Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

deBanked CONNECT Miami Travel Advisory

January 20, 2019 |

|

Please allow yourself ample amount of time to get through airport security. There has been reports of extended security wait times following the partial government shutdown. Eden Roc has limited amount of parking spots. The hotel will accommodate as many as they can in their parking garage. We encourage you to use Uber, Lyft or cab when possible. Join Our Event Community to Connect With Other Attendees Now To maximize your experience, we invite you to join our event networking community. It’s available from your computer, tablet, iOS and Android devices. USE IT TO: It’s so easy! All you’ll need to do is enter the email address you’ve used during the registration and you’re in! |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

deBanked’s Most Popular Stories of 2018

December 22, 2018

Five of the top 10 most read stories of 2018 were related to the saga of 1st Global Capital; The bankruptcy, SEC charges, the revelation that they had made a $40 million merchant cash advance, and finally the devastating news of that deal falling apart. We decided to lump all of them together in our #1 slot, but first, the following story was the most independently read of 2018:

The Saga of 1st Global Capital

1. Largest MCA Deal in History Suffers Multiple Closures was picked up by ABC News in California, placing deBanked’s website on TV for the first time.

These were the other most read stories related to 1st Global Capital

- 1 Global Capital Files Chapter 11

- Syndication at Heart of SEC and Criminal Investigation into 1st Global Capital

- 1st Global Capital Charged With Fraud by SEC

- The Largest Merchant Cash Advance in History

Bloomberg Businessweek began publishing a series in November about the allegedly scandalous merchant cash advance industry. An initial review by deBanked uncovered questionable holes in their reporting, but when the series’ senior editor thanked a state senator for proposing legislation in response, suspicious ties were uncovered, followed by one Bloomberg reporter wiping his twitter account clean. Bloomberg’s exaggerated series dubbed #signhereloseeverything has spawned a highly popular counterseries that has challenged Bloomberg’s reporting. We call it #tweetherewipeeverything. The following stories were all in the year’s top 12 most read, but we’ve lumped them together here at #2.

The Bloomberg Blitz

2. Multimillionaire CEO Claims Predatory Lenders are Causing Him to Sell His Furniture for Food

The other two were:

Arrested for Data Theft

3. CAUGHT: Backdoored Deals Leads to Handcuffs was the year’s third most read story.

MCAs are Not Usurious

4. It’s Settled: Merchant Cash Advances Not Usurious came in at #4 this year, ending the debate that has persisted in hundreds of cases at the trial court level in New York State.

In October 2016, the plaintiffs sued defendant Pearl in the New York Supreme Court alleging that the Confession of Judgment filed against them should be vacated because the underlying agreement was criminally usurious. As support, plaintiffs argued that the interest rate of the transaction was 43%, far above New York State’s legal limit of 25%. The defendant denied it and moved to dismiss, wherein the judge concurred that the documentary evidence utterly refuted plaintiffs’ allegations. Plaintiffs appealed and lost, wherein The Appellate Division of The First Department published their unanimous decision that the underlying Purchase And Sale of Future Receivables agreement between the parties was not usurious.

Debt Settlement Company Sued

5. ISOs Alleged to Be Partners in Debt Settlement “Scam” in Explosive Lawsuit was #5 in 2018. The lawsuit ultimately settled and resulted in a big payout to the MCA companies.

A Broker’s Bio

6. The Broker: How Zach Ramirez Makes Deals Happen was #6. deBanked interviewed Zachary Ramirez to find out what makes a successful broker like him tick, how he does it, and what kinds of things he’s encountered along the way.

Ban COJs?

7. Senate Bill Introduced to Ban Confession of Judgments Nationwide was #7. Although this is related to the Bloomberg Blitz, the introduction of this bill fits more neatly into a category of its own.

Who’s Funding How Much?

8. A Preliminary Small Business Financing Leaderboard was #8. Despite this being published early in the year and offering detailed origination volumes for several companies all in one place, it wasn’t as well-read as all the drama that unfolded later in the year. Unsurprisingly, a chart of The Top 2018 Small Business Funders by Revenue ranked right behind this one, but we’ve lumped it in with #8 since it’s related.

Thoughts by Ron

9. Ron Suber: ‘This Industry Will Look Very Different One Year From Now’ was #9. Known as the Magic Johnson of fintech, the 1-year prediction by former Prosper Marketplace president Ron Suber, originally captured in the LendAcademy Podcast, resonated all throughout the fintech world. Will he be proven correct?

A Rags to Riches Tale

10. How A New Hampshire Teen Launched A Lending Company And Climbed Into The Inc. 500 was #10.

Josh Feinberg was not a complete newbie when he started in the lending business in 2009, but he also had a long way to go to find success. His dad had been in the business for 15 years and shortly after graduating high school, Josh started to work in equipment financing and leasing at Direct Capital in New Hampshire, his home state. He then had a brief stint working remotely for Balboa Capital, but he wasn’t sure that finance was for him.

He was 19, with a three year old daughter, and he took a low paying job working at a New Hampshire pawn shop owned by his brother and a guy named Will Murphy.

“I was making $267 a week at the pawn shop and I was having to ask friends to help me pay my rent for a room,” Feinberg said. “So at that point, I realized that something needed to change.”

Janene Machado Wins PCMA’s RISE Award

December 18, 2018Janene Machado, deBanked’s event planner, was honored by the Professional Convention Management Association (PCMA) last week with the RISE Award. The RISE Award is given to a new member who has made the most impact to the chapter. With more than 7,000 members and an audience of more than 50,000 individuals, the PCMA is the world’s largest network of Business Events Strategists.

Machado volunteers on the New York Area Chapter Marketing committee and manages their social media content.

We congratulate her on her achievement.

deBanked’s “Ice Edition”

December 14, 2018 deBanked’s final issue of 2018 is in the mail. We’re calling it the ice edition because of how the cover’s colors came out. For November/December we cover the new legislation in California, what’s happening in New Jersey, and what may be still to come. In addition we tackle the concept of open banking, delve into Small Business Development Centers, and reflect back on the biggest moments of 2018. There’s more of course, but you’ll have to get your hands on the ice to see for yourself.

deBanked’s final issue of 2018 is in the mail. We’re calling it the ice edition because of how the cover’s colors came out. For November/December we cover the new legislation in California, what’s happening in New Jersey, and what may be still to come. In addition we tackle the concept of open banking, delve into Small Business Development Centers, and reflect back on the biggest moments of 2018. There’s more of course, but you’ll have to get your hands on the ice to see for yourself.

If you’re not already subscribed, YOU CAN REGISTER TO GET ALL FUTURE ISSUES HERE FOR FREE.

And don’t forget, the deadline to become a sponsor of deBanked CONNECT – Miami is Wednesday, Dec 20th. Email events@debanked.com to get signed up.

How Dealstruck Arrived, “Disrupted,” and Died – A Cautionary Online Lending Tale

October 14, 2018Dealstruck just wanted to be loved.

When Dealstruck popped up on the online lending scene in 2013 with promises of long term loans and low interest rates, some industry insiders rolled their eyes at the naïveté. “It’s not about disintermediating the banks but the very high-yield lenders,” Ethan Senturia, chief executive of Dealstruck, told the New York Times in March 2014.

A self-described member of the “lucky sperm club,” a not-even 30-years-old Senturia went on to successfully raise $30 million of investor capital to fund his business, enough to fuel his rise and price-shame his competitors for years. But it wouldn’t last, as he detailed in book, Unwound, about the behind-the-scenes chaos that ravaged Dealstruck until the company closed for good in late 2016.

A self-described member of the “lucky sperm club,” a not-even 30-years-old Senturia went on to successfully raise $30 million of investor capital to fund his business, enough to fuel his rise and price-shame his competitors for years. But it wouldn’t last, as he detailed in book, Unwound, about the behind-the-scenes chaos that ravaged Dealstruck until the company closed for good in late 2016.

“We had taken to the time-honored Silicon Valley tradition of not making money,” Senturia recalls. “Fintech lenders had made a bad habit of covering out-of-pocket costs, waiving fees, and reducing prices to uphold the perception that borrowers loved owing money to us, but hated owing money to our predecessors.” The use of italics are his own.

During Dealstruck’s rise and fall, a journey that reads like an ever-frantic race to raise more money before collapsing, Senturia actually pauses to self-reflect if Dealstruck was becoming a Ponzi scheme. “When does a business go from legitimate but unsustainable to being a Ponzi?”, he pondered before rationalizing that he had not and would not cross that threshold.

At times, the company resigned itself to being a technology play for would-be-acquirers, one of whom included CAN Capital in 2014 when Dealstruck was only originating $3 million a month in loans. Senturia recalls, “For an unprofitable company that had raised $3.5m of equity and whose systems capabilities hadn’t evolved far beyond processing payments on term loans, it would have been tough to make a financial argument that we were worth much more than the capital we invested–$10m soaking wet. But CAN was doing different math. They were trying to go public.”

In Senturia’s view, CAN was trying to check the technology box on the way to an IPO. The offer was $33 million, $13 million in cash and $20 million in pre-IPO stock. Dealstruck first accepted the offer and then ultimately turned it down. CAN never had their IPO.

Dealstruck continued on, rapidly expanding while dealing with major defaults, one of which included an $800,000 loan, the largest deal they ever did at the time, that turned out to be completely fraudulent. One of their early investors never forgave the hiccup and by May 2016, when the online lending bubble was bursting, due in part to the Lending Club scandal, Dealstruck became a poster child for the overheated market.

Case in point, Senturia was mocked during an investor presentation as one individual stood up and asked who in the room would even invest $10,000 into Dealstruck let alone the millions they were seeking. Nobody raised their hand. It was a sign of the times.

At the end, Dealstruck’s dire situation had become entwined with a hedge fund that could not afford to let Dealstruck fail. Senturia referred to their predicament as “mutually assured destruction.” When Senturia warned the hedge fund manager that the game was finally over, it did not go well. “I am like, literally staring over the edge. My life is over,” the hedge fund manager tells him. Dealstruck died. The hedge fund survived.

What Senturia left in his wake were dozens of lost jobs, unpaid vendors, and a cautionary tale he feared nobody would even remember. His book makes sure that nobody will forget.

Though Dealstruck’s failed business could be summed up by bankers as an 180-page “I told you so,” Senturia, concedes throughout that he was learning major lessons along the way. After all, he was only in his twenties and all too self-aware that his family relationships, education (Wharton), and luck played a role in making Dealstruck possible in the first place. Besides, Senturia could easily be telling the tale of many other online lenders of that generation; Lose money, scale, raise capital, shame the competition for their high rates or slow speed, and hope that someone buys you up or you go public.

While it’s a quintessential Silicon Valley story, there are plenty of nuggets of wisdom Senturia sprinkles in along the way that would be valuable to any entrepreneur. It’s also a must-read for anyone interested in lending or fintech. If you were in the business during those years, you probably know some of the characters firsthand. You can buy the book on Amazon here.

deBanked CONNECT San Diego PHOTOS

October 9, 2018

The Largest Merchant Cash Advance in History

September 28, 2018 How would you like to be the funder to do a $40 million MCA transaction? According to the Securities & Exchange Commission, a deal of such magnitude was one of the many negligent acts that 1st Global Capital CEO Carl Ruderman did with investor money. Though the SEC refers to the merchant as an auto dealership in California, it’s roughly 9 dealerships with common ownership that collectively gross more than $550 million a year in sales. It’s the deal of a lifetime except that the ISO who brokered it has become the largest unsecured creditor to file a claim in the 1st Global bankruptcy. Records show they are owed approximately $3.9 million in unpaid commissions.

How would you like to be the funder to do a $40 million MCA transaction? According to the Securities & Exchange Commission, a deal of such magnitude was one of the many negligent acts that 1st Global Capital CEO Carl Ruderman did with investor money. Though the SEC refers to the merchant as an auto dealership in California, it’s roughly 9 dealerships with common ownership that collectively gross more than $550 million a year in sales. It’s the deal of a lifetime except that the ISO who brokered it has become the largest unsecured creditor to file a claim in the 1st Global bankruptcy. Records show they are owed approximately $3.9 million in unpaid commissions.

And its performance has not been without challenges, according to emails disclosed in the SEC case.

In April 2018, 1st Global employees discussed what to do about the dealerships’ lingering cash flow problems after becoming aware that the owner intended to either recapitalize the debt or sell the dealerships. The choice by then had come down to either continuing to fund them or to cut their losses, an email says.

“If they were to become insolvent, everyone loses,” wrote the Director of Accounting and Finance.

1st Global continued to fund them. The $40 million (approximate amount) was not disbursed all at once but in increments over the course of a year.

One week before 1st Global filed for bankruptcy, they signed a Binding Letter of Understanding with the dealerships acknowledging that the owner would be selling them. At that time the merchant had unpaid taxes of at least $9 million and had an outstanding receivable balance with 1st Global of $43 million. The Letter said that 1st Global would accept “whatever amount it receives [..] at this point as complete satisfaction” of the current RTR when the business is sold. 1st Global also agreed to forever release the dealerships’ owner personally from all legal claims. It was signed by Carl Ruderman 8 days before he resigned.

The merchant has not returned deBanked’s inquiries. The banker named in the Binding Letter as having been exclusively hired to sell the dealerships, told deBanked over the phone that he has never heard of 1st Global. 1st Global ceased operations on July 27th. The SEC filed a complaint against Ruderman and the company on August 23rd and an amended complaint on September 26th. The dealership transaction is used as an example of malfeasance in it twice.

New Record

No longer candidates for the largest merchant cash advance in history, two ancient deals that were famous during their eras for their size, ended up in default, and in doing so showed the industry that there was such a thing as too big.

One was a $4 million advance made by Strategic Funding Source in 2011 to a tourist attraction being produced at the Tropicana Hotel in Las Vegas. The Las Vegas Mob Experience, billed as the most technologically advanced interactive presentation of historical artifacts ever devised and set up in a 26,000 square foot total immersion facility, it was predicted to bring in 1.5 million visitors per year. But the deal quickly spiraled out of control, the exhibit shut down, and allegations of fraud were lodged in court. Though the Mob Experience was dubbed the largest merchant cash advance in history, it depends on whether or not you’re counting common ownership of multiple businesses as individual deals or one deal.

Dozens of advances made by Global Swift Funding in 2007 and 2008 to businesses controlled by the same west coast-based restaurateur, led to Global Swift’s demise. When the “restaurant king,” as he was known, filed for bankruptcy across all of his entities, Global Swift had outstanding future receivables with his businesses of approximately $8 million. Dan Chaon, a then representative of Global Swift, told a local newspaper at the time that the restaurateur was “a helluva sales-talk artist… he provided false financial statements, and everyone got caught up in that game.”

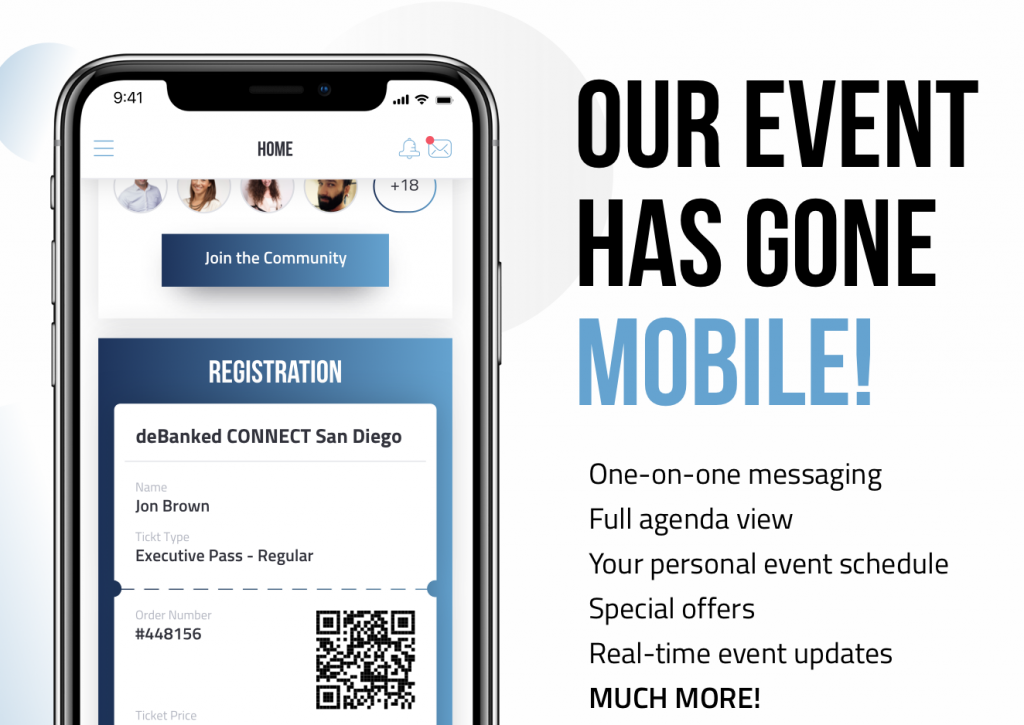

Get The deBanked Events Mobile App

September 24, 2018

deBanked affiliated events will now be accessible through our new mobile app! (iPhone | Android) Whether it’s deBanked CONNECT networking events or Broker Fair, you’ll be able to get all the information you need in one place.

deBanked affiliated events will now be accessible through our new mobile app! (iPhone | Android) Whether it’s deBanked CONNECT networking events or Broker Fair, you’ll be able to get all the information you need in one place.

See who’s attending!

While we don’t distribute attendee lists, you’ll be able to view all attendees that opt-in to our “Community” and even be able to direct message them. You can choose to get push notifications or email alerts when someone views your profile or sends you a message.

The app is only accessible to people registered for events beginning with deBanked CONNECT San Diego on October 4th. Use the email address tied to your registration to log in. No password is required. If you can’t remember what email address you used for your ticket, contact events@debanked.com for assistance.