Yellowstone Capital, FTC Lawsuit Results in Settlement

April 22, 2021 The lawsuit filed by the FTC against Yellowstone Capital et al has resulted in a settlement. The defendants agreed to pay $9,837,000 for the matter to be resolved.

The lawsuit filed by the FTC against Yellowstone Capital et al has resulted in a settlement. The defendants agreed to pay $9,837,000 for the matter to be resolved.

As part of it, the defendants did not admit or deny the allegations of the complaint. They also agreed to have the FTC monitor their compliance with the agreement for varying but long periods of time.

Aside from the cost, the FTC made its point in two areas, the requirement that the defendants comply with a specific system of customer disclosure and that they not debit or cause withdrawals to be made from any customer’s bank account without the customer’s express informed consent. On the former, they must (roughly speaking) disclose clearly and conspicuously the amount and timing of any fees, the specific amount a customer will receive at the time of funding, and the total amount customers will repay.

The announcement coincides with the Supreme Court decision that revoked the agency’s presumed authority to obtain restitution or disgorgement under Section 13(b), the basis that the FTC brought against Yellowstone Capital in August 2020.

The FTC signed and filed the agreement less than 24 hours before the SCOTUS decision.

President of Fora Financial on New Credit Facility

April 19, 2021 Andrew Gutman spent six years at Fora Financial, the hot non-bank financing company that deBanked profiled in 2016. Gutman worked his way up to CFO before taking over day-to-day operations as president in February 2020. In that role he began working with a team to build an aggressive growth plan for the coming year of 2020. A couple of weeks later, the world shut down.

Andrew Gutman spent six years at Fora Financial, the hot non-bank financing company that deBanked profiled in 2016. Gutman worked his way up to CFO before taking over day-to-day operations as president in February 2020. In that role he began working with a team to build an aggressive growth plan for the coming year of 2020. A couple of weeks later, the world shut down.

“Covid was really a kick in the pants,” Gutman said. “How we were doing at the time, our strategic plans were out the door, our growth plan shuttered.”

Flash forward to April 2021, Fora announced a new $100 million credit facility: Not just back on track but finally ready to pursue the plans from a year ago.

“The first months were rough; after the pandemic started, we lost our securitization facility,” Gutman said. “But we kept going, originating aggressively. By around June or July, we started to feel competitive again and rebounded; we started bringing people back– hiring back staff that was furloughed.”

Gutman said the firm was able to change the winds, and by December they were not far off from where they were in 2019. Now set up finally for the aggressive growth plan they had laid out before Covid, Gutman said that though the pandemic threw everything to the wind, Fora still had the capital to back up a good book of business when everything else failed.

Gregory J. Nowak, Partner at Troutman Pepper, Has Passed Away

April 13, 2021 Gregory J. Nowak, a partner at Troutman Pepper, passed away suddenly on April 11th at the age of 61.

Gregory J. Nowak, a partner at Troutman Pepper, passed away suddenly on April 11th at the age of 61.

The firm’s website introduced Nowak as a veteran attorney that was “sought after for advice on complex securities law matters, particularly on issues arising out of the Investment Company Act of 1940; the Investment Advisers Act of 1940; federal and state securities laws and regulations; broker dealer, FINRA, CFTC and NFA regulatory matters; and corporate and M&A transactions.”

That perfectly sums up the context in which I first encountered Nowak in 2017 when he spoke at a small event put on by the Alternative Finance Bar Association where I was the only non-lawyer in the entire audience. One might expect a presentation on the finer minutiae of securities law of which he gave, to be a mundane, easily forgotten experience for a financial journalist such as myself, but his energetic delivery and fluid command of the subject matter translated complex securities questions into a folksy debate wherein one could feel confident in resolving the Howey Test over the dinner table just as easily as they could in the courtroom.

In fact, I approached him afterwards to thank him on his presentation and even followed up later over email, asking if I might have the honor to list him as a recommended securities attorney on the deBanked website. That was four years ago and as fate would have it, he remained the only recommended attorney that deBanked formally listed under the securities category, despite my coming to know very many accomplished and competent attorneys in the same field of law.

Nowak was one of the earliest public voices in the world of merchant cash advance participations and syndication where the securities question was a consideration some weren’t even sure applied as the industry created new products and investing structures at a furious pace.

He spoke at deBanked’s first major conference in 2018 on the subject of “Syndication and Raising Capital,” and he continued to generate recognition of the need for securities legal support in the burgeoning industry.

He was a co-author of an article published with a colleague at Pepper Hamilton LLP (now Troutman Pepper) that he had given permission to be reprinted on deBanked in December 2018, titled MCA Participations and Securities Law: Recognizing and Managing a Looming Threat. It was read by more than 1,500 people on the deBanked website that first day alone.

Nowak was highly sought out on merchant cash advance issues. “Most judges want to see consistency of treatment and that includes your vocabulary,” Nowak said in an interview with deBanked in April 2019. “The word ‘loan’ should be banned from their email and Word files.”

Although our relationship was one of professional acquaintances, I often told those seeking advice about MCA syndication that they should “probably call Greg Nowak about that.”

In “Does Your Merchant Cash Advance Company Pass The Scrutiny Test?“, Nowak explained that funders that decide for business purposes to solicit money from investors, have to be careful not to run afoul of SEC rules. He said that he recommended funders treat these fundraising efforts as if they are issuing securities and follow the rules accordingly. Otherwise they risk being the subject of an enforcement action where the SEC alleges they are raising money using unregulated securities.

“You need to be very careful here because these rules are unforgiving. You can’t ignore them,” Nowak said.

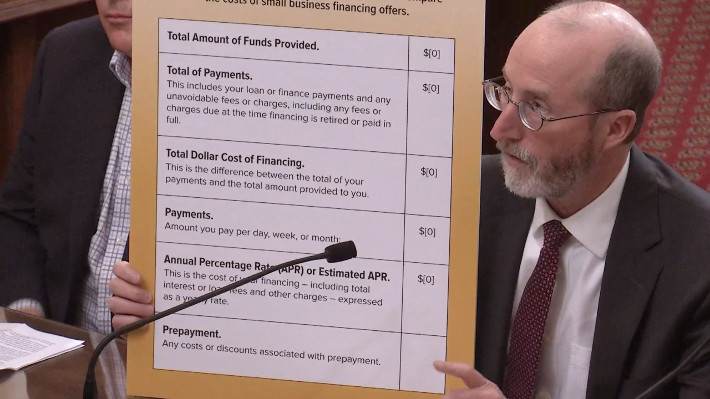

California’s Business Loan & MCA Disclosure Law Is Nearing Finality

April 13, 2021 Nearly three years after California became the first state to pass a business loan and merchant cash advance disclosure law (SB 1235), the actual disclosure rules themselves are finally nearing completion. The public has until April 26th to submit any comments on the amended portions of the proposed rules.

Nearly three years after California became the first state to pass a business loan and merchant cash advance disclosure law (SB 1235), the actual disclosure rules themselves are finally nearing completion. The public has until April 26th to submit any comments on the amended portions of the proposed rules.

The 52-page document is the result of years of negotiations between various parties that all have a stake in its implementation. Among the finer details are the characteristics of the fonts permitted in the disclosures, what column a certain disclosure can be placed in, and the aspect ratio of the columns themselves.

But that’s the easy part. Here’s the hard part, according to a brief published in Manatt’s newsletter yesterday.

“The modified regulations continue to require use of the annual percentage rate (APR) metric, rather than annualized cost of capital (ACC), to disclose the total cost of financing as an annualized rate. This appears to be a final decision, which will make it difficult if not impossible for many commercial finance companies to comply given the significant challenges of calculating APR on products with substantial variance in the amounts and timing of payments or remittances.”

Manatt highlights other issues, including that all the necessary disclosures be provided “whenever a payment amount, rate, or price is quoted based on information provided by the proposed recipient of financing…”

This requirement, the firm says, is not even required under Federal Regulation Z for consumer loans.

“Many companies will not be able to comply with this requirement absent radical changes to their California application and underwriting procedures, as it is common today for companies to have preliminary discussions with applicants about potentially available financing terms before full underwriting has been completed.”

Manatt’s newsletter on the issue can be found here.

Any interested person may submit written comments regarding SB 1235’s modifications by written communication addressed as follows:

Commissioner of Financial Protection and Innovation

Attn: Sandra Sandoval, Regulations Coordinator

300 South Spring Street, 15th Floor

Los Angeles, CA 90013

Written comments may also be sent by electronic mail to regulations@dfpi.ca.gov with a copy to jesse.mattson@dfpi.ca.gov and charles.carriere@dfpi.ca.gov.

The last day to submit comments is April 26, 2021

Industry Ponders: Broker Blacklisting, or Certification?

April 5, 2021 It’s a concept that’s been thrown around the industry for years- swapped like business cards at meetups, conventions, and chatrooms. Shouldn’t there be a broker certification, database, or even blacklist for known bad actors?

It’s a concept that’s been thrown around the industry for years- swapped like business cards at meetups, conventions, and chatrooms. Shouldn’t there be a broker certification, database, or even blacklist for known bad actors?

As deBanked petitioned the question, the industry responded with its naturally diverse responses. The problem: bad actors can keep getting away with shenanigans. The solution? Well, no one size fits all approach could work in the alternative finance industry, but a certification source may do the trick.

CEO of FundFi, Efraim “Brian” G. Kandinov, recently brought up the idea of a “Datamerch for Brokers.” Like a DNC list, Kandinov said there has got to be a way to sort out the known bad actors, scam artists, and even the brokers that play the funding houses by training merchants.

“I think opposed to a blacklist: a list that notes bait and switches, where the merchant was coached by the broker,” Kandinov said. “This way can go around a lawsuit or any fear of that, and the funder is free to choose once reading others’ notes.”

Kandinov said that most of his “problem files” show signs of brokers coaching merchants to start protesting deals after the clawback period ends. Get paid, pass the smell test during a 30-60 day waiting period, and then tell the merchant to jump ship on the deal or argue to lower the payments.

“If they were not [suddenly going out of business], they were calling in like a schedule to lower their payments. No way it can be that uniform unless they were being coached. The broker comes off as the good guy that he played the funding houses,” Kandinov said. “I think harsh means are necessary to expel these guys from the industry.”

Other funding side members of the industry have voiced their support for some type of broker record database. Kristen Ferrara, Director of Underwriting at The LCF Group based in New York, said that LCF pays a high expense to select ISOs. A vetting platform could be a great resource.

“I think it would be a good resource for funders,” Ferrara said. “We turn down about 50% of the ISOs who try to sign up with us. This resource could save funders millions of dollars in deals going bad from ISOs over-promising or committing fraud.”

“I think it would be a good resource for funders,” Ferrara said. “We turn down about 50% of the ISOs who try to sign up with us. This resource could save funders millions of dollars in deals going bad from ISOs over-promising or committing fraud.”

On the other side of the country in San Diego, CEO David Leibowitz from Mulligan Funding said he is all for a way to help funders vet brokers. Mulligan is lucky to work with a trusted brokers network and drops a client like a broken elevator at the first sign of fraud or unethical behavior, he said.

“We are extremely careful about which brokers we do business with. If we see any kind of practice that we think is unethical, we’ll cut a broker loose in a heartbeat,” Leibowitz said. “Is there value in the sort of thing you’re talking about? I think there probably is because I think it makes vetting brokers for [funders] a lot easier, and it also allows brokers to differentiate themselves against their competition by their ethics.”

Leibowitz is a proponent of ethics as an indicator of value and said a certification could help members of the public tell the difference between good and bad funders and let funders spot good ISOs and bad ISOs.

A worry for some is that whatever company, organization, or site that hosts a broker ledger could face lawsuits for liability, could accept payments to make bad reviews go away, list competitors to hurt them, or be outright ignored by an industry always hungry for deals.

But industry lawyers seem to agree that a broker certification or blacklist would ultimately benefit the industry if provided from the right source. Patrick Siegfried, the Deputy General Counsel at Rapid Finance, said that whatever agency would be rating brokers would need its own trusted reputation.

“To have a legitimate background or rating system, it needs to be done by an independent third-party that has its own credentials,” Siegfried said. “I think that’s a big reason you don’t see many third-party or private rating systems.”

Siegfried said one option that ensures a true third-party point of view is a government agency taking care of a broker tracking system. Another option would be an industry coalition, but then it’s a question of cost- Who is paying to staff and maintain a complaint system?

Siegfried said one option that ensures a true third-party point of view is a government agency taking care of a broker tracking system. Another option would be an industry coalition, but then it’s a question of cost- Who is paying to staff and maintain a complaint system?

“At the end of the day, having a good industry regulator is a benefit for the industry,” Siegfried said. “It will allow a third-party, government entity to vet brokers in terms of licensing and then maintenance, looking into valid complaints.”

As conversations across the country point toward a licensing regime, Siegfried said it’s a sign the industry is maturing and that one day there will be a government agency to lodge complaints with and to actually vet brokers in the space.

Steve Denis from the Small Business Finance Association (SBFA) proposed a solution to the issue. He said that in the works right now is an SBFA-sponsored certification program.

“We started just looking at brokers and thinking about how to certify them,” Denis said. “We think that it’s the time, from the feedback we’ve gotten from regulators, that we launch a true industry-wide certification.”

In the coming months, brokers may be able to apply for certification when the program rolls out. Instead of a ‘blacklist,’ Denis said brokers could set themselves apart as trusted providers by going through a basic background test or industry knowledge checks.

“If you’re a broker and you can’t get certified, then there’s probably some issues,” He said. “So our hope is if you carry a certification, that’s sort of a message that you are a good broker.”

When it comes to government regulation, Denis said he is still cautious. While he 100% expects certification programs to crop up for state licenses, he thinks no government agency can achieve what an industry coalition can do.

Tune in Today Live: debanked.com/tv

March 31, 2021Update: The recording is here

deBanked will be streaming live today at approximately 12:15 with special guest Jennie Villano of NewCo Capital Group. She will be joined by host Sean Murray in the studio. This is not a Zoom or virtual discussion. There is no need to register. Anyone can tune in free at debanked.com/tv or debanked.tv

Merchant Cash Advance Facebook Group Hits 1,000 Members

March 26, 2021 The Merchant Cash Advance facebook group, a community created and administered by deBanked, has reached 1,000 members. The social media group is a popular place for those in the non-bank business finance community to engage with each other online.

The Merchant Cash Advance facebook group, a community created and administered by deBanked, has reached 1,000 members. The social media group is a popular place for those in the non-bank business finance community to engage with each other online.

“We’re seeing an uptick in collaborative business development, especially among smaller brokerage organizations and those who work independently on their own,” deBanked President Sean Murray said. “A lot of ideas, motivation, referrals, and deal-making is being conducted online, more-so than before because of the 2020 lockdowns where in-person collaboration slowed to a crawl.”

Separately, deBanked shares common ownership with DailyFunder, the largest b2b finance community on the web.

“We actually witnessed a very insightful trend on DailyFunder,” Murray said. “Approximately 7.5% of the active membership that existed on March of 2020, had left their jobs or closed their business by March of 2021. It sounds troublesome on its face except that we added more members than we lost in that timeframe. More people came in than left, a net increase. I think the data is pointing to the future being very strong!”

NY Court Says MCA Agreement is a Factoring Agreement, Not a Loan

March 22, 2021 A New York Supreme Court judge that was presiding over a breach of contract claim (653596/2018) in a merchant cash advance agreement, said he was bound to follow the decision issued in Champion Auto Sales, the landmark appellate ruling in 2018.

A New York Supreme Court judge that was presiding over a breach of contract claim (653596/2018) in a merchant cash advance agreement, said he was bound to follow the decision issued in Champion Auto Sales, the landmark appellate ruling in 2018.

In Principis Capital LLC v Team Van Eyk, Inc. et al, Principis sued the defendants over a breach of contract. Defendants “did not deny the facts underlying the motion or the the amount due,” the judge said, “but asserted instead that the Agreement is not an agreement for the purchase of future receivables; but is instead, a criminally usurious loan, and is therefore void as a matter of public policy.”

This defense actually led to victory for the plaintiff.

The Appellate Division, First Department, in Champion Auto Sales, LLC v Pearl Beta Funding, LLC (159 AD3d 507, 507 [1st Dept], lv denied 31 NY3d 910 [2018]) has considered this issue, involving a merchant agreement substantially similar to the agreement in this matter, and has held that the type of agreement involved in this case is a factoring agreement rather than a usurious loan. This court is bound to follow Champion and, therefore finds that the Agreement is a factoring agreement and not, as defendants assert, a usurious loan. There are, therefore, no genuine triable issues of fact, and plaintiff is entitled to summary judgment on its complaint.

Case closed.