Archive for 2018

Lawyers Weigh in on Champion Auto Sales, LLC v. Pearl Beta Funding, LLC

March 22, 2018In light of the recent Champion Auto Sales, LLC et al. v Pearl Beta Funding, LLC decision, which decided that the particular MCA contract at issue “was not a usurious transaction,” deBanked spoke to a handful of lawyers, including the plaintiff’s lawyer, Amos Weinberg, to get their thoughts on the decision.

“The contract at issue in Champion Auto v. Pearl Beta Funding was really no different than the contracts reviewed over a hundred years ago by the United States Supreme Court, in Home Bond Co. v. McChesney, 239 U.S. 568 [1916], where our nation’s highest court agreed that “the transactions were really loans, with the accounts receivable transferred as collateral security,” and “[i]n so far as the contracts in question here use words fit for a contract of purchase they are mere shams and devices to cover loans of money at usurious rates of interest.” Like most patrons of funding providers, Champion Auto was a one-person company that needed immediate, overnight cash. Presiding Justice Rolando T. Acosta of the Appellate Division remarked, at the argument, that Champion was a “sophisticated” party that “knew what they were getting into.” It is therefore painfully obvious that even though the NYS Legislature criminalized and voided loans to corporations exceeding 25% interest, and even though all victims of loan sharking knew what they were getting into, the courts are loathe to be used as escape hatches for companies trying to get out of paying back loans.”

Giuliano, McDonnell & Perrone, LLP

“It’s an appellate ruling a lot of people have been waiting for. It handles the usury issue in passing, almost as if it goes without saying.”

Hudson Cook, LLP

“The court confirmed that under New York law, a properly structured MCA transaction is not a loan. But I want folks to focus on the ‘properly structured’ piece of that…The court’s decision did not indicate much. But it did say that based on the documentary evidence, which is the contract, that the transaction was not a loan. So it’s important for folks to understand that for [an MCA contract] not to be a loan, it needs to be properly described…this case really shows us how important the contract is.

This case does not mean that all MCA companies are all in the clear. What it means is that MCA companies with properly drafted contracts, and good practices and procedures, are not making loans.”

Harris Beach, PLLC

“First of all, it was a unanimous decision by the three justices in the first department. That doesn’t always happen, so that’s a good thing. I personally would have liked to have seen more discussion out of the appellate department, but the language that’s there happens to be great for the industry. The one thing that I would caution, though, is not to interpret that all merchant cash advances are outside of transactions that would be subject to usury because it really is dependent on the language of the agreement.

[The decision] is a great tool in the arsenal, but I don’t see it as the tool that is going to prevent challenges.”

Hudson Cook, LLP

“This is a very important decision because New York State has a high volume of merchant cash advance companies…so having favorable case law in New York is great for the industry.”

Mavrides, Moyal, Packman, Sadkin

“I am very pleased with the outcome. There are more cases [to be decided], but this is very beneficial. It’s a win for the industry and I hope to see other decisions go in the favor of the advance industry.”

Platzer, Swergold, Levine, Goldberg, Katz & Jaslow, LLP

“The impact of the Champion decision was direct. We represent several MCA clients and we have a number of cases where Amos Weinberg is representing the merchant. And in one of our cases where a motion to open up a default judgment is at issue, the judge’s law clerk directly emailed us and wants to conference the case based on the Champion Auto Sales decision.”

[Lafont also pointed out that even though it was a short decision, one of its two citations was to Feld v Apple Bank for Sav., which deals with overdraft protection and has interesting parallels to MCA.]

Platzer, Swergold, Levine, Goldberg, Katz & Jaslow, LLP

“Based on the email we just received from the court clerk today, this decision could expedite [future] litigation, and it could decrease certain attorney’s fees for a lot of MCA companies involved in this litigation.”

How One CEO Unified Two Companies with Different Cultures on Different Coasts

March 21, 2018 Company mergers, like marriages, have their pros and cons. Some are more successful than others and many say it’s unwise to rush into one. This is certainly the approach Adam Stettner adopted when he, as CEO of San Diego, CA-based Reliant Funding, oversaw the merger of his company with Merchants Capital Access, based in Melville, NY on Long Island.

Company mergers, like marriages, have their pros and cons. Some are more successful than others and many say it’s unwise to rush into one. This is certainly the approach Adam Stettner adopted when he, as CEO of San Diego, CA-based Reliant Funding, oversaw the merger of his company with Merchants Capital Access, based in Melville, NY on Long Island.

At the time of the merger in April 2015, Merchants Capital Access was an MCA funder. According to Stettner, they were what he considered a “back end” as they didn’t do marketing or sales. They did underwriting and funding, but they did not originate any new business.

Reliant Funding, which Stettner led, did almost the inverse. While it did some cursory underwriting, it mostly marketed and sold funding to small businesses. It would also package small business merchants and place them for appropriate funding. But they did not fund directly. So, it seems, these two companies made for a perfect marriage. They completed each other. But not so fast.

Even though Stettner had considerable experience working as a direct lender in the student loan business prior to taking the helm at Reliant Funding in 2008, he didn’t feel ready to dive into funding a different type of client. (Stettner said he originated and held on his balance sheet $15 billion in student loans at National Lending Associates, a San Diego company he co-founded.)

“I felt like it was easy for somebody to come into the [merchant advance] space and start writing checks and funding businesses,” Stettner said. “It’s hard to figure out how to get that money back. So instead of jumping in with both feet, I thought it would be wise to really understand our target demographic, our end user, the small business owner.”

So while the technical merger of Reliant Funding and Merchants Capital Access happened in April 2015, the newly enlarged entity operated as two distinct brands until September 2017.

During this period, Stettner said, “we were studying everybody’s credit models and the best way to approach American small business owners, the best way to fund them, the best way to service them, and ultimately, the best way to renew them.”

This roughly two year period between the time of the actual merger and the official fusion of the two companies, now simply called Reliant Funding, was not just for Stettner to learn about funding small businesses. A lot more needed to happen to sync together a southern California company and a New York City-area company, each with different corporate cultures, attitudes and ways of getting work done.

“Getting 150 people with different views on work, culture, approach and strategy wasn’t easy,” Stettner said. “But it was definitely worthwhile and it was a lot of fun. There were times, of course, when it was frustrating as well.”

The stereotype of southern California being more laid back doesn’t hold up, according to Stettner, who grew up in New York and has worked in southern California for 14 years.

“While the environment may be laid back in appearance, the effort that’s put forth and the intensity that exists in the southern California office is no less than what you see out from our New York office,” Stettner said. “Both work incredibly hard and have great attitudes.”

However, he did say that the original culture in the New York office (formerly the Merchants Capital Access office) was much more centered around management decisions and Stettner made a point of bringing a culture of empowerment to that office.

What does that look like exactly?

“We talk [with employees] not only about the top line numbers, but also the bottom line numbers with the idea of empowering everyone,” Stettner said. “It’s important to me that everybody knows the why behind what we do. If people understand why we do something, it’s easier for them to get behind it, and they’re better equipped to offer an opinion that can help get us there faster.”

Now as Reliant Funding, Stettner said that the company is fully integrated under the one brand with unified systems and technology. The company is a funder with a sales team focused on direct origination. It also continues to grow what Stettner calls the wholesale channel or broker channel.

Debt Relief Scammers’ Assets To Be Auctioned Off

March 20, 2018 A crew of debt relief scammers that carried out an $80 million fraud are having some of their assets auctioned off in Pompano Beach, FL this week. Among them a Tesla, BMW i8, Range Rover and custom luxury buses.

A crew of debt relief scammers that carried out an $80 million fraud are having some of their assets auctioned off in Pompano Beach, FL this week. Among them a Tesla, BMW i8, Range Rover and custom luxury buses.

According to the FTC and the State of Florida in a lawsuit they filed against Jeremy Lee Marcus, Craig Davis Smith and Yisbet Segrea, the defendants “got people to pay hundreds or thousands of dollars a month by falsely promising they would pay, settle, or obtain dismissals of consumers’ debts and improve their credit. Over time, victims found their debts unpaid, their accounts in default, and their credit scores severely damaged – some were sued by their creditors, and some were forced into bankruptcy.”

A court ordered an injunction against the defendants last year.

In an even uglier twist to the scheme, “the defendants also called people who were already enrolled with debt relief providers claiming they were taking over the servicing of those accounts and falsely claiming they would provide the same or similar services. The defendants told these consumers to transfer their escrow money to defendants, and then debited up to $1,000 each month from the consumers’ bank accounts.”

All of the named entities subject to the court-appointed Receiver’s control can be found here.

How A New Hampshire Teen Launched A Lending Company And Climbed Into The Inc. 500

March 17, 2018Josh Feinberg was not a complete newbie when he started in the lending business in 2009, but he also had a long way to go to find success. His dad had been in the business for 15 years and shortly after graduating high school, Josh started to work in equipment financing and leasing at Direct Capital in New Hampshire, his home state. He then had a brief stint working remotely for Balboa Capital, but he wasn’t sure that finance was for him.

He was 19, with a three year old daughter, and he took a low paying job working at a New Hampshire pawn shop owned by his brother and a guy named Will Murphy.

“I was making $267 a week at the pawn shop and I was having to ask friends to help me pay my rent for a room,” Feinberg said. “So at that point, I realized that something needed to change.”

One day, while working at the pawn shop, Feinberg saw a Facebook post from a restaurant owner in search of financing for equipment. With a background in financing, he said to himself: “I wonder if I could take an application and bring it to one of the sources I know and they could pay me a commission?’”

That question prompted Feinberg to present to his brother and Murphy the idea to start a finance company. Feinberg said he drew up a business plan in a day and a half and his brother and Murphy agreed to give him $3,000 to start the company. That was November of 2012.

“They gave me a spot down in the basement of their shop, which was anywhere from 47 to 52 degrees,” Feinberg said. “I had my jacket, my computer and I was making 400 calls a day.”

After three months of not funding any deals, Feinberg said he almost gave up. He was also focused mainly on the equipment finance market because that’s all he really knew.

“Then come to find out that I talked to somebody that had a need for working capital and I realized that I could find sources [for] capital,” Feinberg said.

So he worked with a few different sources to find capital for this client. The deal went through in 24 hours and it paid about $7,000 in commission.

“I didn’t have any money and I was like, ‘this is awesome,’” Feinberg said. “So I [kept] making 400 calls a day, knowing that this could potentially change my life.”

And it did. After a year, Feinberg’s company, Everlasting Capital, made $110,000 in commissions and $3.5 million in volume. Within that first year, he also hired three people and moved from the basement of the pawn shop in Rochester, NH to a 600 square foot office in the same town. (The current office is also in Rochester, but in a larger space.)

This lightning fast trajectory is by no means common. That’s why Everlasting Capital made it onto 2017’s Inc. 500 list, the iconic list of America’s fastest growing private companies. By year two, Everlasting Capital earned $640,000 in commissions, generating $14 million in volume, and by year three it earned $1.6 million in commissions with $18 million in volume. Ultimately, over a three year period ending in 2016, Everlasting Capital experienced 1,361 percent growth, placing them at No. 323 on the Inc. 500 list.

How did they do it? Feinberg said that creating a company and an office environment that employees enjoy is really critical, as is recognizing employees for their hard work.

“As long as we hit our goals which we have every year,” Feinberg said, “we take our company on a trip at the end of each year.” (Trips have included Las Vegas and Puerto Rico.)

More specifically, Feinberg said that the company’s success had a lot to do with building relationships with senior level people at top funding companies like Pearl Capital and BFS Capital. These relationships gave them higher [approved] volume, better buy rates and the ability to pay out good commissions to ISOs.

“This opened up a whole new aspect of our company,” Feinberg said. “Now, in addition to working with direct clients, we had an ISO division as well.”

But Feinberg said he wanted to create a reputable company to ensure that ISOs could feel comfortable working with them, knowing that Everlasting Capital was not backdooring their deals. So they created a portal for ISOs, called EverHub, which allows them to track their deals at every step along the way.

“We had to think outside the box to come up with a platform that was completely transparent and made it viable to work with another broker to get deals done,” Feinberg said.

There have definitely been hurdles along the way – most notably, employee retention.

“We hired and fired about 20 people in the second year,” Feinberg said. “We wanted to see if quantity would increase sales. Come to find out, it’s more quality than quantity.”

Partnership has been another challenge. The leadership team at Everlasting Capital is now Feinberg and Murphy. Feinberg’s brother, who was Murphy’s initial partner at the pawn shop (which has since been sold), is no longer involved in it.

Feinberg said that what makes for a good partnership is communication, early and often. And being able to hold partners accountable for different responsibilities.

“Partnerships are tough in business – they tend to get a little hairy, a little crazy at times,” Murphy said.

“Like myself and Josh, we have some different views on a lot of different things, but we take our different views and we meld them together to provide the best outcome for our employees and all the people we work with. Some may see that as a downside, but it’s actually a real strength.”

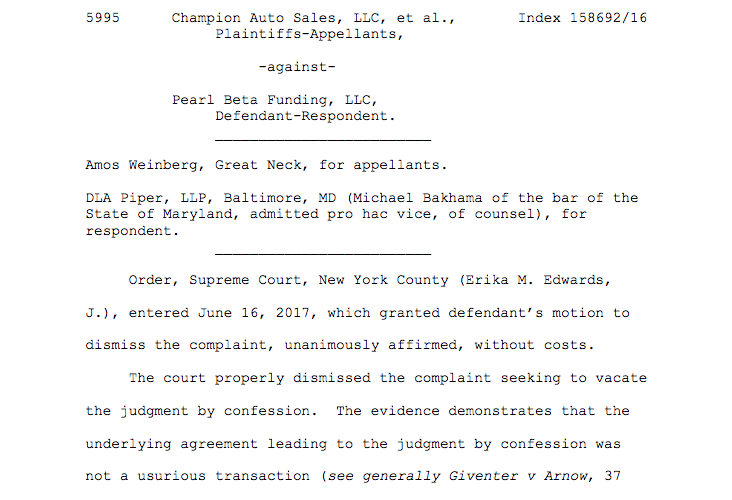

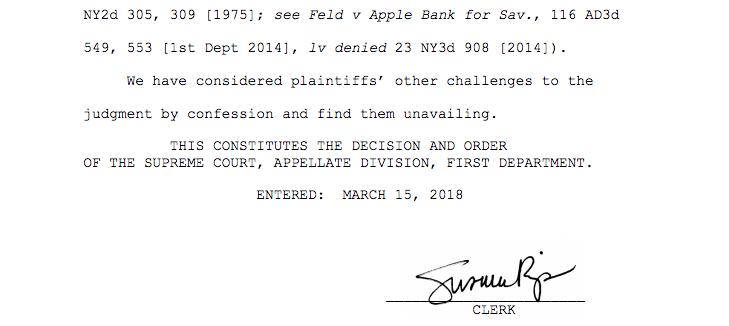

It’s Settled, Merchant Cash Advance Not Usurious

March 15, 2018 It’s not a usurious transaction. That’s how trial courts across New York State have been ruling on merchant cash advances for years, but now, thanks to Champion Auto Sales, LLC et al. v Pearl Beta Funding, LLC, the matter has been settled in a key jurisdiction.

It’s not a usurious transaction. That’s how trial courts across New York State have been ruling on merchant cash advances for years, but now, thanks to Champion Auto Sales, LLC et al. v Pearl Beta Funding, LLC, the matter has been settled in a key jurisdiction.

On Thursday, March 15th, The Appellate Division of The First Department published their unanimous decision that the underlying Purchase And Sale of Future Receivables agreement between the parties was not usurious.

In October 2016, the plaintiffs sued defendant Pearl in the New York Supreme Court alleging that the Confession of Judgment filed against them should be vacated because the underlying agreement was criminally usurious. As support, plaintiffs argued that the interest rate of the transaction was 43%, far above New York State’s legal limit of 25%.

The defendant denied it and moved to dismiss, wherein the judge concurred that the documentary evidence utterly refuted plaintiffs’ allegations.

With the case over, plaintiffs appealed the decision. Their major loss is spelled out below:

The decision is an interesting chapter in the story of Amos Weinberg, the attorney who represented the plaintiffs in this case. Prior to the appeal, he managed to file more than 100 lawsuits against merchant cash advance companies for usury. He has had very little success on the merits. Last May, deBanked reported that a judge in another lawsuit had admonished Weinberg for misleading the court over the actual wording of what a contract said.

Now he’s responsible for one of the biggest legal decisions in merchant cash advance history. And not in his favor.

The matter arose out of Index # 158692/2016 in the New York Supreme Court.

Merchant Advance Capital Closes $30 Million Debt Facility

March 15, 2018 Canadian Merchant Advance Capital closed a $30 million debt facility from Comvest Credit Partners today.

Canadian Merchant Advance Capital closed a $30 million debt facility from Comvest Credit Partners today.

“This is giving us significant runway,” Merchant Advance Capital CEO David Gens told deBanked. “For the next 12 months in particular, we’ve got great visibility as far as where our incremental capital is going to come from. This will allow us to focus less on fundraising and more on just building the business.”

Founded in 2010, Merchant Advance Capital offers several small business financing products including fixed term loans and business lines of credit. It also provides something called “The Good Cents Loan,” which Gens said he would like see more applicants for.

These loans are designed for businesses “that will positively impact the community or environment around them,” according to the company website. They require a more thorough application and the entrepreneur needs to convey to Merchant Advance Capital how the funds will help further their more socially or environmentally responsible cause. The company has only made a few of these loans which Gens said do not make money because the rates are so low.

This is the largest facility Merchant Advance Capital has gotten to date. However, Gens said that the business is primarily equity funded so that even as the business uses this new debt facility, it will still have more equity than debt.

Merchant Advance Capital generates most of its business through ISOs and partners and has two offices, one in Vancouver and the other in Toronto. Of about 50 employees, two-thirds work at the company headquarters in Vancouver.

Lendio Opens Franchise in Charlotte, NC

March 15, 2018

Today, Lendio announced the opening of its latest franchise in Charlotte, NC. Through the Lendio franchise program, Chris Cronk will help local businesses in the community apply for loans, review their options and secure funding.

The company has a network of over 75 lenders and its funding options include SBA loans, startup loans, equipment loans, commercial real estate loans and more. In the last fiscal year alone, Lendio facilitated more than $300 million in funding, according to the company.

“I’ve worked with numerous companies and witnessed their struggles to find capital,” said Cronk, who was a former investment banker for Bank of America Merrill Lynch where he advised and facilitated financing for companies of all sizes. “Charlotte is a fast-growing market and community. I’m excited to be a part of that growth by helping businesses in every industry find funding.”

Mad Over Madden

March 15, 2018 In a dispute that reflects the nation’s rigid political polarization, a piece of legislation pending before Congress either corrects a judicial error or condones “predatory lending.” It depends upon whom one asks. Either way, the proposed law could affect the alternative small-business funding industry indirectly in the short run and directly in the long term by addressing the interest rates non-banks charge when they take over bank loans.

In a dispute that reflects the nation’s rigid political polarization, a piece of legislation pending before Congress either corrects a judicial error or condones “predatory lending.” It depends upon whom one asks. Either way, the proposed law could affect the alternative small-business funding industry indirectly in the short run and directly in the long term by addressing the interest rates non-banks charge when they take over bank loans.

The easiest way to understand the controversy may be to trace it back to a ruling in 2015 by the United States Court of Appeals for the Second Circuit in New York. The case of Madden v. Midland Funding LLC started as claim by a consumer who was challenging the collection of a debt by a debt buyer, says Catherine Brennan, a partner in the law firm Hudson Cook LLP.

“Debt buyers like Midland are sued on a regular basis,” Brennan notes. “That’s a common occurrence.” What’s uncommon is that the appellate court affirmed the idea that the loan debt that Midland sought to collect from Madden became usurious when Midland bought it. The court ruled that because Midland wasn’t a bank it was not entitled to charge the interest the bank was allowed to charge, she maintains.

Under the ruling, non-banks that buy loans can’t necessarily continue to collect the interest rates banks charged because non-banks are generally subject to the limits of the borrower’s state, according to the Republican Policy Committee, an advisory group established by members of the House of Representatives in 1949. Banks can charge the highest rate allowed in the state where they are chartered, which could be much higher than allowed in the borrower’s state.

“So it undermines the concept that you determine the validity of a loan at the time the loan is made,” Brennan says of the decision in the Madden case. The “valid-when-made” doctrine – a long-established principle of usury law – states that if a loan is not usurious when made it does not become usurious when taken over by a third party, published reports say. In 2016, the U.S. Supreme Court declined to hear the Madden case, which in effect upheld the appellate court ruling.

In response, both houses of Congress are considering bills that would ensure that the interest rate on a loan originated by a bank remains valid if the loan is sold, assigned or transferred to a non-bank third party, the Republican Policy Committee says.

On Feb. 14, 2018, the House passed its version of the proposal, H.R. 3299, the Protecting Consumers’ Access to Credit Act of 2017, or the “Madden fix,” as it’s known colloquially. The vote was 245 to 171, mostly along party lines with 16 Democrats joining 229 Republicans to vote in favor. The Senate version, S. 1642, had not reached a vote by press time.

“It’s not a revolutionary concept,” Brennan says of the proposed law. “It had been understood prior to Madden that you determine usury at the time the loan is originated, and that should be restored.”

As the alternative small-business funding industry continues to mature it could benefit from the legislation, Brennan predicts. In the future, alt funders may begin to buy or sell more debt, which would make it subject to the state caps if the legislation fails to pass, she says.

The proposed law would also benefit partnerships in which banks refer prospective borrowers to alternative funders because it would eliminate uncertainty and would thus improve the stability of the asset, Brennan continues. “I would think anyone in the commercial lending space would want to see the Madden bill pass,” she contends.

Stephen Denis, executive director of the Small Business Finance Association, a trade group for alt funders, agrees. While most of the SBFA’s members don’t work with bank partners, the trade group has supported the lobbying efforts of other associations and coalitions representing financial services companies directly affected, he says. “We are concerned on behalf of the broader industry because we all work closely together and everyone has the same goal of making sure that we’re providing capital to small businesses,” he maintains.

That goal of keeping funds available to entrepreneurs also motivates the sponsor of H.R. 3299, Rep. Patrick McHenry, R-N.C., who’s chief deputy whip of the House and vice chair of the House Financial Services Committee. His interest in crowdfunding, capital formation and disruptive finance is fueled by events he experienced in his childhood, when his father attempted to operate a small business but struggled to find financing, according to the Congressman’s website.

Although H.R. 3299 passed in the House with mostly Republican votes, it attracted bipartisan co-sponsors in that chamber. They are Rep. Gregory Meeks, D-N.Y.; Rep. Gwen Moore, D-Wis., and Rep. Trey Hollingsworth, R-Ind. The Senate version of the legislation is sponsored by Sen. Mark R. Warner, D- Va.

Although H.R. 3299 passed in the House with mostly Republican votes, it attracted bipartisan co-sponsors in that chamber. They are Rep. Gregory Meeks, D-N.Y.; Rep. Gwen Moore, D-Wis., and Rep. Trey Hollingsworth, R-Ind. The Senate version of the legislation is sponsored by Sen. Mark R. Warner, D- Va.

But opponents of the proposed law aren’t feeling particularly bipartisan and argue vehemently against it, Brennan contends. “There’s been a lot of misinformation put out there by consumer advocates saying this would somehow embolden payday lending in all 50 states,” she says. “It’s simply not true.”

Payday lenders aren’t banks, so the proposed legislation would not apply to them and thus would not enable them to avoid interest caps imposed by borrowers’ states, Brennan notes, adding that some states don’t even allow payday consumer lending.

Consumer advocates are spreading propaganda because they oppose interest rates they consider high, Brennan continues. Advocates are incorrectly conflating payday lending with marketplace lending, she maintains.

The latter is defined as partnerships where non-banks sometimes work with banks to operate nationwide platforms, mostly online and sometimes peer-to-peer, she says, noting that examples include LendingClub and Prosper.

There’s no evidence marketplace lenders would astronomically increase their interest rates if the president signs into law a bill that resembles those now before Congress, Brennan says. It wasn’t happening before Madden, she notes, and banks involved in those partnerships operate under strict guidance of the Federal Deposit Insurance Corp. (FDIC) or the Office of the Comptroller of the currency, depending upon their charters.

But consumer advocates haven taken to the warpath, Brennan reports. Opponents of the legislation call partnerships between banks and non-bank lenders by the derogatory term “rent-a-bank schemes.” But it’s lawful to create such relationships because the FDIC oversees them, she asserts.

Just the same, the House is considering H.R. 4439, a bill to ensure that in a bank partnership with a non-bank, the bank remains the “true lender” and can set the interest rate, Brennan notes. If the bill becomes law, it would clear up the conflict that has arisen in inconsistent case law, some of which has defined the non-bank as the true lender, she says.

Meanwhile, opponents of H.R. 3299 and S. 1642 have written a letter to members of Congress, urging them to vote against the bills. The letter, drafted by the Center for Responsible Lending (CRL) and the National Consumer Law Center (NCLC), was signed by 152 local, state, regional and national organizations. Most of the signers belong to a coalition called Stop the Debt Trap, says Cheye-Ann Corona, CRL senior policy associate.

The bills create a loophole that enables predatory lenders to sidestep state interest rate caps, Corona maintains. That’s because non-banks are actually originating the loans when they work in tandem with banks, she says. The non-banks are using banks as a shield against state laws because banks are regulated by the federal government. If the legislation passes, non-banks would not have to observe state caps and could charge triple-digit interest rates, she contends.

“This bill is trying to address the issue of fintech companies, but there is nothing innovative about usury,” Corona says. “They are just repackaging products that we’ve seen before. A loan is a loan. These lenders don’t need this bill if they are obeying state interest-rate caps.”

The lenders disagree. In fact, a trade group formed by OnDeck, Kabbage and Breakout Capital calls itself the Innovative Lending Platform Association, according to a report in the Los Angeles Times. The article cites the need for small-business capital but questions whether the loans are marketed fairly.

Innovative or not, lenders offering credit with higher interest rates could condemn consumers to a nightmare of debt, according to the letter from the CRL and NCLC to Capitol Hill. “Unaffordable loans have devastating consequences for borrowers – trapping them in a cycle of unaffordable payments and leading to harms such as greater delinquency on other bills,” the letter says.

However, alt funders say their savvy small-business customers understand finance and thus don’t need much government protection from high interest rates. But the CRL doesn’t adhere to that philosophy, Corona counters. “Small businesses are at risk with predatory lending practices,” she says, maintaining that some alt funders charge interest rates of 99 percent.

Small-business owners plunged themselves into hot water by borrowing too much in anecdotal examples provided by Matthew Kravitz, CRL communications manager. In one example, an entrepreneur found himself automatically paying back $331 every day. He overestimated his future income and now says he feels like hiding under the covers every morning.

Corona also dismisses the idea that high risk calls for high interest rates to compensate for high default rates. When interest rates rise to a level that borrowers can’t handle, no one wins, she maintains.

The right to charge higher interest rates could also encourage lenders to loosen their underwriting criteria, Corona warns. That could result in shortcuts reminiscent to the practices that gave rise to the foreclosure crisis and the Great Recession, she says, adding that, “we don’t want to see that happen again.”