Articles by deBanked Staff

SEC Says You Can Crowdfund Startups This Summer

February 23, 2016Now you can own a piece of a startup doing the next-big-thing or invest seed money in an idea that looks promising starting May this year.

Last week, the SEC released an investor bulletin on crowdfunding for retail investors and said that “Starting May 16, 2016, companies can use crowdfunding to offer and sell securities to the investing public.”

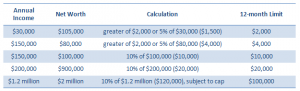

In October last year, the regulator adopted rules permitting companies to offer securities and raise a maximum of a million dollars a year through crowdfunding platforms. Individual investors with annual income or net worth less than $100,000 can invest no more than $2,000 but less than 5 percent of their annual income and not more than 10 percent for investors with income and net worth of over $100,000 in a twelve-month period.

Investors are allowed to invest in these ventures strictly through an online platform including mobile app of a broker-dealer or a funding portal registered with the SEC and a member of FINRA.

This is a major step in recognizing crowdfunding as a legitimate means of raising capital, which thus far has been typically used to solicit charitable donations or raise funds for artistic projects like movies, music and social projects.

The SEC warned investors of the risks involved with such investments like limited disclosure, illiquidity, opacity in valuation and capitalization that is associated with private companies. Investors are also prohibited from reselling their stake for the first year unless it’s a transfer to the company, an accredited investor or a family member.

China: New Regulator In, Stocks Up

February 22, 2016 Chinese stocks got a much-needed respite and traded at a four-week high after the country ousted the head of its securities regulator, China Securities Regulatory Commission (CSRC) Xiao Gang amidst a volatile stock market. Gang will be succeeded by Liu Shiyu, former deputy governor of the central bank and chairman of the Agricultural Bank of China.

Chinese stocks got a much-needed respite and traded at a four-week high after the country ousted the head of its securities regulator, China Securities Regulatory Commission (CSRC) Xiao Gang amidst a volatile stock market. Gang will be succeeded by Liu Shiyu, former deputy governor of the central bank and chairman of the Agricultural Bank of China.

The Shanghai Composite was down 18 percent within the first two weeks of this year and 40 percent since last year. And twice in a week, last month the Chinese stock market traded only for 29 minutes after the CSI 300 Index fell 7 percent.

The slump on stock markets is an amalgam of various factors like a weakening renminbi, slowing down of manufacturing activity and China’s slow transition to a consumption-led economy.

All signs point to drying up of capital in the country. China News Service last week reported a decline in the number of P2P lenders following the Ezubao Ponzi Scheme where marketplace lenders swindled $7.6 billion from investors.

Chinese lender Yirendai closed 0.73 percent up.

Loan Brokers or Self Origination? Here’s What Experts Say

February 22, 2016 Last year belonged to the brokers in alternative finance — with a phone and a few leads pulled up online, anyone could sell a loan. With seemingly no barriers to entry, alternative lending attracted auto and insurance salesmen fleeing their jobs to cash in on the gold rush in an economy which was coming out of the shadows of distrust for big banks. And it found quick ascension to grow into a trillion dollar market.

Last year belonged to the brokers in alternative finance — with a phone and a few leads pulled up online, anyone could sell a loan. With seemingly no barriers to entry, alternative lending attracted auto and insurance salesmen fleeing their jobs to cash in on the gold rush in an economy which was coming out of the shadows of distrust for big banks. And it found quick ascension to grow into a trillion dollar market.

But a year on, as the dust has settled, we asked industry veterans what it means to remain successful in this business and what is the key to sustainability — is it in going for the ISO/broker channel to find deals or originating your own.

Here’s what they had to say

Don’t Break the Broker

Tom Abramov of MFS Global voted for the ISO/broker channel and said that that’s how the company strictly does deals, working with brokers who have a track record as a part of their recruitment system. The six year old company that started as an broker shop now focuses only on funding with products that are a mix of merchant cash advances and lines of credit.

“We don’t look at FICO scores or SIC codes, we only look at cash flows of businesses,” said Abramov. “I want to see if I give a someone a dollar whether they can turn it into two.”

Abramov added that his firm offers brokers 20 percent commission and their default rates are sub 5 percent.

The advantages of scoring deals through a broker channel can be alluring. It involves no overhead, no staff that needs compensation, motivation and incentives, and makes use of the existing broker-merchant relationships.

Jordan Feinstein of NuLook Capital said that his firm works with brokers exclusively and the model has helped them respond to merchants faster. “We do not have a sales team speaking to merchants directly, that’s in conflict with our model,” said Feinstein. “We decided that the best way to grow is to build relationships to avoid the overhead, compliance, training and manpower that a sales team would require,” he said.

Building a Hybrid Model

There are some others who want to make the best of both the models and work with brokers while originating and funding their own deals. Forward Financing which uses a hybrid model has strategic partnerships with some brokers while still originating their own deals. “We have a hybrid model because our goal is to have a program for any type of business and work with companies across the spectrum of risk,” said Justin Bakes, CEO of Forward Financing. “While our priority is to self originate, it is essential to create and maintain partnerships in this business,” he said.

The Original Origination

While the allure of a lean business is certainly attractive, there are some who are in the industry to build a bigger business and create value by making it robust — Jared Weitz of United Capital Source is one of them. “There is a big market for both analytical process as well as sales process. It’s important to go after your strength,” said Jared Weitz, founder and CEO of United Capital Source. “When you originate and fund your own deals, you’re in a rewarding position and in control of how merchants get treated.”

Industry Trends

Speaking of the industry in general, these experts agreed that the business was undergoing a change with new entrants coming in and experimenting with better services and technologies.

“Last year was the year of brokers but we are still missing the education with merchants. Some brokers are interested while some are not,” said Abramov.

“I notice a clear difference between the old and the new in terms of technology and pricing model,” said Bakes.

“New funders are coming in with different products and terms with increased competition in the ISO market,” said Feinstein.

“Marketing is getting more expensive and only the ones who can afford to pay can play,” said Weitz.

Square Goes Back To The Drawing Board, Ahead of First Earnings

February 19, 2016 Square is bracing for its first milestone as a public company – its first earnings report.

Square is bracing for its first milestone as a public company – its first earnings report.

On March 9th, the payments company will present a scorecard of how it’s doing and what that means for its investors. Visa picking up a 10 percent stake in the company came as a respite for the stock which has generated close to 27 percent losses since its IPO.

But that might not be enough to prove that the seven year old company is in a sustainable business. Square has to prove that it is all a small business needs. From capital, payroll to point-of-sale, Square wants to be the one stop shop for small merchants, not relying entirely on its payments business which makes up 95 percent of its revenue.

When the company started in 2009, its strategy was to go after micro merchants that were too fragmented and small for bigger payments companies. Square started by giving these merchants a dongle to accept card payments for a flat fee. While the idea was to serve an untapped market, the company could not be shielded from the risks that these merchants bring to a business with their heterogeneity, fragmentation and smaller deals.

But ahead of its first earnings call, the company is ramping up its efforts towards bringing more businesses into its fold. Forbes reported that Square expanded its payroll product to merchants in Tennessee, New Hampshire, Nevada, South Dakota, and Alaska in addition to the existing markets of California, Texas and Florida allowing them to serve 30 percent of independent businesses in the U.S.

SEC Committee To Examine Capital Raised By SMEs

February 18, 2016The Advisory Committee on Small and Emerging Companies at the SEC announced they will meet next week (February 25th) to examine the capital raised in “unregistered securities offerings”

The committee provides a mechanism for the regulator to receive recommendations on small enterprises, both public and private with a market cap of less than $250 million. Stephen M. Graham, Managing Partner of Fenwick & West LLP’s Seattle office, and Sara Hanks, CEO of CrowdCheck will serve as co-chairs of the committee.

“Small businesses play a crucial role in our nation’s economy,” said SEC Chair Mary Jo White. “The advisory committee members have a wealth of experience and ideas that will help inform the Commission on the many important issues affecting small and emerging businesses.”

Want to Avoid Another Crisis? Break Up The Banks, Fed Official Says

February 16, 2016 How to avoid another financial catastrophe?

How to avoid another financial catastrophe?

Breaking up the big banks is one solution, according to the newly-appointed Minneapolis Fed chief, Neel Kashkari.

Pushing for a radical shakeout in corporate banking, Kashkari on Tuesday urged Congress to ensure that banks hold enough capital to not fail. The former investment banker with Goldman Sachs said the post-crisis regulation, Dodd-Frank is limited and does not go far enough in safeguarding against the ‘Too Big To Fail’ (TBTF) risk.

“Now is the right time for Congress to consider going further than Dodd-Frank with bold, transformational solutions to solve this problem once and for all,” he said.

As a part of this bold transformation, Kashkari proposed options such as breaking up the big banks into “smaller, less connected, less important entities,” taxing leverage to reduce systemic risks and turning banks into public entities by forcing them to hold large amounts of capital.

Kashkari joined the Treasury in 2006 and headed the Troubled Asset Relief Program and managed banking and auto bailouts during the crisis. He also ran for Governor of California in 2014 as the Republican candidate but lost to the incumbent Jerry Brown.

He took over at the Minneapolis Fed in November last year and plans to develop an actionable plan to end TBTF to be delivered by the end of this year.

“Doing everything we can to address the systemic risks posed by large banks will be an important step to fulfilling that mission,” Kashkari added. “Seven years after the crisis, I believe it is now time to move forward and end TBTF.”

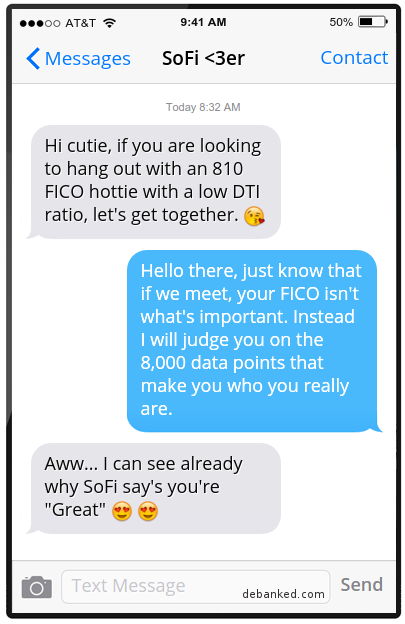

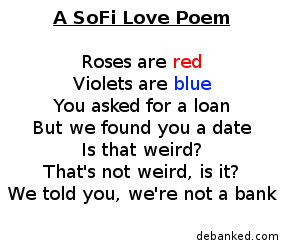

SoFi Dating App Will Take On “Loanly-ness” (Here’s How That Might Look)

February 16, 2016SoFi is apparently serious about creating a dating app for their members. That might seem a little weird considering they’re a company known for refinancing student loans. But according to Inc, Claire Arthurs, SoFi’s Director of Community and Member Success, is planning events in the nation’s big cities to bring singles together. And it’s all because their borrowers are demanding it. Eighty-six percent of attendees at an initial small event said they wanted to meet someone from the event again, Arthurs said to Inc.

Meanwhile, most listeners to SoFi’s CEO Mike Cagney on the re/code decode podcast undoubtedly assumed he was joking about a dating app. But now, rumor has it that they may actually release such an app later this year.

Naturally, deBanked saw this as an opportunity to offer our thoughts on how the SoFi dating experience might play out:

When literally nothing else has worked for your love life

For late night liaisons

If you’re old fashioned

When it’s more than just looks

When you’re trying to be romantic

—–

We hope you enjoyed them.

After CEO Exit, California State Probes Zenefits

February 12, 2016 The California Department of Insurance will investigate the San Francisco-based human resources software startup Zenefits after the exit of its head Parker Conrad earlier this week, amidst a regulatory compliance scandal.

The California Department of Insurance will investigate the San Francisco-based human resources software startup Zenefits after the exit of its head Parker Conrad earlier this week, amidst a regulatory compliance scandal.

Zenefits sells cloud-based human resource software for payroll, talent management and health insurance. The startup, founded in 2013, was touted to be one of the fastest growing companies in Silicon Valley with marquee investors like Andreessen Horowitz, Institutional Venture Partners and Fidelity Management.

The company, valued at $4.5 billion, let health insurance reps fake the mandatory 52-hour training course that is legally required to sell insurance. “After they faked the training course, sales reps were directed to sign a certification, under penalty of perjury, that they had spent the required 52 hours doing the work,” according to Buzzfeed News.

California Insurance Commissioner Dave Jones, in a statement, revealed that the department started probing Zenefits last year. “The recent resignation of Zenefits’ CEO Parker Conrad is an important development, but it does not resolve our ongoing investigation of Zenefits’ business practices and their compliance with California law and regulations,” said Jones.

The company’s COO David Sacks (pictured at right) has replaced Conrad as the CEO.

The Zenefits scandal brings to light Silicon Valley upstarts’ tendency to play fast and loose with regulation and compliance.