’09. Peer-to-peer lending came into existence during the 2008 Recession when consumers and small businesses could not rely on banks for their funding needs. In 2012, President Obama signed a historic bill called the JOBS Act (Jumpstart Our Business Startups Act), allowing companies to raise working capital in the form of debt and equity via a crowdfunding model. When the SEC implemented Title II of the JOBS Act in 2013 it allowed companies to publicly solicit, via Internet marketing, their equity and debt offerings; private placements could now be advertised. Marketplace lending is an evolution of peer-to-peer lending, defined by the participation of traditional financial institutions purchasing the loans being issued by P2P lenders.

Whom do you consider your competition in the industry and how do you differentiate yourself from them?

We approach the competition question from a different perspective. One would think that other online lenders or real estate crowdfunding companies are our competition but they are not. We are all working towards creating more efficiency, transparency and access to real estate and investments. The market that Patch of Land is serving is fragmented, locally delivered, and highly manual — it is ripe for disruption. Banks are exiting the space due to capital and liquidity constraints and hard money lenders are limited by a single source of capital and local footprint. Unlike these offline incumbents, Patch of Land has a national footprint, and uses proprietary software to quickly and reliably make first lien position loans, pre-fund those loans, and then crowdfund the financing from thousands of investors (both individuals and institutions) on a fractional or whole loan basis.

Who regulates P2RE? And what are the challenges there?

P2RE and the real estate crowdfunding sector is regulated by the SEC. Patch of Land operates under Title II, Regulation D, Rule 506(c) whereby we can only accept investments from accredited investors, as defined by the SEC. This is a strict regulation that requires thorough diligence and vetting of the accredited status of the investor. The biggest challenge we face is that we have many retail investors who want to invest with us and we cannot accommodate them.

How are the ripples in the capital markets affected or will affect business?

Capital markets volatility has not had an adverse effect on our business. Our capital sources are very diversified and are not dependent on large capital market players. Over 90 percent of our loan volume has been, and continues to be, funded by crowd capital. We have on-boarded multiple institutions of various sizes that buy loans on a fractional basis, in addition to the whole-loan forward flow agreements in place.

How is crowdfunding for real estate different from marketplace lending specifically?

Crowdfunding for real estate, specifically when referencing debt, is a subset of marketplace lending. Patch of Land is a ‘real estate marketplace lender’ because we focus specifically and exclusively on debt and do not offer any equity projects for funding. Equity deals are crowdfunding deals, not marketplace lending deals. Therefore, a real estate marketplace lender that transacts with individual investors can be considered a crowdfunding platform, and a crowdfunding platform that does not transact in debt is not a marketplace lender. Two other elements that differentiate crowdfunding from marketplace lending are: 1) prefunding, where the platform fully funds the loans upfront and therefore is not engaging in crowdfunding that usually involves raising capital first, before disbursing it to the sponsor/borrower; 2) marketplace lending includes institutional and individual investors who participate in loan purchases, whereas a crowdfunding model is focused exclusively on individual investors.

How is crowdfunding poised to change real estate investing?

Traditional real estate (debt or equity) can be highly time consuming. We offer an alternative to have real estate debt as part of a portfolio, bringing both new and experienced investors all the data they need to make a decision. Most would never have the time to aggregate this much data on their own, through traditional methods. Crowdfunding allows capital to flow more easily to across the nation, rather than locally, to places and projects that might have been shut out or simply left behind because they were too difficult to assess, evaluate and understand, or were the purview only of local investors and gatekeepers “in the know”. Crowdfunding puts investors in the driver’s seat, giving them the power to pick and choose investments that meet their personal risk/return needs. It allows for investment strategies that are both more “bespoke,” and yet more diversified -both in the way of product type and geographies, all through fractional investments across a technology enabled, online platform. Investors not only have broader choices of where to invest, but they can do it from their mobile phones in seconds.

Individual Investors Heart of Lending Club, CEO Says

June 1, 2016 Lending Club CEO Scott Sanborn sent out an email late Wednesday night to individual investors to remind them that they are “emphatically” the heart of their marketplace.

Lending Club CEO Scott Sanborn sent out an email late Wednesday night to individual investors to remind them that they are “emphatically” the heart of their marketplace.

“Our individual investor base is over 150,000 members strong,” the email says, but it was unclear if this is the amount of active investors or all investors that have participated since they launched in 2007.

Lending Club is doubling down on efforts to serve individual investors, Sanborn wrote, by staffing up on their investor services team and dedicating more engineering resources to improve the investment experience.

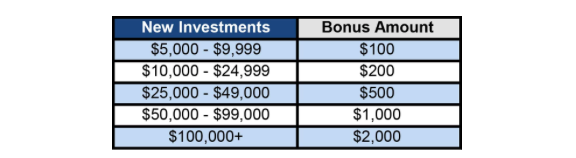

To prove this commitment, they’re offering investors that deposit new money and fully invest it by August 15th a matching bonus of 1% to 2% of the investment amount. The bonus can’t be withdrawn and they say you might have to pay taxes on it in the fine print.

Not mentioned in the email is the consideration of a Bankruptcy Remote Vehicle (BRV) to protect note investors from the underlying credit risk of Lending Club itself, something that many individual investors have been asking the company for. Lending Club rival Prosper instituted a BRV in 2012.

The question now is, will a potentially taxable small bonus that can’t be withdrawn be enticing enough to convince retail investors to double down on their commitment to Lending Club?

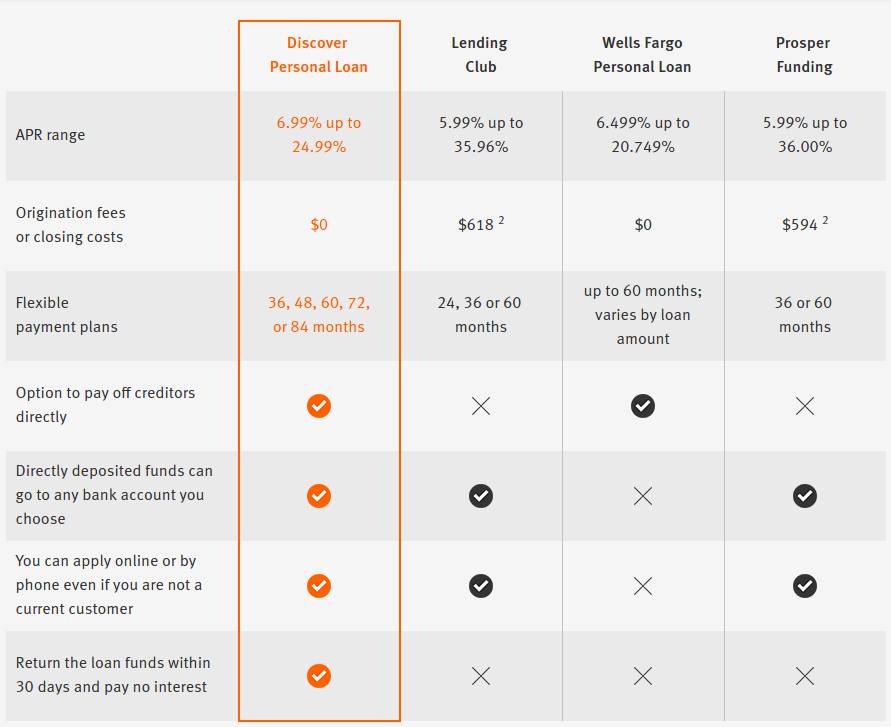

Discover Wants to Steal Lending Club Customers

May 31, 2016Discover used to demonstrate to potential borrowers how their personal loans stacked up next to loans offered by Wells Fargo. But with Lending Club, another rival, showing weakness lately, the columns on their personal loan comparison page have been rearranged to put themselves directly next to Lending Club.

Prosper Marketplace, as shown above, has been part of this comparison chart for quite some time as well. Personal loans from Citi also used to be listed, but they were removed as a competitor last summer. Discover, according to this, seems to show that their loan program offers many advantages over Lending Club.

Both companies market heavily using direct mail and that probably won’t change any time soon. 96% of Discover personal loan borrowers have FICO scores above 660. Meanwhile Lending Club’s minimum required FICO score is technically 640. Both are going after the same type of borrower.

Discover only originated $3 billion in personal loans (which is separate from its credit card business) in 2015 while Lending Club originated $8.3 billion.

Lending Club has at least two weaknesses at the moment, one being that approved loans on the platform could go unfunded if there are too few investors, a problem they’re facing right now. The other is that their relationship with a bank to make their entire business model work is under fire. Discover on the other hand is already a bank and doesn’t have to worry.

Lending Club’s stock price jumped late last week on news that Citigroup might buy the loans that the company originates. The bind Lending Club finds itself in makes a potential Citi deal look like a rescue bailout. If the company cannot find buyers for its loans however, it could indeed be in jeopardy, an issue that has been raised by observers for some time.

It cannot be understated that in Discover’s 2015 earnings report, they championed the originate-to-hold approach. “We believe our brand, disciplined underwriting and ‘originate to hold’ model will continue to allow us to compete very effectively,” they wrote.

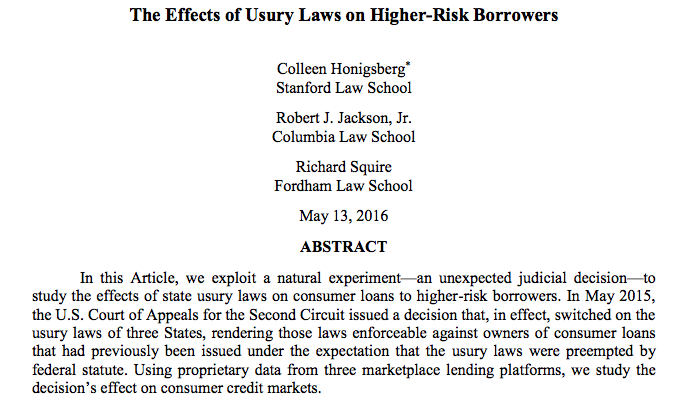

Madden v Midland Has Already Hurt Riskier Borrowers, Study Finds

May 28, 2016 If you thought the Madden v Midland decision was a future risk for marketplace lenders alone, think again. According to a joint study by law professors from Stanford, Columbia and Fordham, one group is already suffering as a result of the decision, people with lower FICO scores.

If you thought the Madden v Midland decision was a future risk for marketplace lenders alone, think again. According to a joint study by law professors from Stanford, Columbia and Fordham, one group is already suffering as a result of the decision, people with lower FICO scores.

Since the Second Circuit’s decision only affected borrowers in New York, Vermont and Connecticut, researchers were able to monitor behavioral changes there against other states. They used data from three of the nation’s top marketplace lenders.

In the Second Circuit’s jurisdiction, approved borrowers showed a significant increase in annual incomes, years of employment and FICO scores compared to other districts. Specifically, growth was concentrated among borrowers with FICO scores over 700. Approvals for borrowers with scores below 644 “virtually disappeared” while literally zero loans were issued to borrowers with FICO scores below 625.

“Madden’s effect on loan volume grows as the borrower’s FICO score falls,” the data reveals.

But even though lenders became afraid of the usurious implications in these states, borrowers did not take the Madden decision as a signal to stop payment. “[We] are unable to find any evidence of strategic delinquencies,” researchers concluded after a series of tests.

We find, consistent with basic economic theory, that the sudden enforceability of usury laws had the greatest impact on higher-risk borrowers. In a market where consumer loans are generally increasing in volume, the Madden decision disproportionately affected loan volume for borrowers with the lowest FICO scores.

Read the full study titled, The Effects of Usury Laws on Higher-Risk Borrowers

SoFi Ads: When You’re too Cheeky to be Nice

May 27, 2016 Controversial SoFi ads are back and this time they’re targeting renters.

Controversial SoFi ads are back and this time they’re targeting renters.

SoFi’s new ‘tone deaf’ ad for its mortgage loan reads, “10 percent down. Because you’re too smart to rent,” implying those who rent aren’t.

The ad, running in San Fracisco and Portland has attracted some ire among people. SoFi’s penchant for cheeky ads is known by now. Its SuperBowl ad — “great loans for great people” boldly labels some people as “not great,” implying that they are ineligible to join a rather exclusive club of people who can get great loans.

Here’s what people said on Twitter:

Tone deaf? Yes. Hard to believe, but even some smart people don't have $110k sitting around @SoFi https://t.co/O8isvxCUjS

— Jess Fleuti (@jessfca) May 25, 2016

Tone deaf ad for SoFi. Especially ill advised when 63% of those in SF rent. https://t.co/cyH63Oe8mv

— Stuart Robinson (@stuartrobinson) May 24, 2016

@SoFi Do you actually think that poor people are stupid or are you just stupid? https://t.co/On9dYo4ByY

— DrunkenGeeBee (@DrunkenGeeBee) May 18, 2016

Screw you, @SoFi. https://t.co/LgNaiPxtCH

— Jesse M. Locker (@JesseMLocker) May 18, 2016

Arrogance isn't that attractive: https://t.co/RaHgq7XdVA #badad #marketingmistake

— Bill Stewart (@billstewartmktg) May 25, 2016

‘As Reality Kicks in, Companies Have to be Discplined,’ Says Fora Financial’s Dan Smith

May 25, 2016

Starting a financial company couldn’t have come at a more inauspicious time for two friends that have known each other since college. Jared Feldman and Dan Smith started Fora Financial in June 2008 and today their company has provided $450 million to over 9,500 small businesses. It recently launched PRISM, a proprietary scoring and decisioning framework and secured a credit facility. Founders Smith and Feldman spoke to deBanked about working with Palladium, recent industry news and did some crystal ball gazing. Below is an excerpt from the interview

What does the industry look like to you, with its myriad of players and the recently surfaced problems?

JF: There are a lot of players but I don’t know how much business they are originating. It might sound greater than it actually is. While there is no doubt that competition exists, it is still from the usual cast of characters who have been around for quite some time. However the competition is driving up acquisition costs, possibly some irrational buying from some companies which then trickles down and causes some ISOs and brokers to fail.

DS: Our competitors and we have felt things change in the market in terms of regulation and capital. The influx of capital that came in with the new players is starting to contract a little bit and the lending companies like ourselves are controlling the amount they lend. There has been a lot of artificial growth in the industry – a lot of companies trying the test and learn strategy to see how deep they can buy into the market but they struggle to maintain profits.

And what will be the aftermath of these changes we see in the next six to twelve months?

DS: The reality is starting to kick in and companies will have to be disciplined about their underwriting models and be wise about where they spend their money in order to to grow and sustain profits.

What then should be the top priority for lenders now?

JF: Two top priorities that lenders should focus on is A) To build out a compliance framework and B) securing a long-term credit facility apart from the already mentioned disciplined underwriting making risk, analytics and data capabilities strong.

You started working with private equity firm Palladium last year. Tell us more about where you are with that?

DS: We got into this great partnership and a fund of theirs gave us the capital to grow our business and it aligned with everything we had in our 100 day plan – we wanted to build our regulatory compliance framework, close on a credit facility and bring some key people onboard — all of which we have accomplished. Working with Palladium teaches us how to run a disciplined company and we have already been entertaining M&A opportunities.

What do you think of the hybrid model approach that some lenders take ?

DS: Hybrid model is a great idea in theory and there are concerns with every approach — of holding everything on balance sheet and then buyers buying the loans. There is a lot that goes into capital raising and we have done what we know well and have continued to organically grow our balance sheet. It’s not to say that we have not considered other options but for now, we are focused on getting the right cost structure.

JF: If you have the credit facility with the right cost structure, that is a cheaper cost of capital than what the marketplace is selling these loans for but we are considering options for diversifying our capital sources and we would like to add some kind of market element but that might be in the future. Maybe in the first quarter of 2017.

Second Circuit Incorrect on Madden Case, US Solicitor General Opines

May 25, 2016

Given the Madden v Midland decision, does the National Bank Act continue to have preemptive effect after the national bank has sold or otherwise assigned the loan to another entity?

This question was presented to the US Solicitor General, the person appointed to represent the federal government of the United States of America in Supreme Court cases. The US Supreme court had asked the Solicitor General to weigh in before deciding to take on the case. And the answer is in:

The US Court of Appeals for the Second Circuit was incorrect in its ruling, the federal government believes.

Nevertheless, the US Supreme Court should not even hear the case, they say, because there is “no circuit split on the question presented” and “the parties did not present key aspects of the preemption analysis” to the lower courts. Put simply, “The court of appeals’ decision is incorrect,” they explain, and the heart and soul of preemption itself has never been in question.

The message from the US Solicitor General is clear, carry on friends, nothing to see here with Madden v Midland.

The US Supreme Court could still opt to hear the case but that is very unlikely at this point. Lawsuits filed against alternative lenders such as Lending Club in recent months had used the Madden ruling as evidence to support usury complaints. The connection between a case where a debt collector bought a charged off credit card debt from a bank (which is what Madden was about) and the business model of Lending Club was already weak, but several plaintiffs hoped to use it as a stepping stone. The Solicitor General’s opinion could likely derail attempts by other plaintiffs to cite Madden.

Of notable mention is that many of today’s alternative lenders have relationships with state chartered banks that are covered under the Federal Deposit Insurance Act, not the National Bank Act which the US Supreme Court was asked about. While the two laws are very similar, it did put alternative lenders at an additional arm’s length from Madden.

You can read the Solicitor General’s full brief here.

Read revious posts about this case:

3/22/16 Plot Twist: Obama Administration to Comment on Madden v Midland

3/2/16 Lending Club Class Action Lawsuit Predicated on Madden v Midland Risk

2/26/16 Lending Club Shifts Fee Arrangement With WebBank

2/18/16 Without Scalia, Media Outlets Reporting Marketplace Lenders Supposedly Doomed With Supreme Court Case (They’re Wrong)

11/15/15 Madden v. Midland Appealed to the US Supreme Court

8/13/15 Madden vs. Midland Funding, LLC: What does it mean for Alternative Small Business Lending?

8/13/15 Madden v. Midland Appeal Rejected

8/8/15 Renaud Laplanche on Madden v. Midland

7/28/15 Blyden v. Navient Corp: A Glimpse of a Post-Madden Future?

6/11/15 Legal Brief: Madden v. Midland Funding