Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Deal Alert: Angelo Gordon Acquires Reliant Funding

July 14, 2015 Angelo, Gordon & Co, a $27 Billion private equity firm has acquired San Diego-based Reliant Funding. Reliant was recognized a year ago as the 385th fastest growing private company in the nation on the Inc. 500 list as well as the 28th fastest growing financial services company.

Angelo, Gordon & Co, a $27 Billion private equity firm has acquired San Diego-based Reliant Funding. Reliant was recognized a year ago as the 385th fastest growing private company in the nation on the Inc. 500 list as well as the 28th fastest growing financial services company.

A person who claims to have worked on the deal and is currently employed by the company shared the news publicly.

The deal is at least the second in the space for the private equity firm, who acquired Long Island-based Merchants Capital Access last year.

A Decade of Funding

July 7, 2015Next month is my 9 year anniversary in the merchant cash advance industry, which means I’ll be starting my 10th year. A decade of merchant cash advance… holy shit. I’ve had the opportunity to view it from many different angles and have accrued my fair share of adventures, plenty of which I’ve written about and others I’ll have to take to my grave.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

I also launched this very website exactly 5-years ago under its original name MerchantProcessingResource.com. Not many people can say they’ve authored more than 600 stories (yes, seriously) on merchant cash advance, but I can. I’m fortunate to have turned something I merely enjoyed in the beginning into a business of its own.

Looking back now, there weren’t many people keeping a live diary of events as the industry dove headfirst into the financial crisis. Who would’ve bothered to report on an industry that was arguably made up of only a thousand people?

In April 2009, even before deBanked launched, I submitted a story to the only merchant cash advance magazine of its kind. It didn’t have a very clever name, just Merchant Cash Advance Publication. My story, titled, An Underwriter in Salesman’s Clothing, rambled on about the end of the industry’s glory days, the wave of declined deals in the recession, and how funders should be more appreciative of ISOs.

Here’s a summary of what I wrote more than six years ago:

Here’s a summary of what I wrote more than six years ago:

I was complaining about stacking as far back as 2007 apparently. I addressed it as a merchant problem. Merchants were taking advantage of funders, not the other way around like some frame the argument in 2015.

I left my post as Director of Underwriting in late 2008 because “I wanted the ringing phones, the commotion, the markerboards with stats, the glory, the $20,000 [monthly] checks.”

Funding companies became super conservative during the financial crisis and all my deals were being killed (25 deals declined in a row at one point.)

I had recently charged my first closing fee, felt bad about it, and got in trouble for it.

I said 1.40 factor rates wouldn’t last (I was wrong about this!)

I bitched about algorithmic declines (I apparently thought computers underwriting files was a good way to upset ISOs.)

I acknowledged my own hypocrisy when I realized how hard it was to be a sales rep after thinking sales reps were overpaid and overrated in my previous years as an underwriter.

I continued on as a sales rep for another two and a half years after I wrote that. That means that in 2010 when I started deBanked, I was still calling UCCs, closing deals and boarding merchant accounts while sitting in a windowless room rented by a startup ISO.

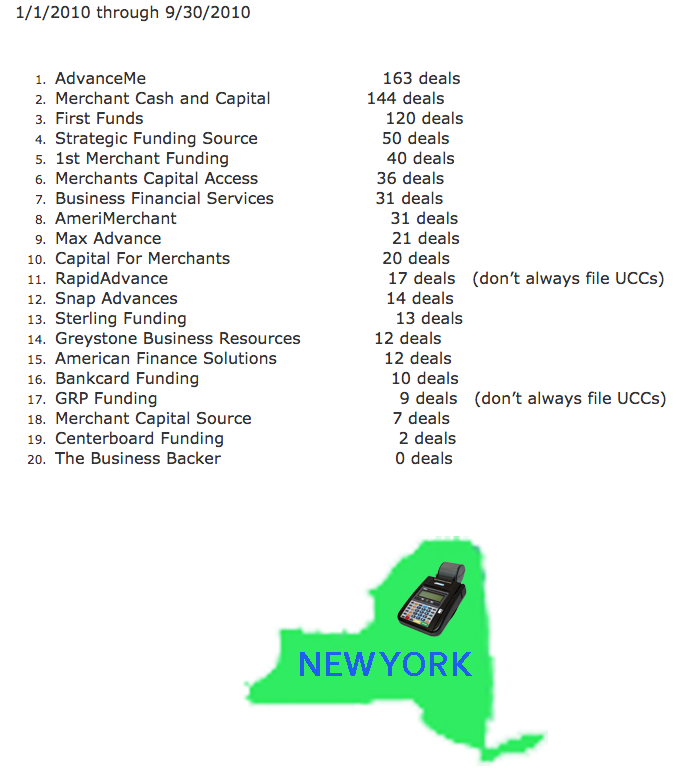

But what was there to blog about in 2010? Oh little stuff like who the biggest funding companies were at the time by checking UCC filings since almost everyone filed UCCs back then. Notably, the third largest merchant cash advance company of 2010, First Funds, is no longer in business.

I also wrote about shopping deals around and the impact that might have on a merchant’s credit report. That was the day-to-day stuff though, information I was just putting out there hoping someone on the Internet might see it. What got everyone excited was the 2010 New York State leaderboard which eventually prompted me to spend my nights and weekends investigating the industry on a wider level.

I began talking to people at other funding companies about their monthly numbers. It wasn’t that hard to get information as an industry insider, especially if you had deals to send somebody’s way. I also spent money to acquire secured party lists to count the number of UCC filings by funders in all 50 states rather than just look at one free state like I did with New York originally. I think I was the only person in the industry at the time running up their personal credit card bill to conduct such research. I had also been in the industry for four years at that point and had a great network of contacts who could clue me in on their volume.

While I said that I also looked at census records and department of labor records, I’ll admit that data wasn’t extremely useful. The end result was a best guess estimate that in 2010, there were approximately 21,000 merchant cash advances transacted for $524 million.

My data would go on to be republished in ISO&Agent Magazine, The Scotsman Guide, and Leasing News, and also end up in many other places I didn’t expect, like in the business plans of merchant cash advance companies that were looking to raise capital. In fact, in a private meeting I had with an MCA company months later in South Florida, the CEO let me take a peek at the docs they had just submitted to a bank for a credit facility. Included was a printout of these numbers with my name on it and all. Apparently there was something to this writing thing…

My last day as a sales rep was in the Fall of 2011. I left the commission-only life (oh what, you 2015 pansy closers actually get a base salary?) for something even more risky, an entrepreneurial life. For a couple years, I played underwriting consultant to a handful of merchant cash advance companies and industry expert to institutional investors interested in the space. I learned how to code in my spare time and spent more than a year in online lead generation.

I never stopped writing.

Along the way I’ve visited the offices of dozens of ISOs and funders, syndicated in deals, and test-drove new technology.

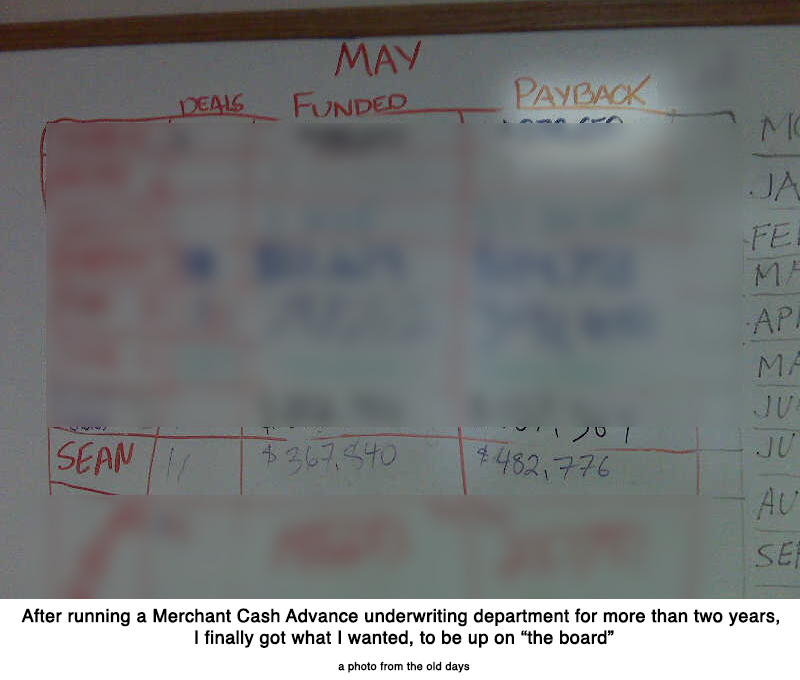

None of this makes me particularly special, especially when I hear about how much some of my old sales buddies are making these days on deals. “Are you SURE you don’t want to come back?” they ask. It’s enticing no doubt. A part of me wants to grab the phone out of their hand and attempt to shatter their record on the markerboard this month even though I’m pretty sure I’m rusty as hell.

One thing noticeable between now and 9-years ago is that my hair turned grey. This industry will do that to you (or at least it did to me.) And I still get a kick out of meeting folks who got into the industry years before I did. The 90s/early 2000s AdvanceMe crowd likes to tell me that they were funding merchants while I was still in diapers. They are practically right.

As I enter my own tenth year in the biz however, it’s exciting to think that the industry is just now getting started. OnDeck was the first IPO in the space and the general public is learning about short term business funding for the first time. There’s no shortage of news to report and that keeps me plenty busy these days.

And so even after a decade of MCA, it’s never too late to put on your Funded pants. Opportunity awaits and I hope you’ll continue to ride the wave with me. Thanks for reading since 2010!

OnDeck Q2 Earnings Announcement

July 6, 2015Update: The news reports that said OnDeck was reporting earnings today on July 6th were false

An OnDeck representative said they have not yet scheduled a date.

OnDeck (ONDK) was reportedly going to release 2015’s Q2 earnings after the market closed on Monday, July 6th (That information was confirmed as false.) Analysts predict the company will show a loss of 7 cents a share.

OnDeck (ONDK) was reportedly going to release 2015’s Q2 earnings after the market closed on Monday, July 6th (That information was confirmed as false.) Analysts predict the company will show a loss of 7 cents a share.

The company has faced a fierce sell-off in recent weeks, moving the stock to all time lows and down more than 50% from its high. The trend began after the Q1 report in which company executives argued that a decrease in the interest rates charged to their customers was not a response to competitive pressure.

Bloomberg’s Zeke Faux ran the following headline anyway:

Since then, the stock has struggled to recover. I posted a summary of why that might be on June 29th, in a short piece tiled, What Happened to OnDeck.

Barron’s was particularly tough on them, labeling them a subprime lender in dot-com clothing. For now, the key to an OnDeck rebounds seems to be about shedding that toxic label and convincing investors that despite a crowded field, they are the clear standout choice.

An increase in the default rate this quarter however would probably evoke a further negative response.

Lending Club Ends Q2 With Crisis Nobody Noticed

July 1, 2015 Lending Club investors are used to wonky stuff happening in the run up to a quarter’s end, but perhaps now since the company is public, making sure the numbers align with nice perfect trends that analysts expect is more important than ever. Either that or all hell really broke loose.

Lending Club investors are used to wonky stuff happening in the run up to a quarter’s end, but perhaps now since the company is public, making sure the numbers align with nice perfect trends that analysts expect is more important than ever. Either that or all hell really broke loose.

On the Lend Academy forum, where you can get a great glimpse of the front lines, chatter about a loan surge started on June 22nd and escalated from there.

“Huge # loans dumped in all of a sudden, and almost all allocated to fractional,” wrote veteran user Fred93. “Hard to fathom. My best guess is that this flow might be a result of having turned on some new source. Hard to guess why they are allocating them all to fractional.”

I personally noticed the increase too when I realized I didn’t have to fight robots and algorithms to get the loans I wanted. There were so many that I could pick them at my leisure.

Around this time, Anil Gupta of PeerCube pointed out that Lending Club’s Q2 loan volume had been about 10% lower than Q1’s, thus potentially putting the company in emergency mode to show growth.

But with all those loans piling up, something else happened. The loans weren’t actually issuing and conspiracy theories began to develop.

“I had nothing issued as well….with over 120 notes pending…lc playing end of quarter games,” wrote one user named kya.

Other users speculated that there was something more ominous than just games. There was a lot of discussion of the possibility that something had happened to the major institutional buyers that was causing almost all of the loans to be suddenly dumped off on retail investors, where there just wasn’t enough supply of capital to handle them.

And for a couple of days there, nothing appeared to be getting through. A handful of users reported that only 1% of purchased notes were actually becoming issued loans. The other 99% were in limbo. Everyone’s money appeared to be locked up.

But then suddenly on June 29th, the loan spigot turned off completely. “This would be a new quarter end behavior,” wrote a veteran user by the name of BruiserB. “Normally they keep placing notes on the platform for investors to buy, but they just hold up actually issuing the notes. This is the first time I have seen them stop even offering notes.”

Not that anyone really needed more notes since practically none of the previous ones they had recently bought had been issued. Everything was backlogged.

So was all the chaos just quarter-end volatility? Many did not think so. A member representing LendingAlpha.com thought the system might actually be breaking down. “What is happening now is highly unusual, as they typically push hard to find a large number of borrowers and at the same time their systems broke.”

Others started talking about a purported breakage too on June 30th, including the possibility that Lending Club’s Automated Investing option stopped functioning in the last week of the month.

LendingAlpha.com claims to have gotten a response from a Lending Club representative that admitted there were actual technical problems at play. “Their engineering team is communicating internally that the problem should be resolved by tomorrow (July 1, 2015), and the supply and demand imbalance should be back to normal by early July,” he posted on the Lend Academy forum.

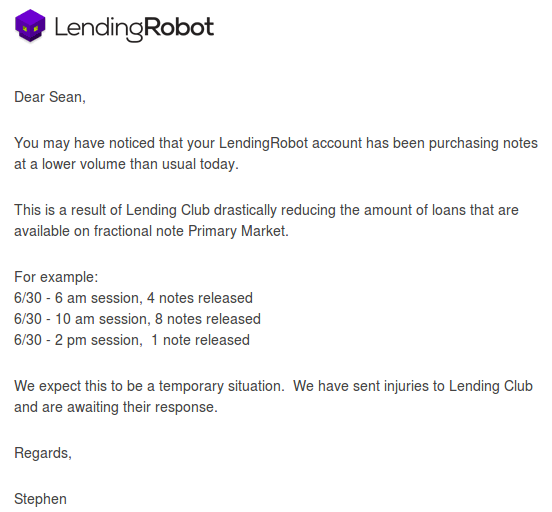

All of the irregular activity prompted LendingRobot, a third party automated investing service to issue a notice to all of its users.

While chatter on Lend Academy’s forum surged about the strange events, it got literally no coverage by blogs or news media. Fortune and Bloomberg claimed that the sudden plummet in Lending Club’s stock price had to do with investors suddenly waking up to the risks of online lending.

Fortune’s Leena Rao seemed to rely on Compass Point Research & Trading analyst Michael Tarkan to form a thesis that long term regulatory concerns were suddenly putting pressure on the stock. “Tarkan further explained that Wall Street has realized that the stock price was overvalued considering the competitive and regulatory risks in the alternative lending space,” Rao wrote.

Meanwhile, veteran note buyers like user lascott were conversing about an unprecedented breakage that had led to long loan issuance delays and in all likelihood, unhappy borrowers.

It should be noted that several forum users also trade the stock. Might the hysteria and speculation that the institutional investors were all dead and backlogged loans were blowing up the system have caused some selling activity?

At the end of June when everyone’s finally starting to hit the beach, I doubt Wall Street suddenly woke up and thought, “Damn, this regulatory risk is scary as hell. Time to sell Lending Club.”

I don’t know why the stock is down exactly but it’s ironic to see news media offer broad market generalities while a crisis unfolds in a public forum.

What happened at Lending Club in the last week of Q2? Nobody really knows but it seems like everything’s getting back to normal now that we’ve started Q3. The institutional investors aren’t gone and backlogged loans are starting to issue.

Nothing to see here folks. What were you saying about regulatory risks again?

Letter From the Editor – July/August 2015

July 1, 2015 G’day mates,

G’day mates,

Merchant cash advance and similar financial solutions have expanded beyond the United States. Canada was always the next logical option but it’s made its way far beyond that, all the way to Australia. And in the land down under, Australian natives are competing with American-based companies for market share. There’s not a lot of information available about the landscape there so we went out and got the inside scoop, fair dinkum!

Speaking of international, the race is on here at home to obtain a national or state bank charter. Loans allow for much more customization than is possible with merchant cash advances, noted Glenn Goldman, CEO of Credibly. But is the industry setting itself up for a stable future or are some companies betraying their roots as a bank alternative by in essence becoming banks themselves?

And even while the crowd cheers for charters, a baffling appellate court ruling in New York State threatens to undermine that strategy completely. If you haven’t heard of Madden v. Midland Funding, we’ve got some information about it inside.

I must note that deBanked celebrated its 5-year anniversary this past July. The world was much simpler when I started it. In 2010, I was able to quantify the industry’s size with ease, but today it’s a challenge to define what the industry even is, let alone calculate how big it is.

Everything is evolving and quickly, but some things still say the same, like when a broker’s commission is pulled back because a deal defaulted. Shouldn’t lenders take full responsibility for their own underwriting decisions? Not all brokers thought so apparently when we asked them. It appears that today’s broker is thinking more like a lender and if long-term growth is one of their goals, they’re probably thinking about becoming a lender themselves. That of course brings us right back to bank charters and court rulings to make that possible.

And if those topics are exhausting to think about, then sit back, relax and let us guide you through the beautiful Australian Outback. From Uluru to a kangaroo, alternative lending is never out of reach.

–Sean Murray

The Rest of the Alternative Lending Industry’s Funding Numbers

July 1, 2015 Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Let’s be serious, the industry’s much bigger than we may have let on when we published the industry leaderboard (some mods have been made) in the May/June issue.

Right after deBanked sent the final file off to the printers in May, PayPal announced that the widely circulated $200 million lifetime funding figures were slightly outdated.

How off were they?

Oh, just by about $300 million or so. By May 7th, PayPal’s Working Capital program for small businesses had already exceeded $500 million. The industry leaderboard has been revised to reflect the news. PayPal says they are funding loans at the rate of $2 million per day, which puts them on pace for more than $700 million a year. Um, wow?

One name that’s missing from that list is Amazon, whose secretive short term business loan program is reported to have already generated hundreds of millions of dollars in loans. Given the $300 million discrepancy that PayPal let ruminate for months, we’re in no position to speculate on Amazon. Anyone could try to assess what they’ve been up to however, since they file UCCs on their clients under the secured party name “AMAZON CAPITAL SERVICES, INC.”

Of course if you’re craving specific numbers, an anonymous source inside Yellowstone Capital revealed that Yellowstone produced $35.5 Million worth of deals in the month of June alone. Yellowstone has a strategically diverse business model that allows them to either fund small businesses in-house (essentially on their own balance sheet) or broker them out to other funders. Yellowstone was listed on deBanked’s May/June industry leaderboard at $1.1 Billion in lifetime deals and $290 Million in 2014. June’s figures indicate that they are probably well on their way to surpassing last year’s numbers.

Curiously, platform/lender/broker/marketplace company Biz2Credit has been hanging on to the same stodgy old number for more than a year.

Funded over $1.2 billion. 200,000+ happy customers.http://t.co/3h64lI4cgG #smallbusiness #Funding

— Biz2Credit (@biz2credit) June 19, 2015

They were touting that same $1.2 Billion number exactly 1 year ago. Surely they have done more since then? Biz2Credit’s service covers a much wider scope however so a direct comparison with their peers may not be appropriate. A lot of their loans are arranged through traditional banks which are typically transacted in amounts larger than the average $25,000 deal alternative lenders do.

A source familiar with Biz2Credit’s breadth said he observed a deal where the company helped a businessman in Mexico obtain financing to purchase a new helicopter, a transaction which apparently necessitated a team to fly down there to sign paperwork. Definitely not a standard transaction!

When we published the industry leaderboard initially, it admittedly omitted some of the industry’s largest players. Many firms are fairly secretive about the numbers they release and we’re in no position to disclose numbers that aren’t supposed to be public. Below is data that we hadn’t published previously.

The industry’s unsung behemoths

The industry’s unsung behemoths

The $300 million lifetime funding figure publicized by NYC-based Fora Financial can’t be that stale. It’s the number currently stated on their website and a late February 2015 company announcement revealed they were only at $295 million at the time. We feel comfortable enough to now have Fora Financial on the leaderboard.

In 2014, Delaware-based Swift Capital revealed that they had funded more than $500 million. It’s unclear how much that’s increased since then.

Credibly (formerly RetailCapital), has publicized that they’ve funded more than $140 million in their lifetime. Founded in Michigan, the company has opened offices in New York, Arizona, and Massachusetts. They’ve been added to the lifetime leaderboard.

New York City-based AmeriMerchant has a claim on their website that they have funded more than $500 million since inception. How much more exactly? We’re not sure.

Coral Springs, FL-based Business Financial Services keeps their figures mostly under wraps but a good guess would place their lifetime figures at somewhere between $700 million and $1.2 billion.

Miami, FL-based 1st Merchant Funding had reportedly funded close to $100 million in the Spring of 2014. It’s uncertain as to where they might be now.

Woodland Hills, CA-based ForwardLine surpassed $250 million in funding as far back as 2013.

Orange, CA-based Quick Bridge Funding disclosed more than $200 million in funding in late 2014.

Troy, MI-based Capital For Merchants has funded $220 million since inception. But there’s more to the story. Capital For Merchants is owned by North American Bancard, a merchant processing firm that acquired another merchant cash advance company, Miami, FL-based Rapid Capital Funding in late 2014. And coincidentally, Rapid Capital Funding had just acquired American Finance Solutions months earlier, which is an Anaheim, CA-based merchant cash advance company that had funded more than $250 million since inception. All told, North American Bancard owns at least three merchant cash advance companies: Capital For Merchants ($220 million), American Finance Solutions ($250 million+), and Rapid Capital Funding (undisclosed). There are rumors that they’re in talks to acquire at least one more company in the space, which, if true, would make North American Bancard one of the industry’s most powerful players.

Don’t bother counting up the above totals

These figures all barely scratch the surface as deBanked’s database indicates there are literally hundreds of genuine direct funders in the industry.

Thanks to the company representatives that took the time to confirm their funding numbers with us directly. Anyone interested in sharing their figures can email sean@debanked.com. If there is a gross inaccuracy somewhere as well, please report it to us.

This page might be updated in the future so check back!

Is Amazon Already a Top 10 Funder?

June 29, 2015 18 months ago I mentioned Amazon’s quiet entry into business lending but nobody’s really talked about it. But earlier today in a story that was supposed to highlight the company’s push into China, they revealed some interesting details that the rest of the alternative lending industry deserves to know about.

18 months ago I mentioned Amazon’s quiet entry into business lending but nobody’s really talked about it. But earlier today in a story that was supposed to highlight the company’s push into China, they revealed some interesting details that the rest of the alternative lending industry deserves to know about.

1. Amazon offers three to six-month loans of $1,000 to $600,000 to help merchants buy inventory.

2. Amazon has already funded hundreds of millions of dollars.

3. Sellers are reporting interest rates of 6% to 14% but it’s unclear if these are APRs or dollar for dollar costs since the loans are for much less than a year. I suspect the effective APRs are higher.

While Amazon is obviously doing these to grow Amazon merchants, the short maturities and stunning loan volume definitely earns them a spot on the list of the biggest funders in the industry.

Another fact worth repeating is this tidbit from PayNet:

“The default rate for small businesses with credit under a $1 million stood at 1 percent in 2014 but is seen rising to 1.6 percent in 2015, as new lenders with varying ability to assess risk increase lending, according to small business credit ratings provider PayNet.”

Tech-based Lenders Clobbered On Dose of Bad Economic News

June 29, 2015How would tech-based lenders fare in a slumping market? Not very well apparently…

OnDeck (ONDK) and Lending Club (LC) set new record lows earlier today amid bad news coming out of Greece and Puerto Rico. OnDeck is down almost 43% from its IPO price and down 61% from its all time high. It was down more than 8% today even though the Dow was only down 2%.

$ONDK was unaware that it focused on Greek loans…. interesting 8.6% drop.

— Mark Holder (@StoneFoxCapital) Jun. 29 at 05:48 PM

The downward trend was dissected in a post that was published just hours before today’s further fall.

Meanwhile Lending Club is in new territory, down 3% from its IPO price and down 50% from its high. So what are investors saying about this?

$LC hmm i really dunno what to say about this…

— mike pham (@mincogneto) Jun. 29 at 05:30 PM

That’s kind of the overall gut feeling. Many feel this company is being unfairly dragged down and yet it continues to fall. A mounting campaign by the Puerto Rican government to declare bankruptcy and a Greek debt disaster clobbered everything today including Lending Club. One tweeter came up with a great idea last week, bail out Greece with a loan from Lending Club…

If all else fails with the IMF #Greece should just apply on @LendingClub pic.twitter.com/RbtnMm5JaO

— World First USA (@WorldFirstUS) June 22, 2015

Last week no one was even talking about Puerto Rico. Now all of the sudden they’re in a “death spiral.”

Watch the death spiral coverage on CNN

The market’s tech lending darlings might’ve gotten pummeled like everyone else but the ease with which they drop should probably be a warning sign. Neither offshore dilemma stands to have any impact on their businesses. So what would happen if a relevant issue were to arise such as a domestic disaster, a sudden rise in unemployment, a recession, a financial crisis, skyrocketing fuel prices, a steep increase in the fed funds rate, or even something no one dares talk about like a legal ruling that could jeopardize the entire bank charter model?

It’s quite possible that both companies haven’t bottomed out just yet….

——–

Note: I have no equity positions in either company. I do own Lending Club notes however.