Industry News

The SEO War for ‘Merchant Cash Advance’

February 12, 2012 Let’s admit it, we’re all at war. If you’ve uttered the terms Panda, PageRank, Backlinks, or Organic in the last few months, you know what we’re talking about. We didn’t choose this fight, Google forced it upon us. And so after a long day of phone calls and handshakes about affordable working capital, we return to our homes at night and search the web. Not for information of course, but to find out where our company website pops up when we Google the phrase: Merchant Cash Advance or other relevant terms. Today we ask, is the fighting worth it?

Let’s admit it, we’re all at war. If you’ve uttered the terms Panda, PageRank, Backlinks, or Organic in the last few months, you know what we’re talking about. We didn’t choose this fight, Google forced it upon us. And so after a long day of phone calls and handshakes about affordable working capital, we return to our homes at night and search the web. Not for information of course, but to find out where our company website pops up when we Google the phrase: Merchant Cash Advance or other relevant terms. Today we ask, is the fighting worth it?

In 2007, back when the industry hadn’t put much thought into the Internet, the #1 search result for Merchant Cash Advance was the blog by David Goldin, the CEO of Amerimerchant. It made sense because it was a self proclaimed “online resource dedicated to the merchant cash advance industry.” There, small business owners and competitors could read about the trials and tribulations of an industry on the verge of explosive growth. It was interesting, it was informative, and best of all, he ranked first without trying.

Nowadays, it’s all commercial. Merchant Cash Advance companies with fat advertising budgets are spending thousands to rank for their favorite keywords, with Merchant Cash Advance still high on that list. The friendly information resource has been replaced by a website that not only crushed the competition in search positioning but seems to publicly brag about it too.

As we write this article, the top 10 Google search results for Merchant Cash Advance are:

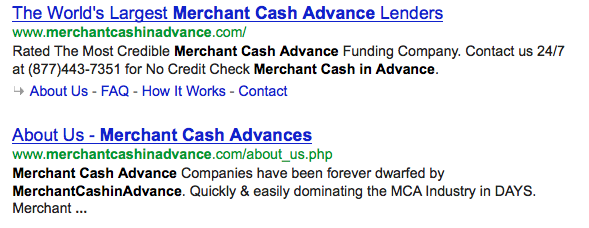

1. Merchant Cash in Advance

2. YellowStone Capital

3. Entrust Cash Advance

4. Merchants Capital Access

5. Merchant Resources International

6. American Finance Solutions

7. Nations Advance

8. Bankcard Funding

9. Rapid Capital Funding

10. Paramount Merchant Funding

Do keep in mind that your results may differ slightly depending on your region. Google geographically targets searchers to bring them the most relevant matches.

How much is the #1 spot worth? The market priced it at $75,000 three months ago when MerchantCashinAdvance.com was sold in an online auction for that amount (saved in pdf). So which powerful Merchant Cash Advance company unloaded their precious website? None. The owner of the site was actually an SEO guru looking to make a quick buck. He studied the industry a bit and then within two months ranked a site at the top of Google.

75k might even be considered a steal, as we were actually approached to purchase that website ourselves in August 2011. The exchange was a bit contentious, with them being unwilling to accept less than $200,000 and us making an insulting offer of $100. Perhaps it was jealousy or perhaps it was because we didn’t realize how a Merchant Cash Advance website could be worth so much, but the discussion quickly degraded into name calling and we never spoke again.

How many small businesses are searching for Merchant Cash Advance anyway? According to Google, there are 14,800 searches for it a month. We assume that at least 75% of those are from the companies offering it. You probably Google the phrases several times a day yourself. Admit it!

The real money is in the long tail keywords, since merchants are more likely to personalize their search. Being first for merchant loan for bad credit might be more potent than Merchant Cash Advance. It’s tough to say since deBanked doesn’t really rank for either of those. Then again, we’re an information destination, much like David Goldin’s Blog was/is.

We’re not SEO experts, but we do quite alright with Google ourselves. Without giving away all of them, this is our current placement for just the following keywords:

- Merchant Cash Advance directory: 1, 2

- Largest Merchant Cash Advance companies: 1

- Merchant Cash Advance UCC: 1, 2, 3

- Merchant Cash Advance statistics: 1

- Merchant Cash Advance stats: 1, 2

- Merchant Cash Advance default: 1, 2

- Merchant Cash Advance UCCs: 2, 3, 4, 5

- Merchant Cash Advance laws: 2

- Merchant Cash Advance forums: 2

- Merchant Cash Advance articles: 3

- Merchant Processing: 3

- Merchant Cash Advance Jobs: 8

- Sell your mom for cash: 1 (don’t ask)

MerchantCashinAdvance.com was no different and they claimed to be #1 for over 300 business lending related keywords. A spreadsheet of the analysis they put up during the auction can be found here.

With nothing more than an organic search presence, they claimed to have had the following results:

Month of July for 2011: Received 647 calls & 148 online business lending applications: Funded 81 deals, $26,000.00 profit.

Month of August for 2011: Received 731 calls & 234 online business lending applications: Funded 113 deals, $29,500.00 profit.

Month of September 2011: Received 1026 calls & 276 online business lending applications: Funded 147 deals, $41,750.00 profit.

If that’s the case, then $75,000 was a bargain. That no doubt led to the auction of a similar site just a month later. MerchantCashAdvances.org is currently ranking 51st for Merchant Cash Advance. They claimed to earn $12,500 annually in ad revenue and $200,000 in commissions. The starting bid was $10,000 and although there were many inquiries, it didn’t sell.

That doesn’t mean it wasn’t worth the price. Most Merchant Cash Advance companies are secretly or not-so-secretly investing thousands into SEO campaigns. Black hat SEO is rampant and even the most reputable companies have engaged in it at some point. The underwriting room is the one they show their clients. The sales floor is the one they show their new recruits. But ask where the internet marketing room is, and they’ll claim it doesn’t exist. But it does of course. They’re usually small quarters with no windows that are filled with computers armed with software like ScrapeBox, Article Marketing Robot (AMR), XRumer, and a list of working proxies.

Even the white hats are building backlinks manually and creating endless articles for use on their own company blogs or for services like BuildMyRank. One moderately sized Merchant Cash Advance company in New York City has just as many SEO employees as they do sales representatives. For some, this is just the beginning. It’s not unusual to spend $10,000 – $20,000 a month on pay-per-click campaigns.

The Internet has become a place where the person with the most to spend wins. Because of competition, a paid Google campaign for Merchant Cash Advance keywords can cost $20 per click! We did a phone call with Google and were told that less than 10% of clickthroughs convert into a sale or completed form. If only 1 out of every 10 visitors calls or inquires through the site, that amounts to $200 for a single lead. If only 1 out of every 5 of those leads turn into a closed deal, the acquisition cost is effectively $1,000. That number is awful especially considering commissions and factor rates have been rapidly declining over the last year. And merchants wonder why this financing is more expensive than a bank loan…

It also explains why the practice of closing costs and service fees have survived internal industry scrutiny. Some resellers would be operating in the red without them. Organic traffic is in essence free, that is if you don’t consider the salary or fees you pay your SEO team. Hopefully they don’t overdo it and place your site in the Google sandbox. Until then, the rewards outweigh the risks and every day the industry pushes the envelope a little further in the quest to rank on page 1.

If you can earn $200,000 a year from a website or sell one for $75,000 after two months of work, then there is plenty of room for growth. If the industry was saturated, it wouldn’t be that easy. If your mother is getting into the Merchant Cash Advance business, make sure she knows how to market her website. It’s a war out there.

– deBanked

https://debanked.com

Does Your Mom Sell Merchant Cash Advance?

February 4, 2012Five years ago, everyone seemed to add the phrase, “but I also do mortgages on the side” in response to questions about their career.

“I’m a stockbroker, but I also do mortgages on the side.”

“I’m a school teacher, but I also do mortgages on the side.”

“I’m a stay at home mom and a loving wife, but I also do mortgages on the side.”

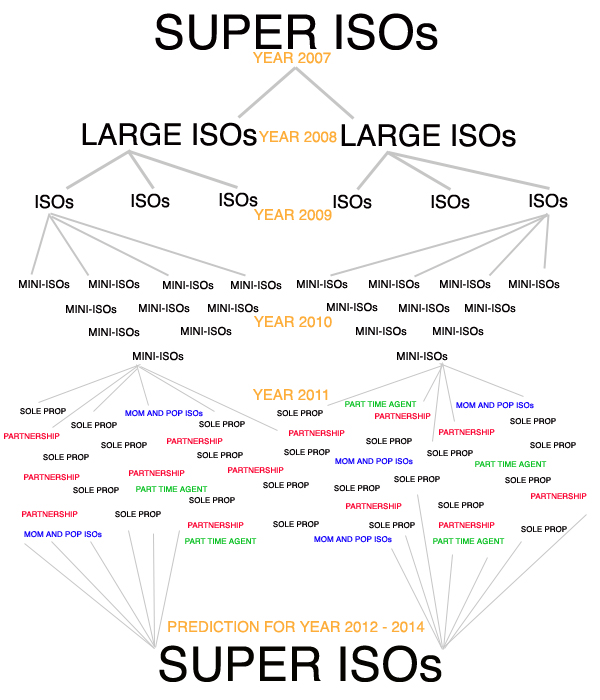

Times have changed and today the new side gig is reselling Merchant Cash Advance (MCA), at least in the New York metropolitan area. The Independent Sales Office (ISO) model is dissipating into a few thousand sole proprietors, all of whom are competing for the same prospects. Most of them started at one of the larger ISOs or funding sources and have over time traded it for the opportunity to work for themselves. Others have pushed it aside as a part time gig while earning a living in another line of work.

It’s encouraging to see that the entrepreneurial spirit is alive and well in the city that never sleeps, but riding solo has its disadvantages. For instance, marketing budgets are more constricted. This inhibits the ability to attract clients, especially when competing against a sizable ISO, who likely has thirty times more to spend on advertising, systems, and service.

It’s encouraging to see that the entrepreneurial spirit is alive and well in the city that never sleeps, but riding solo has its disadvantages. For instance, marketing budgets are more constricted. This inhibits the ability to attract clients, especially when competing against a sizable ISO, who likely has thirty times more to spend on advertising, systems, and service.

And yet, I haven’t heard many complaints from independent agents, which may mean the MCA industry is far from over-saturated. Sixteen of my former co-workers have gone on to start their own MCA ISOs. I even know a pair of twin brothers that run ISOs independent of each other. Some of these newly formed mini-ISOs (less than five people) break apart and each member seems to go on and repeat the cycle.

The Derailing of the Shakeout

In early 2008, it was predicted that low budget marketing would cause a massive shakeout of MCA resellers. David Goldin, the CEO of AmeriMerchant published the following in his blog:

There is another train of thought that is inevitable to fail – those that thought they can sell business cash advances with minimal capital expenditure, meaning hiring unqualified salespeople using inexpensive marketing techniques such as voice broadcasting (with these providers giving the same data to 100s of phone rooms) to dial hundreds of thousands of businessses an hour with a prerecorded message. (Merchants around the country are getting 3 – 5 prerecorded calls a day). The challenge is the quality of anyone that is going to press ‘2’ on their phone for money tends to be “lower hanging fruit” and lower quality deals. With the recent credit crunch and many merchant cash advance funding companies tightening up, some merchant cash advance agents were seeing approval rates as low as 15%-20%. There is no way they can survive and stay in business with that kind of approval rate.

Back then, it was quite popular to have a hundred sales agents in a single room making phone calls. Overhead was the biggest part of the budget, which in places like New York City, could consist of tens of thousands of dollars in rent alone. Add that to all the money that was spent on technology, payroll, dialers, and commissions, and it became really easy to generate a net loss.

With the emergence of mini-ISOs, many are foregoing traditional overhead expenditures such as the renting of a centralized office. Technology costs are also being eliminated since most people already own a personal computer and a cell phone, the only two tools really necessary to interact with prospects. As for state of the art auto dialers? Well, many agents are completely fine using inexpensive resources such as phone books or public UCC filings. Ask around in the MCA industry and you’ll learn just how prevalent this practice is.

There are so few barriers to entry in the MCA industry, that it catches a lot of folks from other financial fields off guard. We receive a dozen e-mails a month from mortgage brokers, stockbrokers, and insurance agents asking what licensing requirements they will need to sell MCA. There are none of course, but they more are shocked to learn that there are no regulations to abide by either. Take your cell phone, throw in your e-mail, spend twenty bucks on a website and you’re an official MCA reseller! It’s just that easy. Thousands of people are getting in on it.

Who is Who?

The flood of resellers and fly-by-night agents is making it increasingly difficult to know where all the MCA money is actually coming from. Here on the Merchant Processing Resource’s website, we’ve created transparency by listing the largest direct funding providers. Need to know if that UCC filing is MCA related? We can help you with that too.

We’re also working on creating an official directory of resellers, for which there will be some requirements for inclusion. That means if you’ve e-mailed us on this topic already and you haven’t heard from us yet, be patient. You will be contacted soon with instructions on how to become an approved MCA reseller.

Consolidation

In the meantime, the increasing fragmentation also presents an incredible buying opportunity. Large ISOs that are looking to add to their portfolios and leverage the brand names that mini-ISOs have created should be able to buy them out at very affordable prices. When this practice starts to happen, it’ll be interesting to see what the market value of mini-ISOs are. Could a business owned by two individuals with a pool of two hundred clients be worth $50,000? $100,000? $300,000? Once someone sets the bar, we should prepare for a year of consolidation, and the little guys will get gobbled up by the big ones. A lot of folks could end up walking away very rich or disappointed. Perhaps now is a good time for your Mother to go into the MCA business for herself and flip the value created for a nice profit a year from now.

ISOs on Steroids

The popularity of co-funding or syndication is also allowing the remaining large ISOs to really flex their muscles in a way they weren’t able to in 2008. Syndication is where an ISO is able to invest their own capital in the MCA deals they close. For instance, on an advance of $20,000, $15,000 of it might come from the MCA funding source, and the remaining $5,000 from the ISO themselves. As long as these accounts perform well, syndicating can create a supernatural rate of growth. This further whets the appetite for opportunities to expand.

So why are mini-ISOs a buying opportunity? Customer loyalty is something big companies can’t always shake, no matter how much is spent courting them. Furthermore, these mini-ISOs tend to have historical performance records on their clients, data that is incredibly valuable. Should a Super ISO invest $20,000 in a small business that has never used MCA before or should they invest it in a business that has responsibly used MCA for two years with no issues, exhibits fierce loyalty, and has a proven record of success? The opportunity to participate in funding that business now and repeated times in the future should be worth a lot.

The Unknown

There are other forces at work that may reshape the industry in a way we can’t predict. The incredible rise of micro-lending is cannibalizing the MCA market, but is also allowing ISOs to offer a variety of financial products to a larger pool of businesses. One New York City MCA funding source privately revealed that micro-loans now make up 80% of their monthly funding volume, a stunning shift from their MCA-only portfolio of 2010.

The growing popularity has also caught the attention of regulators and in some states, the purchase of future credit card receivables is being governed by existing lending laws. The day may come when every agent needs a license to sell, but until then, thousands of people are playing the biggest game in town, helping small businesses get funding to grow. Are you a part of it?

– deBanked

https://debanked.com

The 28% You Don’t Want – New IRS TIN Matching Regulation

January 21, 2012 If your merchant service provider (MSP) doesn’t have your proper business information on file, you could be in for a world of hurt. As per Section 6050W of the Housing Assistance Tax Act of 2008, all electronic payment transactions have been reported to the IRS since January 1st of last year. In order to ensure this reporting is accurate, certain business data must match the data on file with the IRS, such as:

If your merchant service provider (MSP) doesn’t have your proper business information on file, you could be in for a world of hurt. As per Section 6050W of the Housing Assistance Tax Act of 2008, all electronic payment transactions have been reported to the IRS since January 1st of last year. In order to ensure this reporting is accurate, certain business data must match the data on file with the IRS, such as:

- Your Taxpayer Identification Number (TIN)

- Your Legal Business Name

- Your Legal Business Address

- Your Business Organization Type (e.g. Corporation, LLC, Partnership, Sole Prop., etc.)

MSPs are required to report gross revenue, so chargebacks and refunds are included. The official ruling states:

Section 6050W(a) provides that each payment settlement entity must report the gross amount of reportable payment transactions for each participating payee. The proposed regulations defined gross amount as the total dollar amount of aggregate reportable payment transactions for each participating payee without regard to any adjustments for credits, cash equivalents, discount amounts, fees, refunded amounts, or any other amounts.

And if your tax information doesn’t match, the IRS will withhold 28% of all your payments starting on January 1st, 2013, whether it’s your fault or not. Once that happens, your MSP can’t refund you and all issues must then be handled with the IRS directly. If you haven’t received any kind of alarming notice that your information doesn’t match, this warning doesn’t apply to you. Although, it can’t hurt to call your account representative to confirm that all information is up to date and verified. Better safe than sorry.

If you didn’t know about this law, now is a good time to read up on the dense technicalities of it in this 520 page document.

Learn Merchant Cash Advance or Else…

December 15, 2011If you don’t know about Merchant Cash Advance (MCA), you’re not qualified to work in the payments industry! As indicated by the Electronic Transactions Association (ETA), Certified Payment Professionals (CPPs) should be savvy with MCA financing. According to the ETA: “The [new] CPP program sets the standard for professional performance in the payments industry and is a symbol of excellence. It signifies that an individual has demonstrated the knowledge and skills required to perform competently in today’s complex electronic payments environment.”

CPP candidates can preview exam sample questions in the official handbook, one of which asks:

An established merchant that processes $25,000 in bank card transactions per month has no marketing budget, but has been offered a sponsorship opportunity. What product/solution should the payments professional recommend?

The answer is “merchant funding” AKA MCA. Believe it folks. The MCA financing product is here to stay, has benefitted thousands of businesses, and payment professionals must be well versed in it if they are to become certified.

But there is more than a test to become a CPP.

[The ETA says] to be eligible to sit for the CPP examination, candidates must demonstrate the following qualifications:

|

|||||||||

|

CPP candidates will then be required to sit for and pass a Certified Payments Professional written examination. Upon successful completion of the exam and the attainment of the CPP credential, certificants will be required to meet renewal / recertification requirements every three years, to include continuing professional education from ETA / QSP’s or the successful completion of the test.

|

The next exam dates are May 1 – 31, 2012. You can learn more about registering and what it mean to be a CPP on the ETA’s official site. And don’t forget to learn about Merchant Cash Advance. 🙂

Largest Merchant Cash Advance in History Ends in Default

September 27, 2011 Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

Six months ago, news headlines publicized just how far the Merchant Cash Advance (MCA) product had reached. Once the ‘Plan B’ option for retail businesses in need of capital, the sale of future card payments was utilized to finance a project at a Las Vegas casino. And it was no small figure. New York based Strategic Funding Source (SFS) in collaboration with Vion, shelled out $3.147 Million in return for $4.092 Million of the Las Vegas Mob exhibits’s future sales. That’s a cost factor of 1.30, a price that typifies the average MCA deal.

While SFS was given high praise from their peers, some began to speculate if transactions that large were practical. After all, the costly financing of a MCA is priced in accordance with the risk of default, not in accordance with big profits for the financier. When your portfolio is in great shape, it can be easy to forget what the pitfalls are. And since the MCA industry paraded the Las Vegas Mob exhibit as the $4 Million deal that changed everything, we’re eerily reminded of the words by Jeff Mitelman, the CEO of AdvanceIt who was quoted two years ago as asking: “How prepared are you to lose $4 million dollars?”

We won’t pretend to know what led to the downfall of the Las Vegas Mob exhibit or why it went south so quickly. SFS could potentially lose 98% of their investment, a hit that will surely change their outlook on doing large deals in the future. The VegasInc article alleges gross mismanagement and fraud, factors that are difficult to foresee in the course of underwriting.

Industry message boards have been abuzz with comments on the default, with some competitors of SFS being accused of kicking a man while he’s down. “you ought to do smart funding, not just showing off your Balls,” one broker fired off at them. SFS has a stellar reputation and is one of the most knowledgeable firms in the MCA space. We have no doubt they inspected the merits of the deal backwards, forwards, and upside down. But nothing is perfect.

The default is expected to attract attention of the news media, leaving many to wonder how this transaction will be interpreted under the public eye. We assert that it will put to rest any criticism the MCA product has ever received about high costs.

Risk vs. Reward

Back in March when the deal was written, an outsider could claim that SFS just had an easy million handed to them. This view clashes with the Risk vs. Reward philosophy that MCA providers hold dear. To the MCA providers, the question was never “how can I make an easy million?” but rather, “how prepared am I to lose $4 Million?”

Any business that can’t get a bank loan, can’t get one for a reason. There’s a measurable value of risk that’s not worth taking. MCA providers fill the gap but compensate to offset defaults. There’s a term for something like this. It’s called a Happy Medium.

Merchant Cash Advance is the happy medium financing option for small businesses. And for the immediate future it is likely to stay within the small business niche. We all know now what can happen when the concept is applied to a multi-million dollar project. The outcome was not so happy and the loss not so medium.

But it will all even out in the end…

– Merchant Processing Resource