Business Lending

Letter From The Editor

December 23, 2017 It was a year to remember, our sources declare

It was a year to remember, our sources declare

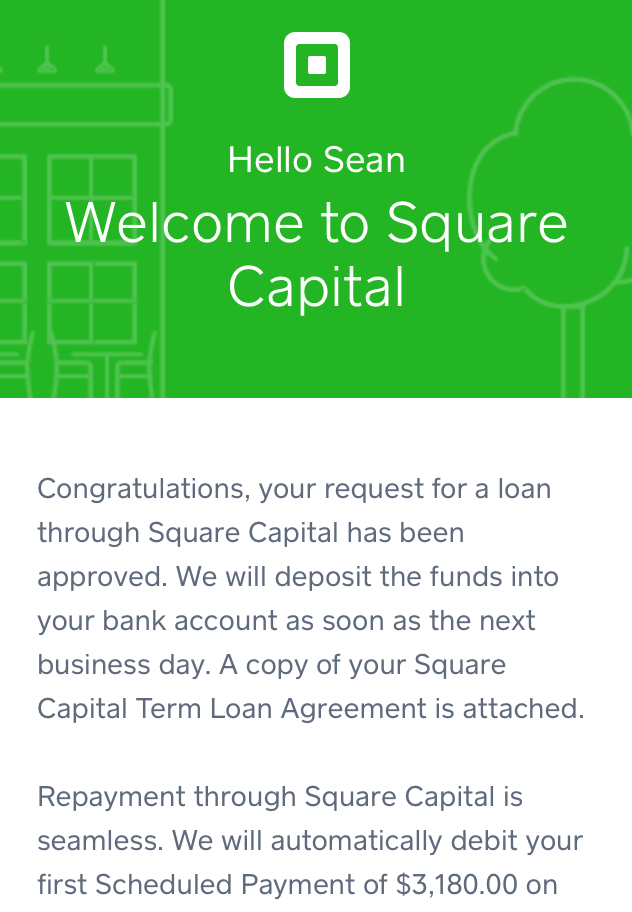

‘Twas the Jan/Feb issue I wrote about my loan from Square

Through March into April salespeople closed deals via text

Through March into April salespeople closed deals via text

As banks looked to fintech as their plan for what’s next

We went to Texas a nexus for finance and lending

We went to Texas a nexus for finance and lending

It was May, maybe June when Bizfi’s final days were pending

Merchants talked, banks adjusted, it was a summer of learnings

Merchants talked, banks adjusted, it was a summer of learnings

For the pressure was on to produce solid quarterly earnings

September, October, liens and judgements were removed

September, October, liens and judgements were removed

But the world hardly noticed and deals still got approved

Winter coats and furry hats meant the year would end soon

Winter coats and furry hats meant the year would end soon

But by golly 10k, no 19k! Bitcoin went straight to the moon!

And so boys and girls the story of ‘17 has been told

And so boys and girls the story of ‘17 has been told

What a time for finance, for money, and a world to behold

See you in ‘18, in ‘19, and the roaring twenties my friend

We’ll be right there, whether you deal in receivables or lend

– Sean Murray

MCA’s Top Social Media Voice

December 18, 2017 LinkedIn has unveiled its top 10 voices for marketing and social media. Fintech did not make the list, but perhaps the social networking site didn’t look hard enough. If they had been following Jennie Villano, who on Dec. 1 joined Kalamata Advisors as vice president of business relationships, that list might have included a nod to the MCA industry.

LinkedIn has unveiled its top 10 voices for marketing and social media. Fintech did not make the list, but perhaps the social networking site didn’t look hard enough. If they had been following Jennie Villano, who on Dec. 1 joined Kalamata Advisors as vice president of business relationships, that list might have included a nod to the MCA industry.

By most standards she’s a newbie to fintech, having joined her previous employer Pearl Capital only two years ago. But that hasn’t prevented her from making her social media presence known. And while she reserves Facebook for her personal life, if you know Villano then you wouldn’t be surprised at her success on LinkedIn, as she seems to have a knack for social media.

“I felt like I needed a very strong presence in this industry to get anywhere,” Villano told deBanked. “It’s funny, I think a lot of people associate sales with a type A personality and being pushy. I’m not an aggressive, pit-bull woman. You don’t have to be that type of woman to get ahead. I thought about how am I going to show this to the industry? Social media was my answer. My Facebook and LinkedIn attract a lot of views.”

Indeed, it was because of her Facebook profile that Villano was featured by a famous painting by David Uhl. The painting, dubbed Steampunk Seduction, is the first in Uhl’s Steampunk series. “I got that through Facebook,” Villano explained. “Someone saw my profile on Facebook, reached out and said, ‘you should contact the artist.’ I told them they were crazy. They insisted, and he chose me. It’s been a blessing.”

Meanwhile, her LinkedIn posts designed for MCA ISOs have similarly caught on like wildfire, and she only “amped up” her activity on the site in July. Villano has been posting on LinkedIn once per week, and the proof is in the pudding. “Since then, in September, October, and November, we broke funding records every month. It works,” said Villano of her previous employer Pearl Capital.

Underpinning that deal flow has been a flow of new relationships she’s forming, evidenced by more than 500 ISOs having contacted Villano on LinkedIn via her previous employer’s Salesforce network.

“That was from posting one time per month and just educating; not posting pictures of me on a beach sipping a Pina Colada,” said Villano. Instead, she was educating them about Pearl’s funding options, the types of deals they wanted, their bonus structure, etc. “So, it’s very basic information. I was just letting them know what they can expect from Pearl, what kind of fundings we were doing, just being a constant reminder,” she added.

While Villano is no longer employed by Pearl Capital, her posts from her tenure there have had a lasting impact. “[Last month] I put up a post announcing that I was leaving Pearl Capital,” Villano said. “The post generated more than 35,000 views.” Meanwhile, since she’s been posting, she’s seen the number of LinkedIn connections skyrocket.

Villano is continuing her social media push at her new employer, Kalamata Advisors.

“Kalamata has a partnership-culture mentality. It’s an amazing opportunity to be elected a partner, like a partner at Goldman Sachs or McKinsey, here after a couple of years. Then you have a real stake in the company and work at a firm where everyone wants to pitch in,” she explained. “Second is their great reputation. The partners put their mission and values first. They’ve grown so fast; but they’ve grown with the purpose to genuinely help people. And lastly, they’re very respected in the industry. Everyone here is very responsive, honest and professional.”

And while she’s no longer employed by Pearl Capital, she has nothing but respect for her former employer as well. The feeling is mutual, evidenced by a going away party that they threw for her on her way to Kalamata.

Gender Gap

So why isn’t social media more pervasive among MCA market participants? According to Villano, the reasons are two pronged, the first of which is compliance. “It’s very important to make sure we convey ourselves properly,” she said.

So why isn’t social media more pervasive among MCA market participants? According to Villano, the reasons are two pronged, the first of which is compliance. “It’s very important to make sure we convey ourselves properly,” she said.

The other has to do with the fact that MCA is a male-dominated industry. “Women are more conversationalists through texting or social media. I find women are more intimate with it on a professional level. I have to say that I have the most active social media in our industry,” said Villano, who again only joined fintech two years ago. She’s inspired by the many women who are behind the scenes at ISO shops, many of whom she explained work as processors.

We asked Villano about whether sharing her trade secrets with competitors in the industry made her uncomfortable. “Not at all. I’m not made like that,” she said. “And Kalamata believes trust is the importance of every brand. With transparency, there is trust. Everyone is authentic and unique. Everyone should have the opportunity to share his/her own self in any industry.”

Banks Set Sights on Small Business Loans Under $100,000

December 13, 2017BOSTON – One of the oldest lenders in the nation had a hand in developing technology intended to enable banks to win back the small business loan market from alternative lenders.

A tech incubator at Boston-based Eastern Bank, founded in 1818, has spun off Numerated Growth Technologies Inc., a startup that developed an online platform designed to identify and contact small businesses eligible for loans of up to $100,000.

Numerated Growth, which was founded in March, developed its tech in Eastern Labs and has generated about $100 million of volume since 2015. The model, which features real-time approval, is based on the tact banks first took with pre-approved credit cards in the 1990s, Numerated CEO Dan O’Malley told deBanked.

“We’re just taking the same rules and applying them here,” he said. “And by the way, that’s what customers want.”

Numerated Growth, which employs 26 workers, came out of stealth mode in May with a $9 million seed funding.

O’Malley, Eastern Bank’s former chief digital officer, said Numerated is now selling the platform to other banks but declined to disclose the specific number. The cost per bank depends on the number of loans being processed, he said.

The average business loan is $40,000 and they can be approved and funded within five minutes of the business completing the online agreement.

Numerated Growth’s real-time platform could be considered loan origination software on steroids. But such software essentially enables a bank to enter an applicant’s information into a digitized system to assist in the approval process. Alternative lending startups have been improving on that model for several years. Competitors in that space include nCino Inc., Decision Lender (Teledata Communications), PerfectLO and defi solutions, LoanCirrus.

But loan origination software is very crowded and startups are constantly launching to reduce the time it takes to approve a loan without increasing the number of defaults.

“Banks need to do things that are counter to each other,” David O’Connell, a senior analyst for the Boston-based Aite Group LLC, told deBanked. “There’s a need to do a fast money transaction, but doing it diligently without making any bad loans.”

“Banks need to do things that are counter to each other,” David O’Connell, a senior analyst for the Boston-based Aite Group LLC, told deBanked. “There’s a need to do a fast money transaction, but doing it diligently without making any bad loans.”

Combining the marketing and approval process is a credible approach because it keeps them on the same page in terms of targeting the most likely prospects. As a result, the number of “false positives” is lower, O’Connell said.

Instead of developing their own small business loan platforms, some banks are referring borderline borrowers to alternative lenders. But that can cause problems for the bank if the customer service doesn’t measure up to the bank’s standards and customers associate shoddy service with the entity that referred them, O’Connell said.

The best option is to develop in house. “Banks need to go as deep into the alternative lending market as they can with their own infrastructure and brand,” he said.

Because of its low value compared with other types of bank business, small business loan origination is one of the last remaining areas of banking to be targeted with innovation. “There’s not a huge price point,” said Kevin Tweddle, executive vice president for innovation and technology at the Independent Community Bankers of America.

Loan origination startups are trying to make such deals worth the bother. Yet the best tools tend to be developed by banking industry people because they understand the regulatory restrictions and integration factors, he said.

The goal of loan tech tools is two-pronged: make the approval process more efficient and make it convenient for borrowers. And so far, no software developer has risen above all the others to capture majority market share, Tweddle told deBanked.

“It’s just too early; there’s too many of them still coming out,” he said. “We’re in the early innings of a nine-inning game.”

Market metrics

Banks can’t afford to ignore the demand for alternative lending tools.

In May, the University of Chicago’s Polsky Center for Entrepreneurship and Innovation reported that the alternative finance market slowed but continued to grow during 2016 in the United States, Canada, Latin America and the Caribbean. The market’s value reached $35.2 billion — a 23 percent increase compared with 2015.

More than 200,000 businesses used online alternative funding sources during 2016. In the United States, marketplace and peer-to-peer consumer lending accounted for the largest share of market volume with $21 billion in the U.S. last year, a 17 percent increase. Balance sheet business lending was the second-largest model in the U.S. with $6 billion originated, the report found.

In Latin America and the Caribbean, marketplace and peer-to-peer business lending was the largest alternative finance segment with $188.5 million last year, a 239 percent rise versus 2015.

The same principles fueling the car-sharing business are being applied to peer-to-peer lending. As a result, adoption is growing as people view the credibility of peer lenders on an equal level of traditional experts, said David Wong, senior director of the innovation and acceleration lab at the Chicago-based CME Group Inc.

“Whether P2P markets reach or exceed the size of the incumbent market platforms (ala Uber and Airbnb), or not, they are driving rapid innovation and new dimensions of competition across industries,” he said.

Early adoption

Industry observers agree that small business loans haven’t seen enough innovation from the banking industry because of its size compared with commercial lending and real estate deals. As a result, it has a long way to go to shorten the time it takes for approvals and improving the customer experience, O’Connell said.

“Banks that fail to embrace automation for their commercial lending lines of business will lose the valuable relationships, loan outstandings, and fee-based income abundant in the commercial and industrial market,” he said.

After the 2009 global financial crisis, bank regulations tightened and data sets were required to be available and analytics-ready, providing another compelling need for commercial loan origination systems, O’Connell said.

After the 2009 global financial crisis, bank regulations tightened and data sets were required to be available and analytics-ready, providing another compelling need for commercial loan origination systems, O’Connell said.

No dominant players have emerged because neither traditional banks nor alternative lenders have figured out the best approach that satisfies both the lender and the customer, O’Connell said.

“Businesses don’t want money right away but they do want a quick and easy process,” he said. “My data tells me that in addition to providing underwhelming turnaround time, no particular lender has an edge over another. Nobody has it right.”

At Numerated Growth, O’Malley said the “initial wake-up call” signaling that a change was needed came in 2013 when Eastern Bank noticed solid small business customers paying off loans from alternative lenders such as On Deck Capital Inc. and LendingClub Corp. The pattern suggested that there was an unmet customer need.

Numerated Growth’s platform is designed to enable banks to proactively aggregate the data they need to identify prospective borrowers instead of requiring business owners to collect the data and present it to banks, O’Malley said.

“We’re making the banks do the work,” he said. “The same process that transformed the credit card industry will transform the financial products industry.”

deBanked Connect: Miami — SOLD OUT

December 12, 2017deBanked’s cocktail networking event on January 25th in South Beach is now SOLD OUT!

If you missed out on your chance to RSVP, you can still register for our much bigger, better, and more comprehensive event on May 14, 2018 in Brooklyn; Broker Fair 2018.

If you missed out on your chance to RSVP, you can still register for our much bigger, better, and more comprehensive event on May 14, 2018 in Brooklyn; Broker Fair 2018.

With 20 sponsors already signed on, Broker Fair is sizing up to be the biggest event in the MCA and small business lending industry of the entire year! During this exclusive full-day conference, brokers, lenders, funders and service providers alike can expect education, inspiration and opportunities to connect and grow their business. You can view our preliminary agenda here.

DON’T GET LEFT OUT. REGISTER FOR BROKER FAIR 2018 TODAY!. Got questions? E-mail: info@brokerfair.org

Closing Loans and MCAs — From the Bedroom to the Office

December 8, 2017 The merchant cash advance industry has gone mainstream so quickly that it has become more difficult to identify potential customers.

The merchant cash advance industry has gone mainstream so quickly that it has become more difficult to identify potential customers.

Market saturation and industry consolidation have caused the cost of sales leads to increase sharply. Yet a New York business loan broker is finding success by applying lead generation and online marketing strategies to merchant cash advance, or MCA, while expanding the number of services he offers prospects. Funding is just the foot in the door.

Philip Smith, founder and CEO of PJP Marketing Inc., told deBanked the MCA industry’s acceptance has made it more difficult for sales lead generators to produce profits. But expanding the number of services that independent sales organizations (ISOs) offer can offset the contraction. Smith’s life as a stay-at-home-dad, was recently featured in Innovate Long Island, a regional newspaper.

An ISO can’t just be a broker anymore. It needs to change, identify new revenue streams to excel. In doing so, a lead generator transforms itself into a business consultant that prospective customers turn to for additional services they often didn’t even know existed, Smith said.

For example, business loans and MCA is Smith’s largest business generator. But his most popular add-on services with such sales leads are credit repair and credit monitoring.

“The market is relatively easy,” Smith said. “The hard part is monetizing. The ISOs are going out of business because they refuse to monetize the other, non-cash advance leads.”

Smith, armed with a degree in business/e-business from the University of Phoenix, is also an advocate for entrepreneurs who want to work from home. It’s a viable model for lead generators because low overhead costs provide entrepreneurs an opportunity to capitalize on aggressive business strategies.

As such, Smith markets his pajama-centric business model with IWorkInMyJams.com. But he acknowledges that working from home presents its own challenges. Entrepreneurs need to be extra focused and tough to distract. No watching Dr. Phil during work hours.

Since they don’t work with more experienced managers, work-from-home entrepreneurs also need to seek their own sources of business advice and strategies. They deal with the reality that some lenders may deem them too small to do business. “Not everyone will work with you,” he said.

Working from home also requires a entrepreneur to set office hour limits and parameters to prevent burnout, Smith said.

“Do you know when to turn it off?” he asked. “That’s my problem. I’m up until 1 o’clock in the morning because I can.”

Smith now brokers sales leads in several verticals such as credit repair, tax relief, mortgage and solar energy. He claims revenue of $1.6 million last year and plans to reach $2 million this year.

When he was just 23, Smith launched his first company, We Link You Internet Services, a business that evolved into a web hosting concern.

He later worked for New York-based Canrock Ventures to launch a search-engine optimization platform called SEOPledge that was acquired in 2013. The following year, he founded what is now called PJP Marketing to broker leads amid the rapidly rising MCA space using the digital marketing skills he’d learned from the previous positions.

In October, deBanked reported that several factors have contributed to several changes in the MCA industry, including consolidation, making it more difficult for alternative-funding business lead generators.

ISOs and brokers have gotten pickier about the types of leads they’ll accept as MCA evolves from a niche business to one that’s more commonplace. Also, a stricter application of the Telephone Consumer Protection Act (TCPA) has chilled soliciting and hamstrung the ability to connect with business owners who are prospective clients.

Last year’s LendingClub Corp. scandal ousted several senior managers, including the company’s then-CEO. Last summer, Bizfi laid off workers and sold the servicing rights to its $250 million loan portfolio to rival Credibly.

The result has been a consolidation of the alternative funding business.

“There are still roughly 75,000 business owners every week who meet the criteria for an [MCA],” California-based Lenders Marketing partner Justin Benton told deBanked. “Now instead of there being 5,000 options in the space, there are 2,000, so those 2,000 are gobbling it all up.”

David Ross, a 12-year veteran of the MCA industry and owner of Pro Leads NYC, said MCAs higher profile has been a game changer for lead generators.

David Ross, a 12-year veteran of the MCA industry and owner of Pro Leads NYC, said MCAs higher profile has been a game changer for lead generators.

“MCA is beyond saturation,” he said. “All of the merchants know about it and understand it. Now, [funders] want exclusive leads.”

Working from home is a possible option for ISOs that are wizards at online marketing. But it’s less attractive for the conventional lead generator who relies on backing from a marketing team, Ross said.

“Realistically, if you’re a broker and want to make money you have to be on someone’s floor,” he said. “You need marketing.”

Last year, a Bryant Park Capital report estimated the MCA market to be worth about $12.8 billion. It’s projected to top $15 billion this year. Smith expects the continued strong demand for MCAs regardless of all the industry consolidation and costlier lead generation.

“I think they will always be fine because they can live through the storm,” he said. “It’s now a mainstream service so more people know about it.”

Smith told Donna Drake during an appearance on the Live It Up television program that going it alone as entrepreneur takes a “do-not-quit attitude” that has served him well so far.

“Any business is pretty much a numbers game,” he said. “I live and breathe it every single day.”

Originations Since Inception

December 8, 2017After several company announcements recently, we’ve compiled a milestone chart to plot where they rank. Originations may indicate business loans or MCAs funded on balance sheet, brokered, or placed through a marketplace. These rankings are a work in progress. This chart may not include companies for which public data is not available. If you’d like your figures to be listed here, e-mail sean@debanked.com.

| Company | Origination Volume Since Inception | Year Founded |

| OnDeck | $8 Billion | 2007 |

| Kabbage | $4 Billion | 2009 |

| Yellowstone Capital | $2 Billion | 2009 |

| BFS Capital | $1.7 Billion | 2002 |

| Funding Circle | $1 Billion (US only) | 2010 |

| IOU Financial | $500 Million | |

| Lending Club | $500 Million (SMB loans only) | 2006 |

| SmartBiz Loans | > $500 Million (SBA loans) | 2009 |

| Lendio | > $500 Milllion | |

| Forward Financing | $275 Million | 2012 |

| Blue Bridge Financial | $200 Million | 2009 |

Kabbage Crosses $4 Billion in Loans, Taps C-Suite Exec for Intl Expansion

December 6, 2017

Alternative lender Kabbage is exiting 2017 with a bang, having just crossed the $4 billion threshold for loans deployed across more than 130,000 small businesses so far. The latest milestone represents a 30% spike in both total funding and the number of merchants on its platform since April 2017, which is when they celebrated their previous new threshold. Victoria Treyger, chief revenue officer for Kabbage, took some time to talk with deBanked about the latest milestone, international expansion and mobile strategy.

“Our lines of credit and amounts taken continue to increase as we begin serving more and larger small businesses. We see great momentum across all industries in all 50 U.S. states,” Treyger said, adding that the momentum is particularly evident among the restaurant, construction, professional services and automotive industries for funding strategic investments such as new locations, specialty equipment, business expansion, etc. The $4 billion milestone is the result of the company’s direct business in America only.

According to recently released data by Kabbage cited in CrowdFund Insider, nearly three-quarters of 400 small business owners polled are forecasting higher revenues by year-end. More than 50% of those merchants are targeting a jump of at least 10%. Kabbage certainly appears to be benefiting from this optimism and an economy that is functioning on all cylinders. Treyger points to the lender’s “fully automated lending process and unique, live data connections with our customers.”

Fintechs & Banks

The relationship between alternative lenders and banks has been at the forefront, and Kabbage has been involved in some of the most high-profile pairings, evidenced by SoftBank’s famous investment. And while there’s no crystal ball, fintech and bank partnerships are one of the trends that will likely persist in 2018.

“Data will be at the heart of everything, how it’s shared, accessed, applied, protected and given back. Expect to hear more about the personalization of lending and to see stronger partnerships between fintechs and banks,” said Treyger. Consumer data, of course, is the Holy Grail for lenders, with banks having a tendency to keep that information close to the vest. And with the Equifax breach so recent in the rearview mirror, the importance of data security is certainly paramount.

“The CFPB recently published data-sharing guidelines between banks, their customers and financial services they choose to permission their data. Kabbage applauds the CFPB guidelines, small business owners should control how, where and with whom their data is shared to best serve their needs. Security is the primary concern, as it should when handling customers’ data. All entities, from fintechs to data aggregators should be held accountable to the same security standards as banks,” Treyger said.

She also pointed to a mobile push in yet another sign that the industry has turned a corner. “Anticipate greater adoption in mobile lending. Today, approximately 20% of Kabbage’s originations come from mobile. We’re the only provider that allows its customers to apply, qualify and draw funding from a mobile app; we have seen growth and expect to see more in 2018,” she said.

Kabbage’s Global Ambitions

Meanwhile, as Kabbage sets its sights on global expansion, they’ve tapped a C-Suite executive from the consumer goods industry who has held leadership roles across North America, Europe and Asia. Robert Sharpe was tapped for the newly created position of COO at Kabbage. Most recently, Sharpe served as president and COO at National DCP, LLC, a supply chain management company. He has also led CSM Bakery Solutions and Spain’s Campofrio Food Group, serving as chief executive at both companies.

According to the press release: “Sharpe will be responsible for Kabbage’s continued growth and operational oversight as the company expands internationally and scales its services to serve more and larger small businesses.”

As Kabbage readies its 2018 roadmap, notwithstanding its $200 million revolving credit facility with Credit Suisse in November, don’t be surprised to see them revisit the capital markets.

“Continuing to diversify our funding options for small business lending is certainly of interest,” noted Treyger.

Institutions Like American Express Are Mainstreaming Daily ACH Payments

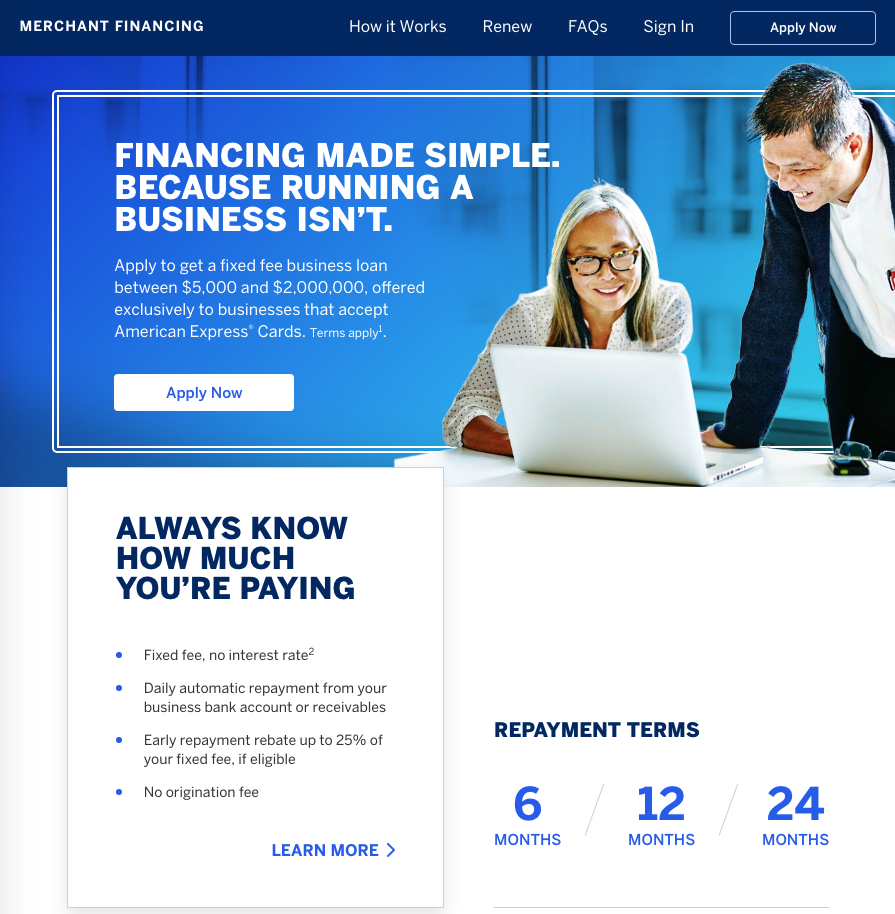

November 30, 2017A takeover-style ad on CNN’s website rang very familiar earlier today. The ad, paid for by American Express, preached merchant financing with a fixed fee.

The ad brought me to a page that offered a fixed fee business loan between $5,000 and $2 million with daily ACH repayment and no interest rate. Terms were 6 months, 12 months, or 24 months.

While this is more similar to an OnDeck loan, than say perhaps, a merchant cash advance, the concept of fixed fee business financing is becoming a standard even among institutional finance providers.

Square, as I experienced firsthand, is another company mainstreaming the fixed fee model. The difference there is that the payments are monthly rather than daily.

The good news for many online lenders and MCA companies of course, is that merchants that may not qualify with some major financial companies, are at least being introduced to the concept of fixed-fee short-term capital and even daily payments.