Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

How the Amazon / Parafin Merchant Cash Advance Deal Came to Be

November 2, 2022Back in December, Parafin, then a fintech startup with 20 employees, submitted a proposal to Amazon to roll out a potential Amazon merchant cash advance product. At the time, Parafin was little known to the general public and its surprise deal with DoorDash wouldn’t even become public until a month later.

The prospect of an MCA would not have been foreign to Amazon given that the company already offers direct business loans, lines of credit through Marcus by Goldman Sachs, and other loans thanks to a successful pilot with Lendistry. But the team behind Parafin were virtual unknowns in the merchant cash advance industry itself. The company’s 3 co-founders, including CEO Sahill Poddar, all hail from Robinhood, the investment app that became wildly popular especially with younger adults over the last several years.

The prospect of an MCA would not have been foreign to Amazon given that the company already offers direct business loans, lines of credit through Marcus by Goldman Sachs, and other loans thanks to a successful pilot with Lendistry. But the team behind Parafin were virtual unknowns in the merchant cash advance industry itself. The company’s 3 co-founders, including CEO Sahill Poddar, all hail from Robinhood, the investment app that became wildly popular especially with younger adults over the last several years.

Coincidentally, more than a dozen people employed by Parafin, including the co-founders, are former Robinhood employees, according to profiles reviewed on LinkedIn. It’s part of a trend, it appears, as other members of their team hail from well known Silicon Valley firms like Lending Club, Stripe, Funding Circle, Google, Amazon, Facebook, StreetShares, and more.

Ultimately, Parafin’s big bet paid off. On Tuesday, November 1st, Amazon announced that the Parafin team was the one it had chosen to debut its official merchant cash advance product.

“Amazon is committed to providing convenient and flexible access to capital for our sellers, regardless of their size,” said Tai Koottatep, director and general manager, Amazon WW B2B Payments & Lending, in the announcement. “Today’s launch is another milestone in strengthening Amazon’s commitment to sellers, and builds on the strong portfolio of financial solutions we already provide. This latest offering significantly expands sellers’ reach and capabilities, and broadens their access to capital in a flexible way—one that helps them control their cashflow, and by extension, their entire business.”

“We founded Parafin with the mission to grow small businesses, and we’re thrilled that we have the opportunity to do that by providing Amazon sellers with this merchant cash advance option,” said Vineet Goel, co-founder of Parafin. “It’s a privilege to count ourselves among Amazon’s suite of financial solutions, and we look forward to making a difference for Amazon.com sellers looking to expand their business.”

The product is already listed on Amazon’s website and was rolled out to some US businesses immediately. It will be available to hundreds of thousands of additional sellers by early 2023, the company claims.

Unique to an Amazon MCA is that funding amounts can start as low as $500 and go up to $10 million.

Amazon’s entrance into the merchant cash advance market coincides wih a unique moment in the product’s history as several states are in the midst of imposing strict regulations on their sale.

Broker Fair 2022 Photos

October 25, 2022The Broker Fair 2022 Photos can be FOUND HERE. Thank you so much to all the sponsors and attendees!

Ready for what’s next? deBanked returns to Miami Beach on January 19th! Registration is now open. For questions, email events@debanked.com.

Broker Fair is Sold Out: Here’s What You Need to Know Now

October 20, 2022

Broker Fair 2022 is sold out. If you’re registered, here’s what you need to know now:

|

Pre-show (Sponsored by Lendini): October 23, 7-9pm (only open to pre-show ticket holders). This event is also sold out.

Location: 48 Lounge

Location: New York Marriott Marquis, 7th floor. Our room block is sold out.

Start Networking Early: Download the mobile app and connect with other attendees that have already begun using it too. |

Think The New California Disclosure Law is Just About a Disclosure Form? Think Again

September 13, 2022 “We’re one of the good guys so of course we’ll comply and include the form with our contracts.”

“We’re one of the good guys so of course we’ll comply and include the form with our contracts.”

Variations of the above phrase have been oft-repeated in the last few months by participants in the commercial finance industry when queried by deBanked about California’s new disclosure law. Several companies have shared that they are prepared for what’s to come, but are they? The regulations go into effect on December 9th and begin a new chapter of compliance for the industry.

Though one might be aware that California will require specific disclosures on commercial finance contracts (including purchases of future sales), Katherine C. Fisher, Partner at Hudson Cook, LLP, explained that the breadth of the state’s law will likely require changes to a funding company’s operational processes as well. Fisher told deBanked that there’s not just the matter of disclosing but also the matter of what triggers a disclosure having to be made. What might otherwise be considered the normal discourse between a funding provider and a customer prior to a deal being consummated is now an area requiring close examination.

“If a broker sends a text to a merchant with the offers, could it trigger this?” is one scenario she posed about the threshold for disclosure.

The funding provider needs to know the answer because once the disclosure requirement is triggered, the broker needs to relay back the details of the offers made, the specific disclosures provided, and the timestamp of when this took place. All of this data then needs be stored by the funding provider to maintain compliance.

And funding providers will need to be vigilant.

“The funder is responsible for broker compliance,” Fisher said.

The entire process of who-said-what, when, and how will suddenly become a realm requiring tight control it seems. And that all comes back to the form itself, which is not all that simple either.

California will require funding providers to estimate an APR on a purchase transaction using one of two methods: the Historical Method or the Underwriting Method. While the methodology selected is probably best left to qualified counsel to assist with, the likely deviation of a future estimated APR from a backwards-looking APR was a reality considered by state regulators. To bridge this gap, California requires that funding providers disclose reasonably anticipated true-up scenarios. A true-up in this instance refers to the already well-established option for a merchant to perform a monthly reconciliation of payments if the amount collected is above or below the purchased percentage specified in the contract.

California will require funding providers to estimate an APR on a purchase transaction using one of two methods: the Historical Method or the Underwriting Method. While the methodology selected is probably best left to qualified counsel to assist with, the likely deviation of a future estimated APR from a backwards-looking APR was a reality considered by state regulators. To bridge this gap, California requires that funding providers disclose reasonably anticipated true-up scenarios. A true-up in this instance refers to the already well-established option for a merchant to perform a monthly reconciliation of payments if the amount collected is above or below the purchased percentage specified in the contract.

Though the very nature of the reconciliation is a consequence of not being able to predict the future exactly, California’s law requires that funding providers disclose the dates and amounts of the true-ups that they reasonably anticipate. Such concepts and mathematics, once perhaps the subjective domain of a funding provider’s in-house underwriters will soon be subject to regulatory scrutiny for total accuracy. And this just scratches the surface.

The scope of this law is so unique and technical that the Hudson Cook law firm spent a considerable amount of time preparing a guide on this very subject. deBanked saw some of the pages of this guide during a call.

Fisher, meanwhile, insisted that compliance in California is different than compliance with the law recently enacted in Virginia and that if funding providers wait until December to begin preparing, it will probably be too late to be ready in time.

“This is more than just a form,” Fisher said. “You need to spread the word about it.”

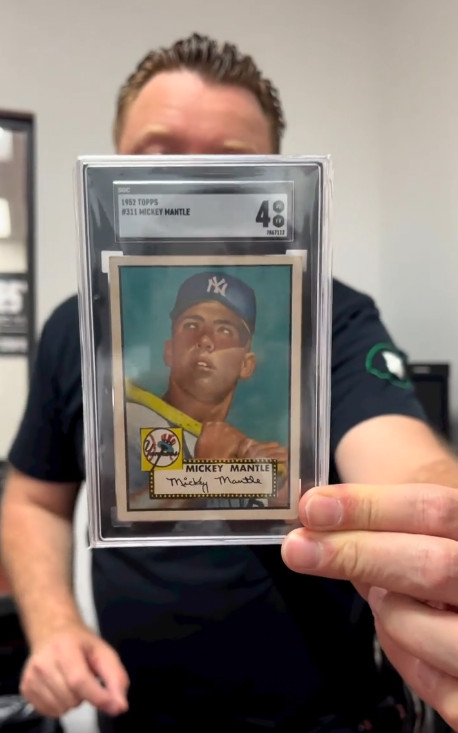

Got a Mantle, Bryant, or Mahomes Card? This Company Wants to Fund You

September 12, 2022 Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

Last month, an anonymous bidder paid $12.6M for a 1952 mint condition Topps Mickey Mantle baseball card, the highest amount ever fetched for a piece of sports memorabilia at an auction. Understandably, the news electrified a fast growing market of collectors, traders, and financiers that predicted the next big asset class wasn’t just going to be real estate or crypto or NFTs, but physical sports trading cards.

The value of the Mantle sale came as no surprise to one budding entrepreneur in South Florida. On Instagram, he’d been talking about Mantle cards for weeks, even going so far as to hold up another ’52 Topps Mantle card to the camera to promote what his company can do, which is provide quick cash advances to owners of valuable sports cards.

The entrepreneur’s name is Edward Siegel, CEO of Card Fi. Siegel’s no stranger to the alternative finance space because he spent about a decade in the MCA industry, most recently as the founder of Bitty Advance, which he sold in 2020. Since then, Siegel returned to his roots and early passion of his youth.

“I had a background in sports cards as a collector, you know as a kid, but then in my early twenties, I was promoting card shows at malls,” Siegel said. “I was heavily into the hobby, setting up the card shows and promoting them and doing player appearances where players come in and do an autograph appearance.”

That was back in the late 80s, early 90s, according to Siegel.

When Covid hit and he exited his most recent company, he noticed a massive resurgence in the sports trading card market. His next business ultimately became Card Fi, a company that will evaluate the market value of a card and make an advance against it. There’s obviously risk involved so they take possession of the card for the duration.

“We have to get a hold of these cards and we’re responsible for them and then we vault them in our in-house bank vault,” Siegel said. The cards are stored in a highly secure climate controlled environment. Card Fi shows the vault off frequently in its Instagram videos.

Such a business requires large amounts of capital so Siegel went searching for investors, a pursuit that led him to a unique place, an Instagram Live pitch competition hosted by famed CEO and reality TV star Marcus Lemonis. Siegel entered himself in as a contestant, knowing full well that the odds of even being chosen to present his business to Lemonis were about a million-to-one.

Somehow, he was called up to pitch.

“So [businesses] went on there during the quarantine and you pitched your business,” Siegel explained. “I went on there and I pitched it […] And he understood it and he thought it made sense.”

The moment eventually led to a deal with Lemonis’ company and Card Fi was on its way.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

Siegel, meanwhile, dispels the notion that the burgeoning trading card industry or his business hinges upon old vintage cards or that it’s a baseball-card-centric universe.

“If we look at it, there’s two different markets, you have the modern card market [where] I would say it’s basketball [that leads the pack],” he said. “For the vintage card market it’s baseball.”

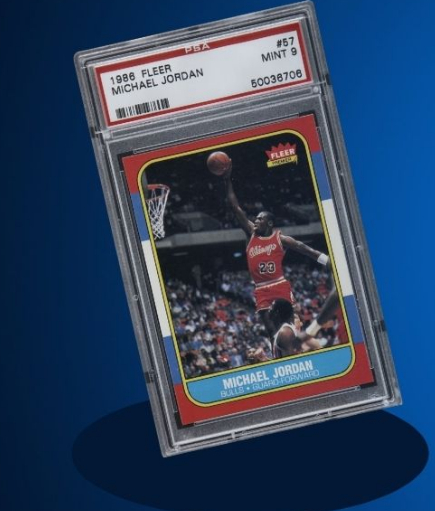

Football is huge as well, he explained. A Patrick Mahomes rookie card, for example, an NFL Quarterback that’s still currently playing, recently fetched $861,000. There are only one of five like it in the world, the scarcity playing a major role in the value. Meanwhile, a Justin Herbert rookie card, an NFL Quarterback who’s only in his third year was already receiving bids above $1 million at the time this story was being written.

“It really depends on the card itself,” Siegel explained. “Some players might be known for having better careers but then you have cards that have more scarcity to them. Something that’s a one of one or maybe a very low populated card and a graded PSA 10 could very well be worth more than a [Michael] Jordan rookie because it has scarcity in it.”

PSA refers to cards that have been verified as authentic and graded on the condition of the card itself. Ten is the highest level a card can receive. Card Fi will only work with graded cards to avoid any funny business when it comes to advancing funds based upon the value.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

Siegel explained that Card Fi’s average advance is about $40,000 – $50,000. The max right now is $500,000. There’s a big market for this type of funding it turns out because Card Fi’s much larger rival, PWCC, just raised $175 million to make similar offerings to sports card owners.

“This financing benefits the market as loans and cash advances have become an increasingly asked-for offering among trading card collectors,” said Chad Fister, PWCC’s CFO in a story that originally appeared on Sportico. “Enabling our clients to access liquidity through a menu of capital offerings is key as trading cards continue to prove themselves to be a valuable tangible asset class.”

For Card Fi, customers that take an advance can track everything through an online portal, including details about their cards, payments, and balance.

“We want to note that we built a full-service automated underwriting and collection platform to where, whether it’s the customer or the broker, they can log into our system and put the description of the card into the system and it’s going to automatically underwrite it and price it out,” Siegel said.

That description sounded like something straight out of the fintech industry of his past, especially the component about brokers.

“Just like the MCA space, we have a whole partnership side, a broker side, where brokers can refer us customers just as an affiliate where they just send the info over,” Siegel said. Similarly, they can earn a commission if a transaction is completed, he explained.

In this industry, brands like Topps, Upper Deck, and Panini have become the bread and butter for Card Fi. Even though it’s all business for Siegel these days, he couldn’t help but mention a particular card he had a personal attachment to.

“My personal favorite card in my collection is the 1965 Topps Joe Namath rookie card,” Siegel said. “Of course being a die hard New York Jets fan, that has to be my favorite card.”

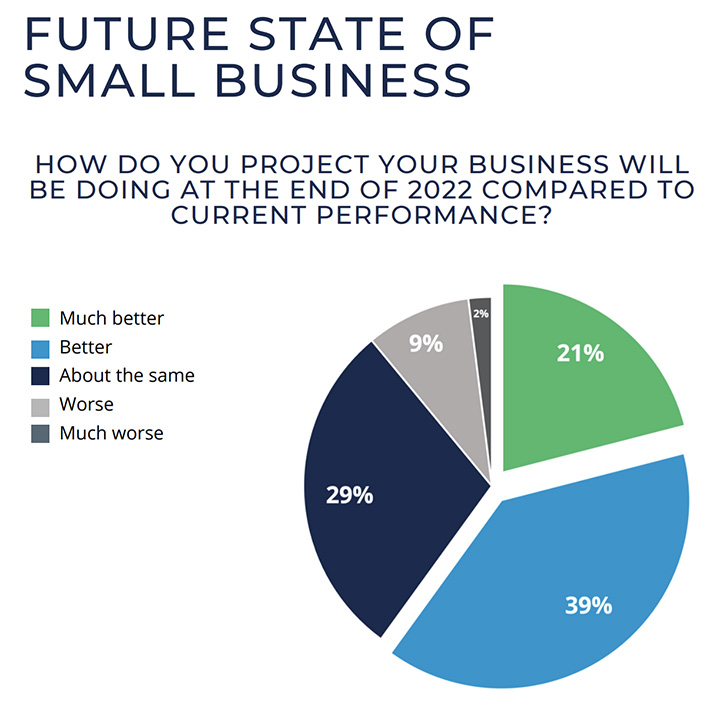

Inflation? So What – SMBs Are Bullish On the Rest of 2022

August 17, 2022Eighty-nine percent of respondents projected that their small business will be doing the same, better, or much better by the end of the year, according to a recent survey conducted by IOU Financial. The majority of those polled actually selected better (39%) or much better (21%). Twenty-nine percent said they expected to be about the same.

The sentiment is significant given that 84% said that they were somewhat concerned or very concerned about rising inflation and 85% said that they were somewhat concerned or very concerned about a possible recession.

This data is in line with responses found from other surveys like the recent NFIB study that determined that inflation was the single most important problem that business owners were facing. But even that study revealed a sense of persistent optimism, similar to the IOU survey, when respondents said that financing and interest rates ranked the lowest on their selected list of problems.

All of which means that the biggest challenge small businesses are facing right now is not viewed as a mortally perilous one. Indeed, 74% of respondents to the IOU survey said that they plan to invest in their business in the next six months.

All of which means that the biggest challenge small businesses are facing right now is not viewed as a mortally perilous one. Indeed, 74% of respondents to the IOU survey said that they plan to invest in their business in the next six months.

“They plan to fund expansion, make equipment or inventory purchases as well as put money into staffing and marketing,” the IOU report states. Only 5% flat out said that they do not plan to invest in their business in the next 6 months. The rest said that they might invest.

The optimism that is there is cautious, however. Seventy-five percent of respondents said that the covid pandemic is not fully over and 32% said that they would rate the current state of their business as somewhat negatively or very negatively.

The damage from the last two years lingers on but business owners are looking at what’s ahead of them and signaling that it’s onward and upward regardless.

The full IOU Small Business Survey can be downloaded here.

Is Your Big Brand a Bank? You Can Turn it into One

August 16, 2022

“Any entity that has employees, customers, and fans can create a banking infrastructure that looks just like a bank,” said Yuval Brisker, Co-founder and CEO of Alviere. Founded in 2020 as a spinoff of Brisker’s previous firm, Mezu, Alviere is ringing in the next generation of fintech through its embedded finance solutions.

Brisker wasn’t talking about turning the corner diner into a bank, but rather about providing the infrastructure to enable the largest companies and brands in the US to be one-stop shops for financial services, including banking.

“[It could look] like a bank in every sense,” he said, “FDIC insured, providing a savings account with yield, being able to ultimately give them a credit card, that is not a co-branded credit card, but it’s a single brand…”

Alviere has already spent loads of time dealing with the hard parts, building the tech, but also navigating the regulatory framework to make this concept a reality.

“We are a 100% regulated entity, meaning we’re not piggybacking on a banking license,” Brisker said. “We are actually licensed across the United States in every state that takes a license (except Montana). We are licensed with the federal government in Canada and Quebec and in the English speaking provinces, we’re in the process of completing our licensing in Mexico, and in Europe and in the UK.”

Brisker says this proactive approach is a “big differentiator” against the competition because they really want to provide the full services end-to-end. And that’s a big range given that it spans from bank accounts to payments to cards to cryptocurrency.

In making this possible, partnerships are key. Alviere has multiple bank partners across the globe, the company claims, one among them being Community Federal Savings Bank in the US. Alviere even solidified a deal with Coinbase back in March that enables brands to provide crypto services to their customers all through their own branded technology.

In making this possible, partnerships are key. Alviere has multiple bank partners across the globe, the company claims, one among them being Community Federal Savings Bank in the US. Alviere even solidified a deal with Coinbase back in March that enables brands to provide crypto services to their customers all through their own branded technology.

Retail customers might not ever know the name Alviere because they remain in the background, Brisker explained. The brands would, but the customers would only see themselves interfacing with the brand, which is basically the whole point.

“We tell [brands] those customers will never be our customers,” Brisker said. “We’re never going to take over the customer relationship.”

Larger companies have probably entertained this whole idea at some point already, according to Brisker. The potential to capitalize on a loyal customer base by trying to offer them financial services is increasingly being looked at.

“If you’re one of those companies and you also look at the same time how difficult it is to get into this business, both from a regulation, an ecosystem, and a technological point of view, then you’re probably putting that on your back burner and saving this for another day,” he said. Alviere, however, can make this a reality right now.

“We have all the contracts, we have all the relationships, you just need to have one point of contact, one API, one relationship, one contract, and that’s us,” Brisker said. “And we take care of everything else.”

But perhaps it’s all a big bet, because would customers actually use financial services offered through non-bank brands that they’re fans of otherwise? Technically, they already are.

When Alviere launched two years ago, more than 1 out of every 2 Americans had already used a Buy-Now-Pay-Later (BNPL) service, an embedded financial concept that’s taken off around the world. BNPL sales amounted to $100 billion in 2021 in the US alone.

“We believe that there’s a huge opportunity for more traditional beloved and essential brands to become the financial service providers for [people] coming of age,” Brisker said. “And then of course there’s a huge unbanked population that for whatever reason has not entered the financial system here and abroad, which we think that through the affinity with sort of less foreboding, less anxiety, stress-ridden relationships like some people have toward banks that they will be more inclined to come into the financial system through the back door of the system, the front door of the brands they already know and patronize.”

Turning Businesses into Funding Warriors

July 27, 2022 The downside to offering any small business a loan to grow is that they might not necessarily know how to do the growing part. And so for years, that’s what a Tempe, AZ headquartered company called Business Warrior had been focused on, helping small businesses grow and become more profitable. If businesses needed funding, Business Warrior could certainly provide that too, but the key was in maximizing the value of that.

The downside to offering any small business a loan to grow is that they might not necessarily know how to do the growing part. And so for years, that’s what a Tempe, AZ headquartered company called Business Warrior had been focused on, helping small businesses grow and become more profitable. If businesses needed funding, Business Warrior could certainly provide that too, but the key was in maximizing the value of that.

It all seemed a swell fit until the company became further intrigued by the value proposition of one of its vendors, Alchemy, an “embedded finance” company headquartered in nearby California. deBanked had interviewed Alchemy CEO Timothy Li via Zoom back in August 2020 and the tech company had only grown since then. After reconnecting in April of this year, Li described Alchemy as the “Salesforce of embedded finance.”

Embedded Finance sounds altogether buzz-wordy, but Business Warrior smelled opportunity. In June, Business Warrior announced that it had acquired Alchemy. Since then, Alchemy’s Li has become a warrior and he is working hard to roll out Business Warrior’s next generation of products.

Among the first on the horizon is an Alchemy specialty, giving small businesses the tools to become lenders themselves. It sounds like Buy-Now-Pay-Later, and to an extent it is, but the difference is that a furniture store, doctor’s office, or repair shop would be the one extending the credit, not a faceless third party on Wall Street hoping to win big.

Li explained the advantage of this by using a doctor’s office as an example. “So the creditors, the banks, don’t understand [the customer] just from reading the credit report, but the doctors understand them, they’re local people, they might have seen this patient before,” said Li. “Now [that patient] wants to do a $10,000 procedure and nobody under the sun will underwrite them.” When this happens, the doctor’s office might try to arrange some type of private financing arrangement, “but they don’t have the software to do it,” Li stated.

Business Warrior’s software solves this. The platform will be free for the business and Business Warrior will process the customer payments, which is where they’ll earn their revenue, on transactions fees.

Business Warrior’s software solves this. The platform will be free for the business and Business Warrior will process the customer payments, which is where they’ll earn their revenue, on transactions fees.

In one respect it reduces two risks for the business: (a) A third party BNPL lender dictating future approval, supply, and cost of financing, and (b) credit card companies cutting the lines of their customers that they would otherwise normally use to pay for services. The downside, so to speak, is that the business itself is tasked with being its customers’ creditor.

But ultimately, just like BNPL, such a service is likely to lead to a boost in sales, which is what Business Warrior’s mission had always been from the start.

“This tool is a tool for the small business to do more business,” Li said.

The Alchemy name will remain as far as Li knows, because they still have a lot of customers using its original products. Day to day now, Alchemy is also working with Helix House, an online marketing company that Business Warrior also acquired. They’re all leveraging each other’s resources.

Li concluded the interview by sharing a recent real world experience, he himself going to a dental office to get some work done.

“They have every single imaginable technology, schedule appointments, all the tech,” he said. “They don’t have something that manages payments. It’s either a credit card, cash, or it’s nothing.”

Referring to the financing capabilities that Business Warrior can bring to the table in those very circumstances, “I feel like it should have been there already.”