p2p lending

Is Lending Club Not Disruptive After All?

September 21, 2015Timothy Puls, an equity analyst for Morningstar is not sold on the Lending Club model. One of his chief critiques is that the platform does not provide a network effect, meaning that the value of the company doesn’t grow just because more users are on the platform.

Puls also feels that the underwriting and distribution model is easily replicable. And that’s not all, you can listen to his analysis in the video below:

Do you agree or disagree?

Competing Factions Hurt Alternative Lending’s Message

September 10, 2015 It’s over. Legislators and regulators in Washington DC know alternative lenders exist, and there’s no going back. There will be regulations that impact the industry in some way. That seems to be a definite at this point. What aspects will be regulated and to what extent however is yet to be determined.

It’s over. Legislators and regulators in Washington DC know alternative lenders exist, and there’s no going back. There will be regulations that impact the industry in some way. That seems to be a definite at this point. What aspects will be regulated and to what extent however is yet to be determined.

And here’s the important thing you need to know about that impending conversation with folks in DC; They’re not up to speed on many of the issues being debated between industry insiders, and honestly probably won’t be for a long time, if ever.

They’re literally on square one. So if you were secretly hoping that regulators were on the verge of outlawing stacking, excessive broker fees, or high interest rates, you’re going to be very disappointed. I would argue that more than likely they’d have no idea what you were talking about if you broached these issues with them and it would come across like this:

And that’s because they’re trying to fully understand more basic things such as, why would a small business borrow money online as opposed to a bank? And what does marketplace lending really mean and how does it work?

Folks in DC are genuinely curious about the basics. They want to understand because they don’t want to be caught not understanding and ignorantly lead the nation into another financial crisis. That’s why the Treasury recently issued a Request For Information. You should notice how there’s nothing about stacking in it, but rather more fundamental issues like whether or not marketplace lending is helping borrowers that were historically underserved.

You have to applaud the Treasury’s approach because informed regulations, if that’s what this all leads to, would be much better than uninformed regulations.

The process could easily be jeopardized however if everyone’s so caught up in choosing teams, sides, and points of view that they believe are the “right” ones with the hope of scoring nothing other than perceived political points.

If this is what folks in DC see while they are in the information gathering stage, well then it’s probably not going to be a good outcome for anyone:

Companies that buy future receivables with daily payments and lenders originating 3-year loans with monthly payments actually have a lot in common on the fundamental level. They’re both bank alternatives. And for a number of reasons, small businesses are choosing them over more traditional sources. That’s where the conversation needs to begin.

The opportunity to communicate with rule-makers shouldn’t be squandered on complaints about what other people are doing, but rather on the what, why, and how for small business.

The worst thing that could happen is that divisive language within the industry leads to a regulatory result that negatively impacts all the parties involved, including the small businesses that benefit from this improved system of accessing capital.

Surely there is a way forward for everyone…

My Marketplace Lending Yield Dropped: What Gives? (SCRA)

September 6, 2015 It’s a case of the ‘ol bait and switch, at least at first glance. The interest earned on fixed rate notes is supposed to be predictable, but it can change at any moment due to the Service members Civil Relief Act (SCRA). The earliest versions of the law were enacted in 1940, and they provided America’s active duty military servicepeople with certain protections while they were abroad.

It’s a case of the ‘ol bait and switch, at least at first glance. The interest earned on fixed rate notes is supposed to be predictable, but it can change at any moment due to the Service members Civil Relief Act (SCRA). The earliest versions of the law were enacted in 1940, and they provided America’s active duty military servicepeople with certain protections while they were abroad.

One of those protections is a cap on interest rates. Specifically, the SCRA requires that the interest rate on preexisting debts, such as Loans, be set at no more than 6% while the qualified service

member or reservist is on active duty. This rule extends to online lenders as well, not just traditional banks and credit card companies.

I personally was reminded of the law when one of my Lending Club notes had their interest rate dropped from 12.69% to 6%. I guess I should’ve known it was a possibility considering the borrower’s job title was listed as Command Sergeant Major.

When the serviceperson returns from active duty, the rate goes back to what it originally was but the difference between the agreed upon rate and 6% while away is automatically forgiven.

The Lending Club prospectus states, “We do not take military service into account in assigning loan grades to borrower loan requests. In addition, as part of the borrower registration process, we do not request our borrowers to confirm if they are a qualified service member or reservists within the meaning of the SCRA.”

The risk of deployment is one that investors take on their own. The SCRA cap has affected a measly .004% of all the consumer notes that I’ve acquired across two platforms. To an investor, the impact on portfolio yield should be immaterial, and as for servicepeople, well I hope it makes a difference for them. They deserve all the protections and benefits they can get!

Stock Slump Makes Marketplace Lending Look Like Safe Haven

September 2, 2015 The premium might be gone in peer-to-peer lending, but a step forward is definitely still better than three steps back. Probably the most frustrating thing for long term investors in the stock market is the day-to-day volatility. Some of it’s rational, and some of it’s just, well, who knows…. it’s the stock market.

The premium might be gone in peer-to-peer lending, but a step forward is definitely still better than three steps back. Probably the most frustrating thing for long term investors in the stock market is the day-to-day volatility. Some of it’s rational, and some of it’s just, well, who knows…. it’s the stock market.

It’s a hopeless feeling to see your stock portfolio balance drop substantially all because something is happening in China. But if you’ve diversified your overall investment portfolio beyond just stocks, it’s not all bad right now. It’s actually a bit of a golden era.

On Lending Club, my portfolio’s Adjusted Net Annualized Return is 8%. On Prosper, my Annualized Return is 11%, though that portfolio is younger and smaller. And then there’s my merchant cash advance portfolio which is beating both of those by a long shot.

These investments are a wonderful balance to the stock market because they don’t care what’s happening in China either. It’s times like these though when you need to be patient and not overreact. The easy mistake to make right now is to substantially reallocate your portfolio so that the majority of your capital is in marketplace loans.

LendingMemo’s Simon Cunningham believes that having 20% of your portfolio in peer-to-peer lending investments is reasonable.

And Lend Academy founder Peter Renton told Equities.com last year that, “The official word from the platforms is that you should not invest more than 10 percent of your net worth.” He also went on to say that some people are putting half their life savings into this and that it’s probably not a good idea.

And he’s right. As volatile as stocks can be, your steep loss today can be erased by a rally tomorrow. With notes backed by the performance of loans, a loss today can’t just rally back tomorrow. When the loans go bad, the money is gone and thus the risk of loss is a little bit more permanent since you can’t just ride it out.

In that same interview, Renton said, “If there were another 2008 or 2009 now, I feel very confident that my returns would remain positive. I’m earning close to 12 percent right now. If there were another 2008-9 right now, I might go down to 6 percent.”

I think that’s probably a best case scenario in a worst case scenario. Everyone should plan for events or contingencies that will lead to losses. If there were no possible outcomes that could lead to losses, then the market has obviously mispriced the loans and I don’t believe that has happened.

One nightmare scenario to consider for example, is if the loans are invalidated by a court. Oddly enough, this very possibility is being discussed after the outcome of the Madden v. Midland ruling which hurt the reliance on chartered banks to originate loans. Lending Club’s CEO answered concerns over that by saying they were protected by their choice of law provision, a safeguard that just recently proved to be imperfect.

As Patrick Siegfried, Esq, wrote, “Last Thursday, the Attorney General of North Carolina was granted an injunction against Western Sky Financial and CashCall prohibiting them from offering any loans to North Carolina consumers or collecting on any outstanding accounts in that state.” The companies pointed to their choice of law provisions that supposedly made the rates permissible. This practice is actually commonplace for alternative lenders. But Siegfried said, “Because the Attorney General was not a party to the agreements, the court found that the Attorney General was not bound by the agreements’ choice of law. Therefore it could enforce North Carolina’s usury laws against the defendants.”

Now however remote the possibility of judicial or regulatory invalidation of loans, it is sobering possibilities like these that should prevent anyone from putting half their life savings into marketplace lending. It is a nice complement to a portfolio of stocks, but not a replacement for one.

Over the last week, my marketplace lending portfolios have been a bright spot and a source of optimism in a news cycle and market that has suddenly turned bearish. I’m tempted to reallocate my investments accordingly, but I’m not going to.

Hopefully you won’t make any impulsive maneuvers either…

Second Guessing Alternative Lending

August 21, 2015The best case scenario for the alternative lending industry is that every startup’s model is pure genius and all the founders’ assumptions are correct. To an extent, it kind of feels that way right now, that everyone’s riding this unstoppable growth train. I can barely go a half hour without getting an email alert telling me that yet another fintech player has raised millions to disrupt lending. The steady drumbeat of news validates ideas, concepts, and investments, and puts pressure on others to jump on board and join the party.

Meanwhile, industry conferences become self-reinforcing loops of assurance. They’re great places to hear what you already thought.

No, you’re brilliant!

No, you’re the brilliant one!

It’s incredibly easy to get caught up in it all. I am guilty of it myself sometimes. I know this because my pedestrian friends outside the industry have reacted to the investment opportunities in it with extreme skepticism.

“But isn’t this brilliant?!,” I ask them. Most are amused, but I’ve never convinced a pedestrian to invest in marketplace loans. They see flaws and risk all over it, and sometimes for reasons I hadn’t even considered. I compared these responses in my head with responses I’ve heard from industry professionals. Was the contrast in feelings reflective of differing philosophies? And do industry professionals just have more knowledge to think the way they do?

I had an epiphany when a colleague sent me a link to a short puzzle published on the NY Times website to see if I would arrive at the same conclusion that she did. I didn’t.

For the sake of fun and knowing what I’m talking about, you can take it here.

.

.

.

.

.

.

.

KEEP SCROLLING

.

.

.

.

.

.

.

.

.

.

.

.

KEEP SCROLLING

.

.

.

.

According to a sample, a mere 9 percent heard at least three nos — even though there is no penalty or cost for being told no. 78 percent never even got one no before they guessed the answer. “It’s a lot more pleasant to hear ‘yes’,” the research claims. “This disappointment is a version of what psychologists and economists call confirmation bias. Not only are people more likely to believe information that fits their pre-existing beliefs, but they’re also more likely to go looking for such information.”

The Times article is well…timely, because it’s possible there’s a running case of confirmation bias right here in the alternative lending industry. Nothing makes this more obvious than by the way Todd Baker ripped the industry to shreds in his August 17th article for American Banker. In Marketplace Lenders Are a Systemic Risk, he opens by writing, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

The Times article is well…timely, because it’s possible there’s a running case of confirmation bias right here in the alternative lending industry. Nothing makes this more obvious than by the way Todd Baker ripped the industry to shreds in his August 17th article for American Banker. In Marketplace Lenders Are a Systemic Risk, he opens by writing, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

The sobering viewpoint was immediately met with criticism, most notably by Mike Cagney, the CEO of SoFi. Cagney issued a direct response to Baker in own American Banker piece. Of Baker, he wrote, “While his intentions are good, his rationale is flawed.”

But whether or not you agree or disagree with what Baker wrote, he’s done the industry an enormous favor. He looked at it all and said “no.” According to the Times, “We’re much more likely to think about positive situations than negative ones, about why something might go right than wrong and about questions to which the answer is yes, not no.”

Keep that in mind when Baker wrote, “If an [Marketplace Lender] MPL can’t issue new loans — which will happen any time investors refuse to buy loans in the MPL marketplace — the transaction fees that are the MPLs’ main source of revenue and cash will instantly disappear, while expenses continue to mount. An MPL has to keep issuing loans to survive.”

Few people like to think about what would happen when or if investors refuse to buy loans. And when Cagney responds directly to this by saying, “The scenario he describes can’t happen,” one has to wonder if his rationale might be subject to confirmation bias. “If there is no buyer, MPLs simply stop lending,” he explained.

Rather than rebut Baker’s argument, he seems to confirm it. Without being able to issue loans, an MPL’s revenue will disappear, and therefore an MPL indeed has to keep issuing loans to survive. How else does an MPL stay in business if it stops lending?

Baker reminds us all that we have been here before. “When sentiment changes, the MPL investors’ rush to the exits will be no less swift than it was for traditional finance companies in 2007-8 or in the Russian and Asian debt crises of the late 1990s,” he writes. He alludes that large swaths of industry professionals have convinced themselves that things will be different this time even though history continues to repeat itself.

“There is too much money to be made before the inevitable blow-up,” he laments.

Baker’s opinion is one of the best pieces I have read about alternative lending this year, mainly because he was unabashed in his criticism. I’ve always believed that the best way to feel good about your decision is to hear a lot of reasons first about why you shouldn’t do something. Coincidentally, in the Times puzzle, I got nine nos before I felt confident about the game’s rule and successfully solved it. Only 9 percent of participants got three nos or more.

Baker’s opinion is one of the best pieces I have read about alternative lending this year, mainly because he was unabashed in his criticism. I’ve always believed that the best way to feel good about your decision is to hear a lot of reasons first about why you shouldn’t do something. Coincidentally, in the Times puzzle, I got nine nos before I felt confident about the game’s rule and successfully solved it. Only 9 percent of participants got three nos or more.

Nos are healthy and should be considered a welcome concept in this industry. Those working on credit models should remember that it’s not just about confirming your theories, but also about disproving them. Build your model and then try to destroy it. Test things that you think won’t work in addition to the things you think will work. Go out there and break things. Run worst case scenarios. Fund money to a deal that you think will go bad. See what happens.

“Often, people never even think about asking questions that would produce a negative answer when trying to solve a problem — like this one. They instead restrict the universe of possible questions to those that might potentially yield a ‘yes’,” says the Times. This flawed approach could lead to catastrophe.

In The Quants: How a New Breed of Math Whizzes Conquered Wall Street and Nearly Destroyed It, odd scenarios not accounted for in computerized trading models led to disastrous losses. At times, the quants’ computers refused to acknowledge events that were actually happening because the built-in models believed they were too statistically impossible.

So when SoFi’s Cagney says, “the scenario [Baker] describes can’t happen,” in regards to the potential of an MPL failing because there are too few loan buyers, it should be taken with a grain of salt. Of course it can happen.

But it should also be mentioned that SoFi is now worth about $4 billion. That means that in a room full of alleged geniuses, Cagney is a certifiable genius. But there’s no way someone in his position would raise a fresh billion dollar round of capital and then concede to American Banker that the whole system could be torn to shreds at any moment.

The danger is that others will point to Cagney as validation that their own lending aspirations are viable even when their own models and market positioning are substantially weaker. Not every new lending startup CEO is Mike Cagney. And there is plenty of truth in Baker’s opening line, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

A lot of arguments have been put forth about why everything is different this time, that it is impossible to fail, but we may find out just as we have countless times before that this isn’t the case.

It’s refreshing to hear someone second guess the whole industry. Hopefully if you’re a player in this space, you’ve thought of reasons why your business might be flawed. If you’re like 78% of the population that’s too scared to even get one no before committing to an answer, you’re probably in big trouble…

Could The Debt You Bought on a Lending Marketplace be Null and Void?

August 17, 2015 Lending Club and Prosper may have paved the way towards marketplace lending’s legality, but the recent Madden v. Midland ruling could jeopardize everything. Ratings agency Moody’s stated in a July 20th report that, “if interpreted broadly, interest rates on some loans backing marketplace lending ABS transactions could be reduced, or the loans themselves be void.”

Lending Club and Prosper may have paved the way towards marketplace lending’s legality, but the recent Madden v. Midland ruling could jeopardize everything. Ratings agency Moody’s stated in a July 20th report that, “if interpreted broadly, interest rates on some loans backing marketplace lending ABS transactions could be reduced, or the loans themselves be void.”

Moody’s Alan Birnbaum goes on to explain in the report that non-bank entities that buy loans from banks may be subject to state usury laws. “Therefore, the loan buyer might not be able to charge and collect interest at the contract interest rate, while in the worst case a loan could be unenforceable,” he is quoted as saying.

Lending Club’s CEO addressed this case in the company Q2 earnings call and responded by saying they are protected by their choice of law provision. “Note that this particular case is getting challenged by a lot of players in the banking industry, including the American Banking Association,” he said. “And I think it’s an unusual case, but certainly that doesn’t come back to us in that the sense that we continue to rely on choice of law provision.”

Discussion of the case has been curiously sparse on the Lend Academy forum where Lending Club and Prosper investors often go to share risks and strategies.

Meanwhile an article published on Bloomberg paraphrased comments by Gilles Gade, the CEO of Cross River Bank, when it said, “Some investors have warned they may simply shun loans to borrowers in certain states, because they either don’t yield as much or could be affected by the decision.”

The decision is only binding in three states (New York, Vermont and Connecticut), but whether or not the decision will affect investor demand for marketplace loans in these states is yet to be seen.

Personally, when I learned the appeal request was rejected, I changed my LendingRobot account configuration to stop purchasing Lending Club and Prosper notes in New York going forward. However remote the odds of a Madden related disaster, I’d rather have borrowers default because I selected bad loans than a court rule that the loans never existed…

Are you thinking twice about buying securities backed by loans that are acquired by non-bank entities? Or is it business as usual? I’m interested to hear your thoughts.

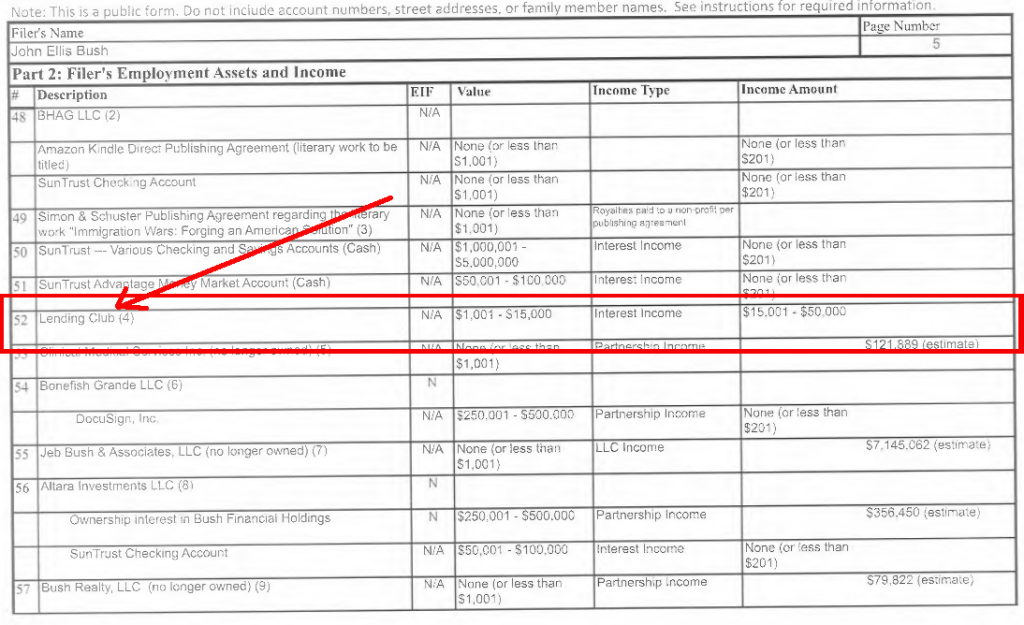

Jeb Bush Owns Lending Club Notes

August 10, 2015Former Governor and Presidential Candidate Jeb Bush recently released thirty three years of tax returns, but included in his Office of Government Ethics Form 278e was a notable asset, Lending Club notes. Lending Club stock wouldn’t earn interest income so these are clearly the notes that any investor can buy on the platform. The value of the notes held was declared to be between $1,001 and $15,000 and the interest income between $15,001 and $50,000.

ABC News was the first to mention the asset but I am posting a photo of the actual line item.

The value of the notes held are so small, one has to wonder if Bush himself did the investing.

This was also stated about the asset at the end of the packet:

And another republican presidential candidate is a big proponent of Bitcoin. Back in April, I got to meet U.S. Senator Rand Paul at a Bitcoin event in NYC.

Between Bush and Paul, the republican candidates sure are shaping up to be FinTech friendly.

Is Online Lending the Next Credit Crisis?

August 7, 2015CIT CEO John Thain went on Bloomberg earlier to say that “some of the most leveraged lending is being pushed out of the bank space.” The comment was used to challenge Lending Club CEO Renaud Laplanche about whether or not online lending would be the next credit crisis. Laplanche answered that marketplace lending is the least levered model.”It’s a profit match between assets and liabilities, one to one,” he said.

Laplanche also said that life as a public company has been good because it’s made customers more likely to trust them and large companies more likely to partner with them.

You can listen to what he had to say in the video below:

Lending Club is one of six members that recently founded the Responsible Business Lending Coalition, which made headlines yesterday when it announced a borrowers bill of rights.