Sean Murray is the President and Chief Editor of deBanked and the founder of the Broker Fair Conference. Connect with me on LinkedIn or follow me on twitter. You can view all future deBanked events here.

Articles by Sean Murray

Fundry’s Isaac Stern Hosts Successful Fundraiser for Hatzalah of Union County

December 6, 2015 ‘Tis the season of giving for Fundry’s Isaac Stern and the dozens of folks that attended the December 5th winter fundraiser at his home in Hillside, New Jersey. The event, which served up 550 pounds of barbecue and included a Scotch taste testing bar hosted by representatives of Glenfiddich, raised over $60,000 for Hatzalah of Union County, a local non-profit all-volunteer emergency medical service organization.

‘Tis the season of giving for Fundry’s Isaac Stern and the dozens of folks that attended the December 5th winter fundraiser at his home in Hillside, New Jersey. The event, which served up 550 pounds of barbecue and included a Scotch taste testing bar hosted by representatives of Glenfiddich, raised over $60,000 for Hatzalah of Union County, a local non-profit all-volunteer emergency medical service organization.

Founded in 2004, Hatzalah EMS provides basic life support in medical emergency situations. They cover Union County NJ including the towns of Elizabeth, Hillside, Union, Roselle and Linden. Today, Hatzalah is staffed with 3 ambulances, 24 EMTs and 18 dispatchers all under the medical direction of a physician and two paramedics.

Hatzalah Chief Yudi Abraham told deBanked that Yellowstone Capital (a Fundry subsidiary) has been a long-time supporter of their organization. A few years ago, when the squad was undergoing a transition of directors, Chief Abraham reached out to Isaac Stern for financial help. At the time, Hatzalah was in serious need of replacing an older ambulance as well as covering monthly operating expenses. “Isaac didn’t waste any time and sprang right into action,” says Chief Abraham. “He immediately convened his employees and his associates and came through for us in a huge way.” Yellowstone Capital raised the funds in under two days for Hatzalah to buy a fairly used ambulance. Ever since then, Stern and Chief Abraham have been working closely together to ensure that other expenses were covered. Over the years, Yellowstone Capital has helped donate the funds to purchase two additional ambulances that currently make up Hatzalah’s fleet. The Yellowstone Capital name appears on the side of each of them.

The most recent event kicked off with a $10,000 personal donation from Stern, prompting others to give too while enjoying the festivities.

“With the help of Yellowstone Capital we are able to maintain our level of service and continue providing the best possible emergency care for our patients,” said Chief Chaim Cillo. “We at Hatzalah will forever be most appreciative for such an incredible company that cares and gives back to the community in such a large way.”

Stern and Yellowstone were also presented an award for their continued generosity.

Chief Yudi Abraham (left) and Fundry CEO Isaac Stern (right)

Chief Yudi Abraham (left) and Fundry CEO Isaac Stern (right)In attendance at the event were Fundry employees, friends, family members, and others from the non-bank finance industry.

From left to right: Andrew Hernandez of Central Diligence Group, Sean Murray of deBanked, and Andy McDonald of Yellowstone Capital/Fundry

From left to right: Andrew Hernandez of Central Diligence Group, Sean Murray of deBanked, and Andy McDonald of Yellowstone Capital/Fundry

Michael Samuels (left) and Steve Weinrib (right) both of Yellowstone Capital/Fundry

Michael Samuels (left) and Steve Weinrib (right) both of Yellowstone Capital/FundryHatzalah means “rescue” or “relief” in Hebrew and for many guests the event fell on the eve of the Hanukkah holiday. The volunteer EMS crew of course helps all people in need of care.

“Our pay,” said Chief Abraham, “is helping our patients and saving lives.”

Lending Club Borrower Exceeded 5 Credit Inquiries | Investors Raise Eyebrows

December 5, 2015 Unblinking investors on the Lending Club marketplace called attention to an anomaly through the LendAcademy forum two weeks ago. At issue was a borrower whose profile reportedly had 9 recent credit inquiries, which exceeded Lending Club’s maximum eligibility to even be listed. As the prospectus of each loan stipulates “5 or fewer inquiries (or recently opened accounts) in the last 6 months,” investors wondered how somebody with 9 had slipped through the cracks.

Unblinking investors on the Lending Club marketplace called attention to an anomaly through the LendAcademy forum two weeks ago. At issue was a borrower whose profile reportedly had 9 recent credit inquiries, which exceeded Lending Club’s maximum eligibility to even be listed. As the prospectus of each loan stipulates “5 or fewer inquiries (or recently opened accounts) in the last 6 months,” investors wondered how somebody with 9 had slipped through the cracks.

But it wasn’t just one, user Fred revealed that this was a very common occurrence. “In my database of LC loans collected so far, I saw 1000+ loans with 6+ inquiries in the last 6 months,” he wrote.

Concerned, somebody reached out to Lending Club to find out what the deal was.

The response they got back was that auto or mortgage inquiries do not count as inquiries in their underwriting. However, their system had glitched and was inadvertently including them. That meant the borrower showing 9 inquiries did indeed have 9 but 4 of them were auto and mortgage related and therefore weren’t subject to the cap of 5.

While car loans and mortgages might not be as relevant to unsecured consumer debt activities, it is interesting that these inquiries are supposed to be glossed over in the total inquiries revealed to potential investors.

For instance, in this case, a borrower with approximately 720 credit earning $73,000 a year has 11 inquiries but for all points and purposes, Lending Club is only counting up to 5 of them. They were seeking a $29,175 personal loan for “business purposes.” The loan was eventually removed for reasons unknown.

For those buying these notes, as always, buyer beware.

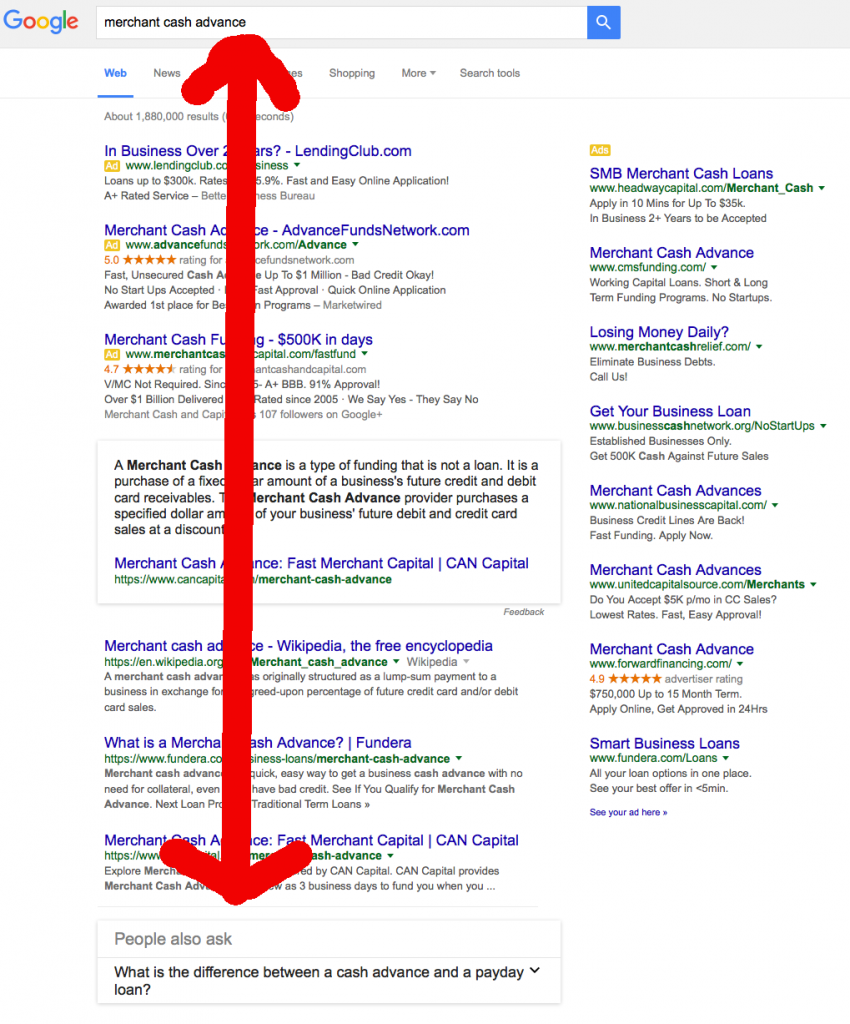

Google Serves Low Blow to Merchant Cash Advance Seekers

December 2, 2015 Almost eighteen months ago, I explored whether or not Google was rigging the search results to benefit two lending companies they had equity investments in, Lending Club and OnDeck. At the time, both companies ranked at the top for highly coveted keywords even if they weren’t directly related to the user’s search query.

Almost eighteen months ago, I explored whether or not Google was rigging the search results to benefit two lending companies they had equity investments in, Lending Club and OnDeck. At the time, both companies ranked at the top for highly coveted keywords even if they weren’t directly related to the user’s search query.

Now that those two companies are public, a company called Credit Karma seems to have inherited the top spots. And wouldn’t you know it, Google has also invested in them.

Google: loans

Google: personal loan

But that’s not the worst of it. Thanks (or no thanks rather!) to a relatively new search result feature called “People Also Ask,” one keyword recently started serving up results with a different kind of hidden agenda.

While my captured results may not be identical for everyone, I have conducted tests with other people on other devices and from other areas and it was present each time. With this box, Google is subtly planting the negative seed that payday loans and merchant cash advances are basically so identical that other people just like you are wondering what the difference between the two are. But here’s the rub, the two have nothing to do with each other and it’s unlikely so many people are asking that.

Pay no mind to the fact that the box makes reference to a “cash advance” not a “merchant cash advance.” The painstaking mishap could be innocently chalked up to an algorithmic error if only googling just cash advance revealed the same box in the results. But it doesn’t. Only merchant cash advance brings this up.

Comparing merchant cash advances to payday loans is straight out of the anti-merchant cash advance propaganda playbook. At least one Google-owned business lending company is actively lobbying against short term business lending and merchant cash advances in Washington so the placement and comparison of the People Also Ask box in their results is highly suspicious.

It’s no secret that Google is also directly lobbying in the online lending space too. One month ago, right before Google magically started to suggest to searchers that merchant cash advances and payday loans were related, Google formed a lobbying organization called Financial Innovation Now with Amazon and Apple. On their main agenda is online lending.

Given the suspicious search rankings for companies they have an equity stake in, I would not doubt for a second that something like this was manually inserted. I admit that my evidence and my case are weak, but given the circumstances, it’s quite possible there’s something deliberate happening here.

What do you think? Do you see this when you google merchant cash advance?

Funding Circle’s Sam Hodges Comments On OnDeck/JPM Announcement (Video)

December 2, 2015Earlier today, Funding Circle’s Sam Hodges appeared on Bloomberg TV to discuss the new OnDeck/JPMorgan Chase announcement. Hodges said he believes its the first step towards many banks working with marketplace lenders and reminded the panel that in the UK, his company already does that.

He was then asked if such a tight relationship even makes sense given the overwhelming consumer sentiment against banks these days. Watch what the video and how he responds below:

JPMorgan Chase and OnDeck Partner Up

December 1, 2015 Coming soon, when small businesses apply at a Chase bank for a loan under $250,000, there’s a good chance that OnDeck will be doing all the work. That’s because JPMorgan Chase and OnDeck announced a strategic partnership earlier today that is expected to commence in 2016.

Coming soon, when small businesses apply at a Chase bank for a loan under $250,000, there’s a good chance that OnDeck will be doing all the work. That’s because JPMorgan Chase and OnDeck announced a strategic partnership earlier today that is expected to commence in 2016.

A comment earlier in the day by Jamie Dimon hinted that something was coming. “We haven’t announced it yet, we’re going to be doing a thing with one of these peer-to-peer, small-business lenders,” Bloomberg reported.

That caused peer-to-peer lending industry advocates like Peter Renton of LendAcademy to speculate who that might be. He originally bet on Lending Club but posited that it could also be OnDeck, Funding Circle, or Kabbage.

When I asked Lending Club on twitter if they were slated to be JPM’s partner, I received a public reply back from a VP at OnDeck saying that it would in fact be them. By then the news had already been released.

The SEC filing states, “JPM will use the Company’s small business lending platform and the OnDeck Score® to serve its small business customers” and adds that they’re still in the process of building things out and finalizing agreements.

OnDeck (ONDK) which closed at $9.01 before the announcement is expected to soar on the news for the Wednesday open.

deBanked Nov/Dec Teaser

December 1, 2015The November/December issue of deBanked Magazine should go out in the mail at the end of this week. In the meantime, can you guess who is on the front cover of this issue?! Here’s your clue:

Jared Weitz, the CEO of United Capital Source, was on the cover of the previous September/October issue.

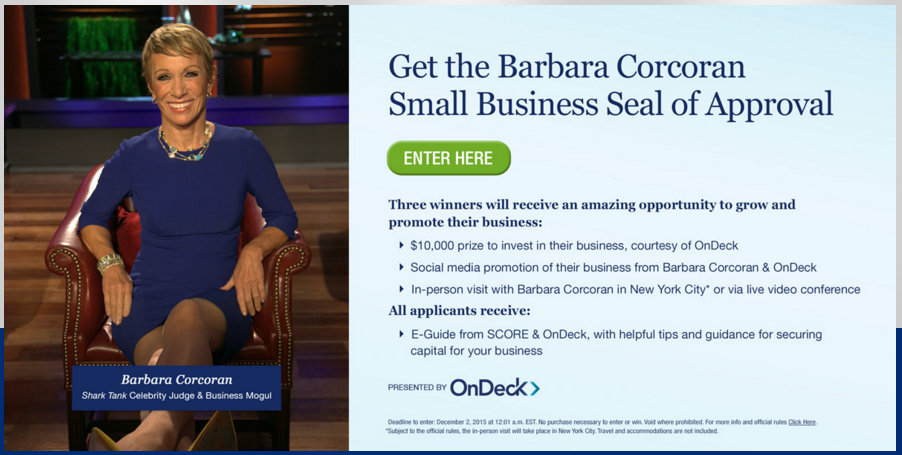

Shark Tank’s Barbara Corcoran Teams Up With OnDeck for Small Business Contest

November 29, 2015 Barbara Corcoran, co-founder of The Corcoran Group and famous Shark Tank investor, has teamed up with small business lender OnDeck to support entrepreneurs through a contest. Three winners will be chosen for a $10,000 prize and they’ll also get to meet Barbara Corcoran.

Barbara Corcoran, co-founder of The Corcoran Group and famous Shark Tank investor, has teamed up with small business lender OnDeck to support entrepreneurs through a contest. Three winners will be chosen for a $10,000 prize and they’ll also get to meet Barbara Corcoran.

Contest applicants are asked to enter what they would spend the $10,000 on to grow their business. The deadline to enter is December 2nd, 2015.

The partnership is significant because it marks yet another time that a Shark has crossed paths with online business lenders. Just one year ago, Kevin O’Leary became a spokesperson for IOU Financial.

I'm thrilled to announce a new partnership between O'Leary Financial & @IOUCentralInc this morning! http://t.co/ECJl1K5ZUC #smallbusiness

— Kevin O'Leary (@kevinolearytv) October 2, 2014

Also around that time, Kevin Harrington, an original Shark Tank investor before Mark Cuban or Lori Greiner, co-founded his own small business lending marketplace, Ventury Capital. Straight out of the OnDeck or merchant cash advance playbook, Ventury’s FAQ says their system “deducts a fixed, daily payment directly from your business bank account each business day.”

Watch Kevin Harrington explain his company here:

Of course there was the time that a merchant cash advance company (Total Merchant Resources) actually went on Shark Tank and pitched the sharks…

It seems that the show and the real world have a lot in common.

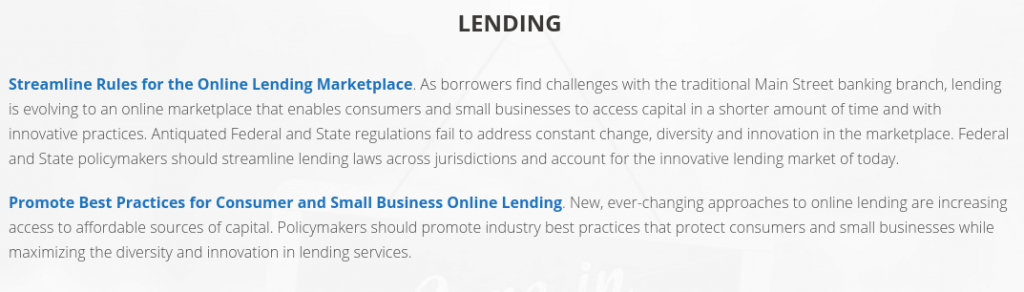

Will the Wild West of alternative lending stay that way?

November 24, 2015Comments on the regulatory future of alternative lending were included in a joint report prepared by Lendio and Dealstruck:

Blake hopes that governing agencies will offer reasonable policies that will encourage best-in-class business practices (to weed out the bad actors) without damaging the innovation and growth in the industry. Furthermore, Lendio highly recommends that any new or additional regulations come from the Federal level, rather than through a state-by-state patchwork of laws that will impose inconsistent and costly regulations on the online lenders.

– Brock Blake, Lendio CEO

Thoughtful regulation to ensure operators are performing with honesty and transparency is a good thing. And good players are stepping up to the plate to take a proactive stance regarding fair and transparent lending practices, executed ethically and with integrity. Fortunately for the small business lending market, the key lenders and marketplaces in the industry have used a blueprint of best practices that were established and implemented in the consumer lending space. It’s fascinating to think about how much room they have left to grow.

– Ethan Sentura, Dealstruck CEO

The report compiles other interesting pieces of data such as OnDeck’s share of the entire business loan market, which stood at less than a quarter of 1% just 1 year ago.

You can view Lendio and Dealstruck’s full report here.