Archive for 2018

Interest in Equipment Finance M&A is Strong

July 19, 2018

Interest in mergers and acquisitions (M&As) in the equipment finance industry has been high in the first half of 2018, according to The Alta Group, a consultancy dedicated to equipment leasing and asset finance.

This follows a May 22 Reuters report announcing that global M&As reached $2 trillion in 2018, which at the time of publication, was a record for the value of deals in that period. This record was achieved in part by the $11.1 billion merger of GE’s (GE.N) transportation business with rail equipment maker Wabtec (WAB.N).

Echoing the robust global M&A climate, Cincinnati-based Verdant Commercial Capital, a large commercial equipment finance company, announced on Monday that it had acquired Intech Funding Corp., which does financing and leasing for manufacturing companies. (The Alta Group was involved in this acquisition). No financial terms were disclosed for this acquisition.

“Several of our clients had not considered selling their businesses yet,” said Bruce Kropschot, Senior Managing Director of The Alta Group, “but M&A market conditions are so favorable now they concluded they could not risk missing out on the opportunity to sell while prices were high and there were many interested acquirers.”

In a statement, Kropschot attributed this favorable climate for M&As to “the relatively high multiples reflected in the stock market and the M&A market, interest rates that are still quite low, substantial liquidity in corporations and financial institutions, and the recent tax legislation with its lower corporate income tax rates and 100% expensing on equipment purchases.”

The Alta Group has clients throughout the world and has been representing equipment leasing and finance companies since 1992. It is headquartered in Glenbrook, Nevada and employs 60 consultants worldwide.

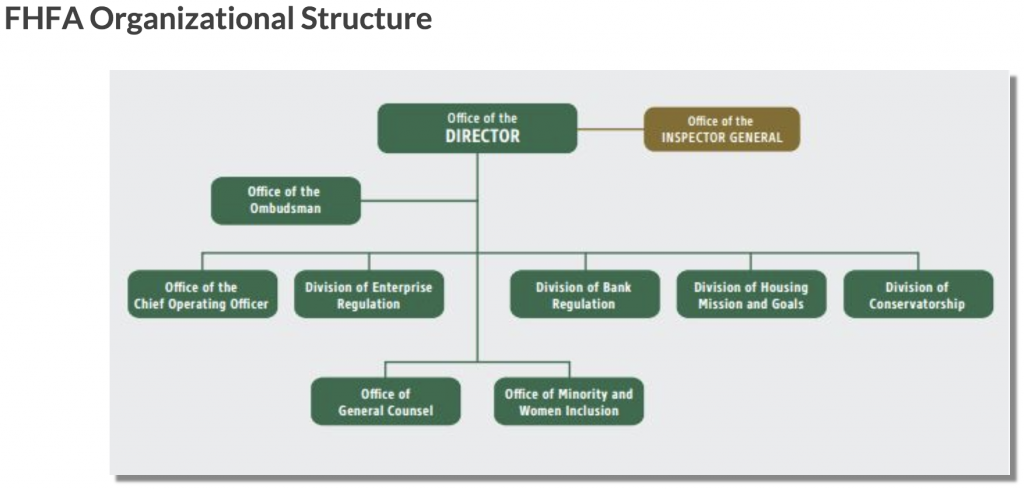

Like Bureau of Consumer Financial Protection, Court Declares FHFA Unconstitutional

July 19, 2018The Bureau of Consumer Financial Protection (Bureau), created largely by Democratic politicians in the wake of the 2008-10 financial crisis, has not been the most popular government agency under the current administration. That said, a June court decision declared that the agency itself is, in fact, not very democratic.

The controversial decision came from District Judge Loretta Preska of the New York’s Southern District who declared the Bureau to be unconstitutional based on its single directorship structure. (The current structure features a director who has full control over decisions with no requirement of a vote or a consensus from other colleagues or parties).

This week, the Court of Appeals for the Fifth Circuit made a ruling against the Federal Housing Finance Agency (FHFA) for the same reason – because it deemed the agency to be unconstitutional based on its single directorship structure.

The FHFA was established by the 2008 Housing and Economic Recovery Act to ensure that Fannie Mae, Freddie Mac and the Federal Home Loan Bank System are operating in a safe and sound manner so they can serve as a reliable source of liquidity and funding for housing finance and community investment.

The defense for this decision against the FHFA cites heavily from a 2016 ruling, written by Supreme Court Justice nominee Brett Kavanaugh, that asserts that the Bureau is unconstitutional in large part because the director cannot even be removed the president. Part of this week’s FHFA decision is as follows:

“Congress encased the FHFA in so many layers of insulation—by limiting the President’s power to remove and replace the FHFA’s leadership, exempting the Agency’s funding from the normal appropriations process, and establishing no formal mechanism for the Executive Branch to control the Agency’s activities—that the end ‘result is a[n] [Agency] that is not accountable to the President.’ The President has been ‘stripped of the power [the Supreme Court’s] precedents have preserved, and his ability to execute the laws—by holding his subordinates accountable for their conduct—[has been] impaired.'”

The 2016 decision decreeing that the Bureau is unconstitutional is similar:

“Other than the President, the Director of the Bureau is the single most powerful official in the entire United States Government, at least when measured in terms of unilateral power. That is not an overstatement. What about the Speaker of the House, you might ask? The Speaker can pass legislation only if 218 Members agree. The Senate Majority Leader? The Leader needs 60 Senators to invoke cloture, and needs a majority of Senators (usually 51 Senators or 50 plus the Vice President) to approve a law or nomination. The Chief Justice? The Chief Justice must obtain four other Justices’ votes for his or her position to prevail…”

Clearly, some judges feel that the Bureau and the FHFA are unconstitutionally formed. Whether these agencies will change their structure in response to these decisions is unclear.

Australia Brimming with Alternative Lending Activity

July 18, 2018 OnDeck announced today that it has closed on a $75 million (AUD) asset-backed revolving credit facility with Credit Suisse for its business in Australia. This will be used to refinance OnDeck Australia’s current loan book at a significantly lower cost, as well as to fund future originations there.

OnDeck announced today that it has closed on a $75 million (AUD) asset-backed revolving credit facility with Credit Suisse for its business in Australia. This will be used to refinance OnDeck Australia’s current loan book at a significantly lower cost, as well as to fund future originations there.

This comes shortly after Lending Express CEO Eden Amirav told deBanked that the success his company had in Australia in just a little more than a year gave them the confidence to enter the U.S. market.

“After the immense success we’ve had in the Australian market, we knew that our platform was ready to take on the U.S.,” Amirav said in June.

And several large fintech companies, including OnDeck, joined forces this month to create a set of best practices, called The Code, that would regulate how fintech companies operate in Australia. The market down under has seen a fairly rapid expansion over the last several years.

Some of the major fintech companies there include Prospa, OnDeck, Capify, GetCapital, Moula and Spotcap.

Texas Man Defrauds Banks with Cattle

July 18, 2018 A Texas man was arrested last week on allegations of using 8,000 heads of cattle he did not own as collateral for outstanding loans of more than $5.8 million, according to Dallas News.

A Texas man was arrested last week on allegations of using 8,000 heads of cattle he did not own as collateral for outstanding loans of more than $5.8 million, according to Dallas News.

The arrest was the culmination of a 16-month investigation carried out by the Texas and Southwestern Cattle Raisers Association. They were contacted by bank officials at the First United Bank in Sanger, Texas, who said that Howard Lee Hinkle had not made payments on loans with balances totaling more than $5.8 million. The bank obtained a court order to collect the 8,000 cows that Hinkle put up as collateral, but they were unable to find any of the cattle at the locations he had given the bank. Hinkle allegedly presented fake documentation.

Fintech lenders have also been victims of fraud whereby a merchant provides false documents, sometimes claiming to own property they do not own

Charged with first degree felony charges of theft, the 67-year-old Hinkle could serve a life sentence in jail. He was arrested last Thursday and brought to the Wichita County Jail, where he was released on bond pending trial.

FCI Implements Factoring Solution That Is Islamic Law-Compliant

July 17, 2018The FCI, an international trade group focused on factoring, implemented changes to its General Rules of International Factoring so that they are now compliant with Islamic (Shari’a) law. The Amsterdam-based factoring group, which just celebrated its 50th anniversary, worked with Dubai-based Noor Bank and other constituents, to create amendments to its rules that would make it Shari’a law compliant, according to a recent FCI announcement.

While the details of the changes to FCI’s rules were not immediately available, deBanked spoke to Abed Awad, founding partner at New Jersey-based Awad & Khoury, who is an expert in Islamic law.

Awad said that Shari’a law’s fundamental problem with factoring is that it involves collecting interest, which is prohibited. While factoring might not seem to involve interest, Awad said that offering less cash upfront for a receivable that is worth more in the future, is essentially a reverse form of interest.

But Awad said that in recent years, people have developed a somewhat controversial concept, called Tawarruq (or monetization) that abides by the prohibition of interest rule while yielding the same result. This is how it works:

A merchant in need of cash goes to a bank. Rather than offering cash to the merchant, the bank instead arranges for a merchant to buy a commodity (like oil or sugar), on credit. The merchant doesn’t have to pay for the commodity until a future date. Meanwhile, the merchant quickly sells the commodity for cash to a third party. The merchant now has cash and will not be paying interest of any kind. The bank still makes money. It gets paid for structuring the arrangement between the merchant and the seller of the commodity, and for evaluating the creditworthiness of the merchant.

The end result is the same for the merchant. The merchant gets cash quickly, albeit a little less quickly because there are multiple parties involved. Noor Bank currently offers an Islamic law compliant factoring product. Tawreeq Holdings, which has offices in Luxembourg, United Arab Emirates and Morocco, specializes in the Tawarruq alternative to factoring.

“Islamic Factoring is an increasingly important element in the finance of international trade and our ability to support Shari’a compliant business is particularly important for our global member base, said Peter Mulroy, Secretary General of FCI. “This development is another real enhancement of the support we can provide for our members.”

Walmart Not New to Financing

July 17, 2018 Walmart is considering switching its branded credit card business partner from Synchrony Financial to Capital One Financial Group, according to a Bloomberg report. Accordingly, the change in banking partner is related to the retailer’s vision for Walmart Pay, Walmart’s current checkout payment system.

Walmart is considering switching its branded credit card business partner from Synchrony Financial to Capital One Financial Group, according to a Bloomberg report. Accordingly, the change in banking partner is related to the retailer’s vision for Walmart Pay, Walmart’s current checkout payment system.

In light of this, it is worth noting that Walmart is no stranger to working creatively and ambitiously with banks. In fact, aside from currently having independent bank branches that operate from inside Walmart stores – including Fort Sill National Bank and City National Bank and Trust – Walmart once had aspirations to become a bank.

In 2006, using an old and now controversial statute, the behemoth retailer attempted to get a charter to become an Industrial Loan Company (ILC) Bank. Chris Cole, Senior Regulatory Counsel at Independent Community Bankers of America (ICBA), a trade group, told deBanked that banks and other anti-Walmart groups banded together to thwart the retailer’s plans.

Recently, two fintech companies, SoFi and NelNet, have submitted applications to become ILC banks.

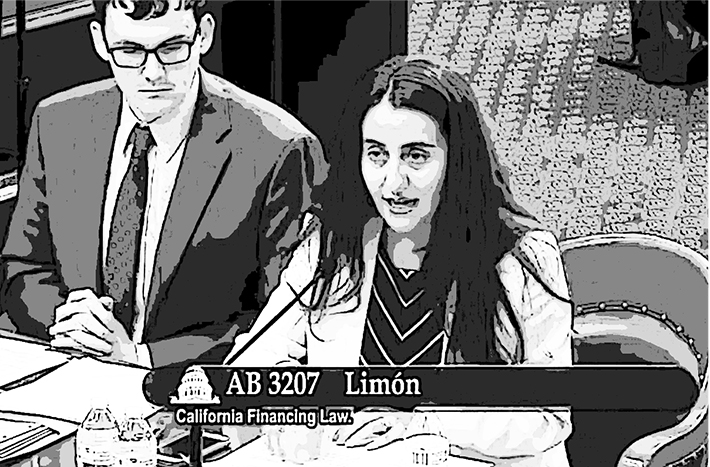

California Bill May Disadvantage Small Brokers

July 17, 2018A California State Assembly bill that carefully defines what a broker is, could significantly affect small, unlicensed brokers, according to Tom McCurnin, an attorney at Barton, Klugman and Oetting in Los Angeles.

Assembly bill 3207 enumerates the ways that the bill would depart from the current law. Most notably, the definition of a broker would be far more precise. The current California Licensing Law, which requires brokers to be licensed, defines a broker as “anyone who is engaged in the business of negotiating or performing any act as a broker in connection with loans made by a finance lender.”

Tom McCurnin – Barton, Klugman & Oetting LLP

Tom McCurnin – Barton, Klugman & Oetting LLP“It’s a circular definition,” McCurnin said. “It presently says that a broker is someone who is brokering transactions.”

Essentially, it defines a broker as a broker, leaving plenty of room for ambiguity.

“With respect to registering to conduct business in the state of California, we’ve got tons of brokers doing deals in California, but they’re not licenced here,” McCurnin said. “They do deals in California, but they’re located in Florida or New York or Michigan. They’re making money in the state of California. Why shouldn’t they pay their fair share of taxes?”

People can always evade the law and not get licenced. But the idea behind this bill is that by making the definition of a broker perfectly clear, it’s no longer possible for a broker to make an argument that they’re not really a broker. With the language in the bill, a broker would be in clear violation of the law if they don’t obtain a licence.

The new definition of a broker would be “anyone who, among other things, transmits confidential data about a prospective borrower to a finance lender with the expectation of compensation.” McCurnin notes that “expectation of compensation” is an important phrase, currently used to describe real estate brokers, because it states clearly that the broker intends to earn money from the consumer. The proposed definition in the bill continues to define a broker as someone who “participates in any loan negotiation between a finance lender and prospective borrower, participates in the preparation of loan documents, communicates lending decisions or inquiries to a borrower, or charges a fee to a prospective borrower for any services related to an application for a loan from a finance lender.”

This definition leaves little room for debate. So what does getting a California State broker licence entail? It requires that a broker have at least $25,000. Beyond this, McCurnin says it inquires primarily about three other things: 1) if you have a criminal record (fingerprints are required), 2) what type of loans you intend to broker (secured, unsecured, etc.), and 3) the size of the loans you intend to broker. There are different regulations for different loan sizes.

Being licensed requires being registered to conduct business in the state of California. And a registered business must pay taxes on earnings in the state. With this in mind, McCurnin said the passage of this bill could be a win for California in that it could result in more out-of-state brokers getting registered and paying taxes on their earnings in the state.

At the same time, should the bill pass, McCurnin thinks it would be a big loss for the small broker who is either unable to show $25,000 or who might have something unsavory to hide. But if the small broker working from his basement has enough capital and is willing to state what he intends to broker in California, then obtaining the license shouldn’t be a problem.

The bill passed in the state Assembly and is being reviewed in the Senate. An amendment to the bill was made on July 5. Another California bill of great significance to the alternative lending industry is SB-1235, which has passed in the state Senate and is being reviewed in the state Assembly. McCurnin said he believes that the broker bill will pass.

“California is a very liberal place,” McCurnin said. “It’s like another country.”

How to Avoid Being Sued by a Professional TCPA Plaintiff

July 13, 2018

Did you know that if you receive an unwanted solicitation call on your private cell phone or residential landline, you can win between $500 and $1,500 in damages from the offending company? The company can be charged for violating a statute of the 1991 Telephone Consumer Protection Act (TCPA), which prohibits companies from calling consumers without their express permission. You might not know about this, but others know about it all too well.

Some people use this TCPA statute as a way of making money, by purchasing multiple phone numbers in the hope they will receive unsolicited phone calls that violate the TCPA statute. And if they do, they sue. deBanked previously explored “professional plaintiffs” like this, with a focus on those who have come up against funding companies.

According to Michael O’Hare, CEO of Colorado-based Blindbid, people who manipulate the TCPA statute for profit also target lead generation companies like his. O’Hare is currently being sued by a plaintiff for several million dollars in a class action lawsuit. The claim is that Blindbid allegedly made five unsolicited calls in 2016 to the plaintiff’s plumbing company. (According to David Klein, Managing Partner at Klein Moynihan and Turco, there is a murky area in the TCPA regulation where, if a cell phone is used for both personal and business use, the phone can be considered a personal phone, protected under TCPA.) In O’Hare’s case, upon further discovery, it was determined that only one of the five alleged calls actually came from Blindbid. But O’Hare says that the number was opted in and manually dialed. Regardless, O’Hare’s plaintiff is a pro, what some might call a “professional plaintiff.”

Over the last six years, this plaintiff participated in four major class action lawsuits that have led to combined settlements of $31 million, according to O’Hare. The plaintiff has also filed 34 cases in federal court since 2016, O’Hare said.

Over the last six years, this plaintiff participated in four major class action lawsuits that have led to combined settlements of $31 million, according to O’Hare. The plaintiff has also filed 34 cases in federal court since 2016, O’Hare said.

What is noteworthy about O’Hare’s case is that it’s part of what he says is a trend towards class action lawsuits based on TCPA violations, and often brought on by professional plaintiffs. O’Hare said it’s no coincidence that his plaintiff waited for two years to sue.

“The longer a plaintiff waits, the more members he can bring into the class. And the more members in the class, the larger settlement,” O’Hare said.

As a way to transform O’Hare’s lawsuit into a class action suit, he said that his plaintiff’s attorney has made the argument that if Blindbid violated his client’s TCPA rights to privacy with the one unsolicited call, then Blindbid likely violated others as well. So in discovery, the plaintiff’s attorney wants to compel Blindbid to turn over its phone records for the past two years to prove that Blindbid had “express written consent” from the other merchants it called. In the age of the internet, “express written consent” translates to filling out an online form where the individual consents to receive a phone call.

To satisfy the attorney’s request, Blindbid would have to match every phone number that was called with a corresponding computer IP address. This should be doable, but O’Hare says that professional plaintiffs, like his, deny that they ever filled out an online lead form, or that the IP address O’Hare has on record belongs to them.

“In the past, if there was an alleged TCPA violation, most companies could settle for a few thousand dollars to $10,000 depending on the number of violations,” O’Hare said. “Now there are these are multi-million dollar settlements.”

Unlike the fines of years past, these class action lawsuits can sink your company. While O’Hare said that there is no way to completely protect one’s company from being sued, below are some of his recommendations.

Have express written consent of all the merchants you call

Online consent is valid if the text explicitly states to the user that he is giving, in effect, express written consent to be contacted by your company by phone, text and/or email.

Register your company with Federal and State Do Not Call Registries.

Respect merchants’ requests

If they do not want to be called any longer, put their numbers on your “Do Not Call” list.

Have a written “Do Not Call” policy

Have a TCPA attorney review the policy and include a copy in your company employee guide.

Find a good TCPA scrubbing service

These are services that have many of the numbers that belong to professional plaintiffs and they monitor for newly registered phone numbers. They tell you which numbers to remove from your lists. Some good scrubbing services are TCPALitigatorList.com and DNC.com.

Don’t buy lists from overseas

These lists are full of professional litigator phone numbers you are taking a huge risks.

Never autodial / robo call

Robo calls are the most dangerous type of calls you can make unless you have a full opt-in list with express written consent from each of the merchants. Robo calls and text messaging TCPA violations are the easiest TCPA cases for plaintiffs to win and the settlements are higher. Every robocall or text is fined. The use of an autodialer is one of the elements to prove a TCPA violation. If you use an auto dialer with human intervention, like EVS 7, you can argue that your autodialer calls are manual calls. Still, use caution.

Consult with a TCPA attorney

I would advise every company that does any outbound calling to consult with a TCPA attorney about best practices. An ounce of prevention is worth a pound of cure.