Legal Briefs

Analyzing Confessions of Judgment

March 4, 2019 Platzer, Swergold, Levine, Goldberg, Katz & Jaslow, LLP (“Platzer”) has built one of the leading Merchant Cash Advance practices in New York City. With years of experience handling traditional lending transactions, Platzer has expanded its representation to Merchant Cash Advance Companies (“MCA”) in all aspects of their business cycles, including Participation Agreements, Assets Utilization, Transactional related matters and litigation.

Platzer, Swergold, Levine, Goldberg, Katz & Jaslow, LLP (“Platzer”) has built one of the leading Merchant Cash Advance practices in New York City. With years of experience handling traditional lending transactions, Platzer has expanded its representation to Merchant Cash Advance Companies (“MCA”) in all aspects of their business cycles, including Participation Agreements, Assets Utilization, Transactional related matters and litigation.

In the course of representing some of its MCA clients within the State of New York, Platzer has identified a potential issue in certain counties within New York State that are denying entry of Confessions of Judgment (“COJs”), notwithstanding language that has been contractually agreed upon and explicitly sets forth that the Confession of Judgment “may be entered in any and all counties with in the State of New York”, when the defendant is a non-resident.

The following is not a legal opinion but is our preliminary analysis:

It is Platzer’s position that New York Civil Practice Law and Rules (“CPLR”) 3218(a)(1) provides that when the defendant is a “non-resident” that judgment by confession may be entered in “the county in which entry is authorized.” Further, CPLR 3218(b) allows entry of judgment by confession as to a non-resident“ with the clerk of the county designated in the affidavit.” Platzer respectfully argued to the subject county that its jurisdiction is within the scope of authorization of “all counties” in the State of New York, and that the defendant “authorized” entry of judgment in the subject County, as contemplated by CPLR 3218(a)(1), and was also designated, as one of “all counties” in the State of New York, satisfying CPLR 3218(b), yet the Confession was denied entry.

As Platzer then noted, there is case authority for the proposition that non-resident defendants may subject themselves under CPLR § 3218 to the entry of judgment by confession in multiple counties. To Platzer’s knowledge, no Court has passed on the precise language of “all counties” or similar language. In the analogous situation where the confession of judgment executed by the non-resident defendant allowed entry in multiple but not “all” counties, Courts have routinely upheld entry of the judgment, while noting that there is no authority that would prohibit such entry under CPLR § 3218. Platzer has contended that this case law supports the notion that entry of confessions of judgment with “all counties” language is proper under CPLR § 3218.

As of March 4, 2019, Platzer is actively discussing these issues with the subject counties within the State of New York and hopes that its arguments will be persuasive based upon current New York law. Platzer is aware, however, of the state and national legislative efforts to curtail the entry of confessions of judgment and, specifically, the recent legislative proposal by Governor Andrew Cuomo to restrict entry of confessions of judgment to defendants doing business in New York and in amounts over $250,000.00. Platzer expresses no opinion as to these efforts.

Contacts:

Howard M. Jaslow

hjaslow@platzerlaw.com

Morgan S. Grossman

mgrossman@platzerlaw.com

Platzer, Swergold, Levine, Goldberg, Katz & Jaslow, LLP

475 Park Avenue South, 18th Floor

New York, New York 10016

Telephone: (212) 593-3000 ext. 248

Facsimile: (212) 593-0353

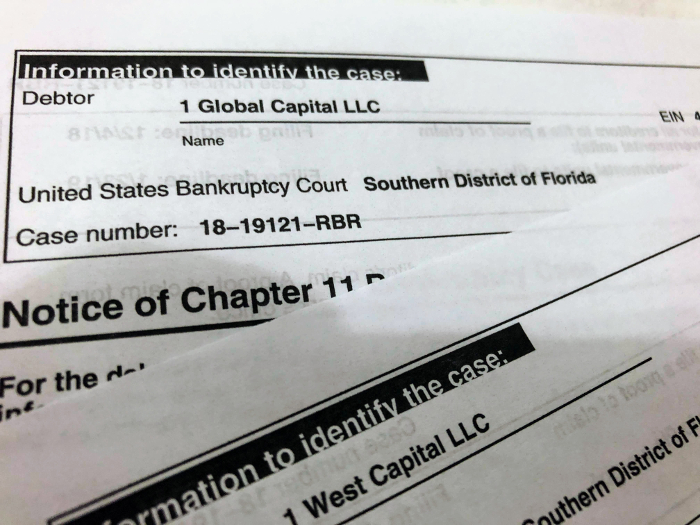

1 Global Capital Issued Securities, Court Rules

February 17, 2019 1 Global Capital founder Carl Ruderman suffered a major setback in his case with the SEC earlier this month, when the Court ruled that his company’s Syndication Partner Agreements and Memorandums of Indebtedness were in fact, securities. Ruderman had filed a motion to dismiss the SEC’s claims against him personally but the Court struck it down.

1 Global Capital founder Carl Ruderman suffered a major setback in his case with the SEC earlier this month, when the Court ruled that his company’s Syndication Partner Agreements and Memorandums of Indebtedness were in fact, securities. Ruderman had filed a motion to dismiss the SEC’s claims against him personally but the Court struck it down.

1 Global sold its notes to more than 3,400 investors in at least 25 states, who collectively invested at least $287 million. The company declared bankruptcy last year amid parallel criminal and civil investigations that hampered its ability to raise capital. The SEC filed suit soon after but no criminal charges have been brought to date.

In the ensuing legal discovery, it was revealed that the company funded the largest merchant cash advance in history, a collective $40 million funded over several transactions to an auto dealership group in California. Those dealerships closed not longer after 1 Global Capital’s bankruptcy. Those closures have sparked a lawsuit of its own and with it the revelation that several of 1 Global Capital’s competitors had also funneled millions into the dealerships.

The Court’s ruling in the motion to dismiss whereby the investments were deemed securities can be downloaded here.

Coming Soon: The End of Confession of Judgments (COJs) in New York State

January 16, 2019 New York State plans to outlaw the use of Confession of Judgments (COJs) in small business loan contracts this year, according to details revealed in Governor Andrew Cuomo’s newly published Justice Agenda.

New York State plans to outlaw the use of Confession of Judgments (COJs) in small business loan contracts this year, according to details revealed in Governor Andrew Cuomo’s newly published Justice Agenda.

The proposal, dubbed “Stopping Predatory Merchant Cash-Advance Loans,” is a 3-part plan to:

- Codify an FTC rule that prohibits COJs in consumer loans

- Prohibit the use of COJs in small business loans under $250,000

- Stop lenders from exploiting New York courts for nationwide collections by requiring that any permissible confession of judgment enforced in New York courts have a nexus to business activity in New York

Cuomo’s proposal echoes calls from the State legislature in response to a series published in Bloomberg Businessweek late last year that speculated COJs were vulnerable to abuse.

Both the Assembly and Senate maintain a Democrat majority, the same party as Cuomo, increasing the likelihood that such a bill could become law.

The proposal is separate from a bill that was recently introduced at the federal level. The Small Business Lending Fairness Act, a bipartisan bill co-sponsored by Senators Marco Rubio and Sherrod Brown, call for a nationwide ban on COJs. That bill has not progressed, perhaps due in part to the government shutdown. Like New York, that initiative was a response to the series published in Bloomberg.

The proposal is separate from a bill that was recently introduced at the federal level. The Small Business Lending Fairness Act, a bipartisan bill co-sponsored by Senators Marco Rubio and Sherrod Brown, call for a nationwide ban on COJs. That bill has not progressed, perhaps due in part to the government shutdown. Like New York, that initiative was a response to the series published in Bloomberg.

A review of Bloomberg’s facts by deBanked revealed highly questionable reporting. In one example, it’s claimed that a business owner had been so victimized by predatory lending that he’d been forced to sell his furniture just to feed himself. deBanked later determined that the “victim” was actually a multimillionaire TV station owner whose account of any such engagement with merchant cash advance companies was incredibly unlikely. The reporters have not responded to deBanked’s findings.

Zeke Faux, who co-authored the series with Zachary Mider, deleted his entire tweet history around the same time that deBanked uncovered strange ties between his editor and the New York Attorney General’s office. The AG is reported to have sent subpoenas to several companies in response to the stories.

On Monday, Faux and Mider reported that clerks in three New York counties, whose job, among other roles, is to enter legally compliant COJs into the public record, were revolting by refusing to process COJs submitted by merchant cash advance companies. Though a clerk’s duties is largely an administrative one, two that spoke on the record with Bloomberg were former state legislators. Erie County Clerk Michael Kearns, for example, who told Bloomberg News that he felt that the use of COJs was criminal, had actually drafted a bill in 2017 when he was an assemblyman that sought to regulate cash advances of a different sort in the litigation financing industry. Although Kearns is a Democrat, he has historically enjoyed support from the Republican Party.

Orange County Clerk Annie Rabbitt and Richmond County Clerk Stephen Fiala, who are rebelling along with Kearns by refusing to enter COJs, are registered as Republicans, demonstrating that the movement is crossing party lines.

According to deBanked, less than half of 1% of all MCA transactions have resulted in the filing of a COJ, despite Bloomberg’s insinuation that the outcome is common or typical.

Among the most prolific filers of merchant cash advance COJs, deBanked found, is Itria Ventures, LLC, a company affiliated with Biz2Credit. Itria filed more than 50 in the last two months. Biz2Credit’s CEO, Rohit Arora, is a writer for both CNBC and Forbes.

Former Merchant Cash Advance CFO Charged With Fraud by New York Attorney General

January 4, 2019 A former merchant cash advance CFO and executive for a fund that provides capital to merchant cash advance companies, has been charged with fraud by the New York Attorney General. The allegations against Stephen Brown stem from his role as CFO of Cardis Enterprises International, a company that claimed to possess patented and proprietary technology to make low-value credit card transactions less expensive for merchants. Brown is the former CFO for Capital Stack, LLC/eProdigy Financial in New York. In reality, Cardis was a massive fraud and a ponzi scheme, the Attorney General alleges. The company raised tens of millions of dollars from duped investors.

A former merchant cash advance CFO and executive for a fund that provides capital to merchant cash advance companies, has been charged with fraud by the New York Attorney General. The allegations against Stephen Brown stem from his role as CFO of Cardis Enterprises International, a company that claimed to possess patented and proprietary technology to make low-value credit card transactions less expensive for merchants. Brown is the former CFO for Capital Stack, LLC/eProdigy Financial in New York. In reality, Cardis was a massive fraud and a ponzi scheme, the Attorney General alleges. The company raised tens of millions of dollars from duped investors.

Brown is one of twelve defendants, but is described as the most senior financial executive of the firm whose principal role was to draft and send investor update letters, which contained a host of false statements and omissions.

Among the allegations against Brown is that he lied to investors about being close to finalizing deals with Sony, Warner, and Universal. “At the time of Defendant Brown’s representation, only one introductory meeting between Cardis and each music company had taken place, and the parties had not even executed non-disclosure agreements,” the complaint says. Several other business deals Brown announced were either imaginary, had never made it past a simple introduction, or had already been outright rejected by the prospective partner.

Despite being the CFO, Brown did not even maintain a basic income statement, a formal share registry, or comprehensive records of its debts and obligations. When the scheme was suspected by investors, Brown doubled down on the lies, the complaint says.

On September 24, 2015, a Cardis investor emailed Defendant Brown asking for the “latest on Cardis” and whether it was “a complete loss,” while mentioning a recent investor lawsuit. Defendant Brown, copying Defendant Rosenblatt, responded that the lawsuit claiming fraud was “frivolous,” while claiming that Cardis’ relationship with Roc Nation was “developing” and ongoing. In fact, the lawsuit had merit, and Cardis’ relationship with Roc Nation was long over.

On February 28, 2018, a Cardis investor recorded a telephone conversation with Defendant Brown. The investor asked “what happened to the cash” investors put into Cardis. Defendant Brown responded by detailing the Company’s large budget and staff, while failing to disclose the substantial misuse of investor funds. The investor also questioned Defendant Brown about various investor lawsuits against Cardis and its principals. The investor asked: “After reading those lawsuits, why should we think that the company has any future?” In response, Defendant Brown told the investor “the lawsuits were not the most credible lawsuits,” attributing them to “angry investors.” Defendant Brown later told the investor “none of those lawsuits have any merit to them.” In fact, there was substantial merit to the investor lawsuits.

These misrepresentations and omissions were material to investors because they bore directly on Cardis’ viability.

The New York Post ran a story that labeled Cardis a Bernie Madoff-style scheme that falsely claimed ties to Jay-Z’s entertainment company.

The defendants stand accused of Material Misrepresentations, Repeated and Persistent Fraud and Illegality, Actual Fraud, Equitable Fraud, and Constructive Fraud. The Attorney General is pursuing restitution for victims, a ban from the securities industry in the State of New York, and to liquidate the company.

The docket # is 452353/2018 in the New York Supreme Court. The allegations have not yet been proven. According to LinkedIn, Brown currently lists himself as the President of GMA USA, LLC, President of CoreFund Capital LLC, and the CFO of Nanovibronix. He also lists being the CFO of eProdigy Financial for almost 3 years until early 2017.

Kornfelds Settle With SEC Over Woodbridge Ponzi Scheme

January 3, 2019Barry M. Kornfeld and Ferne Kornfeld, both fundraising agents for 1st Global Capital, have settled with the SEC for their role in Woodbridge Group of Companies LLC, a $1.2 billion ponzi scheme. Woodbridge was another Florida-based company that is unrelated to 1st Global Capital. As part of the settlement, the Kornfelds agreed to disgorge $3.69 million plus $690,497 in prejudgment interest on top of $650,000 in combined penalties. They also agreed to be permanently barred from selling securities.

Barry Kornfeld was already barred by the SEC for previous securities violations.

No wrongdoing has been alleged against the Kornfelds in the 1st Global Capital case thus far, but court records revealed that Barry Kornfeld raised $8 million from investors for the company. 1st Global Capital is currently in bankruptcy and was charged with securities fraud by the SEC.

Defunct MCA Company Tried to Escape Signed Confession of Judgment

December 13, 2018 When a Florida-based merchant cash advance company, World Global Financing (WGF), declared bankruptcy this past May, it entered into a binding settlement agreement with its largest creditor, a hedge fund known as Eaglewood.

When a Florida-based merchant cash advance company, World Global Financing (WGF), declared bankruptcy this past May, it entered into a binding settlement agreement with its largest creditor, a hedge fund known as Eaglewood.

There was a caveat.

Eaglewood required that WGF sign a Confession of Judgment (COJ) as part of the agreement that would afford Eaglewood the right to file and obtain a judgment without further litigation if WGF breached the settlement. On August 3, that’s exactly what happened. After WGF failed to make the stipulated payments to Eaglewood, the COJ was filed in the New York Supreme Court so as to obtain a nearly $6 million judgment against WGF and company founder Cyril Eskenazi.

While it can be virtually impossible to invalidate a COJ, the courthouse Clerk nonetheless refused to enter it because of alleged technical defects, one of which involved WGF’s use of an out-of-state notary to witness a New York State affidavit.

“The alleged Affidavit of Confession of Judgment upon which Eaglewood’s request for a Judgment by Confession stands like a house of cards is no affidavit at all under New York law, and cannot be used in a New York litigation,” WGF’s attorney argued.

The absurdity of the argument was not lost on Eaglewood because the notary WGF challenged on technical grounds was the notary that WGF and its counsel had themselves chosen and approved. Eaglewood called the charade of contesting the validity of one’s own affidavit signed in the presence of counsel, utterly frivolous and a fraud upon the Court.

Defects or not, the judge concurred with Eaglewood because WGF had irrevocably and unconditionally agreed to the entry of judgment if they breached the settlement agreement in the first place, which they did, rendering the alleged technical errors with the COJ itself a moot point.

The COJ was therefore deemed valid and the judge ordered the Clerk to enter the judgment.

On Nov 29, a judgment for $5,866,477 was entered against WGF and Eskenazi. The index # is 651489/2018 in the New York Supreme Court.

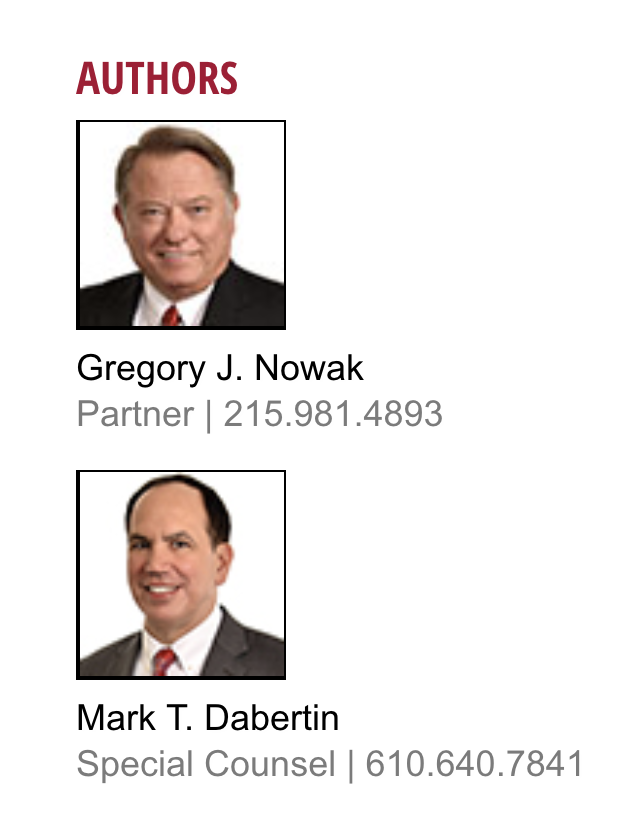

MCA Participations and Securities Law: Recognizing and Managing a Looming Threat

December 11, 2018Authors: Gregory J. Nowak and Mark T. Dabertin

Due to the high volume of relevant judicial decisions issued by New York courts over the past two years, the risk that enforceability of a merchant cash advance (MCA) contract1 might be successfully challenged as a disguised usurious loan has received ample attention in law firm white papers and published legal articles, including articles by Pepper Hamilton attorneys.2 Avoiding this risk of “loan re-characterization” is essential if the MCA industry is to achieve wider acceptance as a source of small business financing. But another risk—which we believe is largely unrecognized—could significantly throttle further expansion of MCA financing. This risk is that the funding structures MCA providers rely on to generate funding from third-party investors could be found to involve the issuance of unregistered securities. Unless an exception is available, that would be unlawful and could result in fines, penalties, defense costs and even rescission of the entire transaction, with the “issuer” being required to return investor capital.

Many MCA providers raise new funding by offering “participation interests” in their MCA contracts to third-party investors. These are usually structured in one of two ways. Under a “true participation,” the participant acquires the right to receive payments, and a resulting return on the participant’s investment, exclusively from the MCA provider. To this end, the participant receives no rights to enforce, nor any direct interest in, the underlying MCA contracts. Alternatively, the participation agreement may be structured so as to make each investor a pro rata “co-funder” of the underlying MCA contracts in an agreed-upon percentage (the “participation share”). Under this structure, the MCA provider’s contract with the merchant typically acknowledges the possible existence of “co-funders” in general terms, and does not require the merchant to ratify and accept named co-funders as they come into being. This add-on is usually accomplished through a novation to the MCA contract.

Under either of the above-described participation structures, the nature of the participant’s investment is purely passive, with no possibility for active involvement in the underlying MCA relationships. In fact, the participation agreement likely expressly prohibits such interference. The passive nature of a participant’s investment matters, because the presence of passivity, and the resulting reliance on the efforts of another party (i.e., the party offering the investment) to realize a profitable return, is a key factor for purposes of determining whether a security exists under the federal securities laws.

In SEC v. WJ Howey Co.,3> the U.S. Supreme Court established the following four-factor test for identifying the existence of a security: (1) an investment, (2) in a common enterprise, (3) with a reasonable expectation of profits, (4) to be derived from the entrepreneurial or managerial efforts of others. The facts of Howey concerned investments in an orange grove operation, where the investors were entirely dependent on the efforts of the orange grove manager/promoter to maintain the trees that the investor had invested in. In the case of an MCA participation structured as described above, all four Howey factors are arguably present. An investment is made with the expectation of realizing a profit. In addition, as discussed above, because that investment is passive in nature, its success hinges on the efforts of the MCA provider. Finally, at least one court has opined that the existence of common enterprise is inherent to any participation relationship.4

The Howey test, which seeks to identify the presence of an “investment contract,” is not the sole means for evaluating whether an investment constitutes a security. In Reves v. Ernst & Young, the U.S. Supreme Court recognized that the expansive definition of the term “security” under the Securities Act of 1933 and the Security Exchange Act of 1934 extends to other forms of “notes” besides investment contracts.5 In determining whether the “demand notes” at issue in Reves constituted a security, the court applied what is commonly known as the “close resemblance” test. Under this test, if the note in question bears a close resemblance to a type of note that has been judicially recognized as not involving a security, that note likewise will not be considered a security. For example, on its face, an MCA contract closely resembles “a short-term note secured by a lien on a small business or some of its assets.”6 However, in an MCA contract, the purchased future receivables provide the source of repayment of the advanced funds, as opposed to providing security for a lien.

This distinction is important. because in an MCA, the receivables do not yet exist, so there is nothing to lien. Rather, the MCA involves receivables to be created, presumably using the proceeds of the MCA to do so. Properly drafted MCAs sidestep all “note-like” characteristics, and make it clear that the MCA is a contract to purchase an asset (i.e., receivables) that are yet to be created. There is no sum certain for repayment – unlike a note, if the receivables turn out to be bad, the MCA provider has no recourse back to the merchant that created them. The receivables are not security for a loan; rather, the receivables are the property being forward purchased. MCAs are different in kind and extent from loans.

Notwithstanding the Howey test, and as noted above, it is possible to argue persuasively that an instrument that appears to be a security instead describes the terms of an individually negotiated contractual agreement. In this regard, in Marine Bank v. Weaver,7 the U.S. Supreme Court held that a contract between a bank and a married couple that called for the latter to pledge a certificate of deposit as security for a loan between the bank and an unrelated corporate borrower in exchange for the opportunity to share in the latter’s future profits did not involve a security. In doing so, the court distinguished the note in question from investments that fall within the “ordinary concept of a security. . . [which are offered] to a number of potential investors.”8 In contrast, the Court in Marine Bank found that the contested note created “a unique agreement [that was] negotiated one-on-one by the parties” and was therefore, “not a security.”9

In the absence of an applicable statutory exemption, the public offering of unregistered securities constitutes a criminal violation of the federal securities laws. Because securities can generally only be sold to the public by a registered broker-dealer, people who engage in selling such securities, as well as their related corporate actors, may be subject to monetary penalties for the resulting violations of law. An improperly structured MCA participation presents the risks that: (i) sales of participations made under the flawed structure could be declared void and subject to rescission; and (ii) both the MCA provider and its primary individual actors could be subject to criminal prosecution and resulting monetary penalties. In the remainder of this article, we discuss ways for effectively mitigating these risks.

Structuring the MCA participation so as to make each participant not merely a “co-funder” in name, but an actual party to each underlying MCA contract by means of a contract novation signed by the merchant and naming the individual participants, would arguably eliminate any risk that the structure might be deemed to involve the unlawful issuance of securities. Under this structure, each participant, at least in theory, could enforce the MCA contracts directly against the applicable merchants, without having to rely on the MCA provider. The main flaw with this option is that the MCA participation agreement necessarily prohibits such independent actions by the participant, because those actions could directly conflict with the economic interests of either or both the MCA provider or additional participants. Hence, any actual ability of the participant to be actively engaged in the underlying merchant relationships will be missing. As the number of participants increases to more than a handful, this structure – requiring as it does that the merchant ratify and accept every new participant as each participant is added, is unwieldy and becomes infeasible to administer.

One could also argue that including a requirement in the MCA participation agreements that the participant must evaluate independently the quality of each MCA contract before the purchase of the participation share precludes the existence of a common enterprise. However, unless each participant has its own series of MCAs, this distinction is unlikely to be of significance, because all participants are participating in the same MCA. Also, notwithstanding the obligation to conduct independent reviews, the MCA participant must still rely on the MCA provider to source qualified merchants. In addition, as noted above, the investor also must depend on the MCA provider’s success in collecting payments from merchants, which will determine whether a profitable return is achieved. Finally, where a pool of investors all share in the risks and benefits of a particular business enterprise (known in securities law as “horizontal commonality”), the resulting presumption of a common enterprise is extremely difficult to disprove.

In view of the above, we suggest that the best way to manage the risk that the participation structure might be viewed as involving the unauthorized issuance of securities is to embrace the substance, if not the precise letter, of the federal securities laws. Specifically, by structuring the participation in a manner that complies with the safe harbor from the requirement to register securities described in Section 506 of the SEC rules under the Securities Act of 1933. This entails: (i) only selling participations to accredited investors; (ii) describing the applicable risks (i.e., the risk factors) and potential conflicts of interest in an addendum to the participation agreement; (iii) making sure that all sales of participants are made on a one-to-one basis, with no general solicitation or marketing; and (iv) advising participants that the resale of their participation share may be subject to a one-year minimum holding period. (Of course, if the MCA pays off before the one year period and extinguishes the MCA, that is not an issue under this rule.)

We caution that the securities laws are both difficult to navigate and prone to divergent interpretations. The consequences of misinterpretation can be severe and could result in the rescission of existing participations and monetary penalties. Hence, this is not a DIY proposition.

Pepper Points

-

The risk that an MCA participation structure could be found by a regulator or court to constitute the unlawful issuance of securities is under appreciated, and has serious consequences that could throttle the availability and growth of MCA financing.

-

Although legal arguments can be made in support of the position that the most commonly used MCA participation structures do not involve the unlawful issuance of unregistered securities, none of those arguments is sufficiently persuasive to preclude the need for additional risk mitigation efforts.

-

Mitigation plans for managing the risk that a given MCA participation structure involves should incorporate complying with the substance, and the precise letter, of the federal securities laws.

The federal securities laws are difficult to navigate and prone to divergent interpretations. The consequences of misinterpretation are severe and could include the rescission of existing participations and assessments of monetary penalties, including against individual actors.

Endnotes

1 An MCA is a business financing option that involves the advance of funds to a merchant, typically to assist the merchant in managing its short-term cash flow needs, in exchange for the sale of a specified percentage of the merchant’s future receivables at a sizeable discount. It is a relatively new offshoot of “factoring,” which likewise involves the purchase and sale of receivables at a discount in exchange for an advance of funds to a business, with the primary difference being that the receivables in the case of MCA financing are not yet extant. An MCA contract might be deemed a disguised usurious loan for many reasons, including the inclusion of a set term within which the advance must be repaid in full to avoid default. The most critical factor in this regard is whether the MCA provider is looking to the purchased receivables for repayment, or to the merchant itself or its individual owner(s); e.g., in the form of a financial guarantee given by the owner(s).

2 For a broader discussion of MCA financing, and the risk of re-characterization as a usurious loan, see: https://www.pepperlaw.com/publications/recent-litigation-illustrates-why-merchant-cash-advances-are-not-loans-2017-04-20/.

3 328 U.S. 293 (1946).

4 Provident National Bank v. Frankfort Trust Co., 468 F. Supp. 448, 454 (E.D. Pa. 1979) (By its “very nature” any participation involves a common enterprise.).

5 494 U.S. 56, 64 (1990) (“The demand notes here may well not be ‘investment contracts,’ but that does not mean they are ‘notes.’ To hold that a ‘note’ is not a ‘security’ unless it meets a test designed for an entirely different variety of instrument ‘would make the Acts’ enumeration of many types of instruments superfluous’ Landreth Timber, 471 U.S. at 692, and would be inconsistent with Congress’ intent to regulate the entire body of instruments sold as investments, see supra at 60-62”.).

6 Id. at 65.

7 455 U.S. 551 (1982).

8 Id. at 552.

9 Id.at 560. In Vorrius v. Harvey, 570 F. Supp. 537, 541 (S.D.N.Y. 1983), the court followed Marine Bank in finding that a contested loan participation agreement involved an individually negotiated contract versus a security. A key factor in that case, however, was the existence of a comprehensive federal regulatory scheme apart from the federal securities laws in the form of banking laws and regulations, which made application of the former unnecessary for purposes of protecting the interest of investors. No such alternative regulatory scheme exists in the case of the MCA industry, which is generally unregulated.

The material in this publication was created as of the date set forth above and is based on laws, court decisions, administrative rulings and congressional materials that existed at that time, and should not be construed as legal advice or legal opinions on specific facts. The information in this publication is not intended to create, and the transmission and receipt of it does not constitute, a lawyer-client relationship.

1st Global Capital Consents With SEC

November 28, 2018Subject to approval in two courts, 1 Global Capital LLC (aka 1st Global Capital) has confirmed it will consent with the SEC to be permanently enjoined and restrained from violating securities laws. The papers were submitted to the Court yesterday.

Though the terms include 1st Global Capital’s California counterpart, 1 West Capital, LLC, there is no connection to the separate securities charges pending against company founder and former CEO Carl Ruderman. Ruderman is seeking to dismiss those charges. According to court records, his reply to the SEC’s opposition is due this Friday.