Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

The Yield Bubble of Marketplace Lending

March 2, 2016 There was a twinkle in his eye, the sort of glimmer one gets when they’ve just learned of a hidden treasure. “It’s called marketplace lending,” I said to him, “and it allows you to invest in loans online. It can be a nice way to diversify your overall portfolio.”

There was a twinkle in his eye, the sort of glimmer one gets when they’ve just learned of a hidden treasure. “It’s called marketplace lending,” I said to him, “and it allows you to invest in loans online. It can be a nice way to diversify your overall portfolio.”

The more I described it, the more it whet his appetite. “Yes, I like it. That sounds awesome,” he said, followed by a huge toothy smile. I was the one seemingly drawing a map to the secret trove of Wall Street riches. Marketplace lending, whatever my old college friend was envisioning it to be, was going to make him a millionaire. He was sure of it. All this techie stuff was involved, big name financial institutions were backing it and Silicon Valley all-stars were driving it. It was all very exciting to him.

“I’m making about 7% on one platform and like 9% on another one, but those are the,” I was saying until he interrupted me.

“–WHAT?! THAT’S IT?”

His dreams crushed by the potential for only single digit returns, he could only laugh at himself for dreaming so big and then at me for thinking numbers like that were worth discussing at all.

I was almost sorry I brought it up.

Somewhere out there, American Greed‘s Stacy Keach is probably shaking his head. On the TV show that he famously narrates, guest law enforcement officials regularly warn people that double digit investment returns are a sure sign of a Ponzi scheme or fraud. Worse, they advise that smart scam artists advertise lower rates like 7-9% so as not to arouse suspicion. The moral of every story? Even those enticed by single digit percentage returns as high as those are partially guilty for being scammed because they too were driven by blinding greed.

And yet there are opportunities to all kinds of people these days that have never have been available before in the past. I know individual investors who regularly make over 20% a year in commercial financing and seriously believe that anything less is an outrage. There are those touting success by earning only 9% through consumer lending and writing blogs to share exactly how they did it. And then there are people who look to double or triple their money and succeed at it.

How to reconcile these new classes of investors in a near-zero interest rate environment when my local bank is paying 5 basis points annually on a savings account and up to 60 basis points annually on a high-yield investment? At times I feel like I am stepping into an alternate reality. Just recently, my bank pitched me on a structured investment that would still gross less than 1% a year. It was presented as something exclusive, exotic and high risk. That’s supposedly why the yield was so high. It was the kind of risk that required a minimum $250,000 investment, you know to see if I was serious about sitting at the big boy table of yield. And we were seriously talking about 60 basis points…

The buildup on their presentation fell so flat that I laughed at myself and then at them for thinking that it was worth discussing at all. Deja vu.

The first time I ever invested in a merchant cash advance, it was at a 1.49 factor rate. It had the potential to cycle through to completion in just two to three months. Do a few of those a year as a passive investor and you could earn triple digit percentage returns. Not a scam, not a Ponzi, totally legit. It was a seemingly real hidden treasure.

The deal went bad in the 2nd week and I took an almost complete loss on my investment. With great reward comes great risk, but I knew that already. I participated in more deals and lo and behold was able to generate double digit percentage returns even after defaults and commissions.

Double digit returns are a real thing. Peter Renton’s investment in the Direct Lending Fund is earning 13.29% according to his latest update. The Direct Lending Fund “owns a diversified pool of high-yielding, 3-36 month business notes. The notes are purchased from a number of lenders including IOUCentral.com and QuarterSpot,” according to their website. “These lenders make loans to qualified, established businesses that fit our strict filtering criteria.”

While very impressive, the fund’s returns are not too good to be true. CNBC labeled it a new flavor of fixed income when interviewing the fund’s founder. In that interview, it was said that returns are ranging from 6% to 14% and that access could soon be open to unaccredited investors as well. Lending Club, a publicly traded loan marketplace, advertises that 99.9% of its investors that buy 100+ notes on their platform have earned positive returns, a fantastically alluring statistic.

My bankers assured me no such investments could legitimately exist. Yet these yields are typical for marketplace lending investors today, and would be considered outrageously low to commercial financing’s high risk crowd. To that end, I know investors that have doubled and tripled their money over a few short years. If they could narrate their own version of American Greed it would be to say that 7% definitely is a sign of criminal intent, because it’s criminally low. “Never settle for less than double digit returns,” I imagine they would advise.

Marketplace lending has created investing anomalies. What shouldn’t be, is. It’s a bad time to be out of the loop. And it’s a bad time to put $250,000 in a non-FDIC insured investment that earns less than 1% a year. There’s always the stock market, you know, if you’re in to that kind of thing. Nobody I know ever talks about the stock market. It’s goes up, it goes down. It can be very emotional.

The new way to avoid the roller coaster is marketplace lending. These returns for the little guy are not supposed to exist and yet they do. 6%, 7%, 9%, 20%, 100%. Take your pick.

Yield is out there.

Letter From the Editor – March/April 2016

March 1, 2016 In early 2016, a recession seemed inevitable, until it didn’t. Rumors of rising defaults across a variety of marketplace lenders have been defended as falling within model estimates. The stock market’s sudden plunge recovered. And Madden v Midland’s long-term impact is being chalked up as overblown. All is well again, well mostly anyway. Institutional investors have gotten a little spooked and the once insatiable appetite seems to have become just a little bit satiable.

In early 2016, a recession seemed inevitable, until it didn’t. Rumors of rising defaults across a variety of marketplace lenders have been defended as falling within model estimates. The stock market’s sudden plunge recovered. And Madden v Midland’s long-term impact is being chalked up as overblown. All is well again, well mostly anyway. Institutional investors have gotten a little spooked and the once insatiable appetite seems to have become just a little bit satiable.

But we’re back, and so is the beast that has come to be known as “marketplace lending.” The FDIC says that term can encompass unsecured consumer loans, debt consolidation loans, auto loans, purchase financing, real estate loans, merchant cash advance, medical patient financing, and small business loans. It can “include any practice of pairing borrowers and lenders through the use of an online platform without a traditional bank intermediary,” they wrote in their Winter 2015 Supervisory Insights report.

In this issue, we examined one piece of marketplace lending that has created many success stories, the merchant cash advance industry. For years, it’s turned hungry 20 somethings into front-page worthy stars. Will that trend continue or has the moment passed? The quality of leads will play a role in who makes it big and who doesn’t, said some of the folks we interviewed. Ironically, while the industry is often considered to be online, the Internet is reportedly becoming a less reliable place to acquire customers because of competition and cost. Having problems with leads? You’re not alone, we’ve learned.

But not everyone is struggling. In March, we published a list of the top 8 alternative small business funders of 2015. The numbers were either reported to us directly or we determined them using publicly available information. In this issue, we’ve got the year-over-year statistics for 18 companies. Some of them might surprise you.

I don’t want to finish off my introduction to this issue with the R-word, but since there were signs of weakness earlier this year, we did ask the wider marketplace lending industry what to expect from the next recession. Everything is at risk, they said, from borrower defaults to institutional backing to regulatory action. Marketplace lending, however big and strong it is now, is not believed to be impervious to market forces. Will the beast prevail? Or is it destined to fail?

–Sean Murray

Task Force Convenes to Investigate Terrorism Financing

March 1, 2016 It’s a hearing that the country probably wishes it didn’t have to have. But after it was discovered the San Bernardino terrorists had obtained a loan from an online lending marketplace, government officials and news media wondered if something could’ve been done to prevent it.

It’s a hearing that the country probably wishes it didn’t have to have. But after it was discovered the San Bernardino terrorists had obtained a loan from an online lending marketplace, government officials and news media wondered if something could’ve been done to prevent it.

Today, members of the House Committee on Financial Services are convening the terrorism financing task force for a hearing titled, “Helping the Developing World Fight Terror Finance.”

“As terrorist financing and other illicit financial activity continues to pose risks to the international financial system, some have called for greater [anti-money laundering / combating the financing of terrorism] cooperation between, and among, national and international agencies,” reads a memo circulated in advance of the hearing.

Back in December, committee spokesman Jeff Emerson said that the task force was expected to look at whether any new regulations are needed after the San Bernardino shootings, according to the Los Angeles Times.

The Hill reported that when asked whether online lenders would get extra scrutiny, Committee Chairman Jeb Hensarling said, “Everything’s on the table.”

In the latest memo however, the words online, marketplace lending, Prosper and other related terms were not on the agenda, but that may be perhaps because the focus of this hearing is on the “developing world.”

The last time this task force was convened was a month ago on February 3rd, when they held a hearing titled, “Trading with the Enemy: Trade-Based Money Laundering is the Growth Industry in Terror Finance.” Online lending was not part of that agenda either.

It is uncertain if online lending will actually become a focus or be discussed by this task force in the future. At this point, it does not appear to be a pressing matter.

CFPB To Begin Accepting Small Business Loan Complaints

February 29, 2016 Unhappy with your small business loan? The CFPB wants you to complain to the federal government about it. Small business loans including term loans, credit lines, and business credit cards, among other products, and lenders both small and large banks and non-banks such as online or marketplace lenders will soon all answer to the CFPB.

Unhappy with your small business loan? The CFPB wants you to complain to the federal government about it. Small business loans including term loans, credit lines, and business credit cards, among other products, and lenders both small and large banks and non-banks such as online or marketplace lenders will soon all answer to the CFPB.

“Subject to an assessment of feasibility, the Bureau’s consumer response team will build the infrastructure to intake and analyze small business lending complaints,” a new priority report says.

That would add a new category alongside mortgages, student loans, vehicle loans, and payday loans.

Accepting these reports will likely mean that small business lenders would have to respond directly to the CFPB. Companies who receive a lodged complaint typically have 15 days to provide an answer. Both the complaint and the answer are stored in a public database that anyone can view.

In their report, the CFPB states that “existing research suggests that significant discrimination against minorities may exist in the small business lending market.” However, no link to any such research is provided and historically they’ve made such judgments (with stunning inaccuracy) by guessing the racial makeup of last names.

The CFPB accepts a wide range of complaints. Some companies have been reported simply because a company representative came off as rude over the phone. In other cases, company customer service was reportedly too slow or website outages caused undue stress.

Small business lenders can’t be penalized by the CFPB, but receiving a disproportionate number of complaints could certainly place one on a regulatory radar.

Over the next two years, “the Bureau will build a small business lending team and begin market research and outreach for rulemaking on business lending data collection,” the report promised.

PayPal’s Merchant Cash Advance Program Grows, Performance Improves

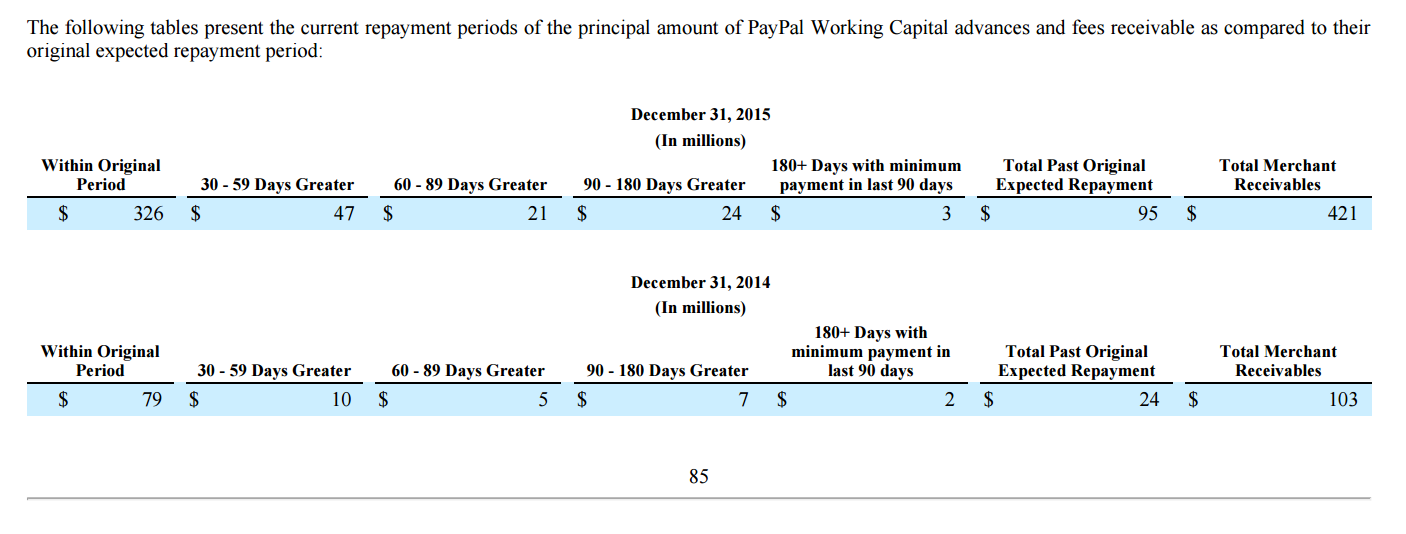

February 27, 2016The PayPal Working Capital program has advanced more than $1 billion to small businesses since inception. Rooted in merchant cash advance methodology since PayPal withholds a percentage of each transaction until receiving payment in full, they are not actually buying future receivables. Rather, they originate loans through WebBank, the same Utah-chartered industrial bank that OnDeck uses. But OnDeck’s payments are fixed and PayPal’s are tied to sales activity.

PayPal’s loans therefore don’t have a fixed term but they evaluate historical sales activity and use that to project a loan payoff usually within 9 to 12 months. According to their Q4 2015 earnings report, their 2015 results performed just as well if not better than their 2014 results.

$421 million was outstanding at the end of 2015 compared to $103 million at the end of 2014. 77% of the $421 million was on pace to pay off within 30 days of their planned projections. 11.16% was on pace to finish 30-59 days beyond them. PayPal broke it down by dollars in their earnings report.

But we’ve broken it down into percentages below:

| Total outstanding balance | Within Projections | 30-59 days greater | 60-89 days greater | 90-180 days greater |

| $421 million | 77.43% | 11.16% | 4.99% | 5.70% |

| Total outstanding balance | Within Projections | 30-59 days greater | 60-89 days greater | 90-180 days greater |

| $103 million | 76.70% | 9.71% | 4.85% | 6.80% |

PayPal borrowers cannot simply stop accepting PayPal payments in order to avoid loan repayment. They are required to pay at least 10% of their total loan amount (loan + the fixed fee) every 90 days so that they make consistent repayment progress regardless of their sales volume. Notably, their website warns, “If you do not meet the requirements in the above policies and your loan goes into Default status, your entire loan balance could become due and limits could be placed on your PayPal account.” For businesses that depend on PayPal sales, that is certainly a downside worth avoiding.

Lending Club Shifts Fee Arrangement With WebBank

February 26, 2016 It’s a “belt and suspenders” precaution according to Lending Club CEO Renaud Laplanche. The Madden v Midland case has forced the company to rethink their arrangement with WebBank, the chartered bank that allows them to make loans nationwide. Under the new terms, the fee LendingClub pays to WebBank for the loans it issues will be related to how the loans perform over time.

It’s a “belt and suspenders” precaution according to Lending Club CEO Renaud Laplanche. The Madden v Midland case has forced the company to rethink their arrangement with WebBank, the chartered bank that allows them to make loans nationwide. Under the new terms, the fee LendingClub pays to WebBank for the loans it issues will be related to how the loans perform over time.

Even if the U.S. Supreme Court were to rule unfavorably in Madden, Lending Club would still have been able to operate freely under their old arrangement. The change then may be a response to several cases, including ones that have accused online lenders of using chartered bank relationships to carry out alleged abuses. According to law firm Ballard Spahr, a “federal court refused to dismiss Pennsylvania racketeering claims against companies alleged to have partnered with a state bank to market Internet loans illustrates the risks inherent in these relationships and the importance of proper structuring.”

In a brief, Ballard Spahr wrote:

In Commonwealth of Pennsylvania v. Think Finance, Inc., et al., the Pennsylvania AG, working with a well-known private plaintiffs’ firm, claimed that the companies and their individual principal had engaged in a “rent-a-bank” scheme in which a Delaware state bank “acted as the nominal lender while the non-bank entity was the de facto lender—marketing, funding and collecting the loan.”

By WebBank maintaining an interest in the outcome of the individual loans, Lending Club will reduce its potential standing as the de factor lender.

Notably, the breaking story focused on Lending Club. WebBank also has a relationship with others in the alternative finance community such as CAN Capital, Prosper, AvantCredit and PayPal. It’s uncertain if their arrangements will also be subject to change.

OnDeck (ONDK) Stock Continues to Sink. Now What?

February 26, 2016OnDeck reached another new all-time low share price on Thursday, closing at $6.35 but hitting $6.05 intraday. The continued spanking follows their 2015 earnings release that apparently did not impress the market. And there’s many reasons to be troubled by that since the tone of the earnings call oozed of renewed confidence. It was expressed as much in OnDeck Regains Their Swagger in Q4 Earnings Call – Lends $1.9 Billion in 2015

OnDeck can’t win. When growth was high, critics complained about profitability. When OnDeck achieved profitability, critics complained that growth had slowed. On Wednesday, critics hit them with the kitchen sink. Growth has slowed, losses are mounting, guidance was revised down, the JPMorgan Chase partnership isn’t yielding revenue, operating expenses rose, etc.

The real problem now is that they can’t seem to overcome these objections during a period of economic calm. The stock market is currently operating at rather rational levels. The S&P 500 is only down 3% year-to-date. OnDeck is down 35% over that same time period.

In a recession, financial companies can be uniquely vulnerable to irrational fear. JPMorgan Chase for example, lost more than 50% of their market cap between August 2008 and February 2009. This is a nightmare scenario now for OnDeck.

“These companies have been valued as if there’s really no credit risk or capital-markets risk whatsoever,” said Bill Ryan, an analyst at Portales Partners, to the WSJ. “I think that’s what changed.”

“We are not seeing weakness in our portfolio at this time,” said OnDeck CEO Noah Breslow during the earnings call.

Apparently that doesn’t matter and one has to wonder what will in the future.

No, Social Media isn’t the New Credit Score

February 25, 2016 The “social media is the new FICO score” crowd suffered a blow on Wednesday when a Wall Street Journal article reported that it ain’t working too good.

The “social media is the new FICO score” crowd suffered a blow on Wednesday when a Wall Street Journal article reported that it ain’t working too good.

Almost 3 years ago, Kabbage co-founder Marc Gorlin told CNN that small businesses who link up their facebook and twitter accounts up with their system, were 20% less likely to be delinquent on their loans. Around that time, Hong Kong-based Lenddo was heralding other positive claims about the value of social media. In the loans they made in Colombia and the Philippines for example, Slate reported that “they scrutinized the applicants’ connections on Facebook and Twitter and that the key to getting a successful loan from Lenddo was having a handful of highly trusted individuals in your social networks.”

For a time, non-bank lenders were saying that social media was the future of credit. That is until it wasn’t.

The WSJ recently reported that lenders are backing away from social media data because it’s becoming harder to tap into and because of the potential regulatory consequences under fair credit laws. Just last month for example, the FTC published a report titled, Big Data, A Tool for Inclusion or Exclusion? In it, the FTC warned that “if a company targets services to consumers who communicate through an application or social media, they may be neglecting populations that are not as tech-savvy.” The implication is that there is potential for unconscious and unintended discrimination of certain minority groups. “Systemic disparate treatment occurs when an entity engages in a pattern or practice of differential treatment on a prohibited basis. In some cases, the unlawful differential treatment could be based on big data analytics.”

But even then, companies like Kabbage have seemingly softened their stance on the value of social media anyway. “Who your social circle is, or whether you play ‘Mafia Wars’—we haven’t seen that as very valuable,” Kabbage CEO Rob Frohwein said to the WSJ.

Facebook is restricting the depth of data available to third parties now anyway. As a result, dozens of startups (not just lenders) that had been using Facebook data have shut down, according to the WSJ.

Lenders like OnDeck might not be surprised by the industry’s sudden realization. Two years ago at LendIt 2014, company CEO Noah Breslow said you have to be careful with the noise of social media as there can be a lot of false signals. And RapidAdvance COO Joe Looney was already telling CNBC three years ago that his company was “not going to make a decision based solely on a string of online comments on a social-media site” even though they would consider the mere presence of an active social-media footprint to be a “good sign.”

It looks like the future of credit scoring isn’t likely to be social media any time soon. All hail the fundamentals.