Business Lending

SBA Loans Go Online: A Q&A With SmartBiz

November 28, 2017 A while back, a merchant deBanked interviewed told us they had obtained what sounded like impossibly good terms from an online lender not known for low rates. When I requested a fact check of it, we learned that the online lender had actually referred the borrower to SmartBiz and that SmartBiz had secured an SBA loan for them. It was so seamless that the borrower had hardly noticed.

A while back, a merchant deBanked interviewed told us they had obtained what sounded like impossibly good terms from an online lender not known for low rates. When I requested a fact check of it, we learned that the online lender had actually referred the borrower to SmartBiz and that SmartBiz had secured an SBA loan for them. It was so seamless that the borrower had hardly noticed.

Curious, I caught up with Sean O’Malley, president and co-founder of SmartBiz last month at Money2020. Below is a modified excerpt of our conversation:

deBanked: [tells the above story about the merchant who got an SBA loan] – So you actually have other alternative lenders and online lenders going through you too. What is really the biggest channel that you tap into to get small business owners to you? Is it other online lenders or do you go direct to merchants?

O’Malley: Well, there are three different areas where customers come to us. The first is through our marketing efforts. We have our own online presence and marketing initiatives that go on, where small business owners are interested in the SBA loan product. The second area lies in our strategic relationships. These are partnerships with companies like Sam’s Club where we’re actually on their lending center; we have been doing that for a number of years. Another channel would be partnerships with companies like Fundera who bring customers to us through their online channels.

deBanked: How about like Lendio?

O’Malley: Yes. We’ve built a relationship with them over the years. Lastly, the third area is the independent financial consultant channel, like our partnerships with accountants.

deBanked: Okay. Didn’t SmartBiz recently celebrate a major milestone?

O’Malley: Yes! We recently passed the $500 million threshold of originated capital on the platform.

deBanked: All SBA loans?

O’Malley: Correct, all the originated capital is a result from SBA 7(a) loans. Today, we have six bank partners on our platform who are doing SBA loan origination. It’s all been facilitated through our platform. There are really four major components to what we do. The first part is we provide an online presence and origination solution for small businesses. They come through our technology solution and then they go through an application process where we’re able to pre-qualify them. So, that’s the first piece. The second piece is really the technology platform around packaging of the loan.

deBanked: What do you mean by packaging?

O’Malley: After a business pre-qualifies, there are still documents that need to be captured and some of the specific analysis also needs to be done. A large piece of that is automated through our platform. Some of it does require sort of a white glove experience for small business. We provide that as well. Then the third piece is the bank’s underwriting platform, where we digitize the bank’s underwriting and provide them with an underwriting platform that they license from us. Leaving us with the fourth part, the marketplace.

deBanked: Can you explain the fourth piece, marketplace?

O’Malley: The core of what we do is we connect small business owners with banks. And the interesting part of that is that because we’re the marketplace, we’re able to say yes more to the small business than any single bank because they all have their own different credit boxes. In effect, we’re able to get more customers approved because we’re able to fit more use cases for that small business owner. If you combine all these, the ultimate value prop is that we’ve reduced the time to originate a loan. It traditionally takes about 120 days for a bank to originate an SBA loan. We’ve reduced that to as little as seven days. And on the bank side, we’ve reduced their costs up to 90%. As a result, we’ve made these loans more profitable for banks. And they’re then more willing to originate as part of their standard business. Whereas you know, in the small business space, banks have not been super eager to be making smaller sized loans because it costs as much for them to originate that type of loan as it does for them to originate a $5 million loan. So, we’ve made it super efficient.

deBanked: So you’re kind of filtering out applicants on your own that they would normally have to deal with.

O’Malley: That’s right. Our platform allows us to filter out all the applications and only feed a bank the deals that they can do. When we provide a deal to a bank, they’re funding it anywhere between 90-95 percent of the time. They’re funding the deals that come from us because we have the knowledge of how the bank looks at their deals.

deBanked: Is there a world in which you move outside of SBA loans and potentially offer other types of bank loans or maybe even non-bank loans or facilitate them? Not necessarily make them, but facilitate them?

O’Malley: We recently just launched a conventional bank loan. So, yes, we are expanding on our product line, and we did this as a result of really looking at that type of product and filling a gap in the marketplace as well. We’re trying to help the customers out and support their needs.

deBanked: Are you noticing a trend with maybe borrowers applying for loans on like a mobile phone? I mean, any loan is a pretty big commitment, right? They go online and apply for $5,000, you know what I mean, for a personal expense or whatever and that’s not such a huge deal because it’s a small loan. I think an SBA loan is a much bigger commitment, you know, it’s long term. Are you seeing borrowers apply for the loans you offer from a mobile device?

O’Malley: About a quarter of our small businesses start the applications over a mobile device. And they are able to get pre-qualified through a mobile device. That said, the majority of borrowers still want to talk to someone. There are still a lot of traditional relation-based elements to a small business lender. When somebody is taking out a couple hundred thousand dollars, like you said, there needs to be some white glove experience for that. And it can’t just be 100% automated. In fact, small businesses a lot of times don’t want 100% automation.

deBanked: Because it’s such a big commitment.

O’Malley: That’s right. And that’s where the market is today. In the future, we look to certainly automate as much as possible, but we hyper-target where we interact with the customer so that we provide the most unique customer-centric solution so that they feel comfortable about the process. If you look at our TrustPilot customer reviews that we use on our site, you will note that people really speak very highly about their experience. We’re super proud of that because we’ve been able to match up technology with people in the right way so that we can hyper-target where human interaction is needed to make sure that the customer feels at ease with the process. We’ve been able to become the trusted source for them getting the loan that they’re looking for.

deBanked: Do you think in the future borrowers will apply for SBA loans entirely online? Will there be an age where they’re not necessarily going to the bank to meet somebody to talk about an SBA loan? Do you think it’s all going to kind of become like an online digitized process or will it always be a layer of I wanna go and sit and talk with somebody in the bank office?

O’Malley: Well, we’re proving small businesses want to do it primarily online. In fact, you know, the point too is that if you just consider the small dollar amount category, we are now the largest provider of SBA loans in the country for loans under $350,000.

deBanked: Anything else I should know about SmartBiz?

O’Malley: We really seek to be an advocate for small businesses. We have gone beyond SBA in supporting our customers with the more conventional product, but we’re always trying to get businesses into SBA loans because it’s the best product out there. And so, our focus is always first and foremost trying to get our businesses SBA loans if at all possible. And it appears to be working. Recently, we were named as one of the fastest growing companies in the Bay area. We’re looking at certainly scaling this solution with as many small businesses as possible.

Canadian Merchants Show An Appetite For Capital

November 25, 2017In Canada, the average deal size for a merchant is anywhere between $20,000 and $30,000 in funding, depending on who you ask. That’s why when one startup recently funded a $300,000 CAD advance from its balance sheet to a Canadian merchant, the deal turned some heads. While it’s unclear whether this amount could be indicative of a trend unfolding at our neighbors to the North, Canadian small businesses are preparing for some changes in the industry landscape in 2018.

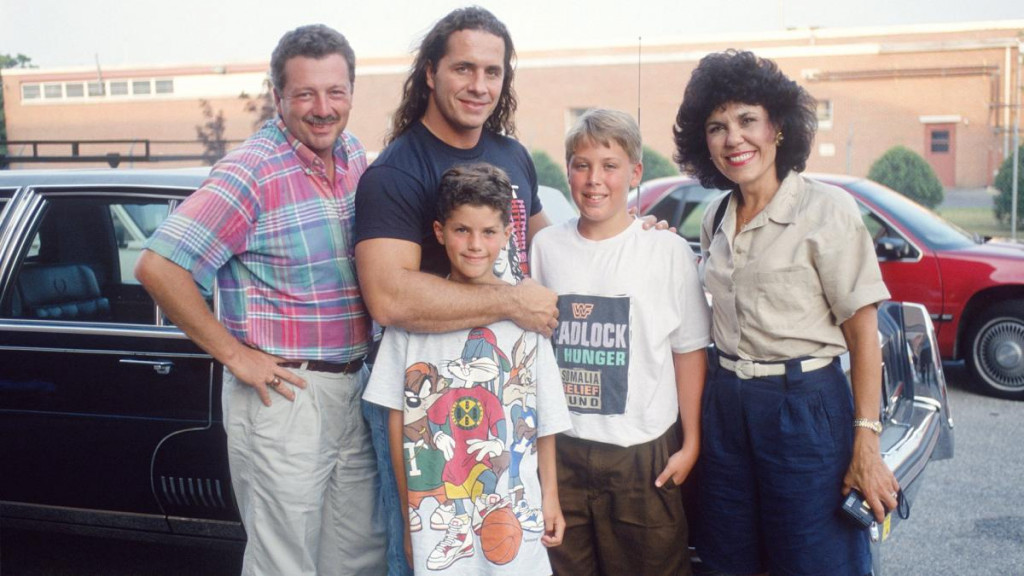

SharpShooter Funding, whose name depicts the famous wrestling move of the WWE’s Bret “The Hitman” Hart, was behind the $300,000 deal with an Eastern Canadian grocer.

If you’re wondering how a merchant funder and WWE legend became partners, chalk it up to a combination of fate and timing. Paul Pitcher, SharpShooter Funding managing partner, has been Hart’s biggest fan since he was a kid. Pitcher got the opportunity to meet his hero when was just 10 years old. It was then that the green shoots of friendship formed, and today the WWE’s Hart is acting commissioner of SharpShooter Funding, having helped to launch the business.

Canadian Merchant Landscape

To get a taste of the Canadian merchant financing landscape, consider that the three top Canadian funders deploy $20 million and $25 million per month combined, explained David Gens, president and chief executive of Merchant Advance Capital, which is included among the top three funders. That’s up from a range of $15 million to $20 million earlier this year.

And while a $300,000 advance may not seem like something to write home about for U.S. funders, it’s a big deal in the Canadian market. The culture among small businesses in the Great White North is different and more conservative than their US counterparts.

“It’s a function of the size of the merchant,” Gens explained. “The typical single-location storefront merchant is going to qualify for $30,000 to $50,000. It takes a larger and more established business, whether it’s a multi-location merchant or a business that is in the B-to-B space, a manufacturer, distributor or wholesaler to be large enough to qualify for large financing.”

Meanwhile there are some changes to small business taxation that are coming down the pike that may influence demand for credit, Gens noted, though the precise shape any changes to the tax law will take remains unclear.

“They will reduce the small business taxation rate on the face of it. But for businesses where they hold cash or need to hold cash, it’s a gray zone as to whether or not they will be able to hold financial assets in those businesses. The government is going after companies that are holding investments. But there’s a gray line as to what is a holding company that is holding an investment and an operating company holding a buffer because of seasonality or cyclical demand. We have yet to see what the rules end up being exactly,” Gens said.

Anatomy of the Deal

In the case of SharpShooter Funding, the grocer merchant originally came to the funder for less than $300,000 but qualified for more, bringing the funder’s tally for a single day’s deals to more than $500,000.

“We never thought we’d hit this milestone in the Canadian market. But the file was right, and the timing was great,” Pitcher told deBanked. Now that they’ve gotten a taste of it, SharpShooter Funding hopes to do more deals of this nature. “For a small funder like us to double the size of a big funder was a big moment for us, especially in the Canadian market,” Pitcher said.

Merchant Advance Capital’s Gens said his company is prepared to take on the risk for deals at even a higher threshold. “Our average is $35,000 to $40,000, and the largest deal we’ve ever done was $600,000. I don’t want to steal their thunder, but there have been larger deals,” said Gens. “A few funders may syndicate when deals get that big, but it’s not an inconceivable size.”

OnDeck, which similarly has Canadian operations, lends up to $250,000 CAD in Canada. OnDeck has extended more than $7 billion in online loans across 70,000-plus customers across the United States, Canada and Australia.

As for SharpShooter Funding, Pitcher said the funder has been on the sidelines for larger deals because they don’t want to grow too fast. He’s been turned off by other funders doing deals within a couple of months of launching and then being forced to close their doors.

“Our capital has always been strong. It’s not that we can’t afford to lend larger amounts. It’s because we want to make sure we’re doing it right from the start,” Pitcher said, adding that SharpShooter Funding has only had its doors open in Canada since June 2015, though its corresponding U.S. business, First Down Funding, has been around since 2012. “It’s been a work in progress, and I love every day of it! We’re only getting started, and I am 100% excited for the future,” he said.

The Canadian grocer reached out to SharpShooter Funding in response to Google advertising. The affiliation with the Bret Hart association didn’t hurt. Pitcher explained there is a seasonality tied to the merchant’s business, evidenced by a couple of months or more each year in which revenue is spotty, that made the grocer unattractive for banks to fund. “That’s why those sized deals are difficult to put out and banks won’t put out, because of seasonality,” Pitcher said.

SharpShooter Funding was not deterred by that. “We were really able to gain in-depth trust and visibility into this merchant from the first call to the last call. There was never a problem with him mixing up stories. Just the honest truth. From his references to his landlord, everyone involved made it clear he was here to work with us and not to play games,” Pitcher said.

Pitcher was impressed by the business owner’s work ethic. “He’s a roll-up-your-sleeves entrepreneur who didn’t borrow $1 million from his father. No bank loans. Six years ago, he rolled up his sleeves and made it work. Now he’s in a situation where banks won’t lend to him. But we will,” he said.

The merchant’s bank statements also made sense to the funder given their consistency, predictability and transparency. “Whenever we ask for finances from someone and that merchant can get them to us in an organized fashion in less than an hour, it speaks wonders. It means they’re honest and ready to play ball. And that’s what we want,” Pitcher exclaimed.

The merchant plans to use the capital for an expansion into a new food product line. If he pays off the advance early the funder will lower the rate.

Take a Break From Funding This Thanksgiving

November 21, 2017This Thanksgiving…

Step back from the daily grind

Those merchants eager for your cold calls can wait

There’s no need to start worrying about next year just yet

It’s Thanksgiving

So hug an underwriter

Kiss a broker

Think about your favorite merchant

And pay no attention to the algorithms automating your job

Give thanks

Because nobody wants to hear you recap your holiday like this

Or this

Or this

Enjoy the Holiday!

You should also check out our 2016 Thanksgiving Day post and 2012 Thanksgiving Day post.

Kabbage Taps Debt Capital Markets for a Cool $200 Mil

November 16, 2017 Kabbage has been accessing the capital markets fast and furiously, most recently on the debt side. Today they’ve announced a new $200 million asset backed revolving credit facility with Credit Suisse. Just a couple of months ago, Kabbage attracted $250 million in equity to its coffers from SoftBank, which the alternative funder will direct toward ongoing operational expenses and expansion.

Kabbage has been accessing the capital markets fast and furiously, most recently on the debt side. Today they’ve announced a new $200 million asset backed revolving credit facility with Credit Suisse. Just a couple of months ago, Kabbage attracted $250 million in equity to its coffers from SoftBank, which the alternative funder will direct toward ongoing operational expenses and expansion.

With the Credit Suisse deal, the tally for Kabbage’s debt funding capacity reaches $750 million. “The new revolving credit facility will be issued by Kabbage Asset Funding 2017-A LLC, a wholly owned subsidiary of Kabbage Inc,” according to a press release.

Kabbage expects the credit facility will help them to scale faster. They plan to use the credit to add bigger small businesses to its client roster as well as extend higher lines of credit with longer durations.

“The new revolving credit facility with Credit Suisse is a debt round. Those funds are for our small business customers, and will be used to continue to provide them with easy access to working capital,” Deepesh Jain, Kabbage Head of Capital Markets, told deBanked.

It’s Kabbage’s maiden credit facility to be rated by credit rating agency DBRS. “The top two classes of the multi-class transaction earned investment-grade ratings of ‘A’ and ‘BBB’ and are collateralized entirely with assets originated through Kabbage’s fully-automated underwriting technology,” according to the press release.

Jain told deBanked the DRBS rating is highly significant. “It strongly demonstrates the proven success of Kabbage’s fully-automated platform and its data-driven risk analysis for small business lending. It speaks to the company’s leading position in the SMB-lending marketplace and Wall Street’s confidence in Kabbage,” he noted.

As Jain pointed out, Credit Suisse has been an early supporter of fintech. Indeed, the Swiss bank a year ago similarly provided a $200 million asset-backed revolving credit facility to another alternative funder, OnDeck.

Alternative Funders and Bank Partnerships in the Spotlight

Jain declined to comment on whether Credit Suisse might be interested in Kabbage’s lending platform for its own use. Alternative funder and banking partnerships were recently thrust into the spotlight with a lawsuit filed by a Massachusetts-based small business owner against Kabbage and Celtic Bank, which have had a partnership for at least several years.

The lawsuit alleges that the funding model of the defendants “was designed to evade usury laws,” according to The National Law Review. Apparently, the plaintiffs, which are listed in the public filing as Alice Indelicato and NRO Boston, had several small business loans and now accuse Kabbage of “renting” Celtic’s bank charter. Jain declined to comment on the lawsuit and the plaintiffs couldn’t be reached.

Capital Markets Pipeline

Meanwhile, at the rate they are going, we could see Kabbage tap the capital markets again in 2018. “Capital markets are something we will continue to explore to further diversify our funding options,” said Jain.

The Bad Broker And Merchant Due Diligence

November 15, 2017 There may be a rogue broker on the loose. The scam involves a fraudulent Letter of Intent (LOI) falsely claiming to be that of a major funder designed to resemble the real McCoy. Events like this place a spotlight on the risks associated with this market and is a reminder that not all small businesses are armed with the right information.

There may be a rogue broker on the loose. The scam involves a fraudulent Letter of Intent (LOI) falsely claiming to be that of a major funder designed to resemble the real McCoy. Events like this place a spotlight on the risks associated with this market and is a reminder that not all small businesses are armed with the right information.

deBanked was contacted by a victim of the fraud, Noah Grayson, managing director and founder of Encino, Calif.-based South End Capital. Grayson said the real victims are the merchants who get taken advantage of by these scams. In this case it was a New York-based small business owner who took on too many MCAs.

Grayson is quick to point out the MCAs were not at fault and each may have even thought they were the first position funder since it all unfolded so quickly. “They’re just trying to do business and provide financing to businesses, and they got burned as well. They’re going to take some degree of financial loss because of this and maybe more,” Grayson said.

False Pretenses

When Grayson reviewed an email that he received from the borrower, which included a copy of the LOI, he knew immediately that it was fraudulent and the borrower had been misled. “It was a fraudulent LOI and we had no record of the borrower or the brokers who provided it in our system,” Grayson exclaimed.

As it turns out, the borrower was tricked by the fake LOI that sought to leverage the reputation of South End Capital’s brand to coerce him into taking out $260,000 of MCAs from four separate funders. They did it under the false pretense that South End Capital would then consolidate those positions in 10 days and extend as much as $900,000 more in working capital to grow the business.

To be clear, South End Capital does offer a genuine MCA consolidation loan program. Grayson had never agreed to consolidate the business owner’s MCA positions, however, or provide an additional $900,000. That part was fabricated. This left the merchant holding the bag for more than a quarter of a million dollars in MCAs, placing his business, which has been successful since the 1960s, on the brink of bankruptcy protection in the interim because of the crippling weekly payments.

Fraud Prevention

Andi McNeal, research director at the Association of Certified Fraud Examiners, or ACFE, said she has seen this before, only on the consumer side of the industry. “Loan consolidation fraud for credit card debt is very common in the consumer space, and it’s not surprising to know that similar schemes are popping up in the small business space, too,” she said.

She went onto explain that because a small business is typically run by a small management team who typically aren’t trained in fraud prevention, they often adopt the same mindset as they do in personal finances. They don’t always have the necessary checks and balances in place, which can place them at risk of being victimized by such schemes.

“Sometimes they’re not savvy enough to detect those types of scams coming at them,” she noted. “Certainly, big businesses can fall prey to this, but it’s less common.”

Staying on Defense

The recent saga unfolded over a period of six weeks. Meanwhile Grayson has outlined some red flags for small businesses to watch out for to prevent becoming the next victim to a new fraud.

“If what you’re being told seems suspicious or doesn’t make sense, question it. Ask questions and get more information,” said Grayson.

Another rule of thumb is to stick to the document in front of them. Again, this may just be a case of a few bad apples spoiling the bunch, but sometimes brokers tell small businesses something contrary to what appears in front of them on the official document. “The LOI spells it out,” said Grayson, adding that when in doubt the borrower should defer to the document.

The merchant should also take it upon themselves to call the lender whose name is on the LOI to verify its authenticity before signing it or providing any upfront fees.

“In this case, it was a fraudulent document and it didn’t help out the borrower but calling us to confirm it initially would have. Most of the time, looking at what’s written out on paper from the verified source will help and getting a verbal or email confirmation from the actual lender, certainly will,” Grayson said.

Another defensive step merchants can take is to simply review the website of the brokers and funders and look for names, press releases and past closings, details which Grayson noted were all missing from the broker in question’s site.

“Anybody can say they make loans and provide financing. They could tomorrow put up a website for a couple bucks and say they’re a lender and start taking applications. But just because there’s a website doesn’t mean they’re legitimate,” Grayson said.

He’s suggesting merchants check out the names of the principals and employees on the site. Google is their friend to check for any history of loans closing. Look for closing announcements and any complaints tied to the entity in question. Call the Secretary of State Department and inquire about any complaints.

At the end of the day, it comes down to the merchant doing their homework. “A lot is on him. He should have done more research, absolutely. But anybody can be coerced or tricked if the right things are said,” said Grayson.

If a merchant does find themselves in a situation where they fall victim to a fraud, there are steps they should take. McNeal said that while each situation is unique, a good first step is always going to be to reach out to a trusted legal counsel.

“They can help guide you through the process of what the options are. Do you have recourse? Does the situation call for insurance to help cover the losses? They also can advise on which law enforcement or government agencies are the most helpful – should the case be referred to the local authorities or do they need to bring in the FBI,” the ACFE’s McNeal advised.

More Pervasive

Grayson’s fear is that this is not an isolated incident. He has reason to be cynical, as this was the second incident this year resembling the most recent situation that they have experienced.

The first incident was relayed to South End Capital by a handful of borrowers about one specific MCA broker. No fraudulent documents were ever recovered, but the borrowers recalled the harrowing details of the incident

“Per the multiple borrowers, the broker used our real LOIs and lied to borrowers about how to interpret them to coerce tens of thousands of dollars in upfront fees from them. For example, for an LOI we issued for our SBA loan program that listed what SBA guarantee fees would be due at closing, he would convince them that that fee was his and they needed to pay it to him upfront to proceed,” Grayson explained.

The small business owner at the center of the scandal declined to comment, and it’s unclear whether they were the one to initiate the original communication with the broker or vice versa.

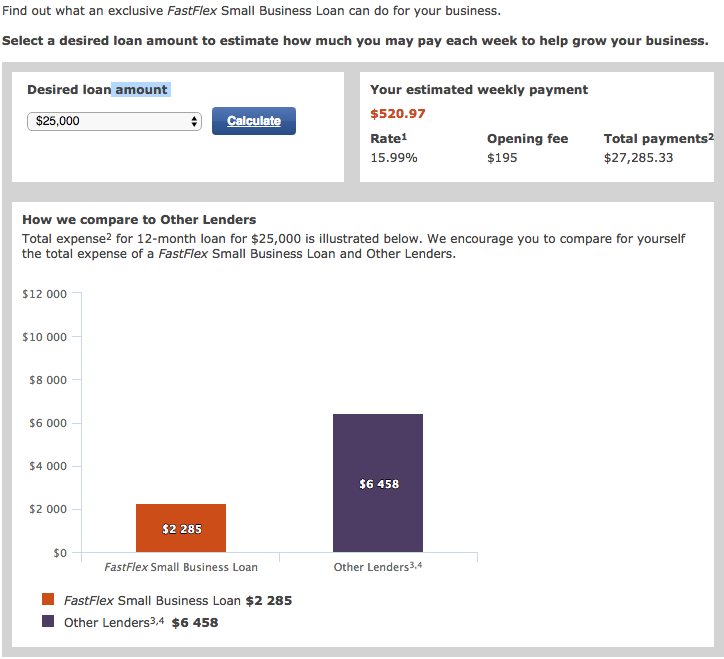

Don’t Forget About FastFlex

November 13, 2017 The OnDeck-Chase partnership isn’t the only game in town when it comes to fast weekly payment bank loans. Wells Fargo announced their own program, called FastFlex, in 2016 as part of a goal to lend $100 Billion to small businesses over five years.

The OnDeck-Chase partnership isn’t the only game in town when it comes to fast weekly payment bank loans. Wells Fargo announced their own program, called FastFlex, in 2016 as part of a goal to lend $100 Billion to small businesses over five years.

deBanked was shown an anonymized bank statement snippet recently of a merchant that was purportedly being debited daily by Wells Fargo. So we reached out to Wells to ask if there might be a daily payment loan product that had not yet been announced.

“[F]or Wells Fargo’s FastFlex Small Business Loan, we only offer the weekly payment option, in which required payments are made on a weekly basis automatically deducted from the customer’s business-deposit account,” they responded. “None of our Small Business loan products have daily payments.”

While the mystery remains unsolved, Wells already compares its FastFlex product to OnDeck, Kabbage, and CAN Capital on their website. Loan amounts ranging from $10,000 to $35,000 come with 1-year terms, weekly repayment, and interest rates starting at 13.99%. Their loan calculator approximates a 1.09 total cost factor on a $25,000 loan.

Their underwriting criteria comprises of cash flow history, existing credit obligations, credit experience, payment history, and relationship status with Wells Fargo. Merchants are funded the day after accepting the terms.

Users on a handful of message boards have reported that cash flow history weighs heavily in the approval.

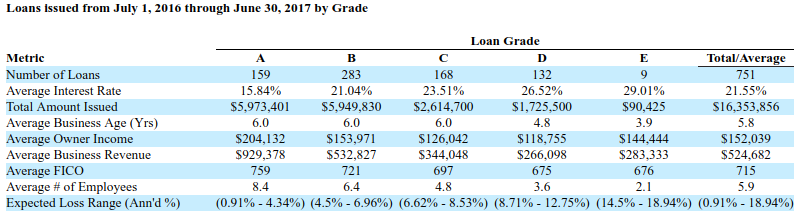

StreetShares Reports $6.2M Loss For Fiscal Year 2017

October 31, 2017StreetShares, the veteran-run small business lender, continued to post sizable losses, according to their June 30th fiscal year-end financial statements. The company had a $6,193,154 loss on only $2,168,067 in revenue. While StreetShares has generated significant buzz for their particular focus on military-owned small businesses, the lender only made 751 loans in the 12-month period and there is no requirement that the businesses they lend to actually be military-owned.

The company spent more on payroll and payroll taxes alone ($3,258,960) than they earned in revenue. They had 32 full-time employees and 1 part-time employee as of June 30th.

“As an early stage, venture-funded company that is not yet profitable, we rely heavily on capital investments to fund our operations,” the company wrote in their annual report. “Based on our current financial situation, it is likely we will require additional capital within the next twelve months beyond our currently anticipated amounts to fund the operations of the Company.”

The chart plotting their loan performances by grade below is from their annual report:

Their loan amounts typically range from $2,000 to $150,000 and require weekly payments for anywhere from 3 months to 3 years.

Even though the company spent nearly triple on marketing in this fiscal year ($1,727,478) versus the previous year ($579,331), revenue only doubled.

StreetShares plans to raise additional capital towards the end of this year through a Series B Round.

View From The C-Suite: Alternative Funding Execs Talk Shop, The Landscape, And The Future

October 30, 2017 Alternative funders have had a roller coaster 2017 with highs and lows that will likely be remembered as a high-stakes time for the industry, one in which the rubber met the road for many and the market landscape shifted for everyone from funders, to merchants to brokers.

Alternative funders have had a roller coaster 2017 with highs and lows that will likely be remembered as a high-stakes time for the industry, one in which the rubber met the road for many and the market landscape shifted for everyone from funders, to merchants to brokers.

Three C-Suite executives in the alternative funding space — Christine Chang, CEO of 6th Avenue Capital, Heather Francis, CEO of Elevate Funding and Torrie Inouye, National Funding president — spoke with deBanked, offering their take on some of the industry shakeups, direction of the alt lending space and upcoming developments at their respective companies.

All three execs are embracing what appears to be shaping up as a bigger and better 2018 with plans on the horizon for new products, relationships and deals but also where there could be further shakeout as the shift in the industry landscape takes hold.

Industry Landscape

6th Avenue Capital, provides short-term funding to merchants that Chang describes as “high touch, high tech and fast.” The company is building an SEC RIA compliant infrastructure as Chang believes that MCA regulation will take place over the next several years. Chang said she is sympathetic to the banks and the onerous rules that they must follow, and whatever form the industry regulation eventually takes on, the company will be ready for.

A recent story in The Wall Street Journal points to community banks comprised of those with less than $10 billion in assets historically funding local merchants in what’s dubbed character-based lending. As the name suggests, the underwriting standard for the loans was tied to the character of the business owner, which the lender knew based on personal relationships in their own communities.

The financial crisis gave rise to greater regulation, driving a spike in that model and the rest is history. Small banks were forced to direct their resources toward risk management and compliance instead of adding more personnel to service loans. The WSJ quotes a small business lender that bears repeating: “When they created too big to fail, they also created too small to succeed.”

When that door closed, however, another one opened, creating the opportunity for alt lenders to service a niche that was getting left out in the cold.

“The alternative funding industry is here to stay. That’s good news for MCA and fintech in general. There’s a need for fast funding and there will continue to be a trend toward that,” said Chang.

Banks, meanwhile, have started coming to the fintech table to compete for deals. “We’re in the process of speaking to a number of banks, some quite large and some regional, that have expressed an interest. We think this is a great opportunity for them. The idea is that we’d help them to serve a population of clients that they would not otherwise be able to serve,” said Chang.

6th Avenue has had discussions about white labeling and customizing the platform for institutions. “We would run everything for them,” said Chang.

In addition to possible new banking relationships, 6th Avenue Capital, backed by a private family and institutional investors, will expand the business model to include more investors on its platform. “We are in discussions with a number of significant international investors. It’s in the works. We’re building an institutional infrastructure, so it was always contemplated,” she said.

Elevate Funding, whose is 100% referral-based and whose product suite is comprised of a trio of MCA solutions, is coming up on its three-year anniversary in December.

“When I created Elevate, I did it with the purpose of providing a product to high-risk merchants. That’s who we deal with. We’re not dealing with credit scores. There is a level of risk to who we work with. Elevate was created to provide a product that is going to fit their needs and also provide a product that doesn’t treat them like they’re high risk. That’s who we are,” said Francis.

Gainesville, FL-based Elevate recently hired Michael Gaura to spearhead a new MCA product that the company is rolling out in 2018. Francis held the details of the new funding product close to the vest, but she did offer her views on the direction of the MCA and alternative lending space.

“I see difficulty in the coming years, especially in 2018, for qualified lead flow. You have a lot of big banks that are getting into this industry. And that’s a lot of marketing dollars that you’re competing against.”

She points to JPMorgan Chase, American Express, Square and PayPal, saying they are “huge marketing dollar companies” with tremendous access to customers on their respective platforms.

“There’s going to be a shakeout of what can you reach, who can you reach, can you get them the first time? How do you engage them to where they only want to work with you and they’re not submitting 20 applications for every website they come across?”, Francis said.

San Diego, Calif.-based National Funding is a balance sheet lender whose primary product is loans, not MCAs. The broker factor has changed significantly for the lender in a very positive way this year. “We’re really seeing sizeable growth in our broker channel in 2017 and have designed a strong and consistent process for our broker clients” Inouye said. The leads have been driven by a variety of factors, not the least of which comes down to CAN Capital and Bizfi’s loss being National Funding’s gain.

“That’s a factor we can’t ignore. The broker community has rewarded us for being consistent and building those relationships and being a partner to them,” Inouye said. “We definitely saw an uptick in business when they left the space. I can say we’ve continually experienced sizeable growth in our broker channel year over year but 2017 was beyond what we had expected. It surpassed other years.”

Incidentally, National Funding was one of the earliest alt funders on the scene along with CAN Capital in the 1990s. CAN’s fate started unraveling about this time a year ago.

“It’s not positive when you see that happen in the industry. However, we are really focused on what we’re doing and the decisions we’re making internally. I think that’s why we’ve consistently had profitable growth over the years. We’ve stayed true to our underwriting principles and the market seems to have rewarded us. We were consistent and not erratic. Brokers know they can rely on us and feel confident that we would quickly fund their deal once we issued an approval,” said Inouye.

The Broker Effect

Elevate, a balance sheet funder, relies on outside brokers and referrals for deals. “I don’t find it a disadvantage for us not having an internal sales team. A lot of companies in this space have the ability for a chief marketing officer who focuses entirely on leads. Elevate isn’t there yet. Will we be there in five years? Maybe. Marketing can change by that time,” Francis said.

6th Avenue Capital welcomes relationships with brokers as well. “We have an in-house business development team that works with brokers. 6th Avenue Capital is also considering direct sales in niche strategies in its future,” said Chang.

6th Avenue Capital has a starter program in which there are no guarantees but considers businesses that have been in existence for less than a year and businesses with credit scores of 500 or more. Plus, they’re willing to do consolidations up to two advances.

In addition, 6th Avenue Capital is open to offering financing to brokers. “It’s really good in that there is an alignment of interests and allows brokers to participate in the deals they put forth. If they think the merchant is credit worthy and a terrific opportunity, they participate. Everyone has skin in the game and interests are aligned,” Chang said.

Technology

While technology is at the core of fintech, all three of the companies take a hybrid approach when it comes to credit underwriting comprised of a tech platform and the human touch, which perhaps keeps character-based lending alive in some form.

With respect to fintech, “6th Avenue Capital’s philosophy is that technology is a tool to supplement human underwriting. We use technology to detect fraud, manage workload processes and manage risk. We do not use technology to make our final decisions,” said Chang.

Specifically, 6th Avenue Capital benefits from research, artificial intelligence and predictive technology of its sister company Nexlend Capital. 6th Avenue Capital has customized Nexlend’s consumer lending algorithmic intellectual property, which uses machine learning and credit analysis with high speed execution to make better and faster decisions.

Elevate also takes a dual-approach to its underwriting process. “I believe in a hybrid method. You have to have someone looking at it, to have eyes on the paper at some point in the process. This doesn’t mean a computer system can’t help to weed out what might not meet the criteria, but I do believe there needs to be a person reviewing the files,” Francis said.

National Funding was started as an equipment leasing company. “We apply some principles we learned as a leasing company and take into account all of the attributes that go into that business in addition to FICO and cash flow,” Inouye said.

Automation is an area of technology that they continue to look to for innovation and process efficiencies. “We do serve our customers online, but we also provide a human contact as well. We deliver a loan experience that builds trust and confidence with customers. We try to deliver on what our customers want in the most efficient way,” said National Funding’s Inouye.

National Funding continues to look at construction deals and accepts them as a niche in their portfolio, which Inouye said differentiates the company. “It allows us to be more flexible and comfortable with certain industries that other lenders might stay away from.”

Corporate Culture

2017 has been a roller coaster year for fintech including alt funders. While there have been plenty of bright spots, there was also some fallout that left veteran players scrambling to salvage either their reputation, status as a funder or both.

SoFi has been at the center of controversies that resulted in the Mike Cagney leaving his chairman post with plans to step down as CEO. Most recently, the lender has removed its application for a bank charter, according to reports.

We asked Elevate’s Francis about it. “SoFi is a very big company. They’re to the level where the CEO has people to answer to. They have a checks and balances system they need to go through,” said Francis. “It worked, and they removed him.”

Francis maintains an open-door policy with her employees, and she says all you can do is focus on your house and keep your house in order. “My door is always open. That’s our office policy. They use that quite frequently; it’s a catch 22,” she said with a laugh.

Fintech and Diversity

Something else that all three executives have in common is that they are all women in top roles in fintech, an industry that isn’t known for its diversity.

6th Avenue’s Chang’s career includes working at a large institutional bank for six years. Out of 200 professionals, only four of them in her group were women. “At the end of the day, performance is the best differentiator. If you perform well, it presents unique opportunities. At 6th Avenue Capital, diversity is embraced. Our underlying merchants aren’t just one gender or color. Diversity helps us understand the needs of small businesses better, so we can provide fast and customized funding quickly,” she said.