Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Should Alternative Lenders Reconsider IPOs?

August 31, 2015 OnDeck has gotten very quiet over the past month as the stock hovers near its all time low, and down more than 50% from its IPO price. The only updates related to them on the news wire lately are reminders from law firms to join in on the existing class action lawsuit. One has to wonder if they regret going public.

OnDeck has gotten very quiet over the past month as the stock hovers near its all time low, and down more than 50% from its IPO price. The only updates related to them on the news wire lately are reminders from law firms to join in on the existing class action lawsuit. One has to wonder if they regret going public.

To make the things murkier, the Madden v. Midland decision effectively makes it illegal in a handful of states for alternative lenders to rely on chartered banks to originate loans for them at interest rates that violate state usury laws. In states such as New York, that’s a big problem for OnDeck, but fortunately for them and other lenders like them, they can still fall back on a choice of law provision to still be able to make the loans.

Combine that landmark ruling with the Treasury RFI, The Dodd Frank Section 1071 Reg B rule that everyone wants enforced all of the sudden, and a chorus of lenders calling for regulatory action, and we don’t exactly have an ideal environment for other alternative lenders considering an IPO.

But does an IPO really matter?

I am reminded of a long email that Elon Musk sent to employees of SpaceX two years ago regarding their aspirations to go public so that they could monetize their stock options and get rich.

“Some at SpaceX who have not been through a public company experience may think that being public is desirable. This is not so.”

“Another thing that happens to public companies is that you become a target of the trial lawyers who create a class action lawsuit by getting someone to buy a few hundred shares and then pretending to sue the company on behalf of all investors for any drop in the stock price.”

“Public companies are judged on quarterly performance. Just because some companies are doing well, doesn’t mean that all would. Both of those companies (Tesla in particular) had great first quarter results. SpaceX did not. In fact, financially speaking, we had an awful first quarter. If we were public, the short sellers would be hitting us over the head with a large stick.”

“Public company stocks, particularly if big step changes in technology are involved, go through extreme volatility, both for reasons of internal execution and for reasons that have nothing to do with anything except the economy. This causes people to be distracted by the manic-depressive nature of the stock instead of creating great products.”

“It is important to emphasize that Tesla and SolarCity are public because they didn’t have any choice. Their private capital structure was becoming unwieldy and they needed to raise a lot of equity capital.”

“Those rules, referred to as Sarbanes-Oxley, essentially result in a tax being levied on company execution by requiring detailed reporting right down to how your meal is expensed during travel and you can be penalized even for minor mistakes.”

Any other alternative lenders possibly considering an IPO should strongly evaluate whether or not it’s necessary to go public to carry out their objectives. Surely the folks at OnDeck must be at least a little bit distracted by the manic-depressive nature of their stock price, the class action lawsuit, reactions to their quarterly reports, and the unyielding scrutiny by analysts and pundits. Surely it could be argued that they’ve lost some of their PR mojo in the mix.

It’s not easy running a public company, especially a lender in a post-financial crisis world where Wall Street hatred still runs hot. Hopefully if you are in this industry, you are in it for the long haul and not just for an IPO to cash out and give up…

Expansion Capital Group Crosses $50 Million Milestone

August 27, 2015 Move over New York and Silicon Valley, Expansion Capital Group (ECG), a young Sioux Falls, South Dakota-based business lender is quickly rising up the ranks. Founded just two years ago, a company representative has confirmed to deBanked that they’ve already funded more than $50 million to small businesses nationwide.

Move over New York and Silicon Valley, Expansion Capital Group (ECG), a young Sioux Falls, South Dakota-based business lender is quickly rising up the ranks. Founded just two years ago, a company representative has confirmed to deBanked that they’ve already funded more than $50 million to small businesses nationwide.

While South Dakota might be better known as the home state of Mount Rushmore, they have made a name for themselves in an industry largely centered around New York, California, and South Florida.

Jay Larson, ECG’s COO, shared with deBanked, “We are definitely excited to cross the $50 million deployment milestone. First and foremost, we’d like to thank all of our industry partners for all their help and support in getting us here. Second, this is only the beginning of ECG’s journey [and] as such we’re looking forward to reaching the $100M milestone in a much shorter period of time.”

On the industry leaderboard, ECG is not that far behind competitors that have been in the industry for much longer. Credibly, for example, has reportedly funded more than $140 million since inception but that’s spread out over a period of more than four years.

Business Financial Services Acquires Entrust Merchant Solutions

August 26, 2015 A representative for Coral Springs, FL-based Business Financial Services (BFS) has confirmed that the company has acquired Entrust Merchant Solutions. Entrust is a well established and widely known NY-based ISO/broker shop that was founded in 2007. As part of the deal, Entrust CEO Ilya Fridman will remain with the company and for the time being, the Entrust name will not change. They are now a part of the BFS family of companies however.

A representative for Coral Springs, FL-based Business Financial Services (BFS) has confirmed that the company has acquired Entrust Merchant Solutions. Entrust is a well established and widely known NY-based ISO/broker shop that was founded in 2007. As part of the deal, Entrust CEO Ilya Fridman will remain with the company and for the time being, the Entrust name will not change. They are now a part of the BFS family of companies however.

The news comes on the heels of a major milestone. Just a month ago, BFS announced that they had funded more than $1 Billion since inception, earning them a spot as one of the industry’s largest players.

The Entrust acquisition is representative of an M&A trend taking place in the industry. Below is a list of some of the more recent ones:

- Enova International acquired The Business Backer (for $27 million)

- Merchants Capital Access acquired Reliant Funding

- Capital Z Partners acquired Pearl Capital

- World Business Lenders acquired the business loan operations of Plan B Growth (and has made 11 acquisitions total over the past 12 months)

Prior to the deal, Entrust was an ISO for BFS. Over the last few days though, some insiders speculated that the relationship had suddenly grown even tighter. It turns out they were right.

Federal Reserve Publishes Results of Alternative Lending Focus Groups

August 26, 2015 Alternative lenders have a lot of work to do!

Alternative lenders have a lot of work to do!

In a study conducted by the Federal Reserve which included focus groups moderated by the Nielsen Company, small business owners that had not heard of online lenders or had not used them, expressed extreme skepticism about their legitimacy. Among the negative responses were words such as shady, scam, identity theft, high APRs, ridiculous, wild west and unregulated, among others.

The focus groups, while small, had to meet a minimum criteria to be eligible:

- Have 2 to 20 employees

- Have annual revenues between $200,000 and $2 million

- Be the financial decision maker

- Not be a new business

Only 44 people participated.

There were both bright and dark spots in the findings, with one of the bright spots being that people’s attitudes became more positive about online lenders once they started to actually navigate the websites of several big industry players.

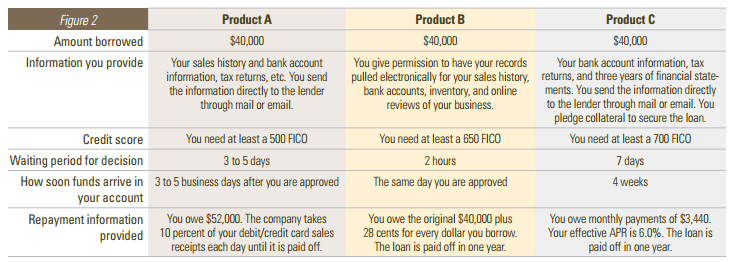

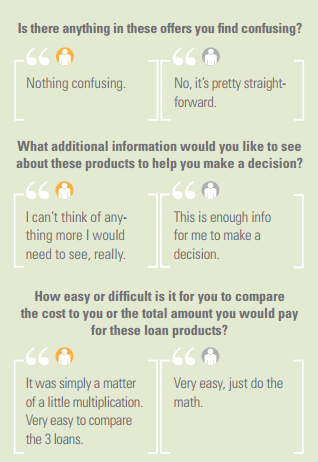

While the extent of the research is significant for any lender trying to get into the mind of a small business owner, there was a section in particular that warrants closer attention. In a mock comparison, participants were asked to compare three unnamed financial products, with one supposedly representing the characteristics of a merchant cash advance based on future credit card sales, another on a daily debit business loan, and the last a traditional bank loan.

Respondents generally reported that they understood these offers and were not confused by them.

Unfortunately, the researchers assigned some gut-wrenching characteristics to the structure of the product alleged to represent merchant cash advances (Product A).

The offer was a loan of $40,000 to pay back $52,000 in future credit card sales via a 10% processing split and participants were asked to guess the interest rate over one year. The question received all kinds of confused answers such as 5%, 9.8%, 15%, and others that made little sense.

The offer was a loan of $40,000 to pay back $52,000 in future credit card sales via a 10% processing split and participants were asked to guess the interest rate over one year. The question received all kinds of confused answers such as 5%, 9.8%, 15%, and others that made little sense.

Since the researchers presented the theoretical product as a loan, not a sale, they have potentially tainted the inferred conclusions about the transparency of future receivable transactions. Given the strong authority associated with the Federal Reserve and Nielsen, there is a troubling implication that the findings about a hypothetical loan could be used as a basis to make future regulatory decisions about unrelated products like receivable purchases.

Ironically, the diversity of wrong answers to the interest rate question could lead one to this conclusion though, that APRs wouldn’t necessarily be a transparency cure.

If business owners don’t understand what Annual Percentage Rates represent, then it might not be a very good medium to make comparisons. This argument is actually reinforced by the study’s own research since two of the three products were presented without the confusion of interest rates and “participants initially reported the three were easy to compare and that they had all the information they needed to make a borrowing decision.”

In regards to the traditional bank loan, one business owner is actually quoted as saying, “I am not sure what they mean by my ‘effective APR.'”

While value can be gleaned from the results of such a small sample size of 44 business owners, it’s obvious that the researchers influenced the participants answers on how they assessed the cost of merchant cash advances in particular.

- A transaction typically structured as a sale was presented to participants as a loan.

- A predetermined time frame of 1 year was provided to participants when they were asked about interest rates even though purchase transactions have no time frame.

The merchant cash advance product presented in the focus groups has just about no similarities to the purchase transactions that exist in real life.

What are your thoughts on this report and particularly the way merchant cash advance is framed in it? You can download the full report, including the focus group questionnaire here.

Some deBanked Swag to Go With Your Magazine

August 24, 2015Some lucky funders and ISOs will receive a Dunkin’ Donuts gift card along with their deBanked magazine shipment thanks to Lenders Marketing, a trigger lead company specializing in merchant cash advance and business loan leads. The gift cards are in limited supply and recipients are being selected at random.

A similar swag lottery took place with deBanked’s May/June issue where dozens of recipients received a Starbucks gift card with their magazines. Those were also courtesy of Lenders Marketing.

And in related news, pictured below in the green Lenders Marketing hat is professional golfer Michael McCabe during the PGA Tour Barracuda Championship in Reno, Nevada. Behind him to his left in the white hat with sunglasses is Justin Benton of Lenders Marketing.

Debt Settlement: A Partner to Alternative Lenders?

August 23, 2015 Call it the flip side of the coin, the part of the universe that helps consumers get out of debt, rather than take more on. Debt settlement, as it’s called, has a bit of a murky reputation thanks to a number of unscrupulous players that operated prior to the implementation of the Telemarketing Sales Rule in 2010.

Call it the flip side of the coin, the part of the universe that helps consumers get out of debt, rather than take more on. Debt settlement, as it’s called, has a bit of a murky reputation thanks to a number of unscrupulous players that operated prior to the implementation of the Telemarketing Sales Rule in 2010.

On October 27th, five years ago, for-profit companies that sold debt relief services over the phone could no longer charge a fee before they settled or reduced a customer’s unsecured debt.

“That law forever changed the industry for the better,” said a company representative at National Debt Relief (NDR), a New York City-based debt settlement firm.

Located right in front of the Bull at 11 Broadway, NDR occupies two floors and employs over four hundred people. And while it may seem that their business model is at odds with the dozens of loan brokers that operate in the neighborhood, they’re actually finding ways to work together.

“We’re monetizing their declines,” said a company representative. Indeed, alternative lenders like to talk about the amount of loans they can issue, but thousands of consumers are ultimately declined.

What those consumers do next and where they go is a storyline that doesn’t get much attention. NDR offers to the consumer an alternative route to become debt free in 36 months.

“NDR is enrolling thousands of consumers per month,” said a company representative. The A+ BBB rating and firm regulatory compliance has enabled them to land several strategic partnerships in this industry ranging from merchant cash advance com- panies to peer-to-peer lenders.

“NDR is enrolling thousands of consumers per month,” said a company representative. The A+ BBB rating and firm regulatory compliance has enabled them to land several strategic partnerships in this industry ranging from merchant cash advance com- panies to peer-to-peer lenders.

“We’ve found that 36% of declines from alternative lenders fit our criteria,” said a company representative. Too much debt is one obvious reason that applicants are getting declined from some of these companies in the first place. And to that end, NDR strives to provide them relief. One condition however is that the client not use credit while in the program.

NDR operates in 42 states and requires a minimum of $10,000 of unsecured debt to be eligible. They are also an accredited member of the American Fair Credit Council, a consumer credit advocacy association that touts the strictest code of conduct in the industry.

At the 2015 LendIt Conference in NYC, NDR stood out as a Gold Sponsor.

“Everybody wanted to know what we did,” said Michael Drehwing who was there as the company’s representative. “I told them we want to monetize your declines. How simple is that?”

Second Guessing Alternative Lending

August 21, 2015The best case scenario for the alternative lending industry is that every startup’s model is pure genius and all the founders’ assumptions are correct. To an extent, it kind of feels that way right now, that everyone’s riding this unstoppable growth train. I can barely go a half hour without getting an email alert telling me that yet another fintech player has raised millions to disrupt lending. The steady drumbeat of news validates ideas, concepts, and investments, and puts pressure on others to jump on board and join the party.

Meanwhile, industry conferences become self-reinforcing loops of assurance. They’re great places to hear what you already thought.

No, you’re brilliant!

No, you’re the brilliant one!

It’s incredibly easy to get caught up in it all. I am guilty of it myself sometimes. I know this because my pedestrian friends outside the industry have reacted to the investment opportunities in it with extreme skepticism.

“But isn’t this brilliant?!,” I ask them. Most are amused, but I’ve never convinced a pedestrian to invest in marketplace loans. They see flaws and risk all over it, and sometimes for reasons I hadn’t even considered. I compared these responses in my head with responses I’ve heard from industry professionals. Was the contrast in feelings reflective of differing philosophies? And do industry professionals just have more knowledge to think the way they do?

I had an epiphany when a colleague sent me a link to a short puzzle published on the NY Times website to see if I would arrive at the same conclusion that she did. I didn’t.

For the sake of fun and knowing what I’m talking about, you can take it here.

.

.

.

.

.

.

.

KEEP SCROLLING

.

.

.

.

.

.

.

.

.

.

.

.

KEEP SCROLLING

.

.

.

.

According to a sample, a mere 9 percent heard at least three nos — even though there is no penalty or cost for being told no. 78 percent never even got one no before they guessed the answer. “It’s a lot more pleasant to hear ‘yes’,” the research claims. “This disappointment is a version of what psychologists and economists call confirmation bias. Not only are people more likely to believe information that fits their pre-existing beliefs, but they’re also more likely to go looking for such information.”

The Times article is well…timely, because it’s possible there’s a running case of confirmation bias right here in the alternative lending industry. Nothing makes this more obvious than by the way Todd Baker ripped the industry to shreds in his August 17th article for American Banker. In Marketplace Lenders Are a Systemic Risk, he opens by writing, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

The Times article is well…timely, because it’s possible there’s a running case of confirmation bias right here in the alternative lending industry. Nothing makes this more obvious than by the way Todd Baker ripped the industry to shreds in his August 17th article for American Banker. In Marketplace Lenders Are a Systemic Risk, he opens by writing, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

The sobering viewpoint was immediately met with criticism, most notably by Mike Cagney, the CEO of SoFi. Cagney issued a direct response to Baker in own American Banker piece. Of Baker, he wrote, “While his intentions are good, his rationale is flawed.”

But whether or not you agree or disagree with what Baker wrote, he’s done the industry an enormous favor. He looked at it all and said “no.” According to the Times, “We’re much more likely to think about positive situations than negative ones, about why something might go right than wrong and about questions to which the answer is yes, not no.”

Keep that in mind when Baker wrote, “If an [Marketplace Lender] MPL can’t issue new loans — which will happen any time investors refuse to buy loans in the MPL marketplace — the transaction fees that are the MPLs’ main source of revenue and cash will instantly disappear, while expenses continue to mount. An MPL has to keep issuing loans to survive.”

Few people like to think about what would happen when or if investors refuse to buy loans. And when Cagney responds directly to this by saying, “The scenario he describes can’t happen,” one has to wonder if his rationale might be subject to confirmation bias. “If there is no buyer, MPLs simply stop lending,” he explained.

Rather than rebut Baker’s argument, he seems to confirm it. Without being able to issue loans, an MPL’s revenue will disappear, and therefore an MPL indeed has to keep issuing loans to survive. How else does an MPL stay in business if it stops lending?

Baker reminds us all that we have been here before. “When sentiment changes, the MPL investors’ rush to the exits will be no less swift than it was for traditional finance companies in 2007-8 or in the Russian and Asian debt crises of the late 1990s,” he writes. He alludes that large swaths of industry professionals have convinced themselves that things will be different this time even though history continues to repeat itself.

“There is too much money to be made before the inevitable blow-up,” he laments.

Baker’s opinion is one of the best pieces I have read about alternative lending this year, mainly because he was unabashed in his criticism. I’ve always believed that the best way to feel good about your decision is to hear a lot of reasons first about why you shouldn’t do something. Coincidentally, in the Times puzzle, I got nine nos before I felt confident about the game’s rule and successfully solved it. Only 9 percent of participants got three nos or more.

Baker’s opinion is one of the best pieces I have read about alternative lending this year, mainly because he was unabashed in his criticism. I’ve always believed that the best way to feel good about your decision is to hear a lot of reasons first about why you shouldn’t do something. Coincidentally, in the Times puzzle, I got nine nos before I felt confident about the game’s rule and successfully solved it. Only 9 percent of participants got three nos or more.

Nos are healthy and should be considered a welcome concept in this industry. Those working on credit models should remember that it’s not just about confirming your theories, but also about disproving them. Build your model and then try to destroy it. Test things that you think won’t work in addition to the things you think will work. Go out there and break things. Run worst case scenarios. Fund money to a deal that you think will go bad. See what happens.

“Often, people never even think about asking questions that would produce a negative answer when trying to solve a problem — like this one. They instead restrict the universe of possible questions to those that might potentially yield a ‘yes’,” says the Times. This flawed approach could lead to catastrophe.

In The Quants: How a New Breed of Math Whizzes Conquered Wall Street and Nearly Destroyed It, odd scenarios not accounted for in computerized trading models led to disastrous losses. At times, the quants’ computers refused to acknowledge events that were actually happening because the built-in models believed they were too statistically impossible.

So when SoFi’s Cagney says, “the scenario [Baker] describes can’t happen,” in regards to the potential of an MPL failing because there are too few loan buyers, it should be taken with a grain of salt. Of course it can happen.

But it should also be mentioned that SoFi is now worth about $4 billion. That means that in a room full of alleged geniuses, Cagney is a certifiable genius. But there’s no way someone in his position would raise a fresh billion dollar round of capital and then concede to American Banker that the whole system could be torn to shreds at any moment.

The danger is that others will point to Cagney as validation that their own lending aspirations are viable even when their own models and market positioning are substantially weaker. Not every new lending startup CEO is Mike Cagney. And there is plenty of truth in Baker’s opening line, “Once again the markets have fallen in love with a group of young, aggressive and not very regulated lenders.”

A lot of arguments have been put forth about why everything is different this time, that it is impossible to fail, but we may find out just as we have countless times before that this isn’t the case.

It’s refreshing to hear someone second guess the whole industry. Hopefully if you’re a player in this space, you’ve thought of reasons why your business might be flawed. If you’re like 78% of the population that’s too scared to even get one no before committing to an answer, you’re probably in big trouble…

Will You be at Lend360?

August 20, 2015This year’s Lend360 conference in Atlanta, GA is shaping up to be one of the industry’s biggest events. A welcome respite for some from the typical trek out to New York, San Francisco, and Las Vegas, the show is being hosted in the same neighborhood as industry leaders CAN Capital and Kabbage.

Just take a look at the speaker lineup so far:

You can register here. Hope to see you there!