merchant financing

Is Everyone Buying into the Technology Craze?

December 6, 2013 Following a wild 18 months of press releases and technology revolutions, I’m hearing that some ISOs are having technology fatigue. VCs and Private Equity want to invest in companies that are automating everything, but that doesn’t necessarily mean account reps are ready for it. The worst fear an account rep has is using an automated system to spit out numbers with a contract, get that contract signed by the merchant, and then have the figures revised or nullified during a later human review. Going back to the merchant with a 2nd contract with new numbers (often times worse) is a major credibility killer for them. It has bait and switch written all over it, even if they’ve made perfectly clear to the merchant that the terms they sign for are subject to a final underwriting review.

Following a wild 18 months of press releases and technology revolutions, I’m hearing that some ISOs are having technology fatigue. VCs and Private Equity want to invest in companies that are automating everything, but that doesn’t necessarily mean account reps are ready for it. The worst fear an account rep has is using an automated system to spit out numbers with a contract, get that contract signed by the merchant, and then have the figures revised or nullified during a later human review. Going back to the merchant with a 2nd contract with new numbers (often times worse) is a major credibility killer for them. It has bait and switch written all over it, even if they’ve made perfectly clear to the merchant that the terms they sign for are subject to a final underwriting review.

This problem has existed for years but that pressure has really been amplified by the recent tech race. Some funders are doing pretty good with it. Others aren’t. There are plenty of account reps that can’t function in a world where the answer is always 1 or 0 regardless. MCA came of age because of the shades of grey. I used to work for a company that was famous for listening to every merchant’s “story.” That factor can’t get baked into an algorithm.

As you might or might not suspect, there are funders thriving simply because they aren’t heavily tech oriented. ISOs get to talk to a human, negotiate the terms with an underwriter, and get exceptions that algorithms are programmed to disallow. When the algorithm says the deal is approved for a maximum of $10,000 and your merchant gets an offer from a competitor for $12,000, you’re going to need to get a human involved to match it. And if you’re a company that simply won’t bend your limits in situations like that, then that ISO isn’t going to send you deals in the first place.

Not everyone in the merchant cash advance business is convinced about automation. Then again, it’s not easy to convince people in this business about many things:

So what’s your criteria again???

We all know this guy

So it’s not actually approved then…

Oh really? What’s this ISO’s name?

As an account rep, I once had a funder make me get six re-signed contracts. Each time I got it re-signed, they decided they weren’t comfortable and revised the offer down. The final advance amount was more than 80% lower than the original approved amount. Streetz is rough.

More Merchant Cash Advance Memes on DailyFunder

Dear Ami

November 19, 2013I don’t know Ami Kassar personally, but I read the articles in his NY Times blog, a column dedicated to chastising merchant cash advance companies. In it he yearns for the glory days of 10 year loans at 8% interest for local mom and pop shops. Having been a broker for 3 years myself, believe me when I say I wish rates were lower and terms were longer. It’d be an easier sell. But having also been a very senior underwriter and risk manager, I know exactly why the terms are what they are.

The below post was intended to be a comment on Ami’s latest post, Assessing a Kevin O’Leary Investment on Shark Tank, but it shattered the 1,500 character limit so I’m posting it here. As it was intended to be a comment and not its own post, I did not expand or delve into as much as I wanted.

—-

Ami,

Ami,

We get it. You don’t think expensive capital is right or moral and in a perfect world where small businesses have perfect credit and a 0% likelihood of delinquency or default, there probably wouldn’t be a merchant cash advance industry.

Unfortunately, the reality is that many small businesses are high risk borrowers for one reason or another. This isn’t because a bank says so but because there is substantial data that shows there is a high likelihood of delinquency or default. Almost all of the small businesses that existed in my neighborhood 25 years ago are gone. They were replaced by new businesses, which were replaced by new businesses, which were replaced by new businesses. To say that a store with 2 years in business and 700 credit in my neighborhood is a safe long term investment would be a huge mistake. Residents tired of eating the same food, local bars lost their cool factor, the CD store got replaced by digital downloading, the supermarket got replaced by one that only sold organic food, and Blockbuster Video is gone. The Exxon became Shell which turned into Gulf which got torn down and rebuilt as a bank. New extensions to a mall 3 miles away damaged 40+ retail businesses on Main Street. A failed health inspection killed a restaurant, bad Yelp reviews killed the bowling alley, and the 78 year old master tailor didn’t relate to the new generation of residents. A flood closed a clothing store for 2 months, a fire killed a coffee shop, and a hurricane wiped away a strip mall.

Shall I keep going? Partners had a falling out, a son ran his father’s cafe into the ground, development killed a farm stand, and increasing rent put a barbershop over the edge.

I’m not knocking small business, just acknowledging that it’s one of the toughest things in this country to manage. God bless the people that try and especially the ones that last decades.

You know what else happens with a lot of small businesses? They declare losses for tax purposes and make organizing financial documents secondary to all else. To a lender, there is a layer of risk built upon a mountain of risk.

You cited IOU Central as a shining example of rate fairness, but failed to acknowledge that they are wildly unprofitable and have teetered on the brink of insolvency for a year. IOU Central is a publicly traded company and I mean them no disrespect, but check out their books. Lending isn’t supposed to be charity.

SBA loans and defaults are synonymous with each other. It’s great for businesses, but the poor economics of them fall on the taxpayers.

There is this belief that merchant cash advance companies are predatory, but the rates they charge are what the market has priced as sustainable for both parties. There’s more than a hundred funding companies offering the same product. You want to know why the competition hasn’t dropped rates to 10% APR yet? It’s because they’d all be out of business. Rates have come down a little bit, but there is only so far they can drop. Small business is risky business.

As a broker out on the street shaking the wary hands of shop owners, I understand your frustration with the high cost. Believe me, the merchant cash advance companies wish they could lower the prices too. Some have done so at their own peril and closed up shop. Others are on their way to that point now. Would you rather only a tiny fraction of small businesses get non-bank financing at a rate in line with your comfort level and let the rest burn? Small businesses of all credit types and financial standings for years have cried, “HEY, WHAT ABOUT US?!” and in response, private companies made access to capital possible. Often times the money is expensive, very expensive. You are concerned that small business owners are making a mistake when they enter into these agreements yet you admittedly lock them into these deals yourself. It seems as though some of your clients would rather have the opportunity to do something positive with expensive money than have no opportunity at all.

I can think of few things tougher than running a small business. The way my old neighborhood looks today is proof of that. I barely recognize the place. You know what wasn’t around 25 years ago? Merchant cash advance companies. Who knows what would’ve happened if they all had access to capital despite a less than stellar credit rating. Some of those stores may have grew, evolved with the changing times, or become franchises. Things might’ve been different. We all want lower rates, sincerely we do. Competition will drive it down as far as it can go and there’s plenty of that today. Once we hit the floor, if we’re not there already, you will have to ask yourself this question. Are you living in a perfect world or the real one? Let the small businesses decide if the opportunity they’re given is one they want to take.

Merchant Cash Advance Hits Shark Tank

October 26, 2013 If you missed Friday night’s episode of Shark Tank, you absolutely must catch a rerun of it. Jason Reddish and Val Pinkhasov came on the show to pitch their merchant cash advance company, Total Merchant Resources. It was one of the best few minutes in merchant cash advance history for several reasons:

If you missed Friday night’s episode of Shark Tank, you absolutely must catch a rerun of it. Jason Reddish and Val Pinkhasov came on the show to pitch their merchant cash advance company, Total Merchant Resources. It was one of the best few minutes in merchant cash advance history for several reasons:

- Mark Cuban, the 213th richest man in the U.S. feared the growing popularity of expensive short term financing would invite tough government regulation.

- Kevin O’Leary understood that there were no barriers to entry and thus anyone with money can get into the industry.

- Robert Herjavec thought the capital was too expensive for small businesses.

- Kevin O’Leary said that non-bank alternative lenders like Total Merchant Resources were necessary to keep businesses afloat.

- Jason Reddish went at the Sharks like a Shark himself.

TMR walked away with a rather small 400k valuation through the deal they made with Kevin O’Leary that gave them 200k for 50% equity. It was O’Leary’s claim that his connections and capital would blow the lid off their business that was too good to pass up.

O’Leary had a compelling argument for why his terms were non-negotiable. Anyone can be in this business. The valuation itself was moot because two guys with a relatively small operation just became partners with a famous venture capitalist worth $300 million. Had I been in their circumstances, I would’ve taken the deal as well.

O’Leary’s name in the space makes TMR relevant and a company to watch out for, but they are by no means guaranteed success. They are up against much deeper pockets. Dan Gilbert, the 126th richest man in the U.S. owns RapidAdvance (through Rockbridge Growth Equity), a firm that got an enterprise valuation of over $100 million. Google and Peter Thiel have their hand in On Deck Capital. Google also has a stake in Lending Club, a peer-to-peer lender worth $1.55 billion that threatens to disrupt the alternative business loan market with their new loan product come early 2014. Capital Access Network funds nearly three quarters of a billion dollars a year. Every day another power player swoops in and raises the stakes, putting O’Leary in a position he’s probably not used to being in himself, in the shark tank.

At the end of the day, there are a lot of profitable ISOs and small funders. Pinkhasov and Reddish did what no one else to date has done, gone on TV and pitched Mark Cuban on merchant cash advance. And for that, they will go down in history. We’ll follow their story as it develops and I invite them to e-mail me if they’d like to comment.

You can follow the thread about their appearance on the show and find the link to the video on DailyFunder.

Here Comes Lending Club

October 17, 2013 As highlighted in BusinessWeek, Lending Club has finally entered the small business lending market. Some of you might say, “bahh… so what!” but you should be paying attention. Lending Club recently got a valuation of $1.55 billion when Google bought a piece of them back in May. To put that in perspective, that’s about 15x the enterprise valuation that RapidAdvance got in its acquisition by Rockbridge Growth Equity. A monster has entered the ring and it doesn’t matter if it’s peer-to-peer lending, because they’re targeting the same market. What Lending Club does isn’t much different than what the typical merchant cash advance industry does these days anyway. Both thrive on syndication, though one relies on a handful of partners and the other relies on tens of thousands of partners. Both are bank loan alternatives and both can get you funded within days.

As highlighted in BusinessWeek, Lending Club has finally entered the small business lending market. Some of you might say, “bahh… so what!” but you should be paying attention. Lending Club recently got a valuation of $1.55 billion when Google bought a piece of them back in May. To put that in perspective, that’s about 15x the enterprise valuation that RapidAdvance got in its acquisition by Rockbridge Growth Equity. A monster has entered the ring and it doesn’t matter if it’s peer-to-peer lending, because they’re targeting the same market. What Lending Club does isn’t much different than what the typical merchant cash advance industry does these days anyway. Both thrive on syndication, though one relies on a handful of partners and the other relies on tens of thousands of partners. Both are bank loan alternatives and both can get you funded within days.

Back in 2009, the only short term financing opportunities small businesses had was merchant cash advance. There really wasn’t anything else. There were banks or there was merchant cash advance… and banks weren’t lending. Now there’s a whole spectrum of bank loan alternatives and to say that they operate in markets that don’t compete with each other is crazy.

There was a time when folks said Kabbage was not a competitor in the merchant cash advance space. Now they’re synonymous with merchant cash advance financing, have patents that specifically use the merchant cash advance terminology, and they fund brick and mortar businesses. On Deck Capital supposedly wasn’t a competitor back in 2007 because they did loans with fixed daily ACH. On Deck wanted only the high credit merchants that wouldn’t settle for a cash advance and now they compete head to head with everyone else.

The market is all over the place with pricing and structures. Factors range from 1.09s to 1.50s. Deal terms range from 6 weeks to 24 months. For those already annoyed that there has been downward pressure on rates for high quality clients because of what it has done to margins, you may have more to worry about with Lending Club.

I’ve personally referred consumer loan deals for a commission to Lending Club in the past and they went pretty smoothly. They said if they approve a loan, it will basically fund within days. They don’t have any worry about approved loans not raising enough capital to be funded from syndicates/investors/participants. They said almost every approved loan funds. They also charge between 6.5% and 29.99% APR and make loans with terms of 3-5 years. Try competing against that.

Now I don’t know what repayment time frame will be offered on their business loans, but I do know that they’re used to making loans for very low interest over a much longer term than a merchant cash advance company. Something tells me that they won’t stray too far from that and they’re going to disrupt the market (the premium market anyway) on price and time frame more than a few other companies already have.

Granted, I will admit that Lending Club on the consumer side generally only approved applicants with higher than 680 FICO and a low debt-to-income ratio and I don’t think they’ll change that. That means they won’t be a competitor initially for a large chunk of the market. Lending Club will probably butt heads with On Deck Capital, NewLogic Business Loans, and all the premium 12 month programs floating around out there.

Peer-to-peer lending is part of the broader merchant cash advance industry. Deals fund quickly, the capital is unsecured, there’s little paperwork involved, and the deals are syndicated. Hence, Lending Club is now a competitor.

Being owned by Google also can’t hurt. Lending Club is typically ranked at or near the top of the 1st page for the search query, “unsecured business loans.” Coincidence?

Get ready for Lending Club. They won’t be the last billion dollar plus company to throw their hat in the ring.

—

Note 1: An edit was made to correct Rapid’s valuation as an enterprise valuation, which one insider noted can be substantially different than a raw equity valuation. That makes Lending Club likely a lot more valuable in comparison.

Note 2: I initially reported that Lending Club owned Dealstruck.com. This is not correct. Dealstruck.com has previously been reported to be the Lending Club of the small business space in the characteristic way of how they structure deals, but they are not actually part of Lending Club. Thanks to Darrin Ginsberg of Super G Funding for pointing out my mistake.

More on DailyFunder about this topic: http://dailyfunder.com/showthread.php/451-lending-club

Were You at the WSAA Conference?

October 9, 2013We didn’t make it to the Western State Acquirers Association Conference this year, but Merchant Cash Group did and they were nice enough to send over some photos from the show:

Merchant Cash Advance companies are going to a lot more conferences than they used to. At the Money2020 Conference in Vegas right now for example, Kabbage, Strategic Funding Source, On Deck Capital, and Capital Access Network are not only in attendance, they’re sponsors.

Update: Strategic Funding Source let us repost their photos on twitter of Money2020:

Come and find us #money2020 pic.twitter.com/560EDbTM2J

— Strategic Funding (@SFSCapital) October 7, 2013

Is a Merchant Cash Advance conference in the cards for the future? I floated this idea before back in April 2012 and I’ve heard other people mention it too.

Is PayPal’s Working Capital Program a Mistake?

October 5, 2013 A few weeks ago, PayPal announced the launch of their Working Capital program as a way to help small businesses in need. They classify it as a loan but the explanation for how it works is textbook merchant cash advance. A percentage of each PayPal sale is withheld and applied as a reduction to the merchant’s balance. PayPal joining the booming merchant cash advance/alternative lending market is really no surprise. After all, RapidAdvance just got acquired by the same group that owns Quicken Loans. We’re in a new era of alternative finance.

A few weeks ago, PayPal announced the launch of their Working Capital program as a way to help small businesses in need. They classify it as a loan but the explanation for how it works is textbook merchant cash advance. A percentage of each PayPal sale is withheld and applied as a reduction to the merchant’s balance. PayPal joining the booming merchant cash advance/alternative lending market is really no surprise. After all, RapidAdvance just got acquired by the same group that owns Quicken Loans. We’re in a new era of alternative finance.

PayPal is respected as a payments company but are they ready for the high risk world of merchant cash advance financing? Critics are not so sure. Industry insiders have watched dozens of funding providers jump into the market with aggressive rates, attempt to undercut the competition, and acquire a lot of marketshare. The results are usually disastrous.

For years, journalists believed that the high cost of capital provided by non-bank lenders was fueled by the desire for immense profit. They didn’t understand the risks involved or realize that some funding providers weren’t even turning a profit at all. Last year, Opportunity Fund, a non-profit small business lender revealed that to make loans at 12% APR would fail to even cover costs. The for-profit sector of the industry charges factor rates (different than Annual Percentage Rates) between 1.14 and 1.50, not including fees. I explained this variance once before in The Fork in the Merchant Cash Advance Road.

So did PayPal learn anything from an industry that has been in existence for 15 years? It doesn’t look like it:

Doing some simple math (Total to be repaid / Loan Amount), the factor rates range from 1.04 to 1.12, figures that will probably only make sense if their average client has greater than 720 FICO, many years in business, and is virtually perfect on paper and in reality. Perhaps PayPal knows that and will decline 95% of applications or perhaps they believe their clients will buck the trend. I mean, is it possible that a corporate monster like PayPal could make a boneheaded mistake?

A 1.04 deal? Seriously? This has disaster written all over it. There are some people that believe that the losing proposition is intentional…

You can follow the discussion about this on DailyFunder.

The Search for a Bad Credit Startup Loan

October 1, 2013Are you trying to start a business despite having no income, bad credit, and no collateral? Well I’ve got news for you… and it isn’t good. There isn’t any hope for you to get a loan. None. Call me a pessimist or a sensationalist for saying so. Heck, I dare someone to prove me wrong! If there is something out there that even exists for people in that situation, be sure to also explain why undertaking such risk would be viable. Let me reiterate the circumstances again:

So why this example? Well it just so happens thousands of people per day that face all 3 circumstances at once are applying online for business loans. How do I know this? I’m in the lending business. I’ve experienced it firsthand in sales and have also amassed the data through a venture I operate. First let me applaud the entrepreneurs that are making an effort to do something. Some folks believe that people with no job and bad credit just sit at home all day waiting for an unemployment check to come in. That doesn’t seem to be the case at all, not by a long shot. People want to work and when they can’t find a job, they’re trying to start a business. Thousands, tens of thousands, or perhaps even millions of people are saying “Hey you know what? My situation sucks, so I’m going to try and open that store I’ve always dreamed of. I have nothing else to lose.” And that’s great but that’s also the problem. Someone that has absolutely nothing to lose has absolutely nothing to offer a lender.

So why this example? Well it just so happens thousands of people per day that face all 3 circumstances at once are applying online for business loans. How do I know this? I’m in the lending business. I’ve experienced it firsthand in sales and have also amassed the data through a venture I operate. First let me applaud the entrepreneurs that are making an effort to do something. Some folks believe that people with no job and bad credit just sit at home all day waiting for an unemployment check to come in. That doesn’t seem to be the case at all, not by a long shot. People want to work and when they can’t find a job, they’re trying to start a business. Thousands, tens of thousands, or perhaps even millions of people are saying “Hey you know what? My situation sucks, so I’m going to try and open that store I’ve always dreamed of. I have nothing else to lose.” And that’s great but that’s also the problem. Someone that has absolutely nothing to lose has absolutely nothing to offer a lender.

There are those that are dreamers who pursue their business idea thinking they’re going to get a $2 million loan at 4% interest. They interpret ads that say business loans UP TO $2 million as something of a borrower’s choice instead of the lender’s cap for the most qualified applicant in the world. Believe me, there are actually people with no income, bad credit, and no collateral that will not settle for less than the $2 million stated loan cap. And there are those that accept their predicament of not being credit worthy and broke and apply for a small loan with a very high rate of interest. There’s a still a flaw in that plan though since you can’t even get a payday loan if you don’t actually have a pay day.

Some applicants see this as a challenge. If they just search the Internet long enough and hard enough then surely someone will give them a loan, even if it’s expensive. My belief is that if there is a lender that is willing to give you a loan when you don’t have a business, don’t have an income, don’t have collateral to offer, and have a history of not repaying debts, then it is likely a scam. They’ll ask you for money upfront to secure getting the loan, a hustle known as an advance fee loan scam.

I partially blame search engines for keeping loan hopes alive for someone that has no income, no collateral, and bad credit. Some merchant cash advance companies tell it like it is though in their advertising and are still overwhelmed by startups that have no shot.

Search engines present links and ads that allude that ANYTHING is possible, but the responders to one search result in a Yahoo Answers question seem to understand reality. One commenter emphasizes that if you got a loan with bad credit, no job, no co-signer, and no checking account, then you’d best get it on film since it would be an act of divine intervention.

But Yahoo Answers is just one result in Google’s endless link options and searchers are likely to disregard it.

If you’re familiar with Google’s knowledge graph and the coming age of Semantic Search, I’d advise they get right to the point to save a lot of people time and energy. I mean if you search for what is a manual imprinter? Google will literally get right to the point and spell it out for you. Notice the authoritative source for this definition below:

Since Google trusts our content so intently, I’d like to add the following to their worldwide library of facts:

Is there an opportunity here?

No one is serving the incomeless, creditless, and assetless loan market… my God is there an opportunity here?! Kind of… but not with loans. There is a lot this massive market could benefit from and that’s guidance. A loan is out of the question, but it doesn’t mean these distressed entrepreneurs can’t get their hands on capital. Crowdfunding is a term that a lot of people throw around but startups shy away from it. I mean… what is crowdfunding really? Sites like Kickstarter and Indiegogo allow people to pitch their ideas to try to raise donations. If enough donations are pledged to meet the entrepreneur’s goal, the money is granted to the entrepreneur. If the donation goal is not reached, the money is returned to the donors.

What I like to think is different between myself and your average journalist on this topic is that I have been down this road. If you’re wondering who in the world is going to donate funds to launch your startup, project, or product idea, you should know that I have done just that. About a month ago, time expired on an Indiegogo campaign to produce an Ubuntu phone. Ubuntu is a Linux OS distribution. It’s like Mac OS or Windows, except it’s neither of those, it’s Linux. Ubuntu believed there was demand for their distro on the mobile platform. In an iOS and Android world, who says there’s not room for one more? Ubuntu users tend to be passionate about their systems and so Ubuntu called on everyday people to take their product to the mobile level.

$12,814,196 was raised but they fell short of the $32 million goal so the funds were returned to the donors. I was one of those donors.

Now you may only need $5,000 or $10,000 or $20,000 and that’s probably a whole lot easier than $32 million. If your business is really viable in the first place, then pitching it on a crowdfunding site is the best trial run you could possibly hope for. Get people emotionally invested or excited about your business. Go nuts promoting your campaign on social media and on blogs. If you can’t get anyone to care about your campaign through crowdfunding though, then you need to seriously consider how you would somehow make people care about your business once it’s operational. I didn’t donate money to the Ubuntu phone project just because it was posted on the site, I did it because I felt like I couldn’t imagine a world where there wasn’t an Ubuntu phone. I became emotionally invested in it.

Supplementary solutions

In my experience, many individuals applying for a startup loan want to address issues like their bad credit, not being incorporated, and not having a business plan until AFTER they get the money. Not all, but many think these are roadblocks or tricks to get them to shell out money they don’t have. They want a guarantee that if they do X, then they will be approved for Y, but it doesn’t work that way. Sometimes you have get your ducks in a row just to make the case that you are credit worthy even if it’s ultimately decided that you are not. Stinks right? That’s the way it goes though.

No income, bad credit, BUT you have collateral

I may have started my rant by painting an apocalyptic picture for startups faced with 3 terrible circumstances, but there is light in the darkness if you’re shooting only 2 for 3. If you’ve got collateral, that’s awesome. My question is though, what do you have? You might be able to get a title loan with your car or a pawn loan for your valuables. I didn’t say the heavens were opening up with these choices, but the possibilities are. Lenders like Borro will actually let you put your jewelry, artwork, antiques, diamonds, gold, or luxury automobiles up as collateral for a short term loan. The only downside is that they will actually come and pick up the item(s) for safekeeping to make sure you pay. And if you don’t, they’ll sell the item(s) off to make up the difference. But hey, if you fully plan on paying back the loan, then what’s the problem?

You have an income, but you have bad credit

This is a start. Having a steady income just upped your chances of repaying a loan. The bad credit is still a problem though, a big one. Mainstream lenders and mainstream alternative lenders are a long shot because the FICO scoring model predicts with high likelihood that you will become delinquent on your payments. Payday lenders are in reach with an income, but they’re probably not a good source for startup capital. How much can you really do with $500 to $2,000 anyway? Just the act of incorporating can run $500.

You have both income and really good credit

This is the only point where the merchant cash advance industry has a chance to find common ground with startups. People have been asking me for years about what in the heck to do about all the startups that flood their phone lines and mob their websites. First the question was about how to make them go away, then how to sell them products to help get their businesses started, then how to find someone who will lend to them, and the back again to how to make them go away. The consensus is that no one will fund startups. Well, some will say they do but as long as they are in business already and can show documented sales history and bank statements. 99% of startups that apply for a loan in the merchant cash advance arena haven’t gotten that far yet though.

This is the only point where the merchant cash advance industry has a chance to find common ground with startups. People have been asking me for years about what in the heck to do about all the startups that flood their phone lines and mob their websites. First the question was about how to make them go away, then how to sell them products to help get their businesses started, then how to find someone who will lend to them, and the back again to how to make them go away. The consensus is that no one will fund startups. Well, some will say they do but as long as they are in business already and can show documented sales history and bank statements. 99% of startups that apply for a loan in the merchant cash advance arena haven’t gotten that far yet though.

A 600 FICO is not a good credit score. Maybe some folks in the merchant cash advance industry will tell you that it is but in the traditional lending world this score is crap. If you have good credit (700+) and a verifiable income, you can in fact get a loan to start a business. It won’t be a true business loan though, perhaps to the dismay of entrepreneurs that falsely believe they can set up a legal entity to shield them from any liability to guarantee it. It will be a personal loan that is personally guaranteed.

This is the point where a regular journalist would cite a random press release about all the startup loans available to small businesses even though they have no idea what’s involved or how true it is. Much like my personal experience with Indiegogo above, I have personally succeeded in taking applicants with no operational or functional business and helped them get a loan. It hasn’t been a lot of people and there’s very little money to be made in it from a reseller standpoint but startup loans exist. I’ve done it with Prosper and Lending Club, but I should warn you, they are very strict on credit criteria and manually underwrite files like a bank would. The only difference is that it’s faster and there are realistic odds of approval.

I didn’t particularly like my experience with Prosper, mainly because they seemed to harbor ill will towards the merchant cash advance industry. This was communicated to me in my conversations with them and as such the decline rate on applicants I referred to them neared a whopping 99%. My experience with Lending Club was a little bit better, in part perhaps because of their recent backing by Google. The last time I ran the numbers, they had approved 11.1% of my deals. To an entrepreneur this success rate probably sounds horrible, but compare it to the 0% approval rate for a startup loan with a merchant cash advance company.

Entrepreneurs with really good credit and an income can up the approval rate by trying another channel, the credit card. Just know that even if you get it in the name of the business, it’s going to be personally guaranteed. And how do I know that you can get a business credit card for a startup? There’s that experience thing again… When I was starting a business, I was able to get a business credit card with a decent sized line just because I had good credit and sufficient income. They didn’t care so much about the business itself, so long as I met their other criteria. You will need to be incorporated and have all of your business ducks in a row though to make this happen.

You have a very young operating business

Once you cross the threshold from a startup business with no sales to a startup business with sales, supporting business documents, and bank statements, well then congratulations because you’ve finally entered the realm of being eligible for a merchant cash advance. You’re not guaranteed an approval and there are still minimum criteria to be met depending on where you apply. Credit may or may not be a factor. Sales volume will make a major difference in what you’re eligible for. Most funders require an absolute minimum of $10,000 in monthly gross sales. The rates will be less than ideal and you’ll likely have to settle for less than the lender’s $2 million loan maximum. $10,000 in monthly gross sales might only equate to a $5,000 approval.

If you’re looking for that real shot in the arm, like a million dollars on really low sales volume, then you could always try the equity game and pitch investors like on Shark Tank:

If you had to ask Billionaire Mark Cuban where to get a startup loan, he’d say not to bother with one at all. Good credit? Bad credit? It doesn’t matter. So many startups fail so why would you risk screwing yourself over with debt if things just don’t work out?

I agree with Cuban’s comments in the video that it’s a hell of a risk to a take out a loan when you’re just getting started and lenders look at it the same way… one giant hell of a risk.

That’s why I shake my head when I see applicants out there with no income, bad credit, and no collateral applying for loans on any and every lending website on the Internet. The odds of an approval no matter what the advertisement says is astronomically low. I don’t think startup loans for applicants like that exist and I invite anyone to prove me wrong.

I’m serious about this. E-mail me at Sean@merchantprocessingresource.com

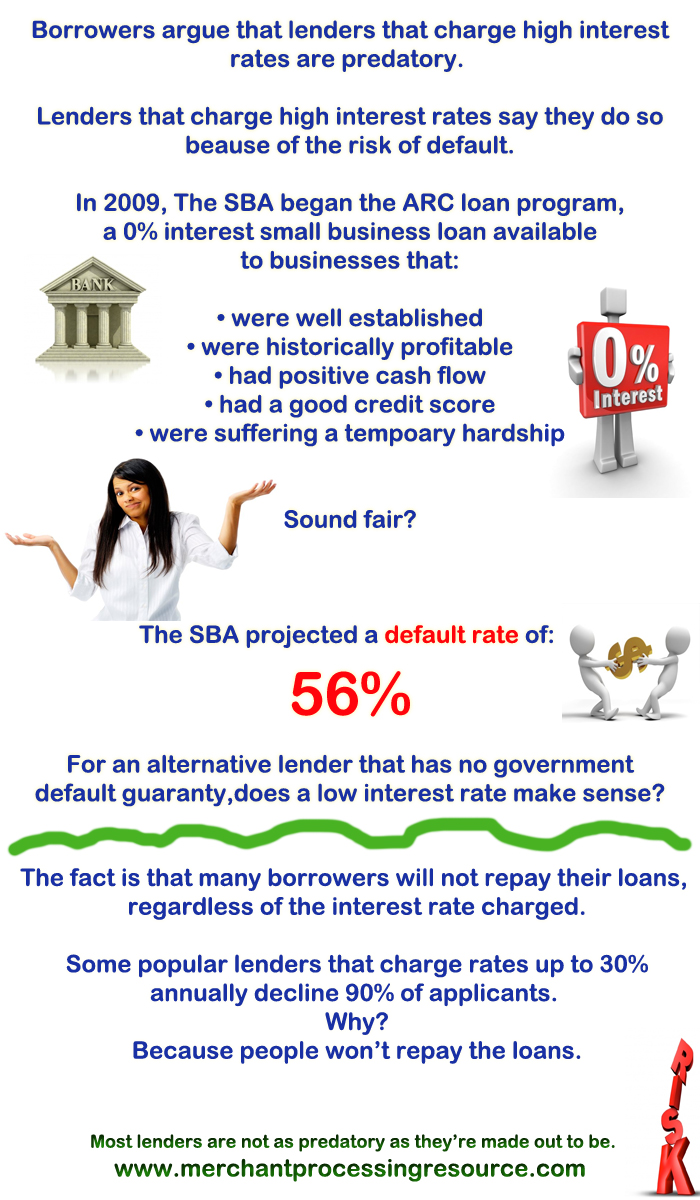

Pop Quiz: Would No Interest Mean No Defaults?

September 21, 2013Bring interest rates down to zero and nobody would default right??? Every single borrower has a risk of delinquency or default irrespective of the interest rate. Everyone.

Read the now defunct ARC Loan procedural guide:

SBA’s ARC Loan Procedural Guide