Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

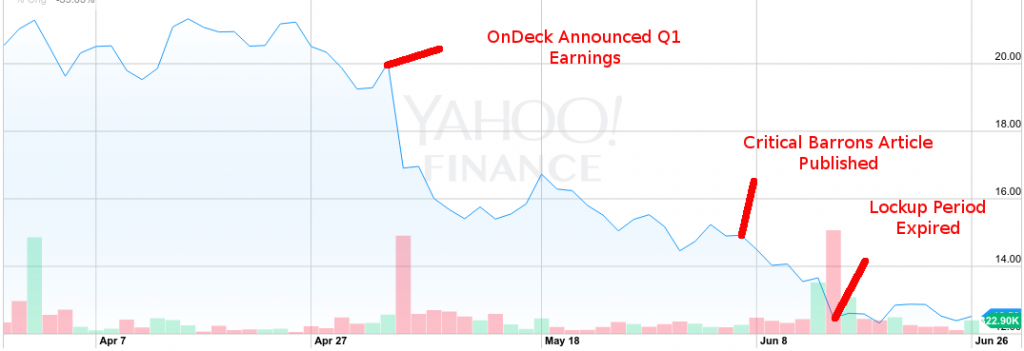

What Happened to OnDeck? (ONDK)

June 29, 2015The lockup expiration came and went but the fall of OnDeck’s stock price started much before that. There were no insider stock sales reported to the SEC since shares became unrestricted anyway.

There’s very little trading volume on an average day and investors on the big message boards either ignore this stock or don’t understand it.

The trend started on May 4th when they released Q1 earnings. The direction wasn’t very much different than Q4. Loan volume went up, interest rates came down, and no profits were to be had, nor were any expected for the rest of the year.

The market interpreted decreasing interest rates as pressure from competitive forces however and down went the stock price.

OnDeck’s execs insisted that they had lowered rates as part of a deliberate strategy to create stickier customers and attract new borrowers. CEO Noah Breslow himself said during the previous 2014 Q4 earnings call that “there’s so much search cost associated with going out and looking at other places and so much uncertainty around that, they [small businesses] typically just take that offer that OnDeck has provided to them.”

His theory is supported by the results of Lending Tree’s recent survey that revealed nearly 60% of small businesses did not comparison shop business loans online during their loan application process.

It’s possible though that the drop had little to do with OnDeck’s actual performance. That same day, Goldman Sachs hinted that they would be joining the tech-based lending field when they announced the hire of Harit Talwar from Discover Financial Services.

But before they had a chance to recover, Barrons published a story that was highly critical of OnDeck just a month later on June 5th. “It’s a subprime lender in dot-com clothing,” the author wrote. It was a tough characterization for them to refute, what with their 50% interest rates and double digit percentage charge-offs and all.

And then the lockup expiration on June 15th coincided with the big reveal of Goldman’s intentions to compete in the marketplace. News sources that picked up the story predicted that the move would impact online lenders like Lending Club and OnDeck. OnDeck’s stock hit a record low that day.

OnDeck has been stuck in the 12s ever since. Can they dig themselves out?

If competition is a factor in the market’s perception, and it probably should be, then investors should keep an eye on the industry’s other top players. OnDeck is not alone in this space and Goldman Sachs will be in for a bigger fight than they probably expect.

Source: deBanked’s May/June Magazine issue

The CFPB is Pretty Busy With Actual Consumers

June 28, 2015 It’s often theorized by industry insiders that the Consumer Financial Protection Bureau (CFPB) will play a role in business to business transactions. But when you actually talk to those employed by the government agency, it seems very unlikely. The CFPB is already very busy playing the role of Better Business Bureau, albeit a nationalized version.

It’s often theorized by industry insiders that the Consumer Financial Protection Bureau (CFPB) will play a role in business to business transactions. But when you actually talk to those employed by the government agency, it seems very unlikely. The CFPB is already very busy playing the role of Better Business Bureau, albeit a nationalized version.

There is currently no categorical option to report business loan or merchant cash advances on their website and the complaints lodged by consumers pertain to very basic consumer problems, such as issues with their credit cards or student loans.

Here’s an example of a CFPB complaint:

2009 XXXX XXXX, XXXX XXXX Thursday of every month I got pulled from class to get a new loan for my living and tuition expenses. I was at XXXX for one year and if I didn’t go to sign the papers for my new loan every month I wouldn’t be able to continue my classes to XXXX. I missed out on important class information and had to make them up on my own time. Homework and other hands on tasks became more difficult to accomplish if I didn’t make up the lost time going to sign loan papers. I was told a rough amount that my school loan would be. About {$15000.00}. I started paying {$120.00} a month for my loan agreement then Genesis Lending increased it to {$190.00}. I called to ask why the increase in payment amount each month. I was told they saw i had a higher income so they adjusted the payment accordingly. Is that legal? I’ve been paying this amount for 6 years and still owe {$13000.00}. I called Genesis Lending and come to find out they have been rolling over all the interest I pay on the loan every year. So all I’m paying is interest basically for the last 6 years. I don’t think I ‘m being treated fairly or legally.

Many complaints are just like this, where consumers are not actually reporting illegal activity but instead using the CFPB to vent their frustration. In this situation, the victim was busy with homework and wasn’t sure how their student loan worked so they filed a complaint with the federal government…

The end result was that the lender responded by saying it wasn’t really their problem, the borrower didn’t dispute this response and the CFPB marked the case as closed. Seems like a great use of everybody’s time.

In the handful of presentations I’ve attended by the CFPB, they said they often find themselves redirecting complaints to the business that the consumer is complaining about much like the BBB would do.

Still Reviewing Paper Bank Statements? Stop

June 26, 2015 Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Are the bank statements you received legitimate? Underwriters in the business financing industry are scouring paper documents for abnormalities hoping to catch fraud in the inducement. And word on the street is that small business owners are doctoring statements and engaging in trickery in record numbers.

Technology has made it easier to create authentic looking documents and the rise in online lending seems to be bringing out the worst in people. Somebody in a desperate situation might not have the guts to look a banker in the eye and hand him a stack of fraudulent documents but they might roll the dice with somebody over the Internet they’ll never have to meet.

The fakes aren’t obvious anymore. Anyone can go online and buy doctored documents from professionals. The business is booming on Craigslist for example where fraudulent documents can be made to order in under an hour.

In the Miami area, fraud hucksters are even beginning to offer deals such as buy 2 fake documents, get 1 free.

Industry-wide, funding companies are complaining that attempted fraud is out of control. One broker recently took to the dailyfunder forum to share her frustration. “I can spot them a mile away!!! 2 different deals submitted this week with fraudulent statements!!!,” she vented.

Other brokers chimed in, sharing their stories such as a merchant whose doctored statements were only noticed because ATM withdrawals were listed with odd amounts like $90.83.

Oddly, nobody seems to be reporting this fraud to the authorities. It all seems to get swept under the rug as business as usual. Orchard co-founder David Snitkoff for example, was asked just last month about the rate of marketplace lending fraud and he apparently said, “No worries, none to date.” He seemed to be implying that fraudulent applicants are getting screened out. But that doesn’t mean people aren’t trying.

Seven months ago, merchant cash advance underwriter Pierre Mena wrote in detail about the challenges he faces in detecting fraud. He said:

Some of the more well hidden fraud can usually be found by comparing the summary page and last page of the bank statement to other statements. Typically, most banks and some credit unions offer you a snapshot of the starting balance, which should generally match up with the ending balance of the previous month. If it doesn’t, you should look for any transactions from the previous month that did not settle until the current month. If there is none, this is usually a red flag indicating that the merchant forgot that statements are continual time series financial data whose totals carry on to the following month.

-Pierre Mena, Rapid Capital Funding

A lot of these issues can be easily overcome by simply disregarding paper statements altogether. Microbilt’s instant bank verification tool for example, will allow you to pull the most recent 90 days worth of transaction data directly from the banks themselves. Funders using these automated checks swear by their effectiveness and the capability is essential for any company that wants to scale.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

But a recent conversation with the owners of a broker shop in NYC said this is easier said than done. Merchants are still using fax machines to send statements or claiming they don’t have access to computers or email accounts, they said. They added that their clients would suffer if approvals were completely contingent upon online verifications.

Cultural differences play a role in this according to Gil Zapata, the founder of Florida-based Lendinero. Zapata recently wrote that latino business owners over the age of 45 are not accustomed to doing business over the Internet, email, fax, or phone. “This group has a high level of distrust in doing business via the Internet,” he said.

So is there a middle ground? On the dailyfunder forum, Chad Otar, a managing partner of Excel Capital Management said that he tells merchants they can change their online banking passwords after a verification. And Andy McDonald of Yellowstone Capital wrote that verifying the bank data is beneficial for the merchants too. “It protects the merchant by allowing us to check their account to make sure our pulls aren’t going to bounce,” he wrote in a thread back in April. He also added that he comes across 2-3 applications PER DAY with altered statements.

Humans can only do so much. Pierre Mena actually wrote, “Some of these statements are doctored so well that you may have to zoom in upwards of 300% to find a comma that should actually be a period to separate dollars from cents.” At this point, an instant bank verification would probably work wonders.

Online business lender Kabbage might have the best model. On their website, applicants are instructed to enter their email address followed by their bank account username and password. Their system will analyze their bank transactions and if eligible, will then ask the applicant for their first and last name. It flies in the face of all the pushback that funders claim merchants give them over data privacy and security.

Four months ago Kabbage announced they were already up to funding $3 million per day. Obviously there is an entire segment of small business owners that are sucking up whatever concerns they had about bank verifications in order to get the capital they need.

The majority of the small business financing industry is still relying on paper statements and probably shouldn’t be. If you have to zoom in upwards of 300% to find a comma that should actually be a period and if con artists are offering discounts for bulk orders of fraudulent statements, it may be time to throw in the towel and join the rest of the world in using the Internet…

Dear Brokers, Investors Love You Too

June 25, 2015Hedge funds, private equity, and family offices have been all hot and bothered by lending marketplaces and direct funders for a while now, but there’s a new sexy stud that everybody wants to take to the dance, the brokers that originate the deals. An entire segment of the industry still calls them ISOs (Independent Sales Organizations) and in 2015, nobody can seem to shut up about them.

One minute brokers are being fingered as the source of the industry’s moral decline and the next minute they’re the lifeblood of it all.

Ever since World Business Lenders began acquiring broker shops and converting them into franchisees, the institutional investors suddenly woke up.

They’re Buying Brokers? BUT WHY?!

Over the years, dozens of funders have opened for business and then realized they don’t know how to get deals or where to get them from.

It’s not a build-it-and-they-will-come industry anymore. As much as certain people try to berate brokers, it’s widely believed that they still control up to 50% of the industry’s deal flow. Institutional investors examining portfolios have taken notice that some funders are successful only because they have a loyal group of broker shops. So if the brokers make the funder, then why not court the brokers?

And so they’re doing just that…

If you’re brokering less than a million a month though, you’re not really investment material yet. There’s thresholds. The more volume you produce, the more options at your disposal.

At this size, you’re really just a couple of dudes (or dudettes) sitting in a room with phones. There’s not enough action to get anyone excited. There may be some potential to get an investor to co-syndicate with you, but that’s it.

$1 Million/month to $4 Million/month

Congratulations, you’re not just a bunch of dudes anymore. If you’re using decent software, hopefully you can print out the necessary reports to woo investors. At this level you’re eligible for co-syndication, an advance rate to fund your own deals, or to be rolled up as a franchisee. If you’ve got a criminal record or have been banned by the SEC, then forget it though.

$4 Million+

If you’re not already funding your own deals at this point, you’re going to be encouraged to by an investor. They’ll want to set you up on a platform that they trust and participate in the funding in some way. You can get a credit facility. You’re also acquisition material. Funders and investors have little interest in acquiring a couple of dudes sitting in a room because there’s no actual assets to value. At $4 million a month and more, there may potentially be something beyond just the dudes running the company and therefore something to consider. If you can’t pass a criminal background check though, then forget it. And if you’re running scrappy like a $200k/month shop, then they’re not really going to be able to help you. It doesn’t help if you’re stack-heavy either.

But just because you do the volume, that doesn’t mean you can just show an investor an Excel spreadsheet and hope that they’ll fork over millions of dollars in return. You have to run your shop like a professional, not a dude (or dudette of course). And if you think you meet that criteria, that’s great news, because investors want to talk to you really badly.

But just because you do the volume, that doesn’t mean you can just show an investor an Excel spreadsheet and hope that they’ll fork over millions of dollars in return. You have to run your shop like a professional, not a dude (or dudette of course). And if you think you meet that criteria, that’s great news, because investors want to talk to you really badly.

Last year, every banker I sat down with told me they were looking to invest in the next OnDeck or CAN Capital. And what happened was, you had 200 bankers competing for the same handful of deals. This year, the conversations are all about brokers.

“Who wants to become a funder?”

“Who needs money to syndicate?”

“Who is serious about growing their broker shop?”

Did someone say Year of the Broker?

It damn sure is. If you’re funding more than a million a month, don’t rely on stacking, don’t have a criminal record, have actual reporting systems (not Excel), and want to be a funder or participate in more deals, then there’s a group of investors that are ready and willing to swipe right.

You might not be the next OnDeck and that’s okay. If you’ve got the flow, you can get the dough. <3 😉

Tech-based Underwriting Shows Cracks?

June 21, 2015 A self proclaimed borrower of Lending Club and Prosper loans posted a tell-all on the Lend Academy forum earlier today and the allegations are alarming. Below is a summary of their experience:

A self proclaimed borrower of Lending Club and Prosper loans posted a tell-all on the Lend Academy forum earlier today and the allegations are alarming. Below is a summary of their experience:

- Stated that when times got tough, they resorted to lying about everything.

- Alleged the lenders don’t care about what they’re using the money for.

- Stated that after consolidating their debt, they immediately maxed out their revolving lines again.

- Proclaimed that these types of loans are for people who are at the end of their rope just trying to survive.

- Alleged their revolving line utilization percentage was wrong because credit bureaus showed old revolving accounts as open even though they’ve actually been closed for years. In their case, the utilization stated 25% but in reality was 100%.

- Alleged their Debt-to-Income ratio was wrong. It looked more favorable than it actually was.

- Stated they stopped making payments and then filed bankruptcy six months later.

- Alleged Prosper never even filed a Proof of Claim with the bankruptcy court and therefore won’t be receiving anything.

Disturbingly, the borrower says they were able to get a second loan from each lender without their employment/income being re-verified.

“I guess I could have lost my job and you never would have known,” the author writes.

Suspiciously however, they go on to make an off-the-cuff recommendation that peer-to-peer marketplaces be required to invest their own money in the loans they issue.

“Why wouldn’t a company file a proof of claim?,” they questioned. “I have to assume because they have no incentive to do so. If the law was changed so these companies had to put up 10-20% of their own money, you may see them caring more about the investors.”

One has to wonder why an individual that successfully evaded a creditor after drowning in debt and filing bankruptcy would come on to lobby for a law that would encourage that creditor to do a better job collecting.

Regardless of us being able to confirm the borrower’s authenticity though, they did raise some good points.

Is it possible that a credit bureau could show accounts as open that are actually closed? Of course. A recently issued FTC report revealed that one in five consumers had an error on at least one of their three credit reports. But even worse, one in just four consumers identified errors on their credit reports that might affect their credit scores.

If 20% of reports are not perfect and 25% of consumers see material errors in their reports, then investors are working off of pretty shoddy data to make decisions.

Additionally, a common complaint by investors on the forum are loan amounts for debt consolidation that wildly exceed the borrower’s actual revolving debt. Could this be a sign that borrower intent is not validated?

And while I couldn’t confirm whether or not income and employment are re-verified on additional loans from the same lender, the implications of playing fast and loose the second time around are troublesome. Lending Club states that past performance is the predominant basis for another loan:

To qualify for a second loan, you’ll need to meet the current credit criteria for the second loan and have made either 6 or 12 consecutive on-time monthly payments on your existing Lending Club loan*, depending upon the size and term of the existing loan.

*Borrowers must have made 12 consecutive successful monthly payments if the original loan principal is $20k or more or the existing loan has a 60 month term, unless the loan has been paid down by 50% or more, in which case borrowers need only have made 6 consecutive monthly payments. Borrowers must have made 6 consecutive successful monthly payments if the original loan principal is less than $20k and the loan has a 36 month term.

But while the defaulting borrower tells us to be afraid, historical data paints a different picture. Peer-to-peer lending guru Peter Renton has long touted repeat borrowers because of the stellar returns they produce.

And Orchard’s analysis of Prosper loans two years ago confirmed the same. The more loans a borrower took with Prosper, the less likely they were to become delinquent on their loan. This was only the case for the first 12 months of the loans, not in their entirety to maturity, which they didn’t examine at the time.

But while the statistics look good, the defaulting borrower is perhaps warning us that a lender’s guard comes down with positive past performance and is therefore vulnerable.

Whatever the case may be and whatever the author’s true intentions are, it is certainly alarming to read that a borrower lied, their credit information was inaccurate, they defaulted on the loan, and the lender made no effort to make a claim in the bankruptcy proceeding.

Is tech-based underwriting and the marketplace model showing cracks? You be the judge…

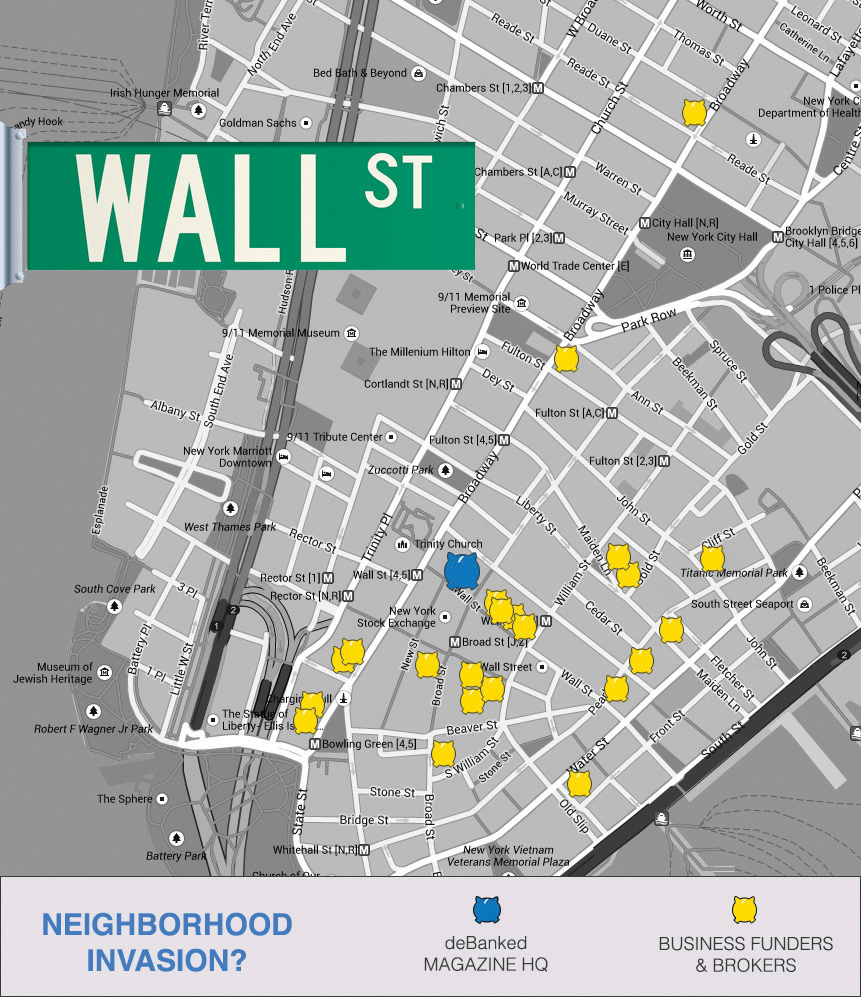

Wall Street Has a New Landlord

June 20, 2015 “You stole my deal bro!”

“You stole my deal bro!”

“No I didn’t. The merchant hated your offer,” replies back a 25-year old dressed in a dark pinstripe suit with no tie.

He then takes a pull from his half-smoked cigarette and continues, “The guy wanted 90k and you offered him twenty. I was at least able to get him fifty. What’d you think was going to happen?”

I walk past the two who eye me suspiciously and am quickly out of hearing range of their conversation. They were strangers, but I know exactly what they were talking about. Walking around the neighborhood here, I feel oddly at home.

This is Wall Street, a new stronghold for the small business financing industry. Midtown has traditionally been the epicenter for merchant cash advance companies, but somewhere along the way, new players started opening up their shops in lower Manhattan.

As a born and bred New Yorker, I never really saw a need to visit the actual street of Wall Street. To my knowledge, it was simply emblematic of high finance, not really a physical place anymore.

But earlier this year when I signed a lease at 14 Wall Street, I would be thrust into the middle of America’s biggest breeding ground for financial brokers and learn once and for all that the ebb and flow of Wall Street isn’t exactly gone, just transformed.

From my office up on the 20th floor, I can see into the windows of the top five stories of the New York Stock Exchange building. The floors appear to be set up for traders, with long white continuous desks peppered with large monitors on both sides. Everyone sits and stares intensely at their screens, pressing buttons on their keyboard at rapid fire pace. Nobody runs around screaming orders anymore.

Outside, tour guides tell excited onlookers about the stock exchange’s past. It’s a historical landmark, a place to learn about history, not necessarily witness it. The spirit is still alive though in a zombified made-for-the-cameras kind of way. OnDeck recently kicked off their IPO there and so too did Lending Club.

Outside, tour guides tell excited onlookers about the stock exchange’s past. It’s a historical landmark, a place to learn about history, not necessarily witness it. The spirit is still alive though in a zombified made-for-the-cameras kind of way. OnDeck recently kicked off their IPO there and so too did Lending Club.

While tourists dance around aimlessly and upload photos to facebook to show they were there, men and women in the office floors above them are engaged in a different kind of dance. Packed in elbow to elbow with phones glued to their ears, commercial financing brokers shout large numbers at an accelerated pace.

Often lacking luxury amenities such as windows, brokers on Wall Street are weathering the heat and lack of oxygen to move money to Main Streets all across America.

When they come out for air to breathe, the tourists move out of their way, as if they’ve suddenly become aware that people are actually trying to get some work done down here.

The little strip of Broad Street between Wall Street and Exchange Place is kind of like a schoolyard for the merchant cash advance industry. War stories are exchanged, cigarettes shared and dreams dreamed. One day, I’m going to start my own ISO and I’ll do it differently because…

You can walk in any direction. The industry can be found on Broad Street, William Street, Pine Street, and Broadway. It’s on Water Street, Rector Street, Maiden Lane, and Fulton Street. It extends outward almost infinitely to Midtown, Brooklyn, Queens, Long Island, Staten Island, The Bronx, Westchester, Orange County, and New Jersey.

You can walk in any direction. The industry can be found on Broad Street, William Street, Pine Street, and Broadway. It’s on Water Street, Rector Street, Maiden Lane, and Fulton Street. It extends outward almost infinitely to Midtown, Brooklyn, Queens, Long Island, Staten Island, The Bronx, Westchester, Orange County, and New Jersey.

And while there are hubs in the outer parts, the most unique experience by far is down here on Wall Street, where you’re infinitely more likely to overhear professionals shouting “ACHs” and “stacks” than “puts” and “calls.”

Although the guides teach tourists that Wall Street as they imagined it to be is dead, Wall Street itself can never die.

Every now and then a pedestrian will look up at the offices above and wonder if the magic of fast-talking finance still exists. Is that world gone forever?

Not quite…

The stockbrokers may be gone, but there’s a new landlord. Wall Street belongs to the small business financing industry now.

The Official Business Financing Leaderboard

June 20, 2015A handful of funders that were large enough to make this list preferred to keep their numbers private and thus were omitted.

| Funder | 2014 |

| SBA-guaranteed 7(a) loans < $150,000 | $1,860,000,000 |

| OnDeck* | $1,200,000,000 |

| CAN Capital | $1,000,000,000 |

| AMEX Merchant Financing | $1,000,000,000 |

| Funding Circle (including UK) | $600,000,000 |

| Kabbage | $400,000,000 |

| Yellowstone Capital | $290,000,000 |

| Strategic Funding Source | $280,000,000 |

| Merchant Cash and Capital | $277,000,000 |

| Square Capital | $100,000,000 |

| IOU Central | $100,000,000 |

*According to a recent Earnings Report, OnDeck had already funded $416 million in Q1 of 2015

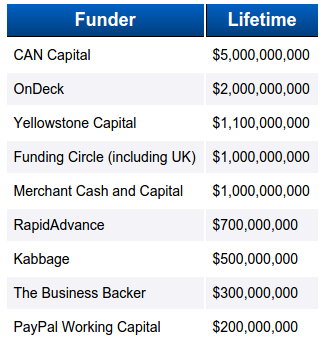

| Funder | Lifetime |

| CAN Capital | $5,000,000,000 |

| OnDeck | $2,000,000,000 |

| Yellowstone Capital | $1,100,000,000 |

| Funding Circle (including UK) | $1,000,000,000 |

| Merchant Cash and Capital | $1,000,000,000 |

| Business Financial Services | $1,000,000,000 |

| RapidAdvance | $700,000,000 |

| Kabbage | $500,000,000 |

| PayPal Working Capital* | $500,000,000 |

| The Business Backer | $300,000,000 |

| Fora Financial | $300,000,000 |

| Capital For Merchants | $220,000,000 |

| IOU Central | $163,000,000 |

| Credibly | $140,000,000 |

| Expansion Capital Group | $50,000,000 |

*Many reputable sources had published PayPal’s Working Capital lifetime loan figures to be approximately $200 million in early 2015, but just a couple months later PayPal blogged that the number was more than twice that amount at $500 million since inception. The print version of deBanked’s May/June magazine issue stated the smaller amount since it had already gone to print before PayPal’s announcement was made.

Lending Club Violated Securities Laws, Forced to File Rescission Offer

June 12, 2015Lending Club appears to have violated the securities laws of several states when it issued stock options as compensation between July 2012 and October 2014. According to an official Rescission Offer filed with the SEC on June 12th, Lending Club is offering to buy back both common stock shares and unexercised options to remedy their mistake. Combined, 40,469,837 shares of common stock are subject to the offer. Their reason for doing so is as follows:

We have issued shares of common stock or granted options to purchase shares to our current and former employees and consultants. From July 2012 through October 2014 (or during the periods specified on the addendum to this offering circular with respect to residents of certain states), the options we granted and shares issued upon exercise of the options may not have been exempt from the registration or qualification requirements under applicable securities laws.

The filing admits they violated the laws of at least 16 states and Puerto Rico.

For New York, it says, “We were required to apply for an exemption from the broker-dealer registration and securities issuance requirements with the State of New York to issue the shares and/or options to you without registration or qualification. Because of our failure to apply for an exemption, you have three years to seek a remedy for our failure to register.”

For New York, it says, “We were required to apply for an exemption from the broker-dealer registration and securities issuance requirements with the State of New York to issue the shares and/or options to you without registration or qualification. Because of our failure to apply for an exemption, you have three years to seek a remedy for our failure to register.”

For California, it says, “Certain options and shares issued pursuant to the 2007 Stock Incentive Plan may have been granted or issued in violation of the California Corporate Securities Law.”

The market price of the improperly issued shares amounts to $700 million. However, few if any shareholders subject to the rescission offer would likely accept it since it proposes buying back the shares at their original value + interest. Those values range from $0.06 to $8.94 per share. Lending Club closed today at $17.28, at double the highest proposed rescission offer price.

Indeed, no company officers are moving to accept the offer as it specifically states, “Seven of our officers and directors, who together hold 1,044,892 shares of common stock and options to purchase 11,081,780 shares of common stock, all of which shares are subject to this rescission offer, are eligible to participate in the rescission offer. We have been advised that these officers and directors do not intend to accept the rescission offer.”

Indeed, no company officers are moving to accept the offer as it specifically states, “Seven of our officers and directors, who together hold 1,044,892 shares of common stock and options to purchase 11,081,780 shares of common stock, all of which shares are subject to this rescission offer, are eligible to participate in the rescission offer. We have been advised that these officers and directors do not intend to accept the rescission offer.”

However, if the stock price were to drop by more than 50% between now and July 15th (the deadline to decide), the rescission offer would actually become in the money for a handful of investors. The odds of that happening are pretty slim.

Lending Club’s explanation for getting in this mess in the first place is as follows:

We became subject to the reporting obligations of section 15(d) of the Securities Exchange Act of 1934, as amended (Exchange Act) upon the effectiveness of our registration statement for our member payment dependent notes on Form S-1 on October 10, 2008. As a result, we were no longer entitled to rely on the qualification requirements pursuant to section 25102(o) of the California Corporate Securities Law. Because we could not rely on section 25102(o) of the California Corporate Securities Law, the options we granted and the shares issued upon exercise of these options during this period may have been issued in violation of California securities laws. In July 2014, we applied for a permit for qualification from the California DBO. In connection with the review of the permit application, the California DBO has required that we make this rescission offer to certain holders of any outstanding, unexercised options or shares of common stock issued upon exercise of stock options. Accordingly, we are making the rescission offer to the approximately 598 persons who received grants of options or purchased common stock upon exercises of options under the 2007 Stock Incentive Plan (except with respect to shares of our common stock which were subsequently sold by such persons at a price per share that exceeded the exercise price per share plus interest at the legal rate from the date of exercise, and therefore would exceed the amount of the rescission offer). If our rescission offer is accepted by all offerees, we could be required to make an aggregate payment to the holders of these options and shares of up to approximately $34.2 million, which includes statutory interest.