Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

California Lending License Process Isn’t Easy, State Painfully Slow on Paperwork

February 15, 2016 Quarterspot recently became a licensed lender in California. And it wasn’t quick, according to Quarterspot’s EVP Mike Green. It took much longer than a year, he says. Their CFLL license # is “603-K646”, but you can’t confirm that with California’s registry because the database hasn’t been updated in 42 days.

Quarterspot recently became a licensed lender in California. And it wasn’t quick, according to Quarterspot’s EVP Mike Green. It took much longer than a year, he says. Their CFLL license # is “603-K646”, but you can’t confirm that with California’s registry because the database hasn’t been updated in 42 days.

Welcome to the State that apparently has an abundance of resources to launch inquiries into marketplace lenders, but little time to work with the ones eager to operate in full compliance.

California attorney Paul Rianda told deBanked back in December that it can take months just to get a reply on a lending license application. And when they do reply, they’re sticklers over details. “I have experienced a situation where the examiner rejected an application because the name of the company was incorrectly spelled on the application,” Rianda wrote. “The name of the company was submitted on the application with ‘Inc’ instead of the complete ‘Inc.’ at the end of the company’s name.”

Yellowstone Capital’s Isaac Stern said it took them 15 or 16 months to get their license and required a lot of legal help from law firm Hudson Cook LLP. The cost, including lawyers’ fees came to about $60,000. “Man, it was like pulling teeth to get that license,” Stern told deBanked last year.

Tom McCurnin, an attorney for Barton, Klugman & Oetting LLP, disagrees. In an op-ed he wrote for Leasing News to counter a story published by deBanked, McCurnin wrote, “I would point out that the process of obtaining a California license is awfully easy, and involves a small filing fee and a bond.”

But for those not from the leasing industry, “easy” is not a word that comes to mind. “They’ll take away your license if you even sneeze the wrong way,” Stern previously told deBanked.

Worse, a change in the law regarding the payment of referral fees has led to a flurry of questions from lenders and commercial finance brokers alike. Law firm Hudson Cook LLP and Patrick Siegfried of the Usury Law Blog, both even had to weigh in on the issue. (See: Can California Lenders Pay Referral Fees to Unlicensed Brokers? | California Finance Lenders Push Legislative Agenda in Response to Growth of Alternative Small Business Finance Industry)

And even more confusing, is whether or not a license can be transferred. In February of 2015 for example, LoanMe Inc was ordered by the Department of Business Oversight to stop using what they claimed was another company’s lending license. But then a month later, the order was paused upon receiving “additional information” and then withdrawn.

As it stands with the State’s marketplace lending inquiry, 14 lenders have to respond by March. Among them is Kabbage Inc., Prosper Marketplace Inc., Avant Inc., On Deck Capital Inc. and Social Finance Inc., according to the Wall Street Journal.

Neither Kabbage or OnDeck are licensed California lenders from what deBanked could ascertain. But both would be legally eligible to make loans in the State through their chartered bank relationships.

“These online lenders are filling a need in today’s economy, and we have no desire to squelch the industry or innovation,” said DBO Commissioner Jan Lynn Owen in a December announcement.

In the meantime, being a licensed lender in the state is being perceived as a competitive advantage. Quarterspot for example, wants brokers to know that they can do loans in California now. Of course, after having waited painfully long to become licensed, it’s disheartening for them to see that the state hasn’t even updated their records since January 4th.

deBanked attempted to reach out to the California Department of Business Oversight a week ago to find out why their data was so slow to be updated. Nobody responded.

Lending Club TurboTax Integration Attempts to Solve Marketplace Lending’s Tax Problem

February 15, 2016 Lending Club’s retail investors scored big on February 12th when they announced an integration with TurboTax software. The complexity of marketplace lending from a tax perspective has historically been one of the most prohibitive cost barriers for retail investors. Unlike savings accounts which issue a standard 1099-INT, Lending Club (and Prosper) issue both a 1099-OID and a 1099-B.

Lending Club’s retail investors scored big on February 12th when they announced an integration with TurboTax software. The complexity of marketplace lending from a tax perspective has historically been one of the most prohibitive cost barriers for retail investors. Unlike savings accounts which issue a standard 1099-INT, Lending Club (and Prosper) issue both a 1099-OID and a 1099-B.

According to the IRS, the 1099-OID should “state the excess of an obligation’s stated redemption price at maturity over its issue price. Original Issue Discount (OID) on a taxable obligation is taxable as interest over the life of the obligation. If you are the holder of a taxable OID obligation, generally you must include an amount of OID in your gross income each year you hold the obligation.”

For the average person, explanations like these are enough to warrant the help of an accountant. But that’s a problem for people that are investing a small amount. For example, if $10,000 invested in Lending Club notes generated $700 in income for the year, it wouldn’t be practical to pay an accountant $500 to help you figure it all out. Between that and the actual taxes owed, an investor could easily end up losing money.

For the average person, explanations like these are enough to warrant the help of an accountant. But that’s a problem for people that are investing a small amount. For example, if $10,000 invested in Lending Club notes generated $700 in income for the year, it wouldn’t be practical to pay an accountant $500 to help you figure it all out. Between that and the actual taxes owed, an investor could easily end up losing money.

Lending Club tries to make it all as easy as possible for investors with their step-by-step tax guide, but it can still feel a little confusing. One problem to consider is that investors can only deduct up to $3,000 of their losses if they don’t have any other capital gains.

While an integration with TurboTax is a win for retail investors, marketplace lending had long been a thorn in the side for TurboTax. Complaints about the software not being “peer-to-peer friendly” have haunted Intuit’s help pages for years.

Chicago Resumes Call for Protection of Small Business Owners Against Predatory Lenders

February 12, 2016 Chicago City Treasurer Kurt Summers has picked up where Rahm Emanuel left off a year ago. During a January 25th Illinois Senate Financial Institutions Committee hearing named, Small Businesses, lack of access to capital, and predatory lending practices, Summers called for new legislation to protect small business owners from misleading and dishonest predatory lenders.

Chicago City Treasurer Kurt Summers has picked up where Rahm Emanuel left off a year ago. During a January 25th Illinois Senate Financial Institutions Committee hearing named, Small Businesses, lack of access to capital, and predatory lending practices, Summers called for new legislation to protect small business owners from misleading and dishonest predatory lenders.

OnDeck we mean you

Spencer M. Cowan, Senior Vice President for Research, Woodstock Institute, also testified during the hearing and referenced OnDeck specifically. “The terms do not, without calculations that few people can make, let the borrower know that the loan will take a full year to repay with an effective interest rate of just under 70 percent,” he said. Cowan’s position was that banks need to lend more so that small businesses don’t need such alternatives. “If businesses do not have access to loans from banks, then they are probably going to resort to the same types of strategies as consumers who can’t get small loans from banks,” he said.

Cowan cited a report he prepared 18 months ago that examined the relationship between banks and the racial makeup of the small business owners they lend to. The sources he cited about alternative lending were blog posts written by industry critic Ami Kassar.

Treasurer Summers meanwhile recommended the following measures be included in draft legislation to protect small business owners:

- Require loan terms to be clear and unequivocal. Loan terms should be clearly stated using straightforward language and the interest rate should be clearly disclosed as an annualized interest rate or an annual percentage rate (APR).

- Loans should be free from traps. Borrowers should not be hit with new fees on existing principal if they refinance or modify a loan. Borrowers should not be charged interest or periodic costs for the remaining period of the loan if they pay it off early.

- Lenders should be required to display information about the results of their previous loans. This information could be anonymous and in the aggregate, but would give borrowers important data points as they determine whether or not to use a particular lender. If borrowers are able to see that a lender has a pattern of providing loans that are not paid back or have caused businesses to fail, they will be more likely to choose a more reputable lender.

- Conflicts of interest should be disclosed to borrowers. Borrowers should know what types of incentives are driving the lender and whether the broker will receive higher fees for using certain lenders or types of loans.

- Because many of these loans are made online, lenders must take substantial steps to protect the data privacy of loan applicants. Borrower data should not be allowed to be sent to third parties without the written consent of the borrower and lenders should be required to take steps to ensure that the data is encrypted and protected from breaches.

Unsurprisingly, the Illinois Bankers Association (IBA), who was not even invited to the hearing, felt compelled to issue a public statement. In a letter addressed to Chairperson Jacqueline Collins, the IBA was rather protective of their own interests. “We share the Committee’s concern with the proliferation of these under-regulated lenders, sometimes known as ‘fintech’ companies,” they stated. “This relatively new ‘shadow banking’ industry — unlike traditional financial institutions — is in many respects unregulated. Consequently, some bad actors are engaging in predatory lending practices with repayment terms that too often are forcing small business customers into cycles of debt.”

However they tapered down the rhetoric and made a technology-forward plea. “We do think it is important for lawmakers to preserve the benefits of lending innovations, and to ensure that mainstream financial institutions are not prevented from adopting technologies that result in better customer service,” they said. “For example, mobile lending interfaces and faster loan approvals, with appropriate safeguards, provide many potential benefits and match changing customer needs and expectations. We should seek to preserve these innovative solutions that benefit entrepreneurs and small businesses, while at the same time curbing abusive lending practices.”

A public digital transcript of the hearing is not currently available.

Lending Club Borrowers Are Paying Off Really Early – And There’s Something Weird About It

February 11, 2016 This week I surpassed more than 500 lifetime early note payoffs on Lending Club. Considering that loans on the platform are either for a fixed term of 36 months or 60 months, I was quite surprised to see that the average early payoff was happening just 10 months in. My portfolio is too young for even the first loans I ever bought to have reached maturity so the data isn’t entirely statistically relevant. But to put what I’ve experienced so far in perspective, out of every note I’ve ever bought on this platform up to and including today, 17% of them have already paid back early in full.

This week I surpassed more than 500 lifetime early note payoffs on Lending Club. Considering that loans on the platform are either for a fixed term of 36 months or 60 months, I was quite surprised to see that the average early payoff was happening just 10 months in. My portfolio is too young for even the first loans I ever bought to have reached maturity so the data isn’t entirely statistically relevant. But to put what I’ve experienced so far in perspective, out of every note I’ve ever bought on this platform up to and including today, 17% of them have already paid back early in full.

One borrower paid back their 3-year loan in just 8 days!

Of the 145 5-year notes I bought just 20 months ago in May 2014, 36% of them have already paid back in full. This is astounding, but apparently old news. A PeerCube analysis conducted two years ago revealed that 80.6% of all fully paid loans were pre-paid in full before reaching maturity.

At face value, these statistics could be used to boost investor confidence. The loans are so affordable that just look at how many people are paying off early! But according to Anil Gupta at PeerCube, these borrowers might not be paying these loans off at all. Lending Club might be refinancing the loans with a new loan, which cashes out the original investors early in the process. As said in his analysis:

A PeerCube user who is also a borrower on Lending Club mentioned that he has been receiving requests from Lending Club to refinance his loan. Such offers are very attractive to borrowers whose FICO score may have gone up since taking the first loan. In this case, the second loan may come with lower interest rate due to improved credit score. Moreover, there is no deterrent in the form of pre-payment penalty for borrowers to refinance the loan. Lending Club benefits from a borrower refinancing an existing loan by charging additional origination fee from the second loan, i.e. more revenue.

Lending Club’s website says that to be eligible for a second loan, borrowers have to have made 12 months of successful, on-time payments on their existing Lending Club loan. “Sometimes,” however, they “identify customers who are eligible for an additional loan before those 12 months and ask them to apply.” That’s the policy for having two active loans at once, not for refinances specifically.

Lending Club’s quarterly earnings reports make no clear mention of repeat borrowers and there’s no way for an investor to know if the debt consolidation loans they’re taking risks in are really just refinances of existing Lending Club loans. But even if they were, that wouldn’t necessarily make them a bad thing.

Would you rather invest in a borrower who has already proved 12 months of positive payment history OR somebody brand new? But then again, would you rather invest in a refinance of a loan that was originally taken to refinance a credit card?

There’s a downside to loans being paid off early. If an equal reinvestment opportunity does not exist to immediately replace the paid off loan, then the investor loses. If they are no longer reinvesting anyway, then an early payoff deprives the investor of the interest to offset future chargeoffs from the remaining loans that will go bad. And worse yet, investors are forced to pay a penalty to Lending Club for any loan that pays off early after the first 12 months in the form of a 1% fee on all outstanding principal. Seriously, investors are penalized for early payoffs for which they have no control over and are not allowed to know why or how the borrower paid off earlier.

Sounds very weird to me…

Yirendai Gets Smoked on Global P2P Lending Fears

February 10, 2016 The market has turned overwhelmingly bearish on tech-based lending companies lately, but no company has perhaps felt the brunt more than Yirendai, a Chinese company listed on the New York Stock Exchange. Since their IPO less than two months ago, the price has already dropped by more than 60%. Investors seem to be basing that judgment on one thing, the general fear of that business model in China.

The market has turned overwhelmingly bearish on tech-based lending companies lately, but no company has perhaps felt the brunt more than Yirendai, a Chinese company listed on the New York Stock Exchange. Since their IPO less than two months ago, the price has already dropped by more than 60%. Investors seem to be basing that judgment on one thing, the general fear of that business model in China.

And who can blame them? Only a week ago, Ezubao, one of China’s largest peer-to-peer lenders, was revealed to be a $7.6 billion Ponzi scheme. More than 900,000 investors were impacted. The CEOs of more than 250 similar companies there are in hiding after experiencing failures of their own.

On February 3rd, Yirendai announced a framework agreement with China Zheshang Bank Co., Ltd and CreditEase Pucheng.

“I am pleased to announce the cooperation between Yirendai and Zheshang Bank in the field of microloan lending and consumer finance,” said Ning Tang, Yirendai’s Executive Chairman. “This cooperation illustrates Zheshang Bank’s recognition of our strong online operation capabilities. It will provide the opportunity for individual borrowers to receive lower cost funding. ”

The news fell flat and the stock dipped down that day. The company closed at $3.83 yesterday, a new all-time low on no news.

CFPB (and others) Not Amused By Quicken’s Push-Button Mortgage Ad

February 9, 2016Is Quicken in the right place at the wrong time?

Imagine a world where you could get a mortgage at the push of a button. And then imagine like literally pushing that button while you’re sitting in a dark auditorium watching a magic show. As the magician saws a woman in half, you agree to a $400,000 loan payable over 30 years. That pivotal moment, according to Quicken’s vision for American prosperity, will lead to a “tidal wave of ownership” that will flood the country with new home owners.

Consider the implications of that commercial on its own merits (or watch it below of course) and then imagine watching it after you’ve just seen The Big Short in theaters. Given that the movie is a true story about the build-up of the housing and credit bubble in the 2000s that led to a near catastrophic global collapse, a mortgage “tidal wave” might not be the best way to describe your new mobile app.

After Quicken’s push-button mortgage commercial aired during the Super Bowl, the Consumer Financial Protection Bureau responded on twitter:

When it comes to #mortgages, take your time, ask questions and #knowbeforeyouowe. https://t.co/UUaGyWDbzk

— consumerfinance.gov (@CFPB) February 8, 2016

While the mortgage process shown on TV looked overly ambitious, a Quicken customer service rep who I chatted with while posing as a borrower, said that it really can be all done online, even if the mortgage was for like $600,000. When I inquired about what documents I’d need to provide through that process, I was told all I needed to do was state the address of the home.

A no-doc process?

According to the Wall Street Journal, “borrowers can authorize Quicken to access their bank and other financial information directly, eliminating the need for sending pay stubs, bank statements and tax returns back and forth.” So there’s still documents, they’re just electronic and retrieved via APIs.

Having scanned the process, there is clearly more than just one button to push (I counted 9 steps), but it may actually be possible to get a mortgage while watching a magic show. Apparently a lot of people on twitter don’t think that’s a good thing:

Thanks Rocket Mortgage for thinking the '08 housing crisis needed a sequel

— Wyatt Rasmussen (@Wyatt_Rasmussen) February 8, 2016

Let's start another financial collapse. #RocketMortgage https://t.co/7CkBTGJRPD

— Turney Duff (@turneyduff) February 8, 2016

My kid was playing with my phone and bought 7 houses. I can return those right? #RocketMortgage #SB50

— Tim Murphy (@TimMurphy104) February 8, 2016

Rocket Mortgage: explaining the 2008 financial crisis in one commercial

— Rahul Vedantam (@RahulVedantam) February 8, 2016

This commercial is making an excellent case for a massive real estate bubble. It worked awesome in 2007. #RocketMortgage

— Ben Shapiro (@benshapiro) February 8, 2016

Meanwhile, Rana Foroohar, Assistant Managing Editor and Columnist for Time and Global Economic Analyst for CNN, argued that the backlash is unfounded. “No, the Rocket Mortgage Ad Is Not the Sign of Another Financial Apocalypse,” was the headline of her Time story published on Monday. Her evidence? Nobody can afford a mortgage anyway so there’s nothing to worry about, she basically says.

Private equity firm Blackstone has become the largest buyer of single family homes in the country over the last few years. […] Most ordinary Americans need mortgages to buy real estate; at current housing prices and incomes, it would take a typical family more than twenty years to save even a 10% down payment for a home plus closing costs. But they can’t get the loans, because in our post-crisis world, banks are still keeping credit tighter than usual. Besides, many individuals simply don’t have the secure employment, nest egg, and increasingly high credit scores needed to obtain a mortgage these days.

– Rana Foroohar

http://time.com/4212259/rocket-mortgage-super-bowl-ad/

See? There can’t be a bubble brewing because nobody can possibly qualify.

So when Quicken makes wildly provocative sales pitches like this:

Push Button. Get Mortgage. https://t.co/UzOXYFF25C#RocketMortgage 🚀🚀🚀

— Quicken Loans (@QuickenLoans) February 8, 2016

What they’re really apparently trying to say is that the process for those that qualify is supposedly more transparent and therefore better for borrowers:

.@CFPB We agree. No better way than #RocketMortgage for full transparency into mortgage options & info needed to make the right decision.

— Quicken Loans (@QuickenLoans) February 8, 2016

Of course, it probably doesn’t help when their legal help page is titled “legal mumbo jumbo.”

Quicken CEO Bill Emerson tried to clarify the message of the commercial to the WSJ. “What we’re saying is that a strong housing market filled with responsible homeowners is important to the economy,” he said.

Don’t worry about the mumbo jumbo folks, just push button, get mortgage.

—

What do you think? Is Quicken walking down a slippery slope?

Former Bizfi Manager is Making a Splash in Delaware State Senate Contest

February 7, 2016 A former Bizfi manager is underwriting a new kind of 4-year deal. Thirty-two year old James Spadola, who lives in Wilmington, is bringing an impressive resumé to the Delaware state Senate contest for District 1.

A former Bizfi manager is underwriting a new kind of 4-year deal. Thirty-two year old James Spadola, who lives in Wilmington, is bringing an impressive resumé to the Delaware state Senate contest for District 1.

The world knows him as #HugACop after an outreach campaign he spearheaded for the Newark, Delaware police department went viral and inspired a new era of positive policing. Spadola has served as an officer there for more than 7 years.

He attended the University of Delaware, an experience that was interrupted when he was called up by the U.S. Army Reserve to take a tour of duty. Deployed in March 2003 for a year, he served as a prison guard and as his battalion commander’s gunner and driver in Iraq. He received the Combat Action Badge when his convoy was hit with an IED.

After returning home and graduating, Spadola moved to New York City and got a job at a hot new fintech startup named Merchant Cash and Capital (MCC). That was in February 2007, making him one of the company’s first ten employees. MCC Changed their name to Bizfi in September of 2015.

As an underwriter, Spadola was tasked with evaluating working capital applications submitted by small businesses. He was quickly promoted to Team Leader and later to Underwriting Manager, a senior departmental position.

Spadola told deBanked of his time there, “I had a great experience at Bizfi and learned an enormous amount about the private sector and the troubles and challenges that small business owners deal with everyday.”

Bizfi General Manager Seth Broman, said of him, “having worked closely with James for several years, it was apparent to me and all those around him that James has a knack for helping those in need.”

After almost two years there, he moved to Delaware to join the Newark Police Department, where he’s been ever since. He still managed to find the time to get his MBA from Wilmington University in 2014.

Today, Spadola is underwriting a new kind of challenge, competing against incumbent state legislator Harris McDowell who has been in office since 1976. Running as a Republican in a blue state, Spadola thinks it’s time for new blood.

“I look forward to putting those business lessons, coupled with what I’ve learned through my other professional experiences, into practical application down at Legislative Hall,” he told deBanked.

Visit his campaign Facebook page.

E-mail james@jamesspadola.com for further information.

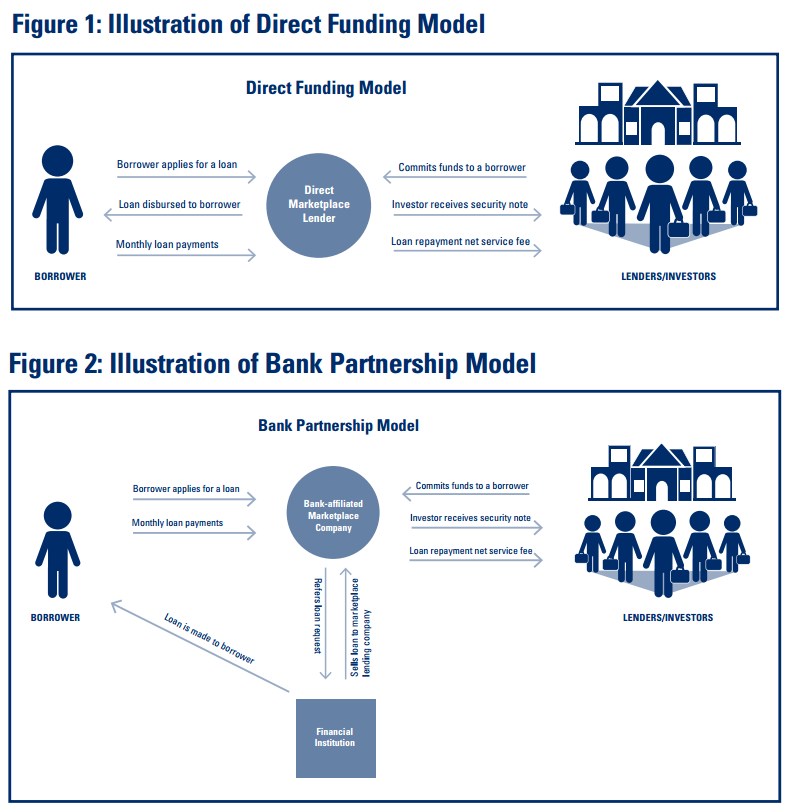

How the FDIC Defines Marketplace Lending

February 5, 2016Marketplace lending is one of this year’s hottest buzzwords but its meaning is not very intuitive. According to a recent Federal Deposit Insurance Corporation (FDIC) report, “marketplace lending is broadly defined to include any practice of pairing borrowers and lenders through the use of an online platform without a traditional bank intermediary.” This might sound similar to peer-to-peer lending and that’s because it’s the same thing, the FDIC explains. “Although the model, originally started as a ‘peer-to-peer’ concept for individuals to lend to one another, the market has evolved as more institutional investors have become interested in funding the activity. As such, the term ‘peer-to-peer lending’ has become less descriptive of the business model and current references to the activity generally use the term ‘marketplace lending.'”

Voilà, marketplace lending is what you get when peers are replaced by private equity firms, pension funds, and hedge funds. Additionally, there is a general assumption that the intermediary platform is also underwriting and grading the loans.

The FDIC separates marketplace lenders into two categories, the “direct funding model” and “bank partnership model,” both of which are illustrated below:

In both circumstances, investors are actually buying securities, rather than participating in the loans themselves.

The FDIC says that marketplace lending can encompass unsecured consumer loans, debt consolidation loans, auto loans, purchase financing, education financing, real estate loans, merchant cash advance, medical patient financing, and small business loans.

For even more information, read the official report.