p2p lending

National Security Could Prove to be Alternative Lending’s Achilles Heel

December 11, 2015 While alternative lenders debate disclosure policies, stacking, and the cost of bad merchants, there’s a new regulatory threat taking root that no one seems to be able to slow down, national security. Ever since it was revealed that one of the two terrorists in the San Bernardino attack received a $28,500 loan from the Prosper Marketplace, government officials and the public at large are pointing fingers at online lenders.

While alternative lenders debate disclosure policies, stacking, and the cost of bad merchants, there’s a new regulatory threat taking root that no one seems to be able to slow down, national security. Ever since it was revealed that one of the two terrorists in the San Bernardino attack received a $28,500 loan from the Prosper Marketplace, government officials and the public at large are pointing fingers at online lenders.

House Financial Services Chair Jeb Hensarling said on Thursday that, “clearly the financing link to terrorism is a critical one.” As quoted by Politico, “everything’s on the table,” he said when asked about further scrutiny of online lenders.

His sentiment echoes other responses, some of which are clearly emotionally charged and accusatory. LendAcademy’s Peter Renton for example wrote, “I have had to answer such ridiculous questions as, is P2P lending going to become the new way for terrorists to get funding?”

With so much misinformation now floating around out there about online lenders, conspiracy theorists are even claiming that it would be impossible for someone earning $53,000 a year (As Syed Farook did) to get an unsecured loan for $28,000, the implication being that there is something more sinister going on. Of course those that work in the alternative lending industry, including myself personally as someone who invests on the Prosper Marketplace, know that’s not true.

But before the experts can be called on to answer the questions, those motivated to protect this country at all costs (with noble intentions) are rallying around swift and immediate consequences for online lenders such as Prosper.

“The issue may end up being whether marketplace lenders are too easy of a source of cash to finance terrorist attacks,” said Guggenheim Partners analyst Jaret Seiberg in a research letter.

In an article published by The Street, writer Ross Kenneth Urken basically likened Prosper Marketplace to Silk Road where bitcoins were used to buy drugs, weapons, and killers for hire.

Breitbart News, a right-wing news website, led in with an even bigger headline, San Bernardino: Has Islamic State Hijacked Consumer Loans?. It quickly sums up the story by insinuating that online lenders will become the funding tool of choice for ISIS. “The San Bernardino terrorists, Syed Rizwan Farook and his wife Tashfeen Malik, funded their killing spree with a debt consolidation loan, raising questions about whether terrorists might use popular consumer loans to fund their activities,” Breitbart wrote.

And the International Business Times argued that Utah industrial banks are aiding terrorism. “Meanwhile, industrial banks in Utah are taking full advantage of the lack of regulation in the peer-to-peer lending market while they still can, aiding potential terrorists along the way,” author Erin Banco concluded.

According to the WSJ, the House Financial Services Committee will examine whether new legislation is needed in online lending. They’ve also made inquiries to the Treasury Department about existing online lending regulations. Treasury Counselor Antonio Weiss’s previous remarks hinted that the Treasury up until recently was concerned about discriminatory lending practices more than anything else, but stressed that they were not a regulator in this area. Terror financing was not something they even addressed.

According to many sources, lawmakers are drafting up legislation on terrorism financing and expect to have something ready early next year. As for how that will impact online lenders is unknown. Right now, everyone’s still trying to figure out what just happened. Hopefully whatever is ultimately done is done intelligently.

Prosper Loan Linked to Terror – A Preliminary Assessment

December 9, 2015By now you have probably heard that one of the San Bernardino terrorists received a $28,500 deposit from WebBank.com two weeks prior to committing the attack. After Fox News broke that story, I may have been the first to publicly connect it to an alternative lender which was later revealed to be marketplace lender Prosper about 12 hours later.

As a Prosper investor myself, here are some things you should know:

The $28,500 deposit (if that was the exact true amount) would have been net of the origination fees. In all likelihood this was a loan for around $30,000 and the borrower only netted $28,500.

Those that have speculated that it would be impossible for someone making $53,000 a year (as Syed Farook did) to qualify for an unsecured loan of this amount are wrong. There are loans on the platform right now that fit these parameters. Online Lenders like Prosper and Lending Club are pretty aggressive with their lending.

The notion that Prosper somehow could’ve detected what the borrower planned to do two weeks later just isn’t possible. In lending, this is known as the asshole factor, meaning that even if the applicant meets all the criteria, they could just decide to be an asshole, and there’s no way to predict that.

There are strict laws in place to prevent all kinds of discrimination, meaning that even if Prosper had formed some kind of suspicion about the borrower, it may have been illegal to act on that suspicion. Such is the hypocritical paradigm of fair lending where factors that are measurable predictors of negative performance (or worse) cannot be legally used. Federal laws have purposely tried to create an environment where lenders make decisions on an objective basis they consider to be fair. In business lending for example, there is a law within Dodd-Frank that has not been implemented yet, but seeks to prevent loan officers from knowing the gender or even the name of the prospective borrower to protect them from subconscious discrimination.

Investigators have publicly announced that the terrorists were not on any watch lists and therefore there are no systems or checks that Prosper could’ve plugged into to have gotten the information.

Prosper and other alternative lenders already have Anti-Money Laundering Policies. I know this because I complained about Lending Club’s over a year ago.

The Wall Street Journal stated, “Only some nonbank financial institutions, such as mortgage lenders, are subject to Treasury rules requiring lenders to report suspicious activity to the government under the Financial Crimes Enforcement Network.” Maybe that’s true, but there is nothing suspicious about someone applying for a loan online who is not on any watch lists. I can’t think of anything that could’ve been suspicious unless they submitted fake pay stubs or forged documents.

“There’s no due diligence that’s done into how these loans are actually going to be used,” said Brian Korn, a partner at the law firm Manatt, Phelps & Phillips, LLP in the WSJ. This is true and at the same time related to anti-discrimination laws. Judging a loan applicant by their detailed monetary plans could potentially induce gender or ethnicity bias, even if subconscious.

There will be plenty of questions in the coming days from Americans, the media, and government officials about what alternative lenders are doing to make sure they’re not funding terrorists. Part of what they may learn is that for all the data that alternative lenders have at their disposal to make intelligent decisions on an automated basis, some of them cannot be legally used. They’ll also find out that there’s only so much that predictive analytics can actually predict.

It’s very unlikely that Prosper could’ve handled anything differently…

Alternative Lender Likely to Be Questioned in San Bernardino Terror Tragedy

December 7, 2015Fox News has reported that terrorist Syed Farook received a $28,500 deposit two weeks before committing the terrorist act with his wife. The source of the money? WebBank.com, an FDIC-insured, state-chartered industrial bank based in Salt Lake City, Utah. Perhaps more notably, it’s the bank that originates loans for dozens of alternative lenders including Lending Club, Prosper, and Avant.

WebBank.com is reportedly refusing to comment but in all likelihood we are probably going to learn that the loan was made by an alternative lender.

As written on Fox News:

The loan and large cash withdrawal were described to Fox News by the source as “significant evidence of pre-meditation,” and further undercut the premise that an argument at the Christmas party on Dec. 2 led to the shooting.

If the loan was indeed originated on a marketplace lending platform like Lending Club or Prosper, hundreds of Americans could potentially face the horror of having bought shares in the loan and made it possible.

For now, all we know is that Farook got $28,500 through a WebBank.com deposit. I’ll post more as the story develops.

Lending Club Borrower Exceeded 5 Credit Inquiries | Investors Raise Eyebrows

December 5, 2015 Unblinking investors on the Lending Club marketplace called attention to an anomaly through the LendAcademy forum two weeks ago. At issue was a borrower whose profile reportedly had 9 recent credit inquiries, which exceeded Lending Club’s maximum eligibility to even be listed. As the prospectus of each loan stipulates “5 or fewer inquiries (or recently opened accounts) in the last 6 months,” investors wondered how somebody with 9 had slipped through the cracks.

Unblinking investors on the Lending Club marketplace called attention to an anomaly through the LendAcademy forum two weeks ago. At issue was a borrower whose profile reportedly had 9 recent credit inquiries, which exceeded Lending Club’s maximum eligibility to even be listed. As the prospectus of each loan stipulates “5 or fewer inquiries (or recently opened accounts) in the last 6 months,” investors wondered how somebody with 9 had slipped through the cracks.

But it wasn’t just one, user Fred revealed that this was a very common occurrence. “In my database of LC loans collected so far, I saw 1000+ loans with 6+ inquiries in the last 6 months,” he wrote.

Concerned, somebody reached out to Lending Club to find out what the deal was.

The response they got back was that auto or mortgage inquiries do not count as inquiries in their underwriting. However, their system had glitched and was inadvertently including them. That meant the borrower showing 9 inquiries did indeed have 9 but 4 of them were auto and mortgage related and therefore weren’t subject to the cap of 5.

While car loans and mortgages might not be as relevant to unsecured consumer debt activities, it is interesting that these inquiries are supposed to be glossed over in the total inquiries revealed to potential investors.

For instance, in this case, a borrower with approximately 720 credit earning $73,000 a year has 11 inquiries but for all points and purposes, Lending Club is only counting up to 5 of them. They were seeking a $29,175 personal loan for “business purposes.” The loan was eventually removed for reasons unknown.

For those buying these notes, as always, buyer beware.

Beat The $3,000 Capital Loss Cap in Marketplace Lending

November 24, 2015 Because interest on platforms like Lending Club is counted as normal income and the losses as capital losses, you can only deduct a maximum loss amount of $3,000 if you don’t have capital gains from other investments. That can be an expensive mistake for an investor with a large portfolio who isn’t paying attention. For instance, if you earned $20,000 in income through Lending Club but had $10,000 in losses from defaults, you’d actually be taxed on $17,000, not on the difference between the two. In, Is the Premium Gone in Peer-to-Peer Lending?, I wrote that there’s a whole lot of risk in marketplace lending and not a whole lot of yield to compensate for it, especially when considering the poor tax treatment.

Because interest on platforms like Lending Club is counted as normal income and the losses as capital losses, you can only deduct a maximum loss amount of $3,000 if you don’t have capital gains from other investments. That can be an expensive mistake for an investor with a large portfolio who isn’t paying attention. For instance, if you earned $20,000 in income through Lending Club but had $10,000 in losses from defaults, you’d actually be taxed on $17,000, not on the difference between the two. In, Is the Premium Gone in Peer-to-Peer Lending?, I wrote that there’s a whole lot of risk in marketplace lending and not a whole lot of yield to compensate for it, especially when considering the poor tax treatment.

It’s surprisingly easy to rack up thousands of dollars in defaults in a single year even if you spread the risk around through small $25 increments. I know this because I’m teetering on the fence of it just on Lending Club alone. I had approximately $2,600 in charge-offs so far for 2015 at the end of October. Anything beyond $3,000 I can’t offset against my gains so there’s little sense in investing any more money.

Unless…

There is one way to build a significant portfolio without breaking the threshold, invest in the low risk loans. Of the 246 A-grade loans I’ve invested in, so far none of them have ever defaulted. Of the 675 B-grade loans, only 9 of them have already defaulted. Compare that to the 52 G-grade loans I’ve participated in where 11 have defaulted. It might interest you to know that the average time remaining to maturity on those G-grade loans is about 3 years. That means 21% of them have already gone bad and there’s still another 3 years left to go. While these stunningly high risk loans might return in yield for what they lack in performance, they’re a great way to build a capital loss mountain, something that could cause significant damage once you exceed $3,000.

By investing in low risk loans and staying below the capital loss cap, you can invest substantially more. Illogical as it may seem, a big lower yielding portfolio can earn more than a higher yielding one because of the tax treatment if you do not have outside investments with capital gains.

If you are a small investor looking to play with $5,000, none of this will likely be relevant to you, but if you were looking to place $100,000 or more, you might want to remember this phrase in marketplace lending, lower yield is more.

Read more about the capital loss rules and Lending Club on the LendAcademy blog.

FDIC Issues Guidance that May Curtail Bank Purchases of Marketplace Loans

November 20, 2015 On November 6, the Federal Deposit Insurance Corporation (FDIC) issued Financial Institution Letter FIL-49-2015, titled “Advisory on Effective Risk Management Practices for Purchased Loans and Purchased Loan Participations.” Though billed as an update to an advisory letter issued in 2012, the new guidance requires all FDIC-supervised banks and savings associations to implement a number of new procedures before purchasing loans or loan participations that are originated by third-party nonbank entities. These restrictions would include the purchase of or participation in small business loans originated by marketplace lenders. In fact, the letter cautions supervised entities from relying on marketplace platforms that the FDIC believes do not provide sufficient information to potential investors:

On November 6, the Federal Deposit Insurance Corporation (FDIC) issued Financial Institution Letter FIL-49-2015, titled “Advisory on Effective Risk Management Practices for Purchased Loans and Purchased Loan Participations.” Though billed as an update to an advisory letter issued in 2012, the new guidance requires all FDIC-supervised banks and savings associations to implement a number of new procedures before purchasing loans or loan participations that are originated by third-party nonbank entities. These restrictions would include the purchase of or participation in small business loans originated by marketplace lenders. In fact, the letter cautions supervised entities from relying on marketplace platforms that the FDIC believes do not provide sufficient information to potential investors:

[A]n increasing number of financial institutions are purchasing loans from nonbank third parties and are relying on third-party arrangements to facilitate the purchase of loans, including unsecured loans or loans underwritten using proprietary models that limit the purchasing institution’s ability to assess underwriting quality, credit quality, and adequacy of loan pricing. In some situations, it is evident that financial institutions have not thoroughly analyzed the potential risks arising from third-party arrangements.

The three pages of new guidance require a variety of procedures be implemented, including:

1. The new guidance significantly expands the policies a bank must establish before purchasing, such as:

- Establishing detailed procedures for purchased loans and participations

- Defining loan types that are acceptable for purchase

- Requiring board of directors approval of arrangements with third-parties to purchase loans and participations

Additionally, financial institutions are required to establish ongoing risk management processes for purchases made through third-party relationships.

2. The new guidance requires enhanced independent analysis of purchased loans and participations. A purchasing institution must ensure that it has “the requisite knowledge and expertise specific to the type of loans or participations purchased and that it obtains all appropriate information from the seller to make an independent determination.” The loans and participations must also be determined to be consistent with the bank’s appetite for risk. The letter states that this analysis must be done in-house and may not be contracted out to a third-party.

3. A supervised bank must also perform due diligence on the validity of a third party’s credit models if the bank relies on the model for credit decisions. A bank is permitted to subcontract this due diligence to third-parties but is still required to review the model validation to ensure it is sufficient.

The new guidance will undoubtedly increase the costs FDIC insured banks incur to purchase loans and loan participations originated by small business marketplace lenders. What effect these costs will have on current and future bank involvement in marketplace lending remains to be seen.

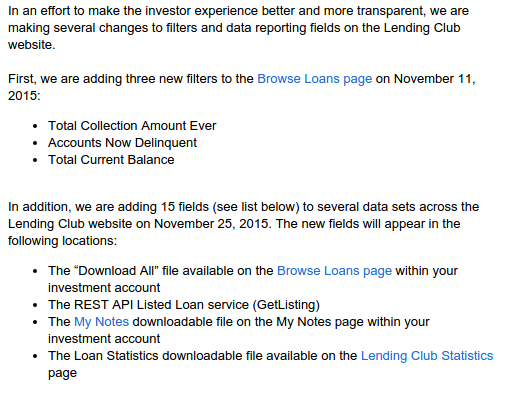

Lending Club Narrowly Avoids Major Transparency Flop

November 18, 2015After many months of Lending Club warning that they would be REMOVING borrower credit data from note listings, they have completely reversed course and ADDED fifteen new credit attributes. On Peter Renton’s LendAcademy forum, one member speculated that this move was made to compete with Prosper for the attention of institutional investors. If true, that would be entirely misguided.

Almost exactly one year ago, Lending Club announced that they were cutting the amount of data points available to investors from 100 to 56. Renton, a marketplace lending evangelist and founder of the LendIt conference, gave it a negative spin in his blog:

It is pretty obvious by now that I don’t like these changes. For quite some time now Lending Club has been reducing the amount of transparency for investors. Now, some changes I completely understood such as removing the Q&A with borrowers and even the removal of loan descriptions. But removing data that investors have been using to make investment decisions is a step too far in my opinion.

I think Lending Club need to ask themselves if they are a true marketplace connecting borrowers and investors in a transparent fashion or whether they are more of a loan origination platform that makes products available to investors. They are certainly moving more towards the latter, I think, and that is a shame for everyone.

The move was seen by many as a way to stop investors from trying to reverse engineer their models and beat their grading system for above average yields. While understanding that perspective, it is mind boggling that they had planned to remove more data points and make the loans on the platform even less transparent. And here’s why…

Lending Club is a key signatory to the Small Business Borrower’s Bill of Rights, a group of political activists that claim innovative small business lending can only achieve its potential “if it is built on transparency, fairness, and putting the rights of borrowers at the center of the lending process.” With transparency being a focal point of their agenda there, one might find their attempts to reduce disclosure and eradicate transparency a bit hypocritical.

Lending Club is a key signatory to the Small Business Borrower’s Bill of Rights, a group of political activists that claim innovative small business lending can only achieve its potential “if it is built on transparency, fairness, and putting the rights of borrowers at the center of the lending process.” With transparency being a focal point of their agenda there, one might find their attempts to reduce disclosure and eradicate transparency a bit hypocritical.

Investors on Renton’s forum who had for months anticipated Lending Club to remove more data points, also viewed it negatively. “I’d have to think hard on whether to continue investing in LC notes without those credit fields — it would be very much like gambling rather than investing,” wrote Fred back on July 8th.

A similarly named user, Fred93, communicated that these data points were all investors had to go off. “We can’t shake a borrower’s hand, feel the firmness of his grip, the sweatiness of his palm. We can’t look a borrower in the eye. We live or die by a handful of numbers, which we hope mean something, on the average,” he wrote.

Clearly some investors weren’t thrilled with the proposed changes. All the while, Lending Club’s co-signatories had been promoting the transparency pledge through speeches, TV appearances, public relation events, and press releases. To be fair, The Small Business Borrowers Bill of Rights is aimed at transparency between business borrowers and sources offering business financing. Lending Club’s planned removal of data was targeted at investors in their consumer notes. It sounds different enough until you consider that 72% of Lending Club’s loans originated in 2014 were funded by investors vastly less sophisticated than the commercial businesses they have pledged to protect. That’s because that money came from consumers, many of whom are unaccredited and went through no screening process. Instead, these investors are presented with a prospectus as if they were buying a stock or bond and stuck with the risk whether they understand it all or not.

These consumers who are legally presumed to be unsophisticated are the very same people that Lending Club planned to reduce disclosures to, all the while heavily promoting to them that they roll over their retirement savings onto their platform. That logic is the very definition of insanity. Obfuscating the reasoning behind certain scoring grades to these investing consumers would be nothing short of unconscionable and would reasonably invalidate any pledge they’ve made towards transparency in other areas.

Lending Club has for now avoided a major flop by reversing course after having added 15 new pieces of data for investors.

While some investors speculated the move had to do with pressure from Lending Club’s institutional investor base. The more likely reason is increasing scrutiny from federal regulators. Less than two weeks ago for example, the FDIC warned banks about marketplace lending and advised them to perform their own underwriting on the loans they buy and not to rely on originator scoring models. A summary of their letter specifically said:

Some institutions are relying on lead or originating institutions and nonbank third parties to perform risk management functions when purchasing: loans and loan participations, including out-of territory loans; loans to industries or loan types unfamiliar to the bank; leveraged loans; unsecured loans; or loans underwritten using proprietary models.

Institutions should underwrite and administer loan and loan participation purchases as if the loans were originated by the purchasing institution. This includes understanding the loan type, the obligor’s market and industry, and the credit models relied on to make credit decisions.

Before purchasing a loan or participation or entering into a third-party arrangement to purchase or participate in loans, financial institutions should:

– ensure that loan policies address such purchases,

– understand the terms and limitations of agreements,

– perform appropriate due diligence, and

– obtain necessary board or committee approvals.

These guidelines conflict with Lending Club’s long sought after goal of getting investors to trust their A-G scoring grades. The banking regulator is advising banks to basically disregard them. “The institution should perform a sufficient level of analysis to determine whether the loans or participations purchased are consistent with the board’s risk appetite and comply with loan policy guidelines prior to committing funds, and on an ongoing basis,” the more complete memo reads. “This assessment and determination should not be contracted out to a third party.”

A law firm with specialized knowledge of the industry, criticized the FDIC’s move when they wrote on their website, “Ironically, given the Treasury Department’s recent request for information, which supported marketplace lending and focused in part on how the federal government could be supportive of the innovations in marketplace lending, we now have a federal banking agency that is creating roadblocks to having banks participate in this dynamic and rapidly growing space.”

Asking banks not to rely on marketplace scoring models alone hardly seems like a roadblock, especially when the models are tucked away in algorithmic obscurity, have hardly been around for very long, and would decide the fate of depositor money. And if this directive indeed contributed to Lending Club’s transparency reversal, then it couldn’t have been any more well-timed.

Asking banks not to rely on marketplace scoring models alone hardly seems like a roadblock, especially when the models are tucked away in algorithmic obscurity, have hardly been around for very long, and would decide the fate of depositor money. And if this directive indeed contributed to Lending Club’s transparency reversal, then it couldn’t have been any more well-timed.

Whether or not the added data points will make any difference to the performance of investment portfolios is irrelevant. If unaccredited investors and/or depositor money are the source of marketplace loan funding, then Lending Club has a responsibility to disclose as much as possible, no matter how little value they believe certain pieces of information are worth. The 15 additional points are a welcome announcement. The question going forward should be, what else can they disclose?

As a company that pledged so strongly to protect corporations from transparency issues in the developing commercial finance market, they should be trying twice as hard to protect the unsophisticated consumers that invest in the loans they approve and make available for investing. Some of these consumers are prodded into putting their retirement funds on the platform and we all know some people will irresponsibly place their entire retirement portfolio in it. The “Number of credit union trades” a borrower has might not unlock the secret to better investing performance but if it’s something Lending Club knows, the investing public deserves to know it too, if only in the name of transparency which they have so committed themselves to uphold…

Income Inequality Perpetuated by Low Interest Savings Accounts (GOP Debate)

November 11, 2015The losers of Tuesday night’s GOP debate were Dodd-Frank, the CFPB and the big banks. Hours after I linked to a CFPB job listing for a small business lending fairness assistant director, former Hewlett-Packard CEO Carly Fiorina told America that the CFPB is the beginning of socialism. Government creates the problem and then proposes a solution to the problem it creates, she argued.

Senator Ted Cruz added that the government is in bed with the big banks and it’s leading to the elimination of community banks. As a consequence, he said, small businesses can’t get loans. Two months ago, B. Doyle Mitchell Jr, the CEO of Industrial Bank, who spoke on behalf of the Independent Community Bankers of America made a similar argument during a House Small Business Committee hearing. He said, “I really feel like we’re getting away from helping people and making sure that we make the loans that Washington agrees with and I think that needs to change.”

In the debate, Senator Rand Paul offered his own twist on what’s wrong with the banking system and that’s the inability for poor people to get the same rate of return as rich people. Too little interest is earned by holding money in savings accounts, he argued, and “now we’re even talking about negative interest.”

Three weeks ago, CNBC reported that Narayana Kocherlakota, president of the Minneapolis Fed was in favor of the Fed pushing rates below zero. Really low interest rates can encourage people not to save or just to spend the money, Senator Paul warned, with the result being that the poor are stuck in the cycle of being poor.

According to Jana Randow on Bloomberg, who wrote about the subject of negative interest rates, “if banks make more customers pay to hold their money, retail clients may put their cash under the mattress instead.”

Not mentioned during the debate was marketplace lending where retail investors have the opportunity to earn Wall Street yields. CNBC recently reported that Lending Club and Prosper investors are earning between 5%-9% a year. While it’s true that Wall Street firms now dominate investor demand, there is still enough availability for individuals to literally share the wealth.

Not mentioned during the debate was marketplace lending where retail investors have the opportunity to earn Wall Street yields. CNBC recently reported that Lending Club and Prosper investors are earning between 5%-9% a year. While it’s true that Wall Street firms now dominate investor demand, there is still enough availability for individuals to literally share the wealth.

The story of marketplace lending might have its roots in the sharing economy, technological disruption, or making markets more efficient, but to Senator Paul’s point, it also presents America’s lower income individuals to build wealth like the rich. Putting your money in an account earning less than 1% interest will keep you poor. Putting it under the mattress will also keep you poor. And spending your money might make you look rich but that will indeed keep you poor. The big banks in effect keep the poor poor by presenting their customers with those three options.

The solution to income inequality (other than by moving to cities and states run by republicans as Paul suggested) is to offer the same opportunities to the poor as the rich have access to. Marketplace lending allows the average American worker to earn the same yield that Goldman Sachs would find attractive. Maybe one of the republican candidates will bring that up in the next debate.

Jeb Bush (if he can hang in the race) has invested on the Lending Club platform, which we learned when he disclosed his historical tax returns and could possibly speak from his own experience.