Industry News

Marathon Partners Targets OnDeck Capital

April 17, 2017 Marathon Partners, which owns 1.25 million shares of OnDeck Capital, has drawn a line in sand on the shore of the online lender. The private investor is urging OnDeck, whose share price has shed approximately three-quarters of its value since its IPO, to lower its risk profile amid lofty overhead expenses, which Marathon believes are preventing the online lender from achieving real profitability. Marathon has given OnDeck until the company’s annual shareholder meeting in May to respond. Otherwise the investor has vowed to withhold its support for a trio of board members who are up for a vote.

Marathon Partners, which owns 1.25 million shares of OnDeck Capital, has drawn a line in sand on the shore of the online lender. The private investor is urging OnDeck, whose share price has shed approximately three-quarters of its value since its IPO, to lower its risk profile amid lofty overhead expenses, which Marathon believes are preventing the online lender from achieving real profitability. Marathon has given OnDeck until the company’s annual shareholder meeting in May to respond. Otherwise the investor has vowed to withhold its support for a trio of board members who are up for a vote.

“We’re talking about a stock that is down 75 percent to 80 percent from its IPO price. You’re not going to find a lot of happy campers in that situation. Shareholders are going to ask tough questions,” Mario Cibelli, Marathon Partners managing member, told deBanked.

OnDeck Capital, meanwhile, believes it is on the right path for creating greater shareholder value.

“OnDeck welcomes open communications with all stockholders and values constructive input. Members of our board and management team have met with Marathon on several occasions. We are committed to driving value for all OnDeck stockholders and will continue to take actions to achieve this important objective,” said OnDeck’s Jim Larkin.

Indeed Marathon and OnDeck executives have had their share of discussions in the past year, over which time Marathon has acquired its stake and during which time the company’s valuation has become more interesting.

While other institutional investors have been buying shares, evidenced by EJF Capital’s 13-D filing in recent weeks, Marathon — though it has the capital to increase its stake in OnDeck — would not consider doing so with the company’s current risk profile. Marathon Capital’s lack of support for the vote, however, is less a reflection on any one individual and more a protest against the actions or lack thereof of the board as a whole.

“The only way for shareholders to reflect any disappointment or criticism on the proxy is by withholding votes for directors. Instead of picking out one or two of them, we said we’re not going to vote for any of them. This is a clear protest vote for poor performance,” said Cibelli.

Chief among Marathon’s criticisms is an executive compensation structure, including that of CEO Noah Breslow, which omits detail for investors. “There is not a tremendous amount of detail on executive compensation in the proxy, so it’s hard for investors to know what the incentives are that drive the senior management team. The board needs to be very thoughtful around creating the right set of incentives to increase shareholder value,” said Cibelli.

For instance, OnDeck Capital in its quest for profitability points to adjusted EBITDA, which Cibelli said is a “terrible” metric to use to incentivize a management team of a lending business. “It excludes stock-based compensation and depreciation. It also ignores the risk level on the balance sheet. For OnDeck profitability ought to mean GAAP net income,” said Cibelli. “You don’t hear Chase, Wells Fargo or any specialty finance company talking about adjusted EBITDA. GAAP net income is the proper metric and that is what we want OnDeck Capital to achieve.”

For instance, OnDeck Capital in its quest for profitability points to adjusted EBITDA, which Cibelli said is a “terrible” metric to use to incentivize a management team of a lending business. “It excludes stock-based compensation and depreciation. It also ignores the risk level on the balance sheet. For OnDeck profitability ought to mean GAAP net income,” said Cibelli. “You don’t hear Chase, Wells Fargo or any specialty finance company talking about adjusted EBITDA. GAAP net income is the proper metric and that is what we want OnDeck Capital to achieve.”

The murkiness surrounding Breslow’s compensation incentives has been exacerbated by what Cibelli described as an “excessive” overhead structure at the company that amounts to approximately $200 million each year.

“Given the high level of overhead, they have a tremendous amount of pressure on them to maintain and grow the loan portfolio,” said Cibelli, pointing to the company’s lack of profitability. If the company were profitable, Cibelli said OnDeck would start from a very different place when making its loan decisions.

“They would focus more on the quality of loans and interest rates. If OnDeck was profitable today, they might choose to step back from certain types and durations of loans since they would be under far less pressure to grow. Instead they could let the market and their competitive positioning dictate the level of growth,” he said, adding that OnDeck Capital is very challenged to be both prudently leveraged and profitable with its current level of overhead at $200 million.

As for next steps, Marathon Partners, which also wants the online lender to consider a sale of the company, is watching and waiting to see what OnDeck Capital will do.

“The ball is in their court,” said Cibelli. “We will see what they have to say and what they tell shareholders in a couple of weeks on the first quarter call.”

Nulook Capital Has Filed Chapter 11

April 13, 2017NY-based merchant cash advance funding company Nulook Capital filed for Chapter 11 on April 4th, according to court records. They listed more than $2.6 million in creditor claims. The largest among them was a secured claim for $2 million by a specialty finance company.

Two other creditors in the bankruptcy proceeding are also involved in the merchant cash advance industry.

The voluntary petition was filed in the Eastern District of New York in the United States Bankruptcy Court.

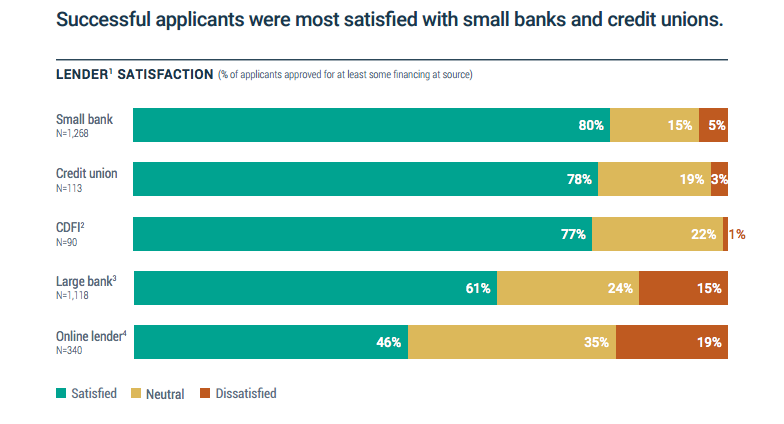

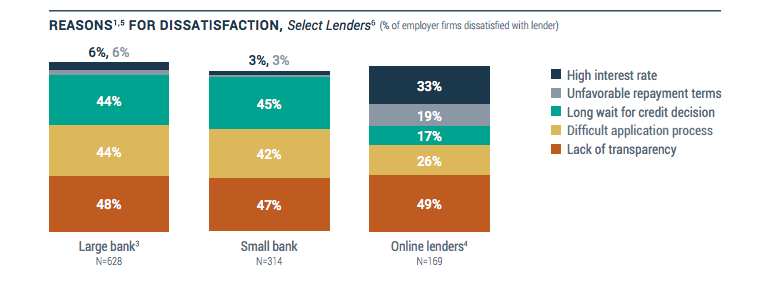

81% of Online Business Lending Borrowers Report Being Satisfied or Neutral

April 12, 2017The latest Small Business Credit Survey published by the Federal Reserve shows that 81% of small business borrowers were either satisfied or neutral about their online loan experience. Online lenders were defined as nonbank alternative and marketplace lenders, including Lending Club, OnDeck, CAN Capital, and PayPal Working Capital.

Of the 19% that were dissatisfied, nearly half cited transparency as a root cause. But that’s to be expected given that businesses dissatisfied with their loan from a large or small bank also cited transparency just as often.

While these charts indicate that there is still room for online lenders to improve, the 2016 report paints a more honest narrative than last year. Last year’s report used net satisfaction scores, which measured the difference between satisfied and dissatisfied borrowers. That methodology resulted in 15% net satisfaction for online lenders in 2015, which unless you read the fine print, easily misled even the most sophisticated of readers to conclude that only 15% of borrowers were satisfied. (Those readers included experts testifying in congressional hearings, the media, and government agencies, all of whom relied on that report to argue that online borrowers were terribly dissatisfied).

The 2016 report shows that businesses borrowing from an online lender were only slightly more likely to be dissatisfied than those that borrowed from a large bank (19% vs. 15%). And it’s the high interest rates that stand out to those dissatisfied online borrowers. 33% said that a high interest rate was the reason for their dissatisfaction. This is to be expected since non-banks inherently suffer from a higher cost of capital than banks.

Cash Advances?

Unfortunately, all of their data on “cash advances” is tainted. If they meant “merchant cash advances” or sales of future receivables, they should’ve specified such in the survey that went out to small businesses. Instead, the survey repeatedly asked about cash advances, a term most commonly associated with borrowing money through an ATM with a credit card. Those surveyed were also asked if they used personal loans, auto loans or mortgages so the multiple choice context suggests a credit card cash advance. Similarly, a cash advance could also mean a payday loan. With so many interpretations, the consequence is that it’s impossible to tell what the Federal Reserve meant or what those being surveyed thought they were being asked.

Notably, one question asked businesses if “portions of future sales” were used as collateral for a debt, but since merchant cash advances do not collateralize future sales (the future sales are actually sold, they don’t serve as collateral for a loan), it’s difficult to understand what they meant or how a respondent might interpret that.

Statistically representative?

The 2016 report also spends more time defending the Fed’s sampling methodology. Perhaps they are aware that their data is being put under the microscope.

Read the full Fed report here

Sneak Peek at the Mar/Apr 2017 Issue of deBanked

April 11, 2017 In the March/April 2017 issue of deBanked magazine, we delve into the industry’s latest trend, the push back towards traditional banking. The featured story is titled accordingly as “Re-Banked” and our many sources lay out a compelling narrative. Our cover, a sketch of a young tech CEO shedding the hoodie to reveal the suit-and-tie attire of a banker underneath, was one of several pieces of art we commissioned for this issue.

In the March/April 2017 issue of deBanked magazine, we delve into the industry’s latest trend, the push back towards traditional banking. The featured story is titled accordingly as “Re-Banked” and our many sources lay out a compelling narrative. Our cover, a sketch of a young tech CEO shedding the hoodie to reveal the suit-and-tie attire of a banker underneath, was one of several pieces of art we commissioned for this issue.

And for you brokers out there, we’ve got something really special, the inside scoop on the latest way that reps are winning deals. Today’s broker is hanging up the phone and texting merchants instead and the merchants are responding in kind. Phone calls and emails are going the way of the fax machine when it comes to gathering documents and pitching offers. The lesson we learned from the several people we interviewed is that when merchants want to know what’s next, send a text.

There’s more of course, so if you haven’t already subscribed to our free print magazine, make sure you do so here. This issue has already printed and shipped so you’ll be getting it very soon.

We hope you enjoy it!

Subscribe FREE

Lights Out for New York’s Attempt to Impose Stricter Lending Rules

April 5, 2017 In a late night session on Tuesday, and days past the budget deadline, the New York State Senate voted 58-2 in favor of a key budget bill. Noticeably gone from it was Part EE, which would’ve imposed stricter licensing requirements on not only just lending, but also other forms of finance. Part EE was originally put there by the Governor’s office as an amendment to Section 340 of the State’s banking law.

In a late night session on Tuesday, and days past the budget deadline, the New York State Senate voted 58-2 in favor of a key budget bill. Noticeably gone from it was Part EE, which would’ve imposed stricter licensing requirements on not only just lending, but also other forms of finance. Part EE was originally put there by the Governor’s office as an amendment to Section 340 of the State’s banking law.

Over the last two months, several trade groups used what little time they had to express concerns over the language. Their biggest frustration was that no one had consulted with them in advance. In February, Dan Gans, the executive director of the Commercial Finance Coalition (CFC) said, “They should allow all the stakeholders to have their voices heard.” The CFC, which represents many small business financing companies, did their best to do just that last month by actually making the trek to Albany.

Ultimately, the legislature did not support the Governor’s plan. Both the Senate and the Assembly removed Part EE from their versions of the budget and on Tuesday night, the Senate passed it. The Assembly passed it the day after.

This is the first time the budget deadline has been missed under Governor Andrew Cuomo. The last miss was in 2010 under Governor Paterson, which came in 125 days late.

Update in the Argon Credit Bankruptcy Case

March 31, 2017On March 28th, United States Bankruptcy Judge Deborah L. Thorne, ordered the trustee in the Argon Credit case to transfer the net proceeds and loan portfolio payments to the biggest creditor, Fund Recovery Services (FRS). That cash will be used to satisfy the approved secured claim of $37.3 million. FRS is an assignee of Princeton Alternative Income Fund, LP. Argon Credit was an online consumer lender that made loans between $2,000 and $35,000 with APRs ranging from 4.99% to 149%.

Initially, Argon Credit had applied for Chapter 11 bankruptcy after “experiencing financial difficulty,” though allegations of improprieties and mismanagement have come up in the legal filings. When FRS tried to stop their collateral from being spent, Argon argued in court that such a thing was unnecessary because they had more than enough collateral to pay off their debt to FRS, including $5.5 million worth of leads. By FRS’s calculations, the leads were worth as little as $1,500, not millions. Ultimately, the judge attributed no value to them.

The case was converted to Chapter 7 and FRS should be able to get repaid.

StreetShares Reports $2.8M Loss on Just $277,000 in Revenue For Last Six-Month Period

March 30, 2017 StreetShares, an online small business lender that is self-described as proudly veteran-run, published their most recent financial statements with the SEC earlier this week. For the six-month period ending December 31st, 2016, StreetShares recorded a $2.8 million loss on $277,883 in revenue. Over the same period in the prior year, they recorded a $1.35 million loss on $145,019 in revenue. To-date, the lender has issued $20 million in loans since they first began in July 2014.

StreetShares, an online small business lender that is self-described as proudly veteran-run, published their most recent financial statements with the SEC earlier this week. For the six-month period ending December 31st, 2016, StreetShares recorded a $2.8 million loss on $277,883 in revenue. Over the same period in the prior year, they recorded a $1.35 million loss on $145,019 in revenue. To-date, the lender has issued $20 million in loans since they first began in July 2014.

StreetShares has so far charged off 23 loans for a combined principal balance of $380,804. Charge-off determinations are made after 150 days of delinquency.

The company made history last year by becoming the first lender in the US to be approved by the SEC to use funds from public investors to back loans to small businesses. This was done through Regulation A+ of the Jumpstart Our Business Startups (JOBS) Act. Reg A+ investors make up $656,675 of StreetShares’ liabilities on the balance sheet.

StreetShares currently makes loans to small businesses between $2,000 to $500,000 for terms of three months to three years.

The company also spent more than 5x their revenue on payroll and payroll tax for the six-month period and more than 3x their revenue on marketing expenses.

Earlier this month, StreetShares announced a partnership with Nor-Cal FDC “to assist small business and veteran business owners in obtaining funding needed to win new opportunities.”

In the release, StreetShares CEO Mark Rockefeller said, “we’re eager to provide veteran-owned small businesses with the funding solutions they need to grow.”

In Advance Capital Secures $50 Million In Additional Financing

March 29, 2017New York, NY — On March 27th, Times Square-based In Advance Capital secured a $50 million credit line to continue the rapid growth of its merchant cash advance business. The eighteen-month-old company, led by founders Shalom Auerbach and Thomas Corliss, attributes its portfolio transparency, discipline, and strong relationships with investors as the key contributing factors in securing the additional capital.

“In an industry that is increasingly difficult to access capital, we are very pleased to have earned the confidence of sophisticated investors who have provided capital that aligns their objectives with ours, which is to provide fast and flexible working capital to small business owners experiencing the challenges and opportunities of high growth,” says Shalom Auerbach, IAC’s CEO. In Advance Capital has focused on creating a more streamlined process to facilitate its own growth, including a quicker underwriting process, while seeing 220% more applications within the last two months.

“In Advance is a testament that you can build and grow a company in a competitive industry if you concentrate on hiring top talent, servicing, and listening to your customers,” Corliss says.

“It’s all hands-on deck at In Advance which also makes our work environment a special place to work.”

In Advance is also please to announce its recent Executive Management addition to staff, Keith Nason as Chief Operating Officer. Keith Nason brings over 10 years of expertise to driving operational leverage, streamlining process and data science analytics.

About In Advance Capital

Founded in 2015, the company provides working capital to small business owners. To learn more, visit http://www.inadvancecap.com or call 646-412-3303.