Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

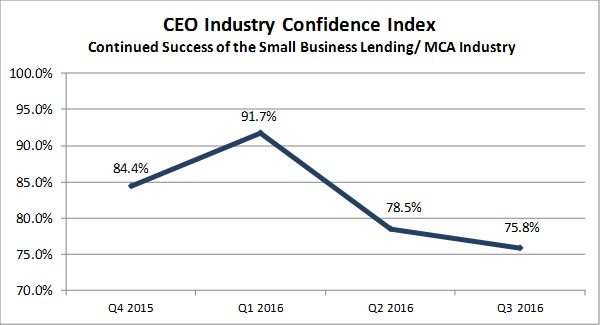

Q3 2016: Confidence in the Small Business Financing Industry’s Success Down Slightly

November 29, 2016Confidence in the industry’s continued success was down among small business financing CEOs in the third quarter, according to the latest survey conducted by Bryant Park Capital and deBanked. At 75.8%, it’s the lowest level recorded since surveying began late last year.

Respondents were not asked the reasoning for their confidence score, but the sentiment may have been influenced by what seemed like an impending Clinton presidency at the time and the 4 more years of regulatory pressure on financial services that would’ve continued as a result. The survey was conducted before the election. Also, the correction taking place in the consumer space with companies like Prosper and Avant have allowed a general feeling of pessimism to waft through the alternative financing universe.

Still, at 75.8%, which is still well into positive territory, the mood is probably best described as cautiously optimistic. The euphoria in Q1 at 91.7%, preceded the resignation of Lending Club’s founder and CEO, which symbolically burst alternative lending’s bubble.

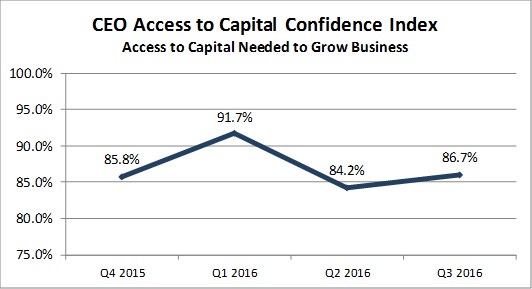

Curiously, industry CEOs were slightly more confident in their ability to access capital needed to grow their business. Respondents were not asked what their capital source options were or the respective costs, but it signals that there are still plenty of investors interested in the space.

Bryant Park Capital and deBanked also produce a comprehensive full-year industry report, available to anyone for $495. To purchase the 2015 report, you can contact me at sean@debanked.com

The History of Alternative Finance (As Told Through Memes)

November 21, 2016Exactly four years ago, I honored the Thanksgiving holiday by slightly exaggerating the industry’s history in a blog post. And every year around this time since, I’ve reposted it to the home page for all the newbies to enjoy. But in 2016, it just doesn’t seem as applicable. Too many things have changed, especially compared to when I first joined the industry.

The technological experience I remember as an underwriter back in 2006 might as well have been the 1700s. From my perspective, here’s how things have changed:

I don’t know about you, but I am afraid to see where we will be in 2026.

Happy Thanksgiving! 🙂

The Season Finale of Alternative Lending Has Everything You’d Expect

November 17, 2016

This month kicked off what appears to be the first segment of the 2016 two-part season finale of alternative lending. So far, it has everything you’d expect, a main character gets killed off, another simply won’t be returning next season, a wedding, a scandal and even a cliffhanger!

So in that precise order, here’s what you missed:

A main character’s surprising death

Crowdfund Insider reported on Wednesday that Dealstruck, a small business lender, had ceased lending operations. An email sent to Dealstruck has not yet been returned, but Crowdfund Insider’s story includes a quote from Dealstruck’s CEO saying that the company is no longer originating new loans.

The company initially arrived on the scene to much fanfare. A writeup in techcrunch last year said that they had raised $8.3 million in venture financing and secured a $50 million credit facility.

Guess who won’t be back next season

Aaron Vermut is stepping down as Prosper Marketplace’s CEO. He is being replaced by company CFO David Kimball. Vermut’s father, Stephan Vermut is also stepping down as executive chairman.

A wedding between an old character and a new one

Peerform, which was founded in 2011, has been acquired by Versara Lending. Versara, an unfamiliar name, appears to be related to NYC-based Strategic Financial Solutions, a debt relief company headed by Ryan Sasson. Peerform CEO Mikael Rapaport has updated his LinkedIn profile to reflect a new role at both Versara and Strategic.

Scandal! The fake business loan negotiator from upstate New York has been arrested

His name is Sergiy Bezrukov, but the world may know him by another name (or three), John Butler, Thomas Paris or Christopher Riley. After terrorizing the MCA and business lending industry for almost a year, he now sits in prison awaiting trial.

Cliffhanger

Oh, so you thought Prosper would file their 10-Q on Tuesday? You were wrong. The company instead informed the SEC that they would be filing their report late, leaving loan investors wondering if there may be more to the recent executive departures.

Stay tuned!

If this were really a TV show, you’d probably think it jumped the shark when the country elected a President that pledged to dismantle Dodd-Frank while potentially defanging the CFPB. But that is precisely what has happened. “The Dodd-Frank economy does not work for working people,” the President-Elect’s website states. “Bureaucratic red tape and Washington mandates are not the answer. The Financial Services Policy Implementation team will be working to dismantle the Dodd-Frank Act and replace it with new policies to encourage economic growth and job creation.”

If anything, this is all the more reason that you should be tuning in and following the industry in 2017.

The Status of Prosper Marketplace???

November 16, 2016 Loan investors will have to wait even longer to find out if the resignation of Prosper’s chief executive on Monday holds special significance. That’s because on Tuesday the company informed the SEC that they would be filing their 3rd quarter results late. They were unable to complete the report in a timely manner, according to the filing, “without unreasonable effort or expense due to a delay experienced by the Registrants in completing its financial statements and other disclosures in the Quarterly Report relating to a recent arbitration decision.”

Loan investors will have to wait even longer to find out if the resignation of Prosper’s chief executive on Monday holds special significance. That’s because on Tuesday the company informed the SEC that they would be filing their 3rd quarter results late. They were unable to complete the report in a timely manner, according to the filing, “without unreasonable effort or expense due to a delay experienced by the Registrants in completing its financial statements and other disclosures in the Quarterly Report relating to a recent arbitration decision.”

Jay Antenen, the Senior Editor for DealReporter, said on twitter that the arbitration reference has to do with “the early 2013 loan purchase agreement Prosper signed with Colchis.” According to a brief Antenen published with Eleanor Duncan on Debtwire, “Under that deal, Colchis gained the right to see Prosper’s origination pipeline and bid for loans at no disadvantage to other investors on the platform.” Apparently, there may be some tension between Colchis and new investors.

This all belies the fact that Prosper’s previous quarter produced a gut-wrenching $35.5 million loss on just $28 million in revenue. They had $14 million in expenses just from restructuring related to their downsizing and layoffs which included the closing of their Salt Lake City office and the termination of 167 employees. Their first quarter of the year yielded a $17 million loss on $56.5 million in revenue.

Meanwhile, loan performance has remained fairly steady, even as they continue to make regular pricing adjustments.

On Monday, the company’s CFO, David Kimball, was promoted to CEO to take over Aaron Vermut’s role. Vermut will remain on the company’s board.

The Art of The ‘Thiel’ – With Fintech Leader On Trump’s Transition Team, Alternative Lenders Could Benefit

November 13, 2016

Peter Thiel is famous for a lot of things, co-founding PayPal, backing Hulk Hogan’s lawsuit against Gawker and being a billionaire venture capitalist, just to name a few. Accustomed to shaking up Silicon Valley with his investments and antics, these days Thiel stands to impart his wisdom on another region, Washington DC. That’s because last week he became part of the Executive Committee of President-Elect Trump’s transition team.

After speaking at the 2016 Republican National Convention and donating $1.25 million towards Trump’s election efforts, his allegiance to the campaign should come as no surprise. His support is said to be genuine too, and that’s perhaps because the two have relied on similar rhetoric to make their points.

“Competition is For Losers”

Who said that quote? If you thought Donald Trump, you’re wrong, but you wouldn’t be blamed for thinking that given that so much of Trump’s mantra was focused on America “winning.” Competition is For Losers is the title of a 2014 Wall Street Journal essay penned by Thiel, that argued a perfectly competitive marketplace, an economic utopia, is flawed. “In business, equilibrium means stasis, and stasis means death,” he wrote. Entrepreneurs should instead strive for a monopoly, to win, he explained.

Winning is certainly something Thiel has done a lot of, making him a role model of the Trump credo.

“I think they should be described as terrorists, not as writers or reporters.”

Who said that quote? If you thought Donald Trump, you’re wrong, but you wouldn’t be blamed for thinking that given Trump’s hostility towards the media. Thiel said that in 2009 about Gawker reporters, and he bottled up that disdain and unleashed it in the form of financial support for Hulk Hogan against Gawker in a lawsuit years later, the force of which crippled Gawker and put the company into bankruptcy. It’s a revenge narrative that sounds oddly Trumpesque.

While there are likely more contrasts between the two men than similarities like these, both share a special penchant for winning. And more to the point, in a Trump presidency, Thiel may have his ear.

That should be welcome news to fintech and alternative lenders, given Thiel’s strong financial interest in that sector. Small business lender OnDeck has already experienced a 43% increase in its stock price since Trump was announced the winner. Enova, which bought merchant cash advance firm The Business Backer, is up 13%. That’s no doubt in part a result of Trump’s campaign promises to put a moratorium on financial regulations and recent pledge to dismantle the Dodd-Frank Act.

But with Thiel, his ties to alternative lending and fintech were made evident when he gave the keynote speech at LendIt earlier this year in San Francisco, in which he colorfully reiterated his theory about competition being a losing endeavor. “If you want to compete like crazy, you should just leave the conference and try to open a restaurant in San Francisco,” he said.

Thiel participated in SoFi’s $80 Million Series C round and Avant’s $225 million Series D round. “There are a lot of banks in the United States, but not enough access to credit,” he said in an announcement for the latter at the time.

He also participated in ZestFinance’s Series C round and both OnDeck’s D and E rounds.

And more recently, his VC fund, Founder’s Fund, led the $100 million Series D round of Affirm. The fund has also invested in Able Lending, BitPay and Upstart.

Last month, Phin Upham, a principal of Thiel Capital, another of Thiel’s investment firms, dismissed Goldman Sachs’ recent attempt to cash in on tech-based lending. “I wonder if Goldman will actually be able to keep up, because this is not a mature industry, everything changes sometimes within months.”

The NY Times reported that Thiel will not be moving to Washington and may not have a formal role in the administration, but that he will have a voice.

“A page in the book of history has turned, and there is an opening to think about some of our problems from a new perspective,” the Times reported Thiel saying. “I’ll try to help the president in any way I can.”

If truly given the opportunity to do so, Thiel’s influence could be a boon to fintech and the larger economy as a whole.

At the Money2020 conference last month, Trump was largely and quite openly derided by industry leaders. They may soon be changing their tune.

Other members of the Executive Committee of the transition team include:

- Congressman Lou Barletta

- Congresswoman Marsha Blackburn

- Florida Attorney General Pam Bondi

- Congressman Chris Collins

- Jared Kushner

- Congressman Tom Marino

- Rebekah Mercer

- Steven Mnuchin

- Congressman Devin Nunesv

- Anthony Scaramucci

- Donald Trump Jr.

- Eric Trump

- Ivanka Trump

- RNC Chairman Reince Priebus

- Trump Campaign CEO Stephen K. Bannon

It is quite possible that we may soon be making fintech ‘Great Again’

With Trump and Co. Now in Control, Has The CFPB Made a Costly Mistake?

November 11, 2016 For years, the CFPB has rejected all calls by republicans (and even some democrats) to reconfigure its one-director leadership to a multi-member commission. At present, Director Richard Cordray has full authority to create the rules and enforce the rules and reports to no one, not even the President of the United States. As the only executive agency with significant authority to operate in this manner, critics have become increasingly worried the CFPB might abuse its power. And just last month, the agency was accused to have actually done so.

For years, the CFPB has rejected all calls by republicans (and even some democrats) to reconfigure its one-director leadership to a multi-member commission. At present, Director Richard Cordray has full authority to create the rules and enforce the rules and reports to no one, not even the President of the United States. As the only executive agency with significant authority to operate in this manner, critics have become increasingly worried the CFPB might abuse its power. And just last month, the agency was accused to have actually done so.

In PHH Corp. v. CFPB, the CFPB was alleged to have made legal errors in their enforcement action against a mortgage lender, but more to the point, that the CFPB itself was unconstitutional. The United States Court of Appeals for the District of Columbia Circuit agreed in part, ruling the agency’s structure unconstitutional. The agency was ordered to cure the defect either by conceding its directorship to a multi-member commission or making its leader report directly to the President of the United States.

But the CFPB has refused to comply, arguing shortly thereafter in another case that the “decision was wrongly decided and is not likely to withstand further review,” amplifying fears that the agency had gone rogue and potentially become drunk with power.

Cordray, who has tried to assure critics that his agenda is merely meat and potatoes, now faces a new challenge, a Republican president and a Republican-controlled Congress, who may see this as their only opportunity to rein him in.

According to Bloomberg, sources contend that the CFPB’s and Democrats’ previous unwillingness to concede anything at all, now puts the entire agency itself in jeopardy. Cordray himself is at great risk of losing his job, the Huffington Post asserts.

Already there is chatter of firing Cordray on Trump’s first day in office either for cause as Dodd-Frank allows for, or simply at his own discretion, as the Appeals Court ruled would be acceptable.

Has the CFPB erred all this time?

The Remedy For a Bad Industry Decision?

November 9, 2016 A recent disappointing New York trial court decision concerning merchant cash advances has been making the rounds over the past few weeks and a few industry players have been asking if there is cause to be concerned. While the case will likely have little precedential value, it should serve as a reminder to all funders and ISOs in the industry to invest resources where they matter; on employee education, contract review, legal representation, and customer service.

A recent disappointing New York trial court decision concerning merchant cash advances has been making the rounds over the past few weeks and a few industry players have been asking if there is cause to be concerned. While the case will likely have little precedential value, it should serve as a reminder to all funders and ISOs in the industry to invest resources where they matter; on employee education, contract review, legal representation, and customer service.

Failures or breakdowns in these areas can lead to consequential events. With so many products being offered in the marketplace to small business owners today, it is of great importance to be educated on what they all are and how they work. Sales reps, underwriters, and other staff should know what’s in the language of the contracts and be able to articulate it accordingly.

A starting point, of course, is getting your certificate in Merchant Cash Advance Basics, the online tutorial that covers the differences between the purchases of future sales and loans. It is worthwhile even for industry veterans to take considering how much MCAs have evolved over the years.

We’ve also got a list of several industry attorneys on our website, none of whom pay to be there.

Of note for contracts and legal compliance is Hudson Cook, LLP, who actually created the MCA Basics course.

Of note for litigation concerning the validity or enforcement of contracts in New York courts, is Christopher Murray of Giuliano McDonnell and Perrone, LLP, whose experience includes the VIP Limo case and several others.

It helps to have a system in place to try and resolve conflicts with merchants before they escalate. But that job is made far easier when the contractual expectations of all parties is understood from the beginning.

What’s the takeaway from a case that has gone wrong? That you should work hard to do everything right.

Make Funding Great Again – Triumphant Trump Trumps Clinton In Big Upset

November 9, 2016

The signs were there, surveys showed, at least a few that deBanked made reference to back in August. Small business owners felt Trump had their best interests at heart by a 2 to 1 margin over those who felt that about Clinton, according to a Capify survey.

Taxes ranked among their biggest concerns, with 20% of business owners ranking taxes as the single most important problem facing their business, according to a survey conducted by the National Federation of Independent Business. And Trump was in tune to that.

“Under my plan, no American company will pay more than 15% of their business income in taxes,” Trump said in Detroit on August 8th. He’s also proposed a moratorium on new financial regulations.

But up on the hill, the chatter over the last few months among the political establishment, including republicans, has been one of uncertainty. No one has been able to ascertain for sure what Trump’s positions would actually be or what agenda he’d actually set. And this wildcard status is probably what helped him win the election in the first place.

On his website however, Trump says that “we will no longer regulate our companies and our jobs out of existence,” and that he’ll “issue a temporary moratorium on new agency regulations that are not compelled by Congress or public safety in order to give our American companies the certainty they need to reinvest in our community, get cash off of the sidelines, start hiring again, and expanding businesses.”

That may be good news for the fintech industry which has grown increasingly concerned and preoccupied with potential regulatory changes. One potential conflict could arise with the CFPB, however, which has argued that its own executive branch authority operates outside the scope of the President of the United States.

In October, the United States Court of Appeals for the District of Columbia Circuit, ruled that the CFPB’s power structure violated Article II of the Constitution.

It’s too early to tell what Trump will really do and we’ll likely learn more about his goals over the next few months. Until then, prepare to Make The Industry Great Again…