Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

The Bad Merchant Database is Free, But Not the One You’re Thinking Of

October 1, 2015 Now you can find out if merchant cash advance and business loan applicants have engaged in suspicious activity with other funders for FREE.

Now you can find out if merchant cash advance and business loan applicants have engaged in suspicious activity with other funders for FREE.

For years, the only way to access such a database was through the Small Business Finance Association (SBFA but formerly known as NAMAA) and doing that hasn’t exactly been cheap or easy. As the SBFA describes itself as a not-for-profit trade association representing organizations in the United States and Canada, acceptance comes with adherence to certain trade association rules and fees often too high for smaller companies.

Just about every merchant cash advance company is aware of the SBFA’s shared database of bad actor merchants. It’s widely viewed as the biggest benefit to being an association member. It’s exclusive, almost too exclusive, many would say.

Enter DataMerch, the startup that’s disrupting it all by making the system open to funders… for FREE. Founded by merchant cash advance veterans, the company’s co-founders have replicated a product that the industry loved, but many could not afford or be accepted into.

deBanked has learned that DataMerch already has an active community of funding companies submitting suspicious merchant activity to the database.

Naturally, DataMerch’s tech-based platform made it a suitable fit to integrate the deBanked’s news feed into its member dashboard. The companies announced completion of the integration earlier this morning.

To sign up for DataMerch, contact support@datamerch.com

Coalition for Responsible Business Finance Submitted RFI on Behalf of Both Funders and Small Businesses

October 1, 2015 If you haven’t heard of the Coalition for Responsible Business Finance (not to be confused with the Responsible Business Lending Coalition), I recommend paying attention to it.

If you haven’t heard of the Coalition for Responsible Business Finance (not to be confused with the Responsible Business Lending Coalition), I recommend paying attention to it.

“The CRBF is a group of businesses and service providers that advocate for the value of alternative financing opportunities for small businesses,” they said in their response to the Treasury RFI. “We created the coalition to help educate Congress, Treasury, and other federal departments and agencies on how technology and innovation are providing small businesses access to capital that is necessary for growth.” Simply put, this coalition allows lenders, funders, and small businesses to have a unified voice to educate policymakers.

And yes, merchant cash advance companies are welcome, though representation is very diverse.

“Small business owners value choice and speed when looking at alternative finance and lending options,” the CRBF says in their response. “Any federal approach needs to balance new regulatory requirements with the impact on the alternative finance and lending sector and on the sector’s small business customers.”

The overall message in the submission is that regulators need not feel shy about opening a dialogue with those most likely to be affected by any change in policy.

For those reasons, CRBF recommends that Treasury create an alternative finance and lending interagency working group that will meet on a quarterly basis. We suggest that twice a year the working group meet as a group comprised solely of governmental personnel, with officials from SEC, SBA, FTC, Federal Reserve, OCC, and other relevant agencies. And, we suggest that twice a year the working group meet with business leaders from across the alternative finance and business lending spectrum including representatives from lead generators, aggregators, merchant cash advance professionals, peer-to-peer lenders, risk analytics services, direct lenders, marketplace lenders, and others. Meeting with different groups of businesses throughout the life span of an interagency working group will allow Treasury to keep up with a rapidly evolving business sector and will help ensure that any federal approach is sensitive to its impact on the sector and on its small business customers.

CRBF is committed to educate federal authorities on how alternative lending and finance benefits small business and the economy. We would certainly help Treasury establish any working group that serves the same purpose.

As I am currently an advisory board member of this coalition, I encourage you to consider the organization’s mission and purpose by visiting the website at http://www.responsiblefinance.com. If you’d like to learn more or consider support for it, email me at sean@debanked.com.

Why OnDeck and CAN Capital Nailed Their Treasury RFI Responses

October 1, 2015 A congressional staffer once told me that if you want your input to have any meaningful impact, you better bring hard statistics and numbers.

A congressional staffer once told me that if you want your input to have any meaningful impact, you better bring hard statistics and numbers.

Both CAN Capital and OnDeck accomplished that in their comprehensive responses to the Treasury RFI.

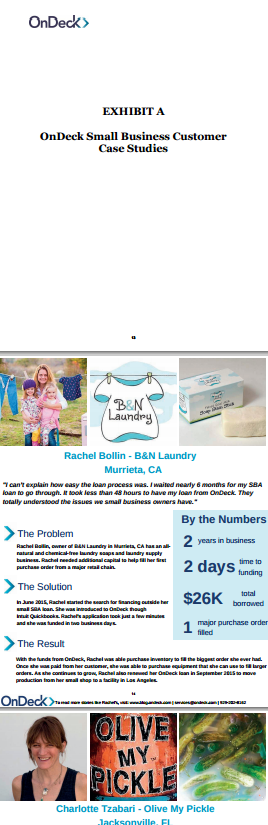

OnDeck went a step further and even attached case studies that included photographs of actual small business owners they’ve helped. They also put to bed the notion that their business model is unregulated:

At the federal level, we are regulated by the SEC and subject to US securities laws. We further satisfy applicable lending requirements under, among others, the Fair Credit Reporting Act, the Servicemembers Civil Relief Act, the Equal Credit Opportunity Act, and sanctions programs administered by the Office of Foreign Assets Control (OFAC).

They also clue us in to the size of the potential market they’re in. “It is estimated that there is $80-$120 billion in unmet demand for small business lines of credit,” they wrote.

Notably, they support the logic that a short term high APR loan can make more financial sense than a long term low APR loan. “With respect to loan cost, by matching a loan’s term with the estimated investment payback (or ROI) period, a small business can minimize total overall interest expense. For example, a loan used to purchase inventory can have a payback term that corresponds to the expected sale of the inventory — in this way, a borrower may pay less in total interest expense on a higher-rate, short-term loan than on a lower-rate, long-term loan (which may take weeks or months to procure).”

Meanwhile, CAN Capital explained just how time consuming the process can be for small business owners. “On average, a small business owner might spend over 30 hours applying for credit from a traditional lender and wait weeks or longer for the underwriting process to run its course and the funds to be disbursed, assuming the loan request is approve,” they wrote.

CAN’s response at time reads like an S-1 registration form (could there be a reason for that?). “Our approach to assessing the risk of small businesses and their ability to pay has been very effective, as manifested by our lifetime weighted average net write off rate of 7.2% over 17 years and more than $5.3 billion in funding transactions,” they say. “For returning customers that access capital through our platform more than once, we see an increase in their gross sales of approximately 7% on average between their first and last funding transaction.”

And if you don’t want your data sources to be questioned, the easy thing to do is cite governmental studies which both companies did often. “Traditional lenders are not serving the capital needs of small businesses. This is especially true when small businesses need $100,000 or less, which accounts for 90% of small business loans,” CAN wrote while citing a report published by the SBA’s Office of Advocacy.

deBanked Magazine Cover Teaser

September 30, 2015Can you guess who is on the cover of the September/October magazine issue of deBanked? Make sure you’re subscribed to the magazine to find out who it is!

SUBSCRIBE HERE

Sam Hodges on Fox Business

September 30, 2015Funding Circle’s Sam Hodges appeared on Fox Business on Monday, September 28th. One of the things he said is that loans under $1 million are still out of reach for most small businesses.

He also mentioned that his company has the lowest loss level of any digital small business lender anywhere in the world.

Details about Funding Circle disclosed:

- $1 billion lent to more than 10,000 businesses

- 40,000 investors globally

- $25,000 to $500,000 small business loans

Watch the full video below:

What The BFS Capital IPO Announcement Means for the Industry

September 29, 2015 Under the Jumpstart Our Business Startups (JOBS) Act, “an emerging growth company may confidentially submit to the Commission a draft registration statement for confidential, non-public review by the Commission staff prior to public filing.”

Under the Jumpstart Our Business Startups (JOBS) Act, “an emerging growth company may confidentially submit to the Commission a draft registration statement for confidential, non-public review by the Commission staff prior to public filing.”

According to the New Yorker, this process “allows companies that are thinking about going public to test the waters—they can gauge investor reaction, get feedback from the S.E.C. on their filings, and so on—before deciding if they want to go ahead with an I.P.O. If a company goes through that process publicly, and then decides to abandon the offering, its reputation gets damaged, even though it often makes sense for a company not to go public. Do it privately, and no one gets hurt.”

That’s what makes BFS Capital’s announcement (formerly Business Financial Services) that they had filed a confidential draft registration so bold. Companies normally choose this method if they don’t want anyone to know what they’re up to. But BFS is a different funder than the ones that came before them. OnDeck submitted their original draft registration confidentially for example and actually tried to keep it a secret.

“The initial public offering is expected to commence after the SEC completes its review process, subject to market and other conditions,” states BFS’s September 25th release.

The intent to go public follows a recent rebrand and the announcement that they had crossed $1 billion in funding since inception.

The most shocking part about a BFS IPO is that it’s not a CAN Capital IPO. While CAN is both older and larger, the industry has heard no word about a CAN Capital IPO since rumors leaked in Bloomberg almost an entire year ago. Back on November 20th, 2014, it was reported that the “New York-based company could be worth as much as $2 billion in the share sale.”

There was kind of a universal expectation that CAN Capital would go public immediately after OnDeck and Lending Club. Some insiders have pointed to OnDeck’s disappointing reception and performance as the reason CAN has delayed moving forward. OnDeck is currently trading at less than 50% of its IPO price and is facing a lawsuit from its own shareholders over it.

Others have said that CAN Capital isn’t waiting for anything because the company doesn’t actually need to go public. Long reported to be profitable and self-sustaining, opening themselves up to the volatility and fickleness of the public markets may not be worth the additional capital.

And still more have pondered if CAN Capital has what it takes to excite investors. Unlike some of the brand new tech startups that dominate the headlines, CAN has been operating since 1998, a time when only 42.1% of American households had computers and only 26.2% had Internet access. Of course the company has evolved and these days is as tech-equipped as their young brethren but a 17-year old lender may not be as easy to sell in a market obsessed with companies such as Uber, Snapchat and Airbnb.

BFS Capital was founded 13 years ago in 2002 so they’re not exactly new either. And their CEO, Marc Glazer, has led the company since its beginning.

BFS has been expanding however both here in the U.S. and abroad. In the U.K., they operate under the name Boost Capital. Meanwhile, independent financial brokerage firms such as Entrust Merchant Solutions are being acquired and rolled up into their organization.

What makes BFS different from OnDeck and Lending Club is that BFS also does merchant cash advances, not just loans. The only other publicly traded company that is significantly involved in merchant cash advances is Enova International and that’s only due to their recent acquisition of The Business Backer. The investor uncertainty surrounding lenders and marketplace platforms might not carry over to a company that got its start by purchasing future credit card processing receivables 13 years ago.

It would be safe to say that there’s a whole group of industry insiders who feel that Lending Club is a poor representative sample of the tech-enabled business financing space and that OnDeck’s unique model prejudices investors into thinking all lenders are like them. A BFS Capital IPO could in effect set the record straight for the industry and revive the IPO plans of their peers and competitors.

It might actually take a BFS IPO for us to finally see a CAN IPO, not that there aren’t plenty of other quality candidates right behind them.

What would a BFS Capital IPO mean for the industry? Perhaps a chance at redemption. There’s a lot of great things happening in this industry and investors ought to know about them.

OMG: Same Day ACH

September 25, 2015 Coming soon, the ability to ACH funds same-day will finally exist. The change will be a boon to tech-based lenders that have become famous (or infamous) for their ability to approve and issue loans quickly. No matter how fast the systems have become however, the ACH network has continued to slow the process down.

Coming soon, the ability to ACH funds same-day will finally exist. The change will be a boon to tech-based lenders that have become famous (or infamous) for their ability to approve and issue loans quickly. No matter how fast the systems have become however, the ACH network has continued to slow the process down.

Next-day funding has long made borrowers skeptical about the online lenders they apply to and many applicants become anxious when they hear that the funds will be in their account tomorrow rather than today, after the deal has been closed.

Speaking from my own experience, there was almost nothing worse than telling a merchant that the funds had gone out and would be in their account the next day because they would disregard the last part of that statement and check their bank accounts immediately and of course would not see those funds. They’d immediately reach back out to me or the underwriter and say that they had been deceived because no money was there. This scenario played out on at least half of all the deals I ever worked on and it was awful.

And I’d remind them, “It’s an ACH. It’s overnight. It should be there in the morning depending on your bank. If for whatever reason it isn’t, give me a call.”

Even after repeating myself, I’d often get an email later that day at 6 pm (bank closing time) to say that they were at the bank and the teller has just told them that they don’t see any incoming wires.

So many merchants just could not believe that a tech-based funding company could not make the money appear instantly in their account and every passing second caused them more anxiety and fear that they had been tricked.

Enter Same Day ACH, which is slated to launch in September 2016. According to the National Automated Clearing House Association (NACHA), who governs the ACH network, there will be two settlement times.

A morning submission deadline at 10:30 AM ET, with settlement occurring at 1:00 PM.

An afternoon submission deadline at 3:00 PM ET, with settlement occurring at 5:00 PM.

Virtually all types of ACH payments, including both credits and debits, would be eligible for same-day processing, according to their announcement.

The industry can’t get Same Day ACH fast enough!

And if you thought you were excited about ACHing, just watch the below video produced by NACHA about how awesome their network is.

Qwave Fails to Acquire IOU Financial, But Becomes Major Shareholder

September 24, 2015 After some tense fanfare, Qwave Capital failed to acquire a controlling stake in IOU Financial but has succeeded in becoming a major shareholder. In a published statement, Qwave manager Serguei Kouzmine said, “As a significant shareholder in IOU, I plan to work constructively with the Board of Directors to ensure the company is focused on growing profitably and creating value for all IOU shareholders over the long term. I appreciate the support my offer has received and look forward to helping IOU realize its potential.”

After some tense fanfare, Qwave Capital failed to acquire a controlling stake in IOU Financial but has succeeded in becoming a major shareholder. In a published statement, Qwave manager Serguei Kouzmine said, “As a significant shareholder in IOU, I plan to work constructively with the Board of Directors to ensure the company is focused on growing profitably and creating value for all IOU shareholders over the long term. I appreciate the support my offer has received and look forward to helping IOU realize its potential.”

Nearly 15% of the company’s issued and outstanding shares were acquired under the offer.

Qwave stands to materially benefit in the long run especially since the timing coincides with IOU Financial hitting historic milestones.

“The Company’s loan originations for the months of July and August, totaled US$31.3 million, representing a year over year increase of 150% in comparison to the same period in 2014,” IOU announced.

They also funded more than $100 million in 2014 and if that volume is a metric that anyone is measuring then IOU is substantially undervalued.

If the takeover attempt accomplished anything, it may have stirred IOU from a slumber at just the right moment in alternative lending history. They’ll be a lender worth keeping an eye on.